ABC Lateline carried a segment featuring BrickX, which can either be seen as an innovative way to facilitate housing affordability, or the ultimate in the financialisation of property. You decide!

Digital Finance Analytics (DFA) Blog

"Intelligent Insight"

ABC Lateline carried a segment featuring BrickX, which can either be seen as an innovative way to facilitate housing affordability, or the ultimate in the financialisation of property. You decide!

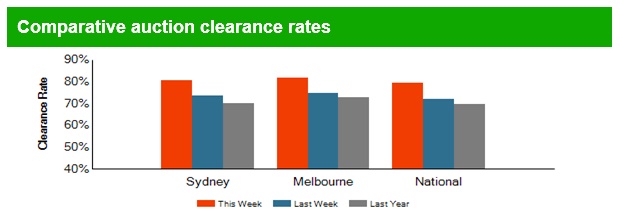

The combined capital city preliminary clearance rate rose to 76.9 per cent this week, increasing from last week, when final results saw the clearance rate fall to 69.8 per cent after 10 consecutive weeks remaining in the mid-70 per cent range. The rebound in the preliminary clearance rate has occurred against a backdrop of higher auction volumes, with 2,347 properties taken to auction across the combined capital cities, up from last week’s 1,751, however lower than one year ago (2,675). The higher clearance rate and increase in volumes this week were attributable to stronger results across the two larger auction markets of Melbourne and Sydney, with performance across the remaining capitals remaining varied over the week.

Considering the slowdown in auction markets over previous weeks as well as widespread speculation that the housing market is moving through its peak, the final auction clearance rate, published by CoreLogic on Thursday, will be an important follow up to this strong preliminary result.

The federal government may be poised to unveil a special savings account and tax breaks for first home buyers in next week’s budget, despite government ministers refusing to confirm leaked reports in the media at the weekend.

With the housing affordability crisis close to the top of voter concerns, the federal Treasurer last week appeared to change focus from the housing sector to infrastructure, but those hoping to get into the housing market will be encouraged to hear the issue may be tackled, if in limited form only.

Reports suggested that Treasurer Scott Morrison’s upcoming budget would feature a provision allowing aspiring first home buyers to salary sacrifice in order to raise their needed deposits.

If that is true, it will be a case of back to the future, as a similar measure was introduced during Kevin Rudd’s first turn as prime minister before being scrapped by the Abbott government.

While Resources Minister Matt Canavan would not deal in specifics during a Sky News interview on Sunday, he stressed that home ownership would be a key theme of the upcoming budget.

“We are focused on making sure Australians can afford a home,” he said. “It is a fundamental principal.”

Under the Labor scheme, First Home Saver Accounts saw the government make co-contributions of up to $1020 (or 17 per cent) on the first $6000 that account holders deposited each year.

While there were tax concessions associated with the accounts, there were also restrictions around access to the funds, including that they were only to be used towards payment for first homes.

That scheme proved to be something of a disappointment. While Labor treasurer Wayne Swan predicted as many as 750,000 accounts would be established, only 46,000 had been opened when his successor, Abbott-era treasurer Joe Hockey, wound it up six years later in 2014.

And there was no shortage of critics, including the consumer group CHOICE, which complained in a submission to Treasury that it provided disproportionate assistance to high-income earners while doing little to help those who genuinely needed it.

“We are unaware of any evidence to suggest that sufficient savings are more difficult to achieve for higher-income earners,” CHOICE noted sarcastically.

Another criticism came from Treasury itself, which warned that the scheme as initially conceived would be complex to administer while not benefitting those on low incomes.

If the Turnbull government is indeed planning to revive home-saver accounts or something similar, the one near-certainty is that government contributions and associated tax breaks will need to be far more substantial if they are to have a positive impact than under Labor, when house prices were substantially less.

According to the Australian Bureau of Statistics, the national average home price rose a staggering 4.1 per cent in the last quarter of 2016 alone, and 7.1 per cent for the year.

Despite First Home Saver Accounts being in effect for six years, Labor frontbencher Mark Butler insisted on Sunday that they had not had time to work – and, if something similar were to be re-introduced, it wouldn’t do much good anyway.

“The critical message is this,” he told the ABC’s Insiders, “you cannot deal with housing affordability in Australia without dealing with negative gearing.”

Greens senator Sarah Hanson-Young also rejected the notion that salary sacrificing would have a major effect.

“We have to bring the pressure down, not just give people more money to go straight into the hands of property investors.”

There’s been quite a bit of speculation over whether Australia has a property market bubble – where house prices are over-inflated compared to a benchmark – and when it might burst. According to housing experts, there’s at least four scenarios where this could happen.

Australia could see a property bubble burst due to:

These four scenarios focus on different tension points in Australia’s and the global economy. One scenario focuses on the balance of actions between regulators like APRA and the Reserve Bank, combined with household mortgage stress. Another envisions the affect that unemployment might have in certain areas.

Some of the factors we may see play out, such as the federal and state government trying to intervene to “fix” problems in the market, as happens in one scenario. But other factors may be out of the government’s control, for example, where a global crisis pushes up risk premiums.

All of these scenarios highlight just how complicated and interrelated the steps that lead to a property bubble burst could be.

Associate Professor Harry Scheule, UTS Business School

Following concerns of the housing bubble, bank regulator APRA increases bank lending standards, it also increases the risk weight on Australian mortgages resulting in lower loan supply and higher loan costs. Banks are encouraged to reduce interest-only loans, hold a greater amount of costly capital (making home loans more expensive) and reduce the loan amounts offered to applicants due to higher future interest scenarios.

Following increases in interest rates in the US and Europe, as those markets recover, the Australian dollar begins to decline – forcing the Reserve Bank of Australia (RBA) to increase interest rates.

Higher interest rates lead to higher monthly repayments, as most of Australia’s home loans are adjustable. Interest only loans are the most exposed. Higher interest rates also lead to more mortgage delinquencies.

The banks tighten bank lending standards in response to the increase in delinquencies. This further constrains interest-only borrowers seeking to refinance after the end of the interest-only terms. This means more mortgage stress, as many had expected to roll over the interest-only period indefinitely, but now they are forced to make principal repayments next to interest payments.

The cycle between delinquencies and tightening bank lending standards continues and as a result there’s a noticeable drop in loan supply and a fall in house prices.

Danika Wright, Lecturer in Finance, University of Sydney

Unemployment and underemployment – workers who want to work more but can’t – increase. As the apartment development boom dies down, and without a mining boom to replace it, construction industry workers are at high risk.

Households with a lot of mortgage debt are forced to limit their spending, particularly on discretionary items. This in turn affects companies that employ retail workers, reducing hours and employment.

Employment opportunities are a major component of house price amenity, in part because demand for housing is pushed higher by inbound work-related migration. So, as there are less jobs nearby, the amenity value of some areas decreases.

The amount of people at risk of defaulting on their mortgage increases in areas where there is a loss of employment or reduced income. In 2008, arguably the last time Sydney house prices went through a correction, the incidence of mortgage defaults and property price declines was geographically localised.

Borrowers who have the least amount of equity in their homes (typically the least wealthy, younger and newer entrants to housing market) are the hardest hit by falling property values. They are more likely to end up “underwater” – that is, owing more than the property is now worth – and face the prospect of a distressed sale. This in turn contributes to the downward spiral in house prices.

Australia has tighter lending criteria than regulators enforced before the global financial crisis in the United States. But concerns by regulators, including APRA, over current lending practices and potentially fraudulent activities raise questions over the real quality of mortgages and the ability of borrowers to repay them.

Professors of Economics, Jason Potts and Sinclair Davidson, RMIT

A combination of low interest rates and low growth in new housing stock drive up Australian housing prices, a situation compounded by poor policy choices by state and federal governments and high demand from foreign residential property investors.

As a result housing is misallocated in the Australian market, across demographic and especially age groups. This produces demographic pressures, as millennials delay leaving home, delay starting families. This leads to political pressure on governments – increases the urge to intervene.

The federal government intervenes, blaming the secondary drivers (particularly the non-voting group: foreign investors). They increase restrictions on foreign investment in residential housing stock.

The federal government also lobbies APRA to increase rules on financial products, while promoting a scheme to subsidise and promote first home ownership.

Because none of these previous measures from the federal government affect the primary drivers of the misallocation of housing, domestic interest rates don’t change, and state governments do not act to release new stock. As a result housing prices continue to grow.

Increasingly alarmed that house prices continue to rise, the federal government starts to panic, threatening ever further regulation and starts to blame the financial system. This triggers the RBA to finally act, raising interest rates.

As interest rates rise, this causes mortgage stress, resulting in default among investors with high amounts of debt, pushing these properties onto the market. These distressed sales finally cause prices to fall.

Timo Henckel, Research Associate, Centre for Applied Macroeconomic Analysis, ANU

International crisis (whether it be political, military, economic) leads to an increase in global risk premiums.

Borrowing costs for Australian banks rise because of this and supply of global capital falls, pushing up mortgage rates in Australia.

The most vulnerable mortgagees can no longer afford their mortgages and are forced to sell their homes.

House prices fall which, coupled with rising interest rates, adds further distress to households’ balance sheets, leading to more selling of houses and so on.

Authors: Jenni Henderson, Editor, Business and Economy, The Conversation; Wes Mountain, Deputy Multimedia Editor, The Conversation

Interviewed: Danika Wright, Lecturer in Finance, University of Sydney; Harry Scheule, Associate Professor, Finance, UTS Business School, University of Technology Sydney; Jason Potts, Professor of Economics, RMIT University; Sinclair Davidson, Professor of Institutional Economics, RMIT University; Timo Henckel, Lecturer, Research School of Economics, and Research Associate, Centre for Applied Macroeconomic Analysis, Australian National University.

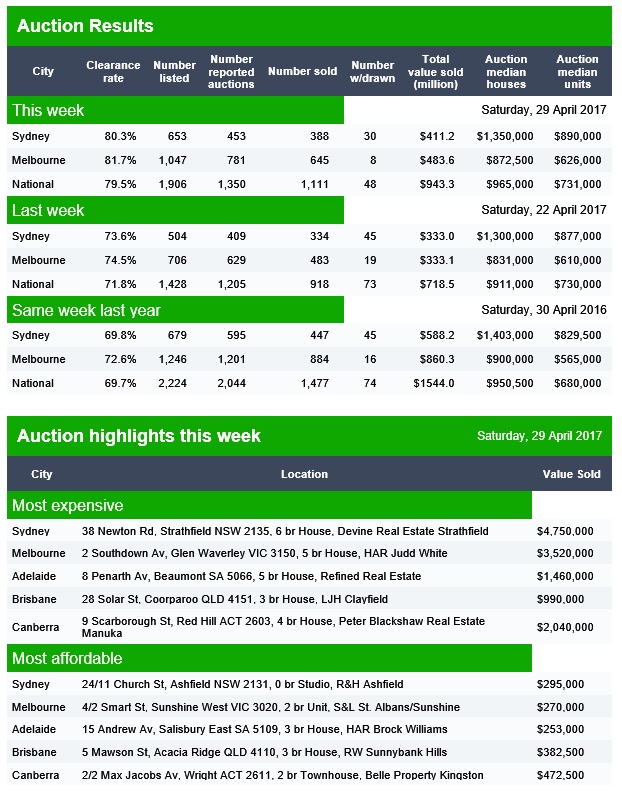

The preliminary auction clearance results are in from Domain. Nationally, it stands at 79.5% on 1,111 sales, compared with 71.8% last week and 69.7% a year ago. Melbourne has greater volume with 645 sold, at a rate of 81.7%, compared with 74.5% last week and 72.6% last year. Sydney cleared 388 at 80.3%, higher than last week.

Brisbane cleared 53% on 85 listed, Adelaide 73 on 65% and Canberra 58 on 64%.

Brisbane cleared 53% on 85 listed, Adelaide 73 on 65% and Canberra 58 on 64%.

So to real evidence to suggest a slowing market.

Today we launch the first of our regular Property Imperative Weekly Update Blogs and Vlogs; the next stage in the development of the Digital Finance Analytics site and in response to requests for a summary service.

We have been publishing regular reports on the residential property and mortgage industry in Australia for many years, in our Property Imperative series. Volume 8 is still available.

With so much happening in the property and mortgage sector, we will discuss the events of the past week in an easy to watch summary. We also will deploy the video blog on our YouTube channel and provide a transcript here, with links to the key articles.

This is the first. Watch it here.

We start with the latest data from the Reserve Bank and APRA for March showed that investment mortgage lending grew more strongly than owner occupied loans, and also that the non-banks are getting more active in this less regulated segment of the market. Pepper for example reported strong loan growth.

Smaller regional banks are getting squeezed, and mortgage lending overall is accelerating despite regulatory pressure. As the total mortgage book grew at more than 6% in the past year, when household incomes are static, the record household debt is still growing. More definitive action from the regulators is required.

APRA Chairman Wayne Byers discussed the residential and commercial property sectors this week at CEDA, and indicated the 10% speed limit on investment loan growth was maintained to protect the pipeline of dwellings under construction. This seems a bit circular to me!

In the past week, the upward momentum in mortgage rates continued with both Westpac and ANZ lifting fixed rate and interest only loan rates, by up to 30 basis points, though some owner occupied loans fell a little. These moves follow recent hikes from CBA and NAB, and continues the cycle higher in response to regulatory pressure, funding costs, competitive dynamics and the desire to repair net interest margins. The regulators have given the banks a perfect alibi!

For investors, these out of cycle rises are now getting close to 1%, though owner occupied borrowers, on principal and interest loans have not been hit as hard. However, even small rises are hitting households in a low income growth environment.

Mortgage stress was in the news this week, with a good piece on the ABC’s 7:30 programme, looking at stress in Western Australia, and citing the example of a property investor who is now in trouble. Our research into stress was also covered in the media, with a focus on Melbourne. Our latest analysis, for April shows a further rise in households in mortgage stress. More of that later.

Meantime, Finder.com published analysis which suggested more than half of mortgage holders were close to a tipping point if mortgage repayments rose by just $100. This would equate to a rate of just 5.28%, not far from current rates at all.

Mortgage Brokers were in the news again thanks to evidence given to the Senate Standing Committee on Economics looking at a consumer protection in the banking and finance industry. Evidence suggested commission aligned to achieving specific volume targets and the use of lender lists may mean the interest of consumers are compromised. We discussed this on the DFA blog last year. In addition, ASIC highlighted deficiencies in the information flows between brokers and banks, and suggested that more robust systems and processes are needed, especially around commission data and broker performance.

Also, the risk of loans originated via brokers was discussed again, with the argument being mounted that financial incentives make broker loans intrinsically riskier.

Meantime whilst the government switched the narrative to good and bad debt, housing affordability remained in the news, with the HIA arguing again that supply side issues are the key, despite the fact that the average number of people living in each dwelling across Australia has hardly changed in years.

We think supply is not the big issue. Yes, there should be more focus on building more affordable social housing, but the main focus needs to be the reduction in investor tax incentives. The financialisation of property is the real underlying issue, but this is hard to address, and explains why the government is now wanting us to look elsewhere.

In broader economic news, inflation rose a tad, thanks to a strong rise in Victoria, and as a result there is less reason to expect an RBA cash rate cut. That said, the official CPI understates the real experience of many households, not least because housing costs are so significant now. We maintain our view that the next RBA rise will be up, not down, unless we get a significant external shock. Of course a cash rate rise will likely flow on to mortgage holders, putting them under more under pressure.

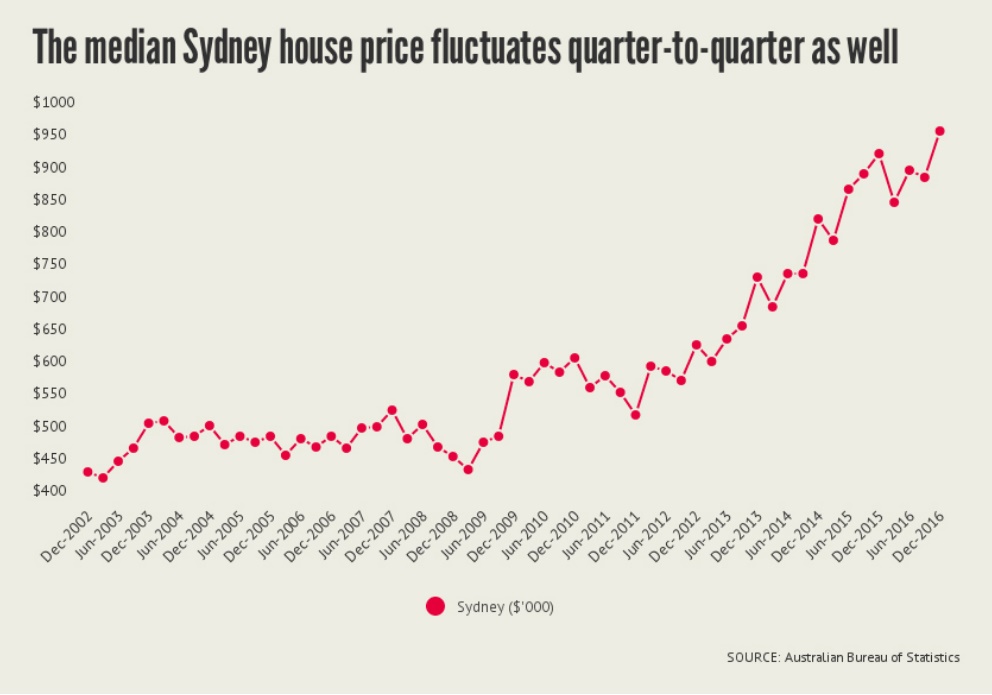

Finally, in preliminary news from CoreLogic they suggest that Sydney home prices may have stalled in April. Whilst some reports say this is the top, there are a range of technical issues which suggests it is too early to make this call. We need to see more data, and the Auction clearances may be an indicator of what is to come.

Nevertheless, we hold the view that we have probably reached the peak, and as mortgage lending tightens, and investors become more sanguine, prices in the major centres are likely to slide, mirroring the falls in WA, now, in some places down more than 20%. It then becomes a question of whether is turns into a rout, or whether prices drift sideways for some long time.

And that’s the Property Imperative week to the 29th April!

Experts have warned against predicting that property prices have peaked just yet.

A flurry of headlines this week generated by UBS analysts, Australian Financial Review columnists and others all warned that Sydney and possible Melbourne prices had peaked and we should brace for a correction.

Most were based on slower price growth in Sydney dwelling values and slight reductions in auction clearance rates compiled by CoreLogic, a property data firm.

However, CoreLogic director of research Tim Lawless cautioned against reading into the results (especially dwelling values, which are yet to be officially released for April) because April and May are generally weaker periods.

“Potentially there is some seasonality creeping into these numbers and that’s one of the reasons why I would probably suggest caution calling the peak right now before we see a few more months and see if the trend actually develops,” Mr Lawless told The New Daily.

“When we look at, say, a year ago or any sort of seasonality in the marketplace, yeah, we do generally see some easing in our reading around April and May.”

A further complication is that CoreLogic adjusted how it calculated dwelling values in May 2016 to account for seasonality. The result, according to Mr Lawless, is that “technically speaking, there are some challenges and complexities making a year-to-year comparison”, although he said the adjustments were “quite minor” and values could still be compared.

The change sparked a scandal last year, with the Reserve Bank ditching the company as its preferred data source after claiming it had overstated dwelling values in April and May.

Despite this, CoreLogic remains the most widely cited property data source because it reports dwelling values daily. But the most authoritative is the Australian Bureau Statistics, which has measured similar quarter-on-quarter falls in the past, especially between the December and June quarters. And yet, the trend has been ever upwards.

IFM chief economist Dr Alex Joiner agreed we shouldn’t jump to conclusions based on the latest statistics.

“I wouldn’t suggest that anyone looks at any month-to-month data in Australia and makes firm conclusions from it,” Dr Joiner told The New Daily.

“People might want to rush to call the top, but the trends are for gradually decelerating growth, and I think that’s about right.”

But if this is not the peak, the market is “very much approaching it” because the Reserve Bank and the banks are likely to lift interest rates even as wage growth stays low, Dr Joiner said.

“When that actually decelerates price growth, whether it’s this month or later in the year, I don’t know. But we’re certainly eeking out the very last stages of price growth in the property market.”

From The Real Estate Conversation.

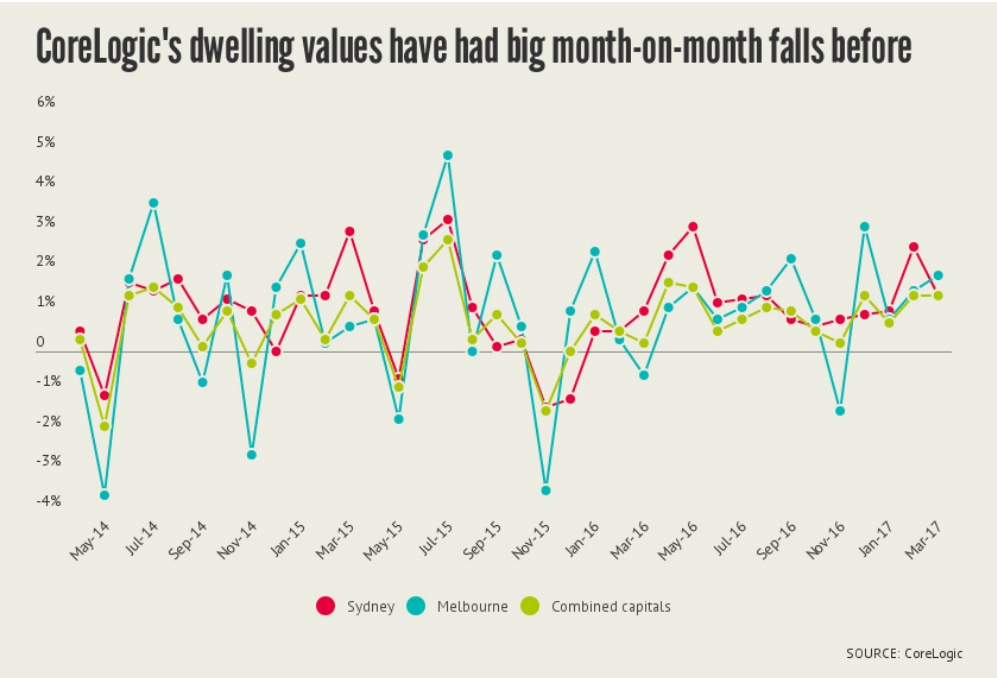

CoreLogic has revealed the property market has been largely flat during the month of April, ahead of the release of its end-of-month numbers on Monday.

CoreLogic’s hedonic home value index for Australia’s top five property markets held virtually steady in the first 27 days of the month, indicating that the current cycle could be moving through its peak.

Sydney prices recorded a “subtle” decline, according to CoreLogic, a dramatic though welcome turnaround from the blistering 18.8 per cent increase recorded in March. The five-city aggregate also recorded an exceptionally strong result in March, rising 12.9 per cent despite a 4.7 per cent decline in Perth prices.

Leeanne Pilkington, deputy president of the Real Estate Institute of New South Wales, says the April decline in Sydney prices was only very slight, and will vary from suburb to suburb.

“None of my agents are telling me they’re worried about prices going down,” she said.

However, Pilkington said her agents are saying there a lower numbers at open houses, which means there could be less competition in the market between buyers.

“We’ve seen that [trend] with the lower clearance rate last week,” she said. Pilkington said clearance rates above 80 per cent were not sustainable, and that a modest decline in clearance rates would actually be desirable.

“We really want some stability in the market,” she said.

Pilkington said April was a holiday month, containing both Easter and ANZAC day, so the numbers for the month may not reflect the true state of the market. Auction clearance rates over the weekend will provide clearer guidance, she said.

Tim Lawless, head of research Asia Pacific with CoreLogic, attributes the flat overall result to recent regulatory changes which have led to higher mortgage rates and weaker investment demand, causing a “dampening” effect on the property market.

Wayne Byers APRA Chairman spoke at CEDA’s 2017 NSW Property Market Outlook in Sydney today. Of note, he explains the reason why the 10% investor speed limit was not reduced, because of the potential impact on commercial propery construction!

My remarks today come, unsurprisingly, from a prudential perspective. Property prices and yields, planning rules, the role of foreign purchasers, supply constraints, and taxation arrangements are all important elements of any discussion on property market conditions, and I’m sure the other speakers today will touch on most of those issues in some shape or form. But I’ll focus on APRA’s key objective when it comes to property: making sure that standards for property lending are prudent, particularly in an environment of heightened risk.

Sound lending standards

Our recent activity in relation to residential and commercial property lending has been directed at ensuring banking institutions maintain sound lending standards. Our ultimate goal is to protect bank depositors – it is, after all, ultimately their money that banks are lending. Basic banking – accepting money from depositors and lending to sound borrowers who have good prospects of repaying their loans – is what it’s all about. Of course, banking is about risk-taking and it is inevitable that not every loan will be fully repaid, but with appropriate lending standards and sufficient diversification, the risk of losses that jeopardise the financial health of a bank – and therefore the security offered to depositors – can be reduced to a significant degree. The banking system is heavily exposed to the inevitable cycles in property markets, and our goal is to seek to make sure the system can readily withstand those cycles without undue stress.

Our mandate goes no further than that. We also have to take many influences on the property market – tax policy, interest rates, planning laws, foreign investment rules – as a given. And there are credit providers beyond APRA’s remit, so a tightening in one credit channel may just see the business flow to other providers anyway. For those reasons, there are clear limits on the influence we have. Property prices are driven by a range of local and global factors that are well beyond our control: whether prices go up or go down, we are, like King Canute, unable to hold back the tide.

Of course, that is not to ignore the fact that one determinant of property market conditions is access to credit. We acknowledge that in influencing the price and availability of credit, we do have an impact on real activity – and this may feed through to asset prices in a range of ways. But I want to emphasise that we are not setting out to control prices. Property prices will go up and they will go down (even for Sydney residential property!). It is not our job to stop them doing either of those things. Rather, our goal is to make sure that whichever way prices are moving at any particular point in time in any particular location, prudentially-regulated lenders are alert to the property cycle and making sound lending decisions. That is the best way to safeguard bank depositors and the stability of the financial system.

Residential property lending

APRA has been ratcheting up the intensity of its supervision of residential property lending over the past five or so years. Initially, this involved some fairly typical supervisory measures:

- in 2011 and again in 2014, we sought assurances from the Boards of the larger lenders that they were actively monitoring their housing lending portfolios and credit standards;

- in 2013, we commenced more detailed information collections on a range of housing loan risk metrics;

- in 2014, we stress-tested around the largest lenders against scenarios involving a significant housing market downturn;

- also in 2014, we issued a Prudential Practice Guide on sound risk management practices for residential mortgage lending; and

- we have conducted numerous hypothetical borrower exercises to assess differences in lending standards between lenders, and changes over time.

These steps are typical of the role of a prudential supervisor: focusing on the strength of the governance, risk management and financial resources supporting whatever line of business is being pursued, without being too prescriptive on how that business should be undertaken.

But from the end of 2014, we stepped into some relatively new territory by defining specific lending benchmarks, and making clear that lenders that exceeded those benchmarks risked incurring higher capital requirements to compensate for their higher risk. In particular, we established quantitative benchmarks for investor lending growth (10 per cent), and interest rate buffers within serviceability assessments (the higher of 7 per cent, or 2 per cent over the loan product rate), as a means of reversing a decline in lending standards that competition for growth and market share had generated.

I regard these recent measures as unusual, and not reflective of our preferred modus operandi. We came to the view, however, that the higher-than-normal prescription was warranted in the environment of high house prices, high household debt, low interest rates, low income growth and strong competitive pressures. In such an environment, it is easy for borrowers to build up debt. Unfortunately, it is much harder to pay that debt back down when the environment changes. So re-establishing a sound foundation in lending standards was a sensible investment.

Since we introduced these measures in late 2014, investor lending has slowed and serviceability assessments have strengthened. But at the same time, housing prices and debt have got higher, official interest rates have fallen further and wage growth remains subdued. So we recently added an additional benchmark on the share of new lending that is occurring on an interest-only basis (30 per cent) to further reduce vulnerabilities in the system.

Each of these measures has been a tactical response to evolving conditions, designed to improve the resilience of bank balance sheets in the face of forces that might otherwise weaken them. We will monitor their effectiveness over time, and can do more or less as need be. We have also flagged that, at a more strategic level, we intend to review capital requirements for mortgage lending as part of our work on establishing ‘unquestionably strong’ capital standards, as recommended by the Financial System Inquiry (FSI).

Looking at the impact so far, I have already noted that our earlier measures have helped slow the growth in investor lending (Chart 1), and lift the quality of new lending. Serviceability tests have strengthened, although as one would expect in a diverse market there are still a range of practices, ranging from the quite conservative to the less so. Lenders subject to APRA’s oversight have increasingly eschewed higher risk business (often by reducing maximum loan-to-valuation ratios (Chart 2)), or charged a higher price for it.

For example, there is now a clear price differential between lending to owner-occupiers on a principal and interest basis, and lending to investors on an interest-only basis (Chart 3). And as a result of our most recent guidance to lenders, we expect some further tightening to occur.

Looked at more broadly, the most important impact has been to reduce the competitive pressure to loosen lending standards as a means of chasing market share. We are not seeking to interfere in the ability of lenders to compete on price, service standards or other aspects of the customer experience. We do, however, want to reduce the unfortunate tendency of lenders, lulled by a long period of buoyant conditions, to compete away basic underwriting standards.

Of course, lenders not regulated by APRA will still provide competitive tension in that area and it is likely that some business, particularly in the higher risk categories, will flow to these providers. That is why we also cautioned lenders who provide warehouse facilities to make sure that the business they are funding through these facilities was not growing at a materially faster rate than the lender’s own housing loan portfolio, and that lending standards for loans held within warehouses was not of a materially lower quality than would be consistent with industry-wide sound practices. We don’t want the risks we are seeking to dampen coming onto bank balance sheets through the back door.

Commercial real estate lending

For all of the current focus on residential property lending, it has been cycles in commercial real estate (CRE) that have traditionally been the cause of stress in the banking system. So we are always quite interested in trends and standards in this area of lending. And tighter conditions for residential lending will also impact on lenders’ funding of residential construction portfolios – we need to be alert to the inter-relationships between the two.

Overall, lending for commercial real estate remains a material concentration of the Australian banking system. But while commercial lending exposures of APRA-regulated lenders continue to grow in absolute terms, they have declined relative to the banking system’s capital (partly reflecting the expansion in the system’s capital base). Exposures are now well down from pre-GFC levels as a proportion of capital, albeit much of the reduction was in the immediate post-crisis years and, more recently, the relative position has been fairly steady (Chart 4).

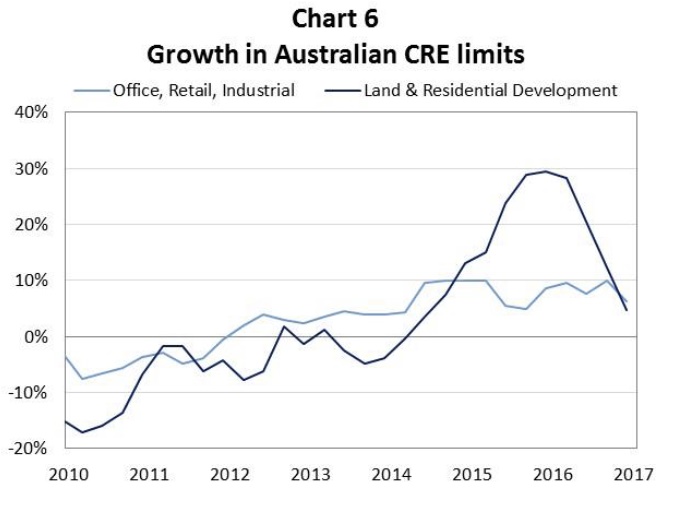

The story has been broadly similar in most sub-portfolios, with the notable exception of land and residential development exposures (Chart 5).

These have grown strongly as the banking industry has funded the significant new construction activity that has been occurring, particularly in the capital cities of Australia’s eastern seaboard. At the end of 2015, these exposures were growing extremely rapidly at just on 30 per cent per annum, but have since slowed significantly as newer projects are now being funded at little more than the rate at which existing projects roll off (Chart 6).

(As an aside, this is one reason why we opted not to reduce the 10 per cent investor lending benchmark for residential lending recently. There is a fairly large pipeline of residential construction to be absorbed over the course of 2017, and there is little to be gained from unduly constricting that at this point in time.)

In response to the generally low interest rate environment, coupled with relatively high price growth in some parts of the commercial market, low capitalisation rates and indications that underwriting standards were under competitive pressure, we undertook a thematic review of commercial property lending over 2016. We looked at the portfolio controls and underwriting standards of a number of larger domestic banks, as well as foreign bank branches which have been picking up market share and growing their commercial real estate lending well above system growth rates.

The review found that major lenders were well aware of the need to monitor commercial property lending closely, and the need to stay attuned to current and prospective market conditions. But the review also found clear evidence of an erosion of standards due to competitive pressures – for example, of lenders justifying a particular underwriting decision not on their own risk appetite and policies, but based on what they understood to be the criteria being applied by a competitor. We were also keen to see genuine scrutiny and challenge that aspirations of growth in commercial property lending were achievable, given the position in the credit cycle, without compromising the quality of lending. This was often being hampered by inadequate data, poor monitoring and incomplete portfolio controls. Lenders have been tasked to improve their capabilities in this regard.

Given the more heterogeneous nature of commercial property lending, it is more difficult to implement the sorts of benchmarks that we have applied to residential lending. But that should not be read to imply we have any less interest in the quality of commercial property lending. Our workplan certainly has further investigation of commercial property lending standards in 2017, and we will keep the need for additional guidance material under consideration.

Concluding remarks

So to sum up, property exposures – both residential and commercial – will remain a key area of focus for APRA for the foreseeable future. Sound lending standards are vital for the stability and safety of the Australian banking system, and given the high proportion of both residential mortgage and commercial property lending in loan portfolios, there will be no let up in the intensity of APRA’s scrutiny in the foreseeable future. But despite the fact the merit of our actions are often assessed based on their expected impact on prices, that is not our goal. Prudence (not prices) is our catch cry: our objective is to make ensure that, whatever the next stage of the property cycle may bring, the balance sheet of the banking system is resilient to it.

The federal Minister for Small Business, Michael McCormack MP, has said he is “in awe” of what brokers do and is urging them to email him to highlight any areas where bureaucracy can be reduced.

Speaking at a breakfast meeting hosted by the Mortgage & Finance Association of Australia (MFAA) in Sydney yesterday, the small business minister and representative for Riverina, NSW, said that government “values what [brokers] do” and wanted to help reduce the “burden of bureaucracy” on small business owners.

He said: “What really struck me from the people [I met today] is the fact that your sector does face challenges. There is no denying that… You are facing many challenges and also many opportunities in what you do every day, driven by housing affordability, driven by the banking sector, driven by regulation and government — but also driven by such things as innovation and the need for your sector to get onboard.”

He continued: “I am in awe of what you do. I know how hard it is. I don’t just say that lightly [and] I don’t just say that because I’m the minister of small business, I truly am in awe of what you do…

“You’ve taken the leap of faith to be your own boss, to be someone who is the master of their own destiny and that takes a lot of effort and work.

“I know, and my government knows and appreciates, what you do. Not just for the small business sector but what you do for your customers, your consumers — those people who need finance, those people who need good advice — and that’s the sort of thing you people are doing each and every day.”

The minister added: “You’re starting very early in the morning and finishing very late at night and sometimes when you get home you’ve got more paperwork, courtesy of our government, and that’s what we’re trying to cut through as much as we can; that regulation over-reach.

“That’s why we’re trying to cut through some of the bureaucracy. And if there are examples in your sector, in your industry, of federal government bureaucracy paperwork that you feel is a little bit onerous or a little bit replicated in some other areas of state, please let me know.

“It’s not hard, just google my name and flick me an email or flick it to your industry body. Because we want to lift the burden of bureaucracy, as much as we can as a government, from you.”

Noting the MFAA’s earlier statement that there were 17,000 mortgage brokers in Australia, Minister McCormack said that although a “mere handful” were at the Sydney event, they were a “very important handful” given the fact that Sydney is “a driver of much of Australia’s economy”.

He explained: “What you people do for your customers here in Sydney is so, so vitally important. You’re assisting with not just home loans mortgages but financing many small businesses. This is as many bank branches reduce their retail footprints… making brokers the only source (in some areas) of financial services for what, I would say, is a growing customer base. That’s one of the reasons why your industry is so strong and we as a government want to make it stronger…

“Brokers now do more than half of all home loans and that is exactly what our government wants to see – you people ‘having a go’. And it’s important that its incumbent on government to make policy setting as easy for you to be able to actually have that go, to back yourself to do what you have done so well, for so many years.”

Brokers ‘generally get it right’

Taking a moment to drink some water, Minister McCormack noted that he was drinking from the same glass that MFAA CEO Mike Felton had used and joked: “If you can’t trust a mortgage broker, who can you trust?”

Continuing on the theme of trust, the minister touched on the recent ASIC remuneration review.

He commented: “This was finalised last month and what they found is that, as you would know, current ownership remuneration structures could create conflicts of interest and lead to poor outcomes for consumers. and of course, none of us want to see poor outcomes for consumers, not least of which government, but also not least of which you, the people in this room. Repeat customers, repeat businesses are what makes your small business great.”

Noting that the review didn’t recommend government action, but instead asked the industry to provide feedback, he said he “agreed wholeheartedly with that approach”.

“The government values this industry very, very highly. We put you up there, we really do. And I do personally, and I know people in this sector from my dealings over the years… that you people generally get it right. You generally get it right 99.9 per cent of the time. So that’s across industry models across Australia [and] is pretty darn good. The government wants to help you, and I know you want to help yourself, so I encourage that you engage with the review process.”

He concluded: “More transparency leads to better outcomes to consumers and that makes your industry more sustainable.

“Ultimately, it’s the best outcome for everyone and that’s how the industry will continue to grow and that’s what the government wants.”