Demand for property on realestate.com.au skyrocketed in 2016, with the REA Group Property Demand Index increasing by 16.2% across the year. The REA Group Property Demand Index is produced by the REA Group, owner and operator of realestate.com.au.

After peaking in October and November, demand for property dropped slightly to close out 2016, with the index falling 6.6% nationally in December. Victoria saw the largest decline over the month, driven by low levels of demand for both houses and apartments. New South Wales followed closely, suggesting the housing boom may be over, or at the very least slowing quickly, in both Sydney and Melbourne.

Despite December declines, Tasmania, New South Wales and Victoria continue to see the highest levels of demand in Australia with Western Australia and Northern seeing the lowest

While still early into the new year, the easing of demand nationally suggests that the record price rises we saw in Sydney and Melbourne last year are likely to be more subdued as we move further into 2017.

The key drivers of this demand decline are likely due to Australian banks increasing interest rates for buyers independently of the Reserve Bank of Australia in late November and early December and continuing affordability issues across the Eastern seaboard.

Given the RBA has indicated that it may still cut the cash rate further, the banks have sent strong signals that they will respond by not passing cuts onto borrowers and we expect out of cycle interest rate rises by banks to continue. This will be a key issue for borrowers this year, especially first home buyers and investors, with access to cheap money becoming more difficult.

The states which saw the largest declines in demand in December were New South Wales and Victoria. Continued concerns about apartment over supply are starting to cause concern in these markets with demand for apartments dropping by more than 7% in both states.

Western Australia and Northern Territory remain the lowest in-demand markets on realestate.com.au, however Western Australia’s demand index was relatively stable and both states saw an increase in apartment demand. The result suggests that barring any surprising negative economic news or changes to the supply outlook in Western Australia, the bottom of the housing market could be close.

Tasmania continues to see elevated levels of demand and is now the strongest demand market in Australia. Relative affordability is likely a key factor driving interest

Category: Property Market

Economist’s radical plan to cut bubble lending

To stop the ever increasing levels of debt in Australia, one economist believes that there needs to be a hard reset of private debt levels via a “people’s quantitative easing”.

In an interview with the Australian Financial Review, author and economist Steve Keen, outlined his two-step plan to reduce household debt from current levels of 120% to between 50 and 100%.

The first step involves banks using government cash injections that reduce account holders’ existing debt. Customers with no debt would receive cash.

Keen said this instalment would be a bit larger than the $1,000 stimulus Kevin Rudd offered in 2009.

“In anything like this, which hasn’t been tried before, I would want to do it in small doses,” he told the AFR.

Radical yet simple reform of the banking sector would then be required, he said.

“What I want to do is bring in a range of bank rules which would limit the amount of lending you can give against an asset to some multiple of the income-earning capacity of the asset.”

For instance, banks could put a loan limit of $500,000 on an estimated annual rental income of $50,000. This ensures that the bidder for the house with the most savings who is more capable of handling the debt comes out as the winner.

“I want to cut off the asset bubble lending. When you look at the empirical data, overwhelmingly it’s leverage that determines asset prices. You have this positive feedback loop between lending and asset prices and that’s how you get the bubbles we’ve got. These guys are making money by creating Ponzi schemes.”

Channel Nine News Does House Prices and Mortgage Defaults

A segment today from Channel Nine featured the latest data on Sydney residential property, and featured data from the Digital Finance Analytics mortgage default heat mapping, as well as the latest from CoreLogic on Home Prices.

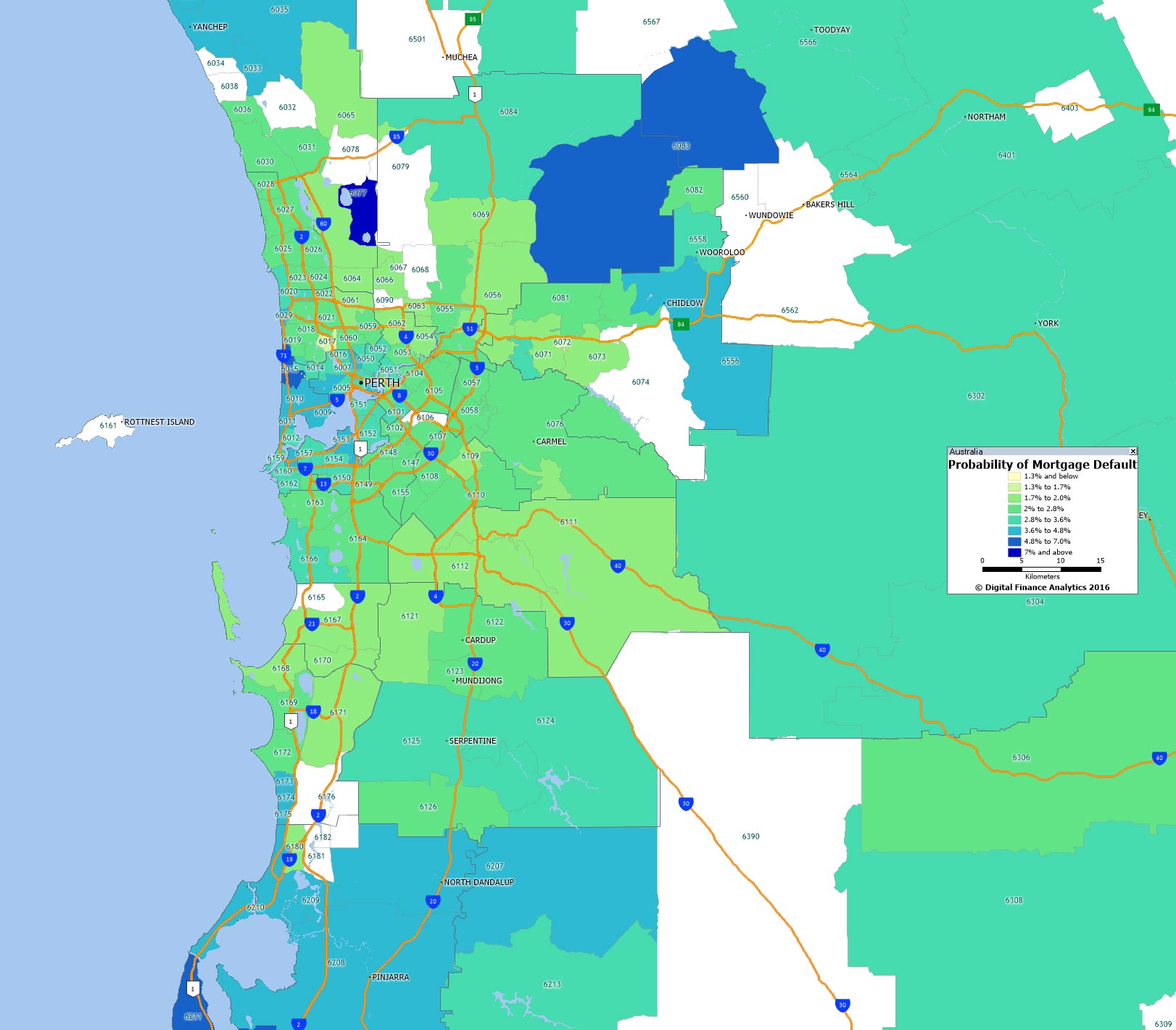

Mortgage Default Heat Map Predictions

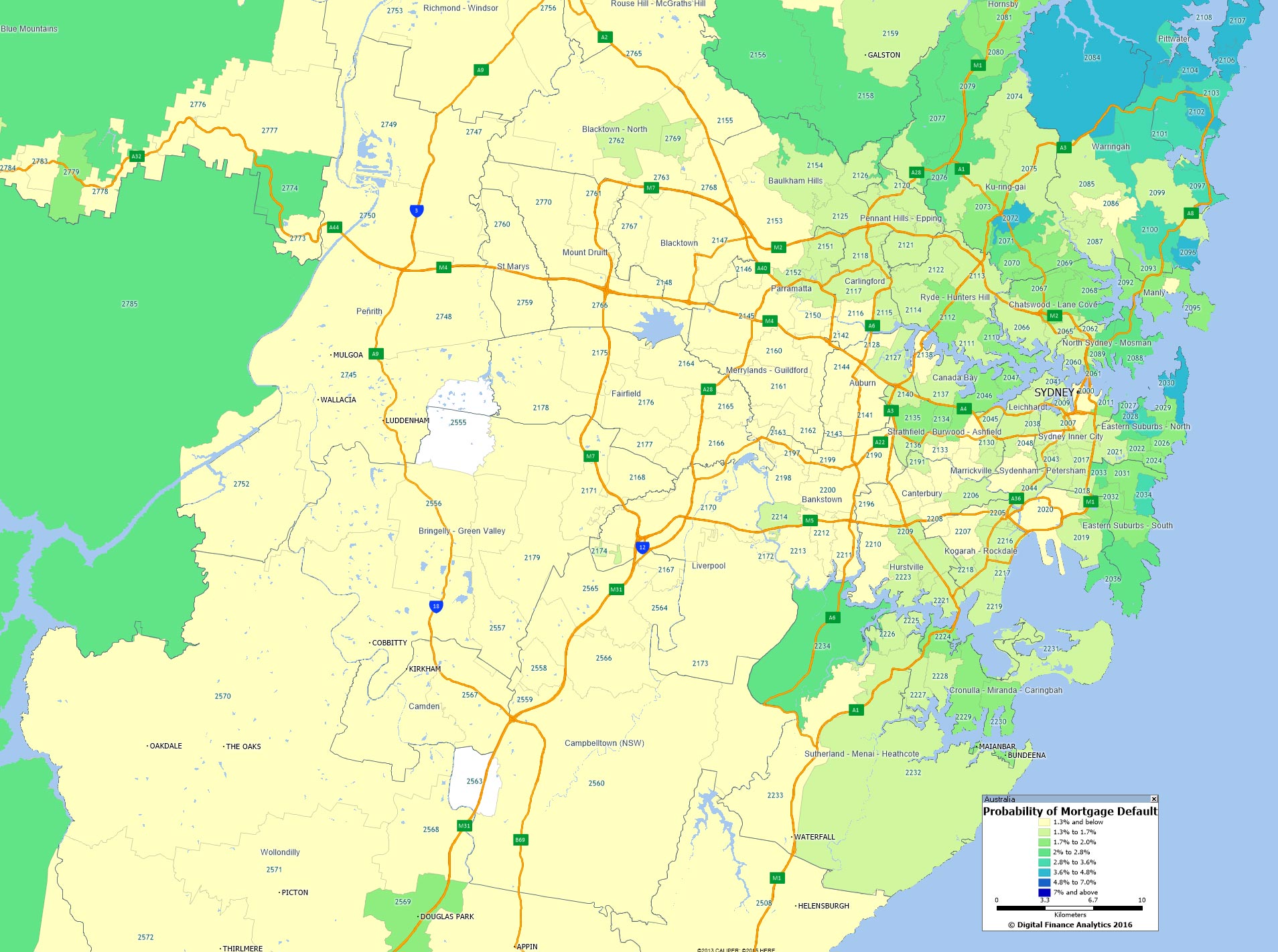

In our last post for 2016 we have geo-mapped the probability of mortgage default by post code across the main urban centres through 2017. You can read about our approach to the analysis here.

We start with Sydney, which is looking pretty comfortable.

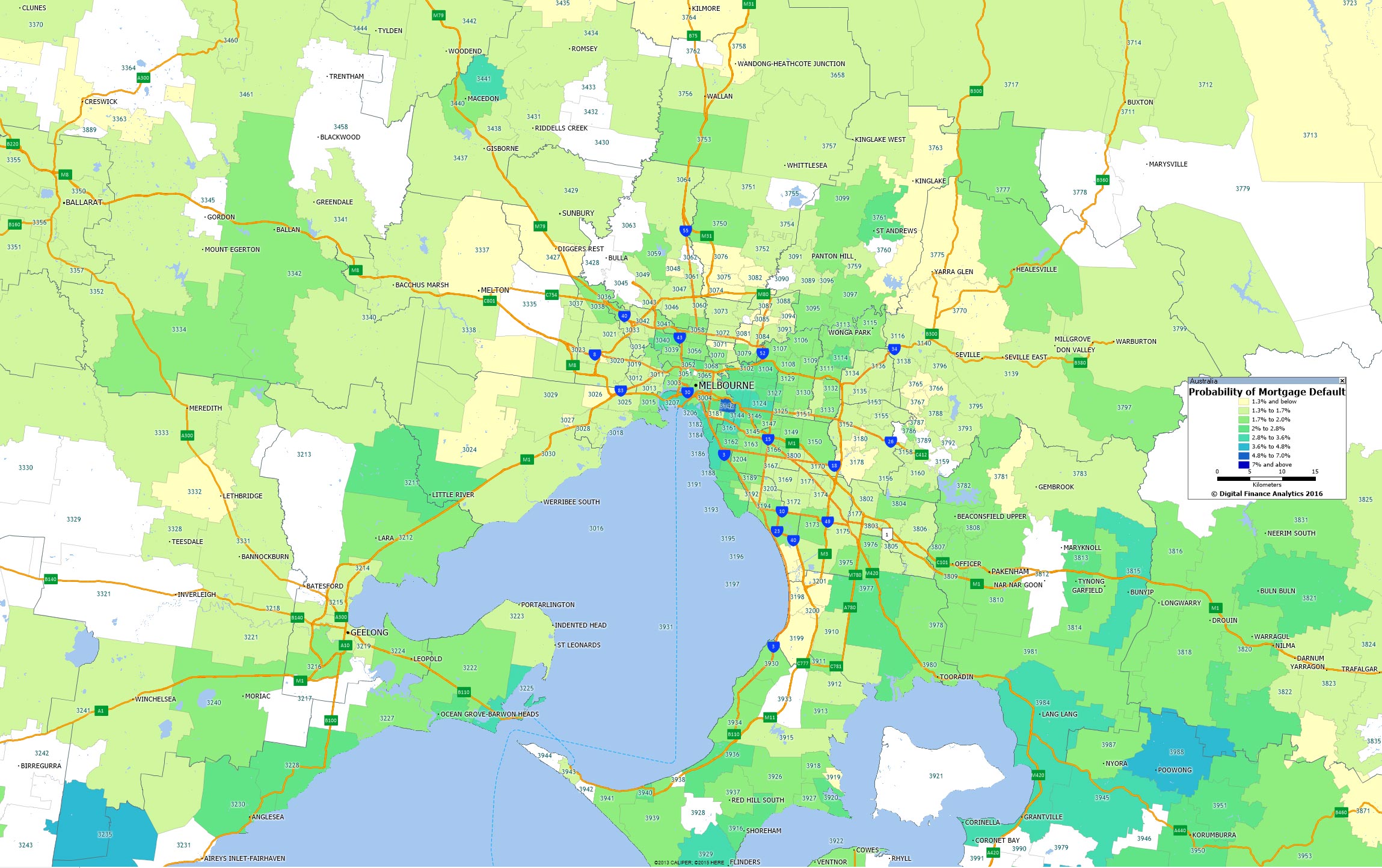

Melbourne is also looking reasonable, though with a few hot spots.

Melbourne is also looking reasonable, though with a few hot spots.

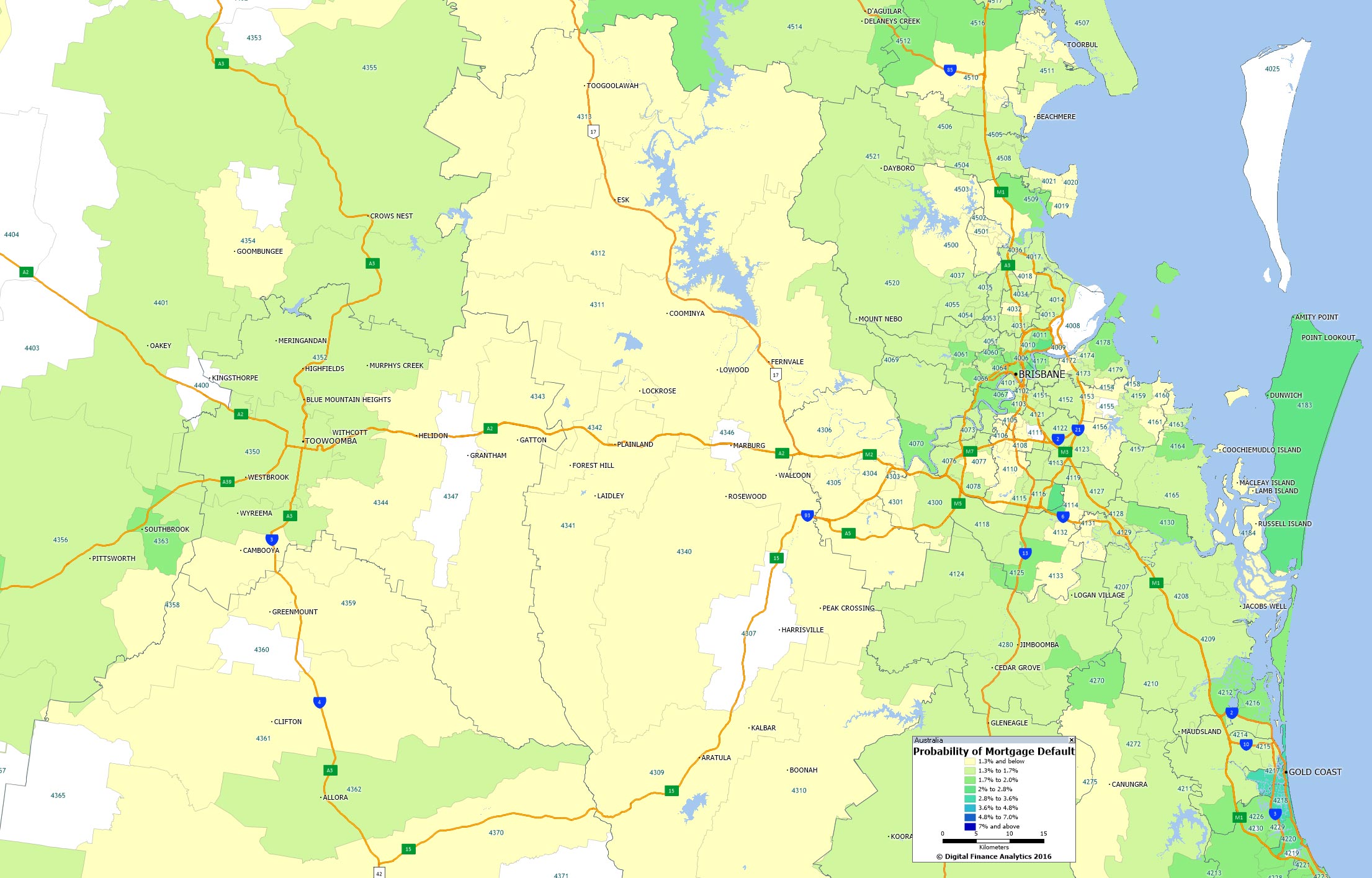

Brisbane default levels are also benign (though the mining areas are more at risk).

Brisbane default levels are also benign (though the mining areas are more at risk).

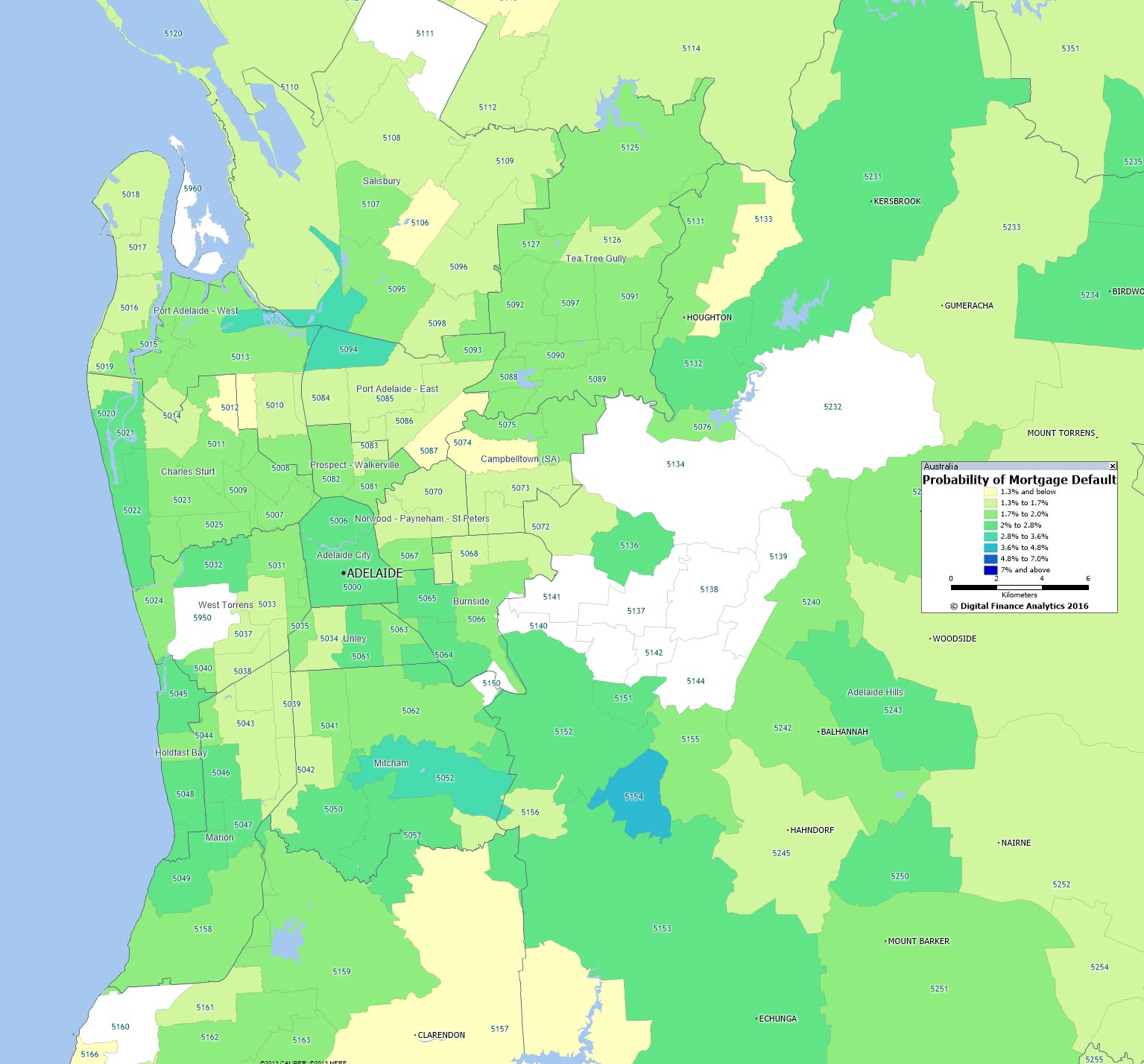

Adelaide shows a few hot spots.

But greater Perth is where we think much of the action will be – plus the mining areas beyond the urban area.

But greater Perth is where we think much of the action will be – plus the mining areas beyond the urban area.

As we discussed, our prediction for 2017 is that the property market generally will still be gaining ground, though some regions will be under significant pressure. Banks will be seeing losses rising a little, but defaults will remain contained.

As we discussed, our prediction for 2017 is that the property market generally will still be gaining ground, though some regions will be under significant pressure. Banks will be seeing losses rising a little, but defaults will remain contained.

Thanks to those who followed the DFA blog in 2016. We wish you a peaceful new year. We will be back in 2017 with more intelligent insights.

Capital city clearance rate remain above 70 per cent

CoreLogic confirms the auction clearance stats for the last weekend of the year, with combined capital city clearance rate remaining above 70 per cent, while auction volumes continue their seasonal taper.

Auction activity continued to ease this week after a surge in auctions over the past four weeks. The combined capital city clearance rate fell slightly to 70.5 per cent, down from last week’s 71.6 per cent. The number of properties taken to auction this week also fell across the capital cities, with 2,722 reported auctions, down from 3,432 last week, when the second busiest auction week this year was recorded. However, compared to the corresponding week last year, auction activity is significantly higher, with 1,818 auctions and a lower rate of clearance (59.4 per cent) reported over the same period last year. Auction numbers will remain relatively sedate over the festive period, with CoreLogic resuming auction reporting in late January.

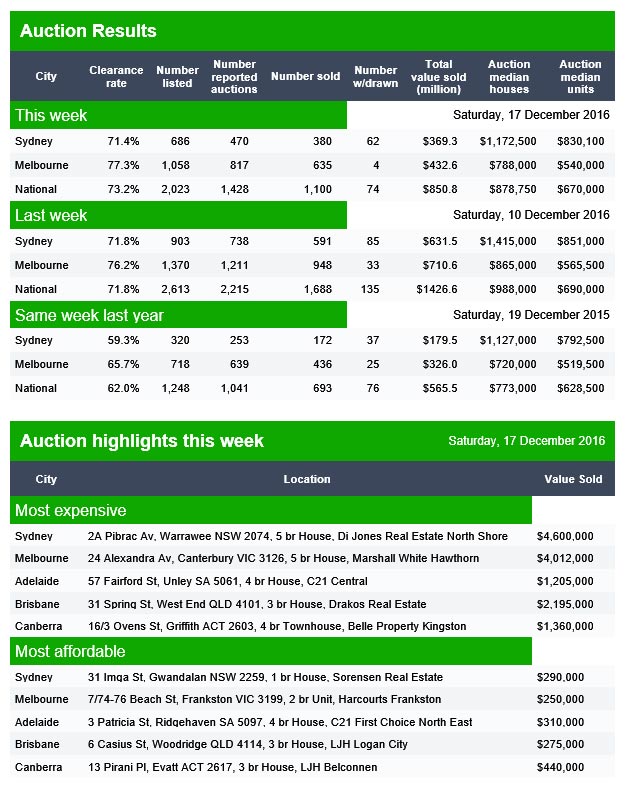

Today’s Auction Results Are In

The preliminary auction results are in from Domain for the last weekend before the Christmas break. Compared with last year, momentum is still strong, especially in Sydney and Melbourne.

Sydney cleared 71.4%, Melbourne 77.3% and Nationally 73.2%. Elsewhere Brisbane cleared 42% of 142 listings, Adelaide 75% of 75 listed and Canberra 70% of 62 listed.

Sydney cleared 71.4%, Melbourne 77.3% and Nationally 73.2%. Elsewhere Brisbane cleared 42% of 142 listings, Adelaide 75% of 75 listed and Canberra 70% of 62 listed.

More Proof That Young Australians Are Choosing Property Investment Over First Home

Regular followers of the DFA Blog will know we have been highlighting the drift of first time buyers towards the property investment sector for the past couple of years. We produce this chart each month, which combines data from our households surveys and the ABS first time buyer series (which stubbornly refuses to identify FTB investors, despite the recent methodology change. The red line shows the number of FTB purchasers who go direct to the investment sector. So called “Rentvesting”.

![]()

Now two surveys, as reported in The Real Estate Daily, confirm this trend.

Both NAB’s Residential Property survey and ING Direct’s Financial Wellbeing Index show an increase in the number of young, first-time property buyers purchasing a property investment instead of a home.

The NAB Residential Property survey for the third quarter found first-home investors made up 12.2 per cent of all new property sales in the third quarter of 2016, up from 11.1 per cent in the second quarter, according to the survey.

The survey also found that first home investors represented 10.6 per cent of all established property sales, an increase from 9.7 per cent in the second quarter.

Peter Mastrioanni, of rentvesting.com.au, said the results were a sign that young people still want to invest in property, but in more flexible ways.

“First-time investors are now taking every opportunity to invest in real estate in a way that allows them to invest for reasons such as comfort instead of security, lifestyle instead of retirement, and versatility instead of restriction,” he said.

Mastrioanni said Generation Y in particular were choosing to become “rentvesters” instead of giving up on their dream of property ownership.

Rentvesting involves investing in property in more affordable locations, including interstate if necessary, while continuing to rent in the inner-city suburbs.

“This way, they’re having their property cake and eating it, too,” said Mastrioanni.

The result is backed up by ING Direct’s latest Financial Wellbeing Index, which shows a growing numbers of young buyers in the 18 to 34 age bracket are becoming property investors.

The index showed that 22 per cent of Generation Y own at least one investment property, followed by 20 per cent of Generation X and 19 per cent of Baby Boomers.

Mark Woolnough, ING Direct Head of Third Party Distribution, said concerns about housing affordability are not preventing young people from buying an investment property.

“What’s interesting is that while there are continued questions around affordability and the challenges for younger generations in getting onto the property ladder, it’s actually Gen Y that is leading the property investment pack,” he said.

Rates Plough Higher

Following the FED’s decision today, the benchmark T30 US Bond yield continues to move higher. A strong indicator that capital markets rates will continue to rise. The FED is signalling more hikes next year, so yields will continue to climb. This has global significance.

The knock on effect for Australia is significant. Banks will have to pay more for their capital markets funding. International money market investors will switch money from Australia in favour of US markets, putting downward pressure on the AU$. This makes an RBA rate cut in 2017 even more remote (though some economists are still talking about 2 cuts!).

The knock on effect for Australia is significant. Banks will have to pay more for their capital markets funding. International money market investors will switch money from Australia in favour of US markets, putting downward pressure on the AU$. This makes an RBA rate cut in 2017 even more remote (though some economists are still talking about 2 cuts!).

Mortgage rates here will continue to rise. Our outlook on the Property Market for 2017 took these rate movements into account.

Further evidence the world changed last month.

China’s Housing Market Isn’t a Bubble, Says One Strategist

A financial crisis in China is no more likely in the coming decade than it was in the past 10 years, and pessimists predicting one have long done so without regard for fundamentals.

So says sinologist Andy Rothman, a San Francisco-based investment strategist at Matthews International Capital Management LLC, which oversees $26.1 billion. Before joining in 2014 he lived in China for two decades, working in the U.S. Foreign Service, including as head of the macroeconomics and domestic policy office of the U.S. embassy in Beijing. He later was a Shanghai-based strategist in CSLA Ltd., an investment banking arm of Credit Agricole SA.

China has no housing bubble and there’s no looming banking crisis, he says. His optimism rests on his view that the housing market is on a solid foundation. Leverage is the most important precondition for a bubble in any asset, and home buyer indebtedness in China is very low because down payment requirements are high, unlike in the U.S., he says.

“This isn’t like speculating in Las Vegas with zero money down,” he says. “China has a lot of problems, but they don’t tend to be the apocalyptic, catastrophic problems that we often read about. They’re more mundane, longer-term problems like how do you develop a rental market.”

While the country’s overall debt situation is serious, it’s still unlikely to lead to a financial crisis or economic hard landing, he says. That’s because potential bad debts are in state entities, which allows the government to manage how or whether they go bad, Rothman says.

He projects new home sales may fall 10 percent next year after rising about 30 percent in 2016 as the government continues to curb prices. While bears may see that as evidence of impending disaster, Rothman says it would still make 2017 China’s second-best year ever for new home sales because the base has grown so big.

So Where Will The Property Market Go In 2017?

Having looked at events in the Property Market in 2016, we now turn to our expectations for 2017. There are many uncertainties which may impact the market, but using our surveys and modelling as a guide, we can make some educated guesses.

First, mortgage rates will be higher by the end of 2017 than they are now. We have already seen the impact of the Trump Effect on capital markets, and these higher costs are already flowing into higher mortgage rates. This process will continue as banks fight for a share of the deposit market, and at the same time continue to build their capital buffers. We think, on current trajectory rates could rise by more than half a percent, meaning the average repayment mortgage would rise by over $100 a month next year. Larger mortgages would rise by much more.

The RBA is unlikely to cut rates, and it is possible they may lift later in 2017 – but as the cash rate is disconnected from the mortgage rate, this is not necessarily such an important factor as in previous decades.

Many younger households are already using more than half their disposable income to repay their mortgage, and any increase will be very painful in a low income growth environment. We do not expect real incomes to rise at all next year, despite the rising costs of living and higher mortgage repayments.

As a result, we expect mortgage delinquency rates to continue to rise. There will be specific hot spots in the mining belts of Western Australia and Queensland, and we also expect to see problems emerging in the high-rise areas of Melbourne and Brisbane.

Households with a variable rate interest only loan will find their repayments rise more, with a half percent rise in rates translating to a monthly rise in repayments of $146. This illustrates the two problems with interest only loans, first they are more leveraged, so sensitive to rate changes, and second, households still have to find a way to repay the capital. No surprise therefore that the regulators have been forcing the banks to ensure interest only loan holders have a repayment plan, something which many currently do not possess. One third of borrowers could be impacted.

Mortgage finance will still be available, although we expect to see further tightening in underwriting standards, meaning that households will need larger deposits, and will not be able to borrow as much. Remember that our banks rely on mortgage book growth to sustain their business models, so the supply will not be turned off. We also expect to see ongoing lending from the non-traditional banking sector. Recently some of these players have been extending credit – at higher interest rates – to non-conforming loans, and foreign investors. This will continue. Regulation of the non-bank sector needs to be addressed.

We expect property investors to continue to pile into the market, especially in the eastern states, so the volume of investment loans will continue to rise. A high proportion of these will be interest only loans. Given the current tax settings, where negative gearing and capital gains assist investors, many see this as the best investment option, including those in a self-managed super fund.

We expect momentum in owner occupied lending will slow, as the rate of refinancing eases. In the first part of the year, we expect a rise in the volume of fixed rate loans, as households decided to fix at a rate lower than the market’s expectation. But beware, most fixed loans already imply a hike in rates, so many of the best deals have already gone. More households will turn to mortgage brokers for assistance, and we expect they will grow their market share to well above fifty percent.

Foreign investors will still be attracted to the market here, and migration will continue, so we expect to see ongoing support to prices in the main markets of Sydney and Melbourne and they will remain above long term fundamentals.

First time buyers will continue to be squeezed from the market, thanks to higher underwriting standards and flat incomes. A proportion of these households will choose to go direct to the investment sector as a result.

But net-net, demand will remain strong, auction clearance rates will be elevated, and property in many places will be in short supply.

As a result, we think home prices will in most centres continue to rise. We are certainly not anticipating a dramatic fall. This is because supply of new property is likely to slow in line with the fall in building approvals.

There will be specific areas across Australia however where prices are likely to fall. We expect further weakness in Western Australia and Queensland, and also in the apartment markets in Brisbane and Melbourne, as well as across a number of regional centres. But the core Sydney market, and houses in the broader Melbourne and Brisbane markets will remain strong.

We are expecting underemployment to become an important thematic next year. Many households, even those with multiple jobs, are not getting the levels of income they need to maintain their lifestyle. Whilst the core unemployment rate is unlikely to rise significantly, cash flow with be a major issue for many households. As a result, we do not expect to see any significant growth in personal credit – other than in the short-term credit sector, where online origination will stimulate demand. Household mortgage stress will continue to rise.

A number of factors are likely to weigh on household financial confidence next year. Rises in mortgage repayments, flat incomes and rising costs will all take their toll. However, ongoing property price growth, higher returns on bank deposits and higher stock market prices will counteract the drag. We expect property investors and home owners in the eastern states to remain quite bullish, despite depressed rental income growth. However, in WA, QLD and some regional centres, and among those living in rented accommodation, confidence will be significantly lower.

Banks will largely be able to buttress their profits, thanks to improved margins and low levels of mortgage default. As a result, we think the majors will mostly be able to maintain their payouts to their shareholders at current levels. Regional banks will remain under severe pressure, and we are not convinced that their drive to move to advanced capital models will be a panacea. We will also know the required final capital settings from Basel. We expect banks will need to hold more capital, and the benefits of advanced capital models be further reduced.

So in summary, expect higher mortgage rates and delinquencies to slow the property market a little, but momentum in the major centres is unlikely to stall completely because the banks need mortgage book growth to sustain their businesses. As a result, we expect household debit to be extended further.

Finally, a word on the broader economy. Housing momentum is not sufficient to replace the drop-off in mining investment, and given the reluctance of businesses to invest in growth, we think overall growth will still be sluggish. We might get a free kick from higher commodity prices – if they continue – but we do not have a realistic path to sustained growth. This structural issue needs to be addressed, and soon, if in the longer term the property market is to not go into a spiral of decline. However, we do not think 2017 will be the start of that down cycle.