The opening quarter of 2016 was not the greatest three months for Brisbane’s property market and one member of the real estate industry believes the end of the current growth cycle in the city and the wider south east Queensland region is already in sight.

Figures released this week by the Real Estate Institute of Queensland (REIQ) show the median house price in the Greater Brisbane area fell 4% over the March quarter to $480,000, while in the Brisbane Local Government Area, which encompasses the city’s inner suburbs, the median house price fell 2.4% to $620,000.

Speaking to Australian Broker‘s sister publication,Your Investment Property, REIQ chief executive officer Antonia Mercorella said the March quarter was a “slow” one for Brisbane, but she believes there isn’t too much cause for concern.

“Both of those markets, which had been performing consistently well slipped a little bit in the quarter. But that is only one quarter so we do need to be careful not to draw too much from that or sound the alarm bells at this stage,” Mercorella told Your Investment Property.

“Both the LGA and Greater Brisbane have been performing consistently well and if you look at the broader data they’re still tracking nicely,”

According to the REIQ’s figures, the Greater Brisbane median house price has grown 2.1% growth over 12 months to March and 7.8% over the past five years, while in the Brisbane LGA the median house price is up 6.1% over the 12 months to March and 17.9% over the past five years.

Mercorella said figures from the June quarter may too show a softening in Brisbane’s performance due to the impact of the ongoing Federal Election campaign; however she predicts the market will bounce back relatively quickly after the campaign is completed.

While Mercorella believes Brisbane still has plenty of fuel in the tank, Scott Northcott, director of Queensland based Real Property Advice, believes the peak of the current cycle is steadily drawing closer for the Queensland capital.

For Northcott, one of the factors that had breathed life into the south east corner of Queensland will also be its undoing as he predicts a post-Commonwealth Games slump.

“Brisbane will always follow Sydney and Melbourne and precede places like Adelaide, Perth and Darwin, that’s just the order things happen,” he told Your Investment Property.

“In our on the ground experience we have seen very strong price growth activity over the last 24 months and even a bit longer.

“I think we’ve got 18 more months for decent activity and I think after the Commonwealth Games at the end of 2018 we’re going to see quite an abrupt slowdown starting from the Gold Coast area. The Gold Coast will sort of infect upwards from there.”

The REIQ’s figures show over the March quarter that the median house price on the Gold Coast increased 0.5% to $557,500 and is 5.8% higher than 12 months ago and 10.2% higher than five years ago and Mercorella doesn’t believe the end of the Commonwealth Games activity will bring the Gold Coast and surrounding regions to a halt.

“I don’t think that’s going to be the case. Obviously there’s a lot of new construction going on there at the moment and other things because of the Commonwealth Games, but we were already sort of seeing the gold coast bounce back from the GFC anyway,” she said.

“I don’t think it’s going to be this situation that after the games we’re going to be left with this glut of stock and people are going to leave the Gold Coast.”

But Northcott’s outlook for the region is much grimmer, likening the current state of the Gold Coast to that of areas that went from boom to bust during the resource boom of recent years.

“People are chasing the Commonwealth Games boom.

“The big issue is that there’s a whole lot of stuff being built and sold and everybody thinks it’s all rosy, but when investors, both international and local, want to get out post Commonwealth Games they’ll simply dump their stock.

“Twelve to 18 months after the games there will be a bad taste in people’s mouths and then from mid-2020 to 2001 we’ll power on again.”

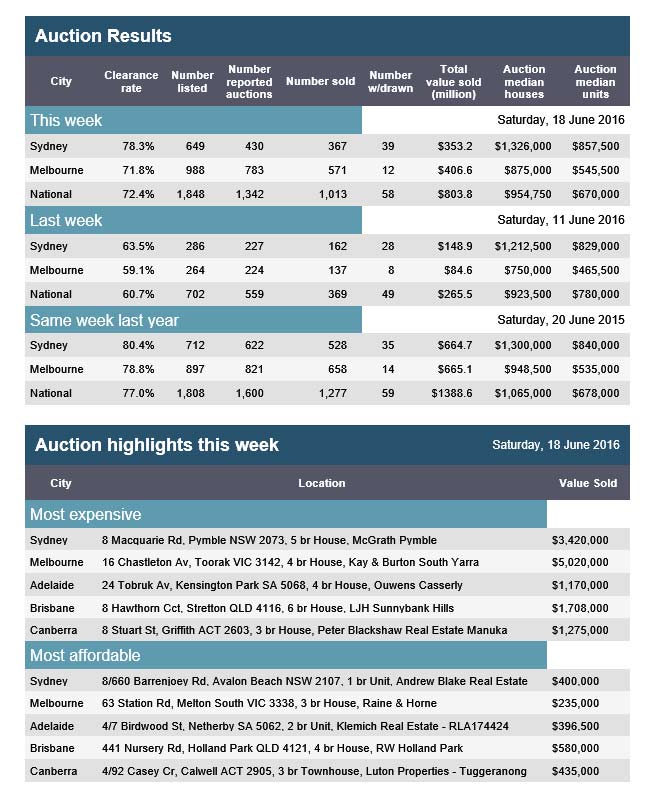

According to the APM Home Price Guide Auction results for 18th June 2016, the national clearance rate was 72.4%, up from 60.7% last week. Sydney led the way with a 78.3% sold, but Melbourne had the largest number of sales. Whilst the results are a little down on last year, its still looking pretty hot at the moment.

APM publishes auction activity results for the Sydney, Melbourne,Brisbane and Adelaide capital cities every Saturday evening, providing a snapshot of how demand and supply in the auction market is behaving and as a leading indicator for the overall property market. (Auction activity for the other capital cities is also monitored and made available by mid week). You can read about their methodology here.

Housing affordability and tax reform have shaped up to be two of the defining issues this election. The Property Council of Australia – which describes itself as “the Voice of Leadership” – has helped frame the debate on behalf of its 2200 company members.

The council began as the Building Owners and Managers’ Association of Australia (BOMA) in 1969, and was renamed the Property Council of Australia in 1996, with advocacy a core focus. The Residential Development Council and International and Capital Markets division were formed in 2001 and the Retirement Living Council in 2015.

With a board of directors drawn from Australia’s largest residential and commercial developers, the Property Council’s considerable annual revenue (A$27.3 million in 2015) is drawn primarily from membership fees and services.

The financial stakes are high when it comes to lobbying for regulatory settings which favour property development and investment. The Property Council’s healthy budget for advocacy and communication ($6.4 million and $1 million in 2015 alone) has generated a voluminous amount of reports, advertising campaigns and government submissions on taxation and planning reform. Another $7.2 million for “networking” ensures that this information is disseminated where it counts.

These deep coffers have funded the Council’s high profile television campaign to preserve negative gearing and capital gains tax discounts in response to mooted changes early this year. Likening the housing market to a fragile house of cards on the brink of collapse, the ad (released on 22 February) carried a menacing warning, “don’t play with property.”

The government has got the message. The Treasurer, Scott Morrison, who served as National Policy and Research Manager for the Council between 1989-1995 ruled out changes to negative gearing in the lead up to the 2016 Budget. Despite speaking out against negative gearing prior to becoming Prime Minister, Malcom Turnbull also changed his tune recently, rejecting “reckless” changes to existing arrangements and suggesting that aspiring home buyers hit up their parents for help.

While the campaign to retain negative gearing is the Property Council’s most visible, behind the scenes the council has been busy meeting with government and writing submissions. In 2015 alone, the NSW division wrote 55 submissions and attended an extraordinary 230 government meetings. Its 2016 election brochure presents a number of “solutions” to “grow the economy through property”. Here are some highlights.

Negative gearing and the CGT

The council wants to retain negative gearing (which allow interest rates and other expenses associated with housing investment to be offset against total income) and capital gains tax discounts on investment properties. This is despite substantial evidence that these bonuses stimulate demand for housing, pushing up prices and leaving first home buyers unable to compete. But by framing housing affordability problems as a symptom of supply side pressures rather than demand side incentives, the council shifts the affordability debate to planning reform.

Housing and planning reform

Current incentives for property investment (such as negative gearing) don’t target new housing supply – only a small proportion of investor loans finance new dwellings. So the Council argues that Commonwealth payments to the states for “micro economic reform” should incentivise planning system changes needed to “turbocharge housing supply pipelines and deliver innovative affordable housing solutions.”

This is a tired argument which ignores the years of planning reform already undertaken by the states and territories, while levels of new housing production are currently at their highest in decades. This supply has done little to dampen price inflation in a market awash with domestic and foreign investors.

While the Property Council always bangs on about bottlenecks in housing supply (which it argues are caused by planning system constraints), such arguments miss the obvious issue that prices are a result of an interaction of supply and demand. What the combination of negative gearing and capital gains tax do is to drive demand so hard in boom times that even with sharp increases in supply, prices keep on rising, especially in today’s low interest environment.

The chart below shows this problem with respect to Sydney. It shows dwelling completions falling slowly when prices flatlined after the 1996-2004 boom, but rising in line with price inflation from mid 2011 on.

Prices: Department of Family and Community Services, Rent and Sales Report.Source: Completions. NSW Department of Planning, CC BY-SA

The Council’s election platform does call for institutional investment in affordable and social housing, and this is one idea worth taking up.

Cities and Infrastructure

The Property Council support long term infrastructure planning and delivery, coordinated by Infrastructure Australia. Who doesn’t?

But the problem is how to assign the costs and benefits. Land value rises due to investments in public infrastructure – such as a new rail line or road – are typically pocketed by landowners and developers.

Commonwealth and state governments are now canvassing value capture arrangements which would use some of this uplift to offset costs of provision. The council oppose this model, instead suggesting Tax Increment Financing (TIF), which leverages increases to commercial rates in defined districts.

While popular in some parts of the US, it has not been proven effective for larger schemes. It would be difficult to implement in Australia because our recurrent property charges are much lower than the US.

The Property Council also wants existing development contributions towards basic facilities like open space, local roads, and footpaths to be wound back, along with stamp duties on property transactions.

The idea of removing stamp duty has some merit (at least for domestic purchasers), since taxes on property transactions can discourage mobility, deterring retirees from moving to a smaller home, for example. But experts think stamp duty should be replaced by land taxes, to encourage more efficient use of land.

This would also provide a mechanism for capturing back values arising from public infrastructure investment. Not surprisingly, the Property Council thinks otherwise, calling instead for a higher GST.

While the Property Council complains about unfair tax burdens on its members, they seem content to spend a lot of money on their advocacy and networking activities. Described by economists as “premium seeking expenditure”, lobbying for more generous regulatory and financial settings clearly promises a high return for the property sector.

But it’s important to remember that despite their size, the Property Council only represents a portion of the development, construction, and real estate industry – they don’t really cover many smaller suburban developers or house builders. The question is whether the “Voice of Leadership” will dominate the agenda or whether wider perspectives on housing and cities will be heard.

Authors: Nicole Gurra, Professor – Urban and Regional Planning, University of Sydney; Peter Phibb, Chair of Urban Planning and Policy, University of Sydney

We see their spokespeople quoted in the papers and their ads on TV, but beyond that we know very little about how Australia’s lobby groups get what they want. This The Conversation series shines a light on the strategies, political alignment and policy platforms of eight lobby groups that can influence this election.

Excellent post from Cameron Kusher, CoreLogic RP Data, discussing the impact of the higher tax being imposed by several states on foreign investors in the context of state tax raising – they are highly dependent on stamp duty to support their coffers. He concludes that ultimately these changes may deter some foreign investment but these changes are not going to scare off all foreigners from investing in housing market. At the same time it will raise much needed revenue for these governments. If state governments are looking at taxes on property, they should move away from stamp duty to a more efficient land tax.

The state governments of New South Wales, Victoria and Queensland are all now charging additional tax on foreign investment in residential property. In New South Wales foreign buyers are being charged a 4% stamp duty surcharge from June 21. In Victoria, foreign buyers are charged a 7% tax and in Queensland foreign buyers are being charged a 3% surcharge. All three of these taxes are specifically targeted on transactions of property by foreign buyers.

Property (both residential and non-residential) is already the largest source of taxation revenue for state and local government. These additional charges to foreign investors in the three most populous states will probably raise additional revenue (as long as the higher cost of doing business doesn’t result in a downturn in demand from overseas buyers). For each government there is a benefit in these changes outside of additional revenue, foreigners don’t vote so politically it is likely to be a fairly popular decision. Especially in New South Wales and Victoria where housing affordability is a growing problem and there is a perception that foreign investors are bidding up prices and contributing to locking first home buyers out of the market.

In New South Wales, state and local governments collected $14.705 billion in property taxes over the 2014-15 financial year. Property tax revenue increased by 12.8% over the year and has increased by 80.5% over the decade to 2014-15. Property taxes accounted for 48.5% of total taxation revenue to New South Wales state and local government in 2014-15.

In Victoria, state and local governments collected $12.246 billion in property taxes over the 2014-15 financial year which accounted for 53.1% of total taxation revenue. Property tax revenue increased by 10.7% over the 2014-15 financial year to be 109.9% higher over the past decade.

Queensland property tax revenue increased by 12.6% over the 2014-15 financial year to be 80.7% higher over the decade. Over the 2014-15 financial year Queensland state and local governments collected $8.267 billion in property tax revenue which accounted for 51.5% of total state and local government tax revenue.

Over the decade to June 2015, property taxes have increased by 80.5% in New South Wales, 109.9% in Victoria and 80.7% in Queensland, over the same timeframe inflation has increased by 30.1% which is significantly lower than growth in property taxation.

Given the importance of property tax revenue to state and local governments it is no wonder that the three largest states have decided to increase taxes on foreign investment. These changes don’t impact on voters and they collect additional much needed revenue.

My concern is that it shows that none of these states have any intention of moving away from transactional taxes on property to more efficient land taxes. Keep in mind that in a typical year only around 5% to 7% of residential properties are transacting so you are only collecting stamp duty from a small proportion of the housing market that are deciding to move. When transactions and values slow or fall, stamp duty revenue is also susceptible to large declines.

In New South Wales and Victoria, governments are gaining substantial revenue from stamp duty as property values and transactions rise. In New South Wales, stamp duty collection rose 22.2% in 2014-15, in Victoria it rose by 18.9% and in Queensland it was 12.3% higher. Over the past decade, the total increase in stamp duty revenue has been recorded at: 125.1% in New South Wales, 116.8% in Victoria and 56.1% in Queensland.

Some of the commentary around the increases in tax have been around the fact that without foreign investors many of the new housing (particularly unit) projects would never have even commenced construction. To me, this is really the crux of the problem. As the resource investment boom has faded to some extent housing construction has helped to fill the void. If a projects viability is totally dependent on foreign demand, to me that suggests that it is not really a viable project. The reality is that the current home value growth phase has now been running for four years and new housing construction and unit construction in particular has hit record highs. Foreign investment has increased quite significantly over this time however, many of these purchasers are buying units which many locals wouldn’t purchase due to the size, location and price of these properties. Furthermore, anecdotally many of these properties don’t actually create additional housing because they are left empty and not made available for rent.

I believe that these additional charges will provide some deterrent for foreign buyers investing as the costs continue to add up with FIRB application fees and now these additional charges. Of course, while these changes may deter some investors other will just see it as a cost of doing business and it shouldn’t impact them too much if they are investing for the long-term. If fewer foreign investors results in some new housing projects not going ahead, that is not necessarily a problem either in light of the fact that housing supply has increased dramatically over recent years and will continue to do so over the coming years given the housing currently under construction. Finally if it means that certain developers decide to rotate their offering away from one catering to foreign buyers and towards one which is more palatable to a local market, I believe that is a good thing.

Ultimately these changes may deter some foreign investment but these changes are not going to scare off all foreigners from investing in housing market. At the same time it will raise much needed revenue for these governments. If state governments are looking at taxes on property I would once again call on them to look for a way to move away from stamp duty to a more efficient land tax.

The New South Wales government is after a bigger slice of the overseas investment flooding into Sydney’s booming property market, with treasurer Gladys Berejiklian announcing today that next week’s state budget will include foreign investor surcharges on stamp duty and land tax on residential real estate.

A little over 20% of property in Australia is sold to foreign investors.

NSW is now the third east coast state to look at foreign investment to boost state coffers after Victoria increased the surcharge for foreign buyers of residential property from 3% to 7% in its April budget. The change comes into effect from July 1. Victoria also trebled its land tax surcharge on “absentee landholders” from 0.5% to 1.5%.

Treasurer Tim Pallas expects it will deliver an additional $486 million in revenue over the next four years. The move comes after the introduction of the 3% surcharge appeared to have no impact on demand, despite predictions to the opposite from the real estate industry.

Last week Queensland’s Labor government announced its own 3% transfer duty surcharge.

Treasurer Curtis Pitt says the move will generate around $25 million for the state annually, adding about $14,000 to the price of the average $475,000 price of a Queensland home.

NSW treasurer Gladys Berejiklian will add a 4% stamp duty surcharge on residential property bought by foreign purchasers, plus 0.75% land tax surcharge for foreign owners from the 2017 land tax year.

She expects the move to generate $262 million in total next financial year and more than $1 billion over four years.

“The Victorian experience has demonstrated that the measures have not had an adverse impact on the property market,” Berejiklian said.

“These new measures will ensure NSW’s property market continues to be an attractive destination for international investors while making sure that we are able to fund vital services into the future.”

Under the changes, foreign investors will no longer be entitled to the 12-month deferral for the payment of stamp duty for off-the-plan purchases of residential property and will not get the tax-free threshold for the land tax surcharge.

The Property Council of Australia has been vociferous in its opposition to the surcharges, last week accusing the Queensland government of breaking its promise from 12 months ago not to introduce a surcharge, and turning its back on investors, claiming it would cost jobs.

Today, Scott McGill from Pitcher Partners Sydney claimed that Victoria was starting to see foreign investors pulling out of the market, and international developers scaling back on land acquisition.

Amid tightening lending restrictions, recent National Australia Bank data revealed foreign buyers of new property in Victoria in the March quarter slumped to their lowest since 2014.

McGill claimed the NSW decision would push up the price of property for everyone.

“Government can’t afford to come in with a knee jerk reaction to foreign investment without considering the downstream effects,” he said.

“You run the real risk of restricting supply and pushing up real estate prices – which is the last thing Sydney needs.”

McGill said it was “far too simplistic” to argue foreign investors were pricing local buyers out of the market.

“Higher taxes on foreign investors will not improve housing affordability, but rather it will undermine new supply coming on board,” he said.

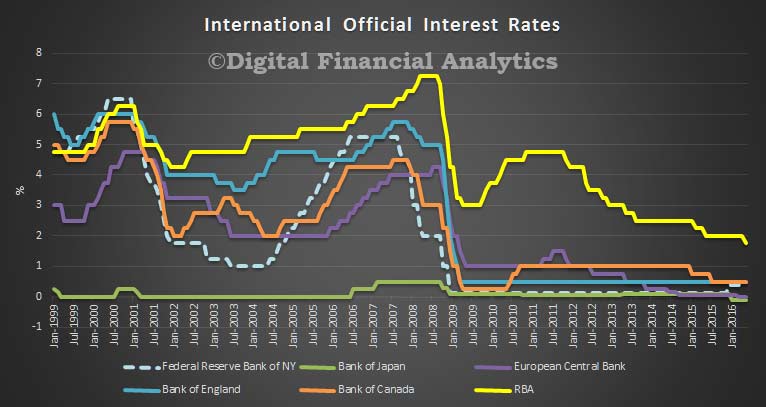

The RBA statistical release shows the relative policy rates in US, UK, Canada, Japan, ECB and Australia. Looking at the rates from 1999, we see that since the GFC rates have been lower, thanks to unconventional monetary policy. In contrast to other countries, the Australian cash rate has remained higher, for longer, but is at a record low. Will it fall further?

Yahoo7News reports that according to 1300HomeLoan managing director John Kolenda, who last year accurately warned banks would lift their mortgage rates out-of-sync with the Reserve Bank, said the current official rate of 1.75 per cent would be the “new norm”.

The Reserve sliced rates to 1.75 per cent – the lowest level on record – last month over fears about the level of inflation. Prices have been dropping for several months across the country with deflation a real threat in Perth.

Mr Kolenda said consumers were now more sensitive to the impact of higher interest rates which meant taking them back to what was once considered normal was unlikely.

“We are unlikely to see official interest rates move to pre-global financial crisis (GFC) levels and the standard norm of the future will be lower than historical levels for the next decade,” he said.

“The monetary policy game has changed and the RBA has found cutting its cash rate is not necessarily an instant remedy for economic stimulus.

“Conversely, any time the RBA increases official rates in the future could have a disastrous impact on consumer confidence and the economy. Consumers are now very rate sensitive and when they rise they are likely to stop spending and revert to saving.”

Markets are pricing in another interest rate cut by the end of the year although economists believe the Reserve’s next move will be a rate increase.

Mr Kolenda said there was a real prospect the Reserve would cut rates again.

So, on one hand, there are good reasons to expect the RBA to cut further, and keep rates low for a long time. On the other, the property market is alive and well, and will be a handbrake on further cuts.

We expect out of cycle rate hikes for many mortgage holders, once the election is passed as lenders attempt to repair their margins, and we are less convinced the RBA will cut again anytime soon, give the current property trends – in fact, we need more macroprudential controls, not lower interest rates. That said, the medium term outlook is for rates to stay low for a long time, and this does mean large mortgages will continue to be serviced as current levels. But any hike in rates would have significant negative impact on households and the economy, given the sky-high debt levels in place at the moment.

According to CoreLogic RP Data, the number of capital city auctions held this week was 1,053, falling significantly given most states and territories have a public holiday today. Preliminary results show that 67.2 per cent of auctions were successful this week, compared to 68.2 per cent last week across 2,008 auctions and 75.9 per cent one year ago, across 2,076 auctions. Since the end of March this year, the combined capital city auction clearance rate has been trending around the high 60 per cent mark, demonstrating an improvement when compared to the end of 2015, however consistently tracking lower compared to the same time last year when across the combined capitals, clearance rates were in the mid to high 70 per cent range.

The latest data from the ABS on home lending for April 2016 indicates that overall lending flow fell in trend terms by 0.3%. But within that, owner occupied lending fell 0.5% while investment housing commitments rose 0.2%. In other words, we are seeing a rotation back towards the investment sector. Since then, several banks have relaxed their investment lending underwriting criteria, and have started to offer bigger discounts. The picture is quite complex.

In seasonally adjusted terms, the total value of dwelling finance commitments excluding alterations and additions fell 1.8%. But we will stick to the trend data, which irons out some of the bumps.

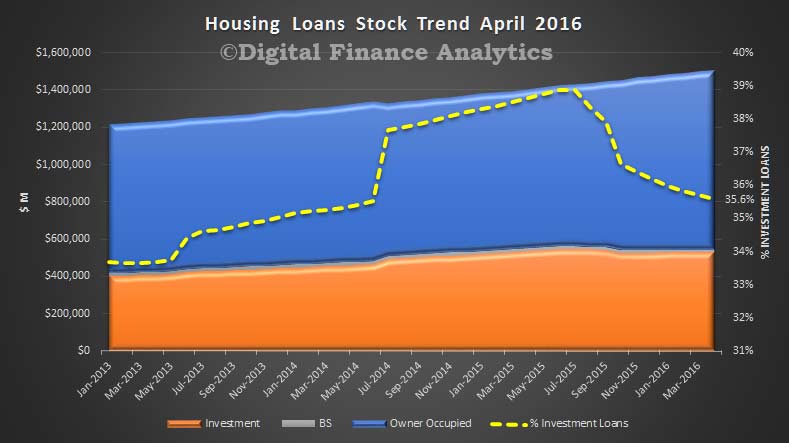

Looking at the overall stock of loans, it rose again to $1.49 trillion, we see that investment loans comprise 35.6% of all loans, still high

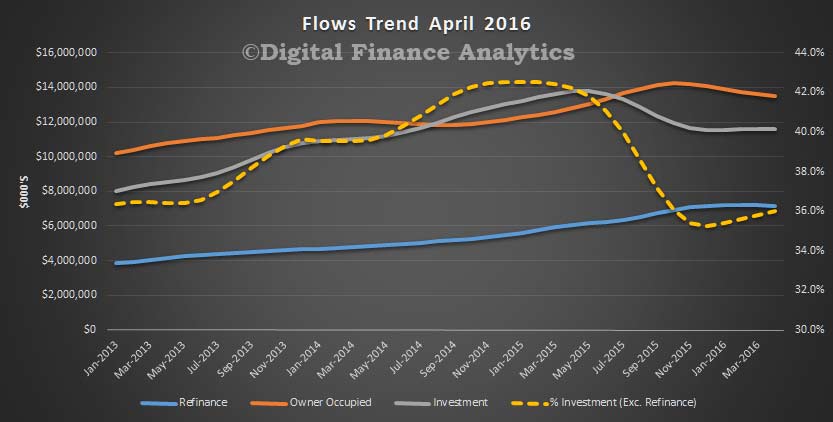

Looking at the monthly flows, we see a fall in owner occupied new loans by value, and a small rise in investment loans. The momentum in the refinance sector has slowed a little, but rose as a proportion of all loans.

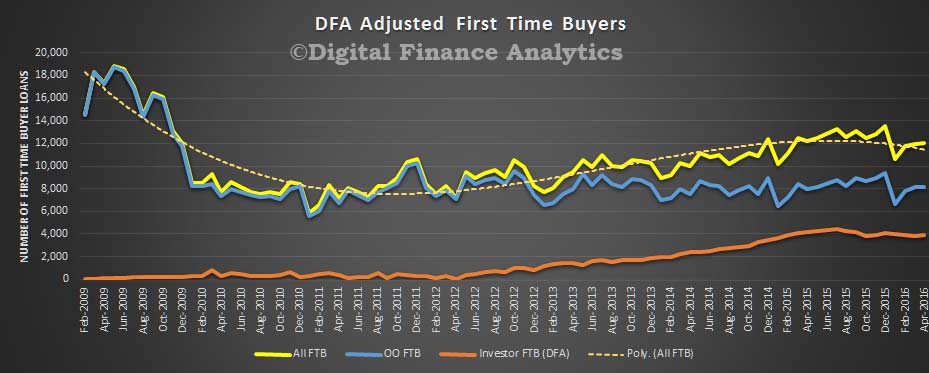

Turning to first time buyers, we a rise in the number of new owner occupied and investor loans, together the show around 10,000 new first time buyers entering the market. This is an original, not trend data set.

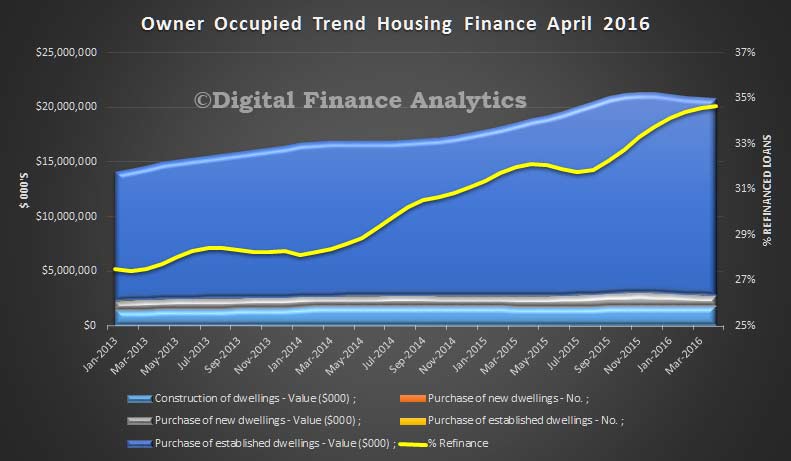

The largest volume of owner occupied loans was for the purchase of established dwellings, and to total value fell. The proportion of loans refinance rose again, to nearly 35% of all loan values.

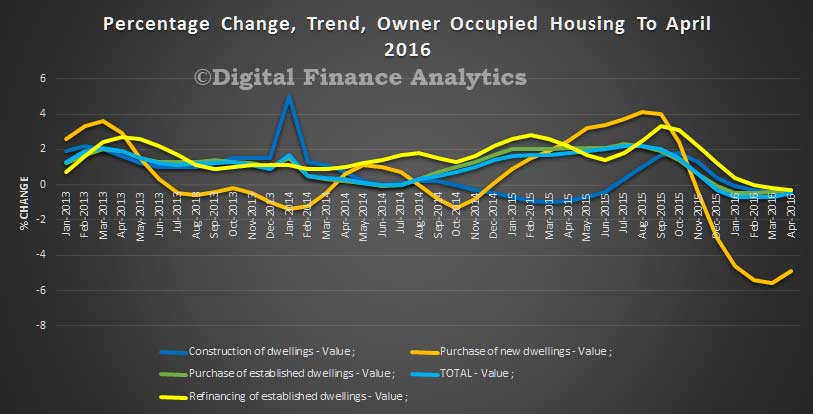

Looking at owner occupied loans, the purchase of new dwellings has risen a bit, but is still 4% lower whilst other types of borrowing are relatively static.

By state owner occupied loans grew the strongest in ACT and VIC, whilst TAS showed the largest fall.

Finally, looking at lender type, we see that the non-banks grew the strongest (up 0.8%), building societies lost momentum (down 7%), and banks lent slightly less thin month (down 0.7%).

From CoreLogic RP Data. Despite the recent slowdown, housing finance data highlights that investor activity in the housing market is starting to rise again and when you look at total returns from housing it’s no surprise.

The CoreLogic RP Data Accumulation Index which has been published since June 2009 highlights the total returns from residential property. The total returns include both the increase in values as well as gross rental returns.

The first chart shows the annual change in the total returns (accumulation) index over time. While combined capital city home values recorded longer and deeper falls during 2011-12, total returns were negative for only a short period of time thanks to the uplift from rental yields. More recently you can see that the annual change in total returns across the combined capital cities has remained quite strong.

Combined capital city annual changes in total returns for houses and units

Over the 12 months to May 2016, combined capital city home values have increased by 10.0% while total returns have been recorded at a higher 13.9%. Looking at the individual capital cities, all cities except for Perth have recorded positive total returns over the past year. Sydney and Melbourne which have been the most active investment markets have seen the highest total returns at 16.9% and 17.5% respectively over the past twelve months. It should be noted that gross rental returns in both of these cities are now at record lows highlighting that the majority of these returns have come via an increase in home values.

Annual change in capital city total returns, 12 months to May 2016

The third chart highlights the total returns over the past five years across all capital cities. Again, Sydney in particular, has seen far superior total returns compared to all other capital cities. Melbourne has also experienced relatively strong total returns over the past five years. Again this highlights why these two cities in particular have remained so popular with investors. In all other capital cities returns from residential property have been positive. In many of these cities the total returns have been driven more so by the rental returns rather than the capital growth which has been the key driver in Sydney and Melbourne.

5 year total change in total returns, to May 2016

Despite the recent rebound in value growth, the mature capital growth cycle and record low rental returns in Sydney and Melbourne, total returns are unlikely to be as strong in these cities over the coming years. A more balanced investment approach which focusses on moderate capital growth and relatively strong rental returns is likely to be a superior housing investment profile over the coming years. This data also highlights why housing investment has been so popular. In a low interest rate and subsequently low return environment housing has, over recent years, offered attractive returns. Whether this continues to be the case remains to be seen.

New rules affecting foreign student visas, which go into effect from 1 July 2016, will be a boon for the property market, especially in Sydney and Melbourne.

The Simplified Student Visa Framework (SSVF) aims to “support the sustainable growth of Australia’s international education sector” by reducing red tape. Key changes under the SSVF include reducing the number of student visa subclasses from eight to two and introducing a simplified single immigration risk framework for all international students.

The head of Australia for Chinese property portal, Juwai.com, Gavin Norris, said the new framework is positive for the Australian housing market.

“Six out of every 10 Chinese property buying inquiries made in Australia last year were related to education,” Norris said.

“Juwai.com sent about AU$1.6 billion of property buying inquiries to Australian vendors last year, and almost $1 billion of that value came from families who wanted to buy homes for their children to live in while studying here.

“Anything Australia does to increase the number of Chinese students will also increase investment in strategic areas of the real estate market that generates more construction jobs, more new housing being built and more economic growth.”

Last year, Chinese students made up 1 out of every four international students in Australia, and international students support about 130,000 jobs, according to research from Juwai. Norris said these statistics demonstrate the invaluable contribution foreign students have on the Australian economy.

“When Australia wins a foreign student, it gains tens of thousands in education fees, additional tens of thousands in retail and services spending, hundreds of thousands in a potential real estate investment and – most important of all – the possibility that highly educated individual will decide to stay and work here and contribute to our economy over the long term,” he said.

“Every student who might have come here, but doesn’t, could represent substantial lost benefits.

“The reverse is also true. Anything that discourages international property investment also risks causing adverse impacts the education industry.”

Norris has also praised other SSVF changes, which include trialling visa applications in Mandarin and trialling 10-year student visas.

“These visa changes are smart, and help Australia catch up to nations like the US, which offer similar visa terms.

“The most important elements are the Mandarin language applications, the 10 year validity pilot and the simplified paperwork.

“For the most part, these changes are about avoiding the loss of our privileged place as a destination of choice for overseas students, rather than beating the competition,” Norris said.

Yahoo7News reports that according to 1300HomeLoan managing director John Kolenda, who last year accurately warned banks would lift their mortgage rates out-of-sync with the Reserve Bank, said the current official rate of 1.75 per cent would be the “new norm”.

Yahoo7News reports that according to 1300HomeLoan managing director John Kolenda, who last year accurately warned banks would lift their mortgage rates out-of-sync with the Reserve Bank, said the current official rate of 1.75 per cent would be the “new norm”.

Looking at the monthly flows, we see a fall in owner occupied new loans by value, and a small rise in investment loans. The momentum in the refinance sector has slowed a little, but rose as a proportion of all loans.

Looking at the monthly flows, we see a fall in owner occupied new loans by value, and a small rise in investment loans. The momentum in the refinance sector has slowed a little, but rose as a proportion of all loans. Turning to first time buyers, we a rise in the number of new owner occupied and investor loans, together the show around 10,000 new first time buyers entering the market. This is an original, not trend data set.

Turning to first time buyers, we a rise in the number of new owner occupied and investor loans, together the show around 10,000 new first time buyers entering the market. This is an original, not trend data set. The largest volume of owner occupied loans was for the purchase of established dwellings, and to total value fell. The proportion of loans refinance rose again, to nearly 35% of all loan values.

The largest volume of owner occupied loans was for the purchase of established dwellings, and to total value fell. The proportion of loans refinance rose again, to nearly 35% of all loan values. Looking at owner occupied loans, the purchase of new dwellings has risen a bit, but is still 4% lower whilst other types of borrowing are relatively static.

Looking at owner occupied loans, the purchase of new dwellings has risen a bit, but is still 4% lower whilst other types of borrowing are relatively static. By state owner occupied loans grew the strongest in ACT and VIC, whilst TAS showed the largest fall.

By state owner occupied loans grew the strongest in ACT and VIC, whilst TAS showed the largest fall.