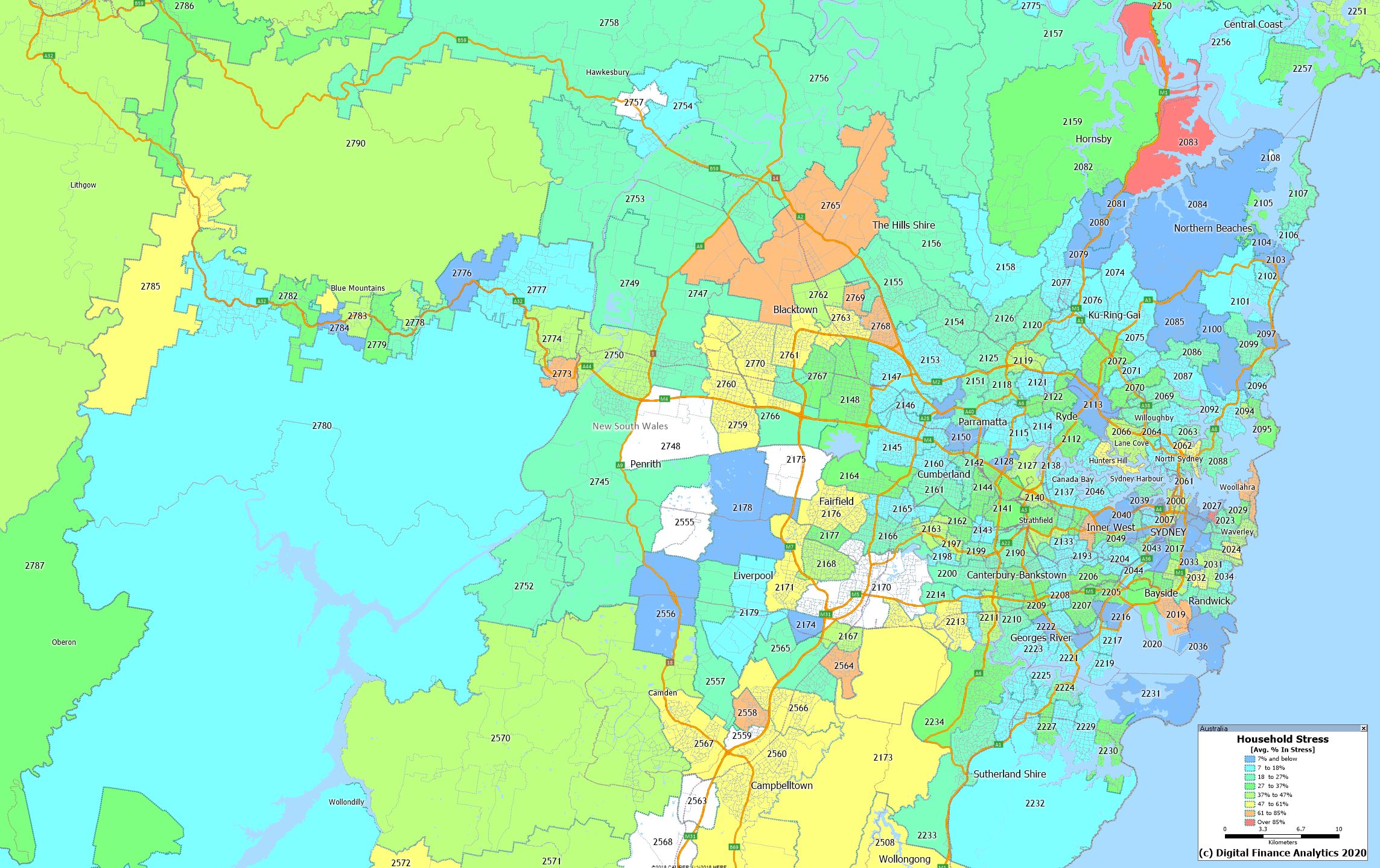

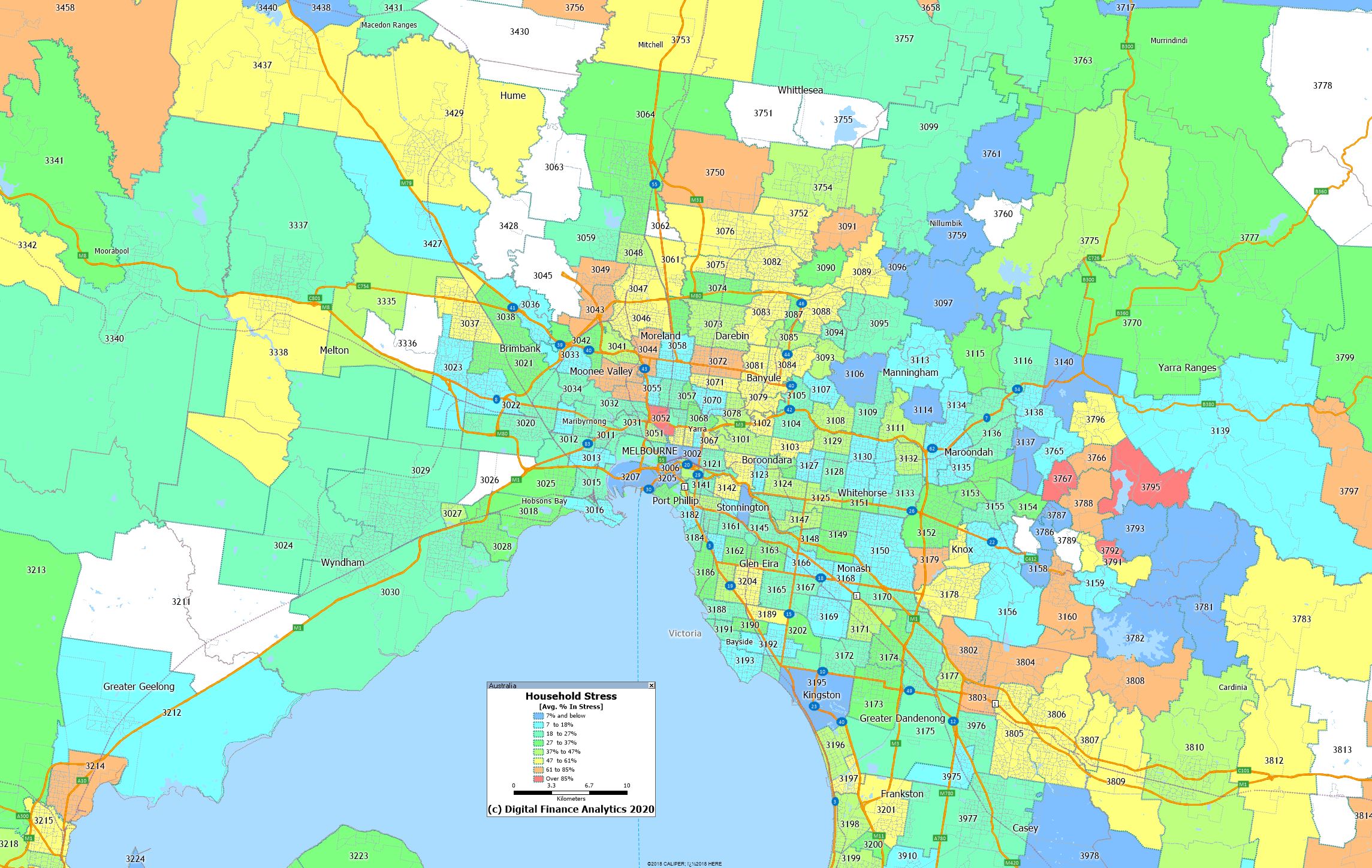

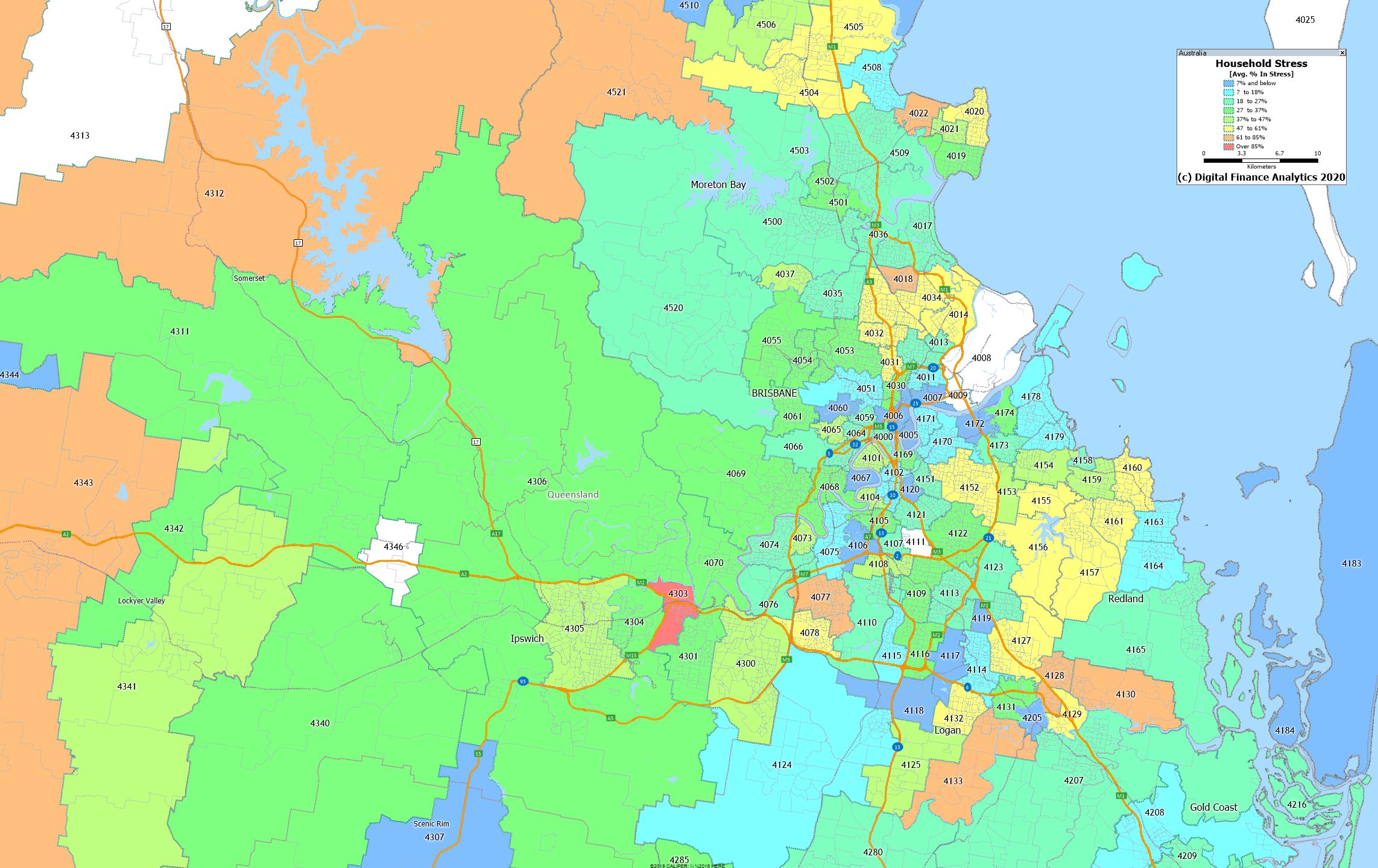

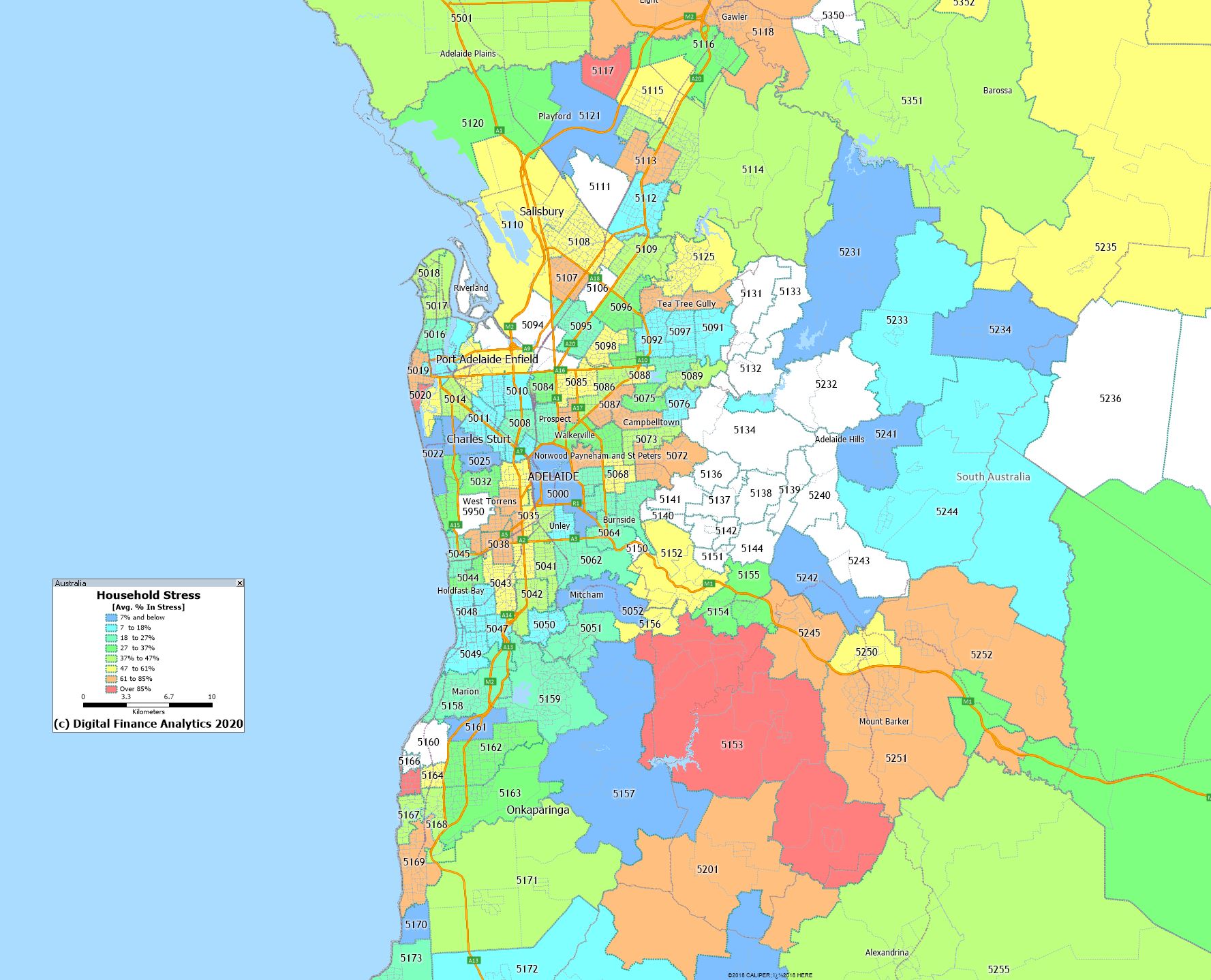

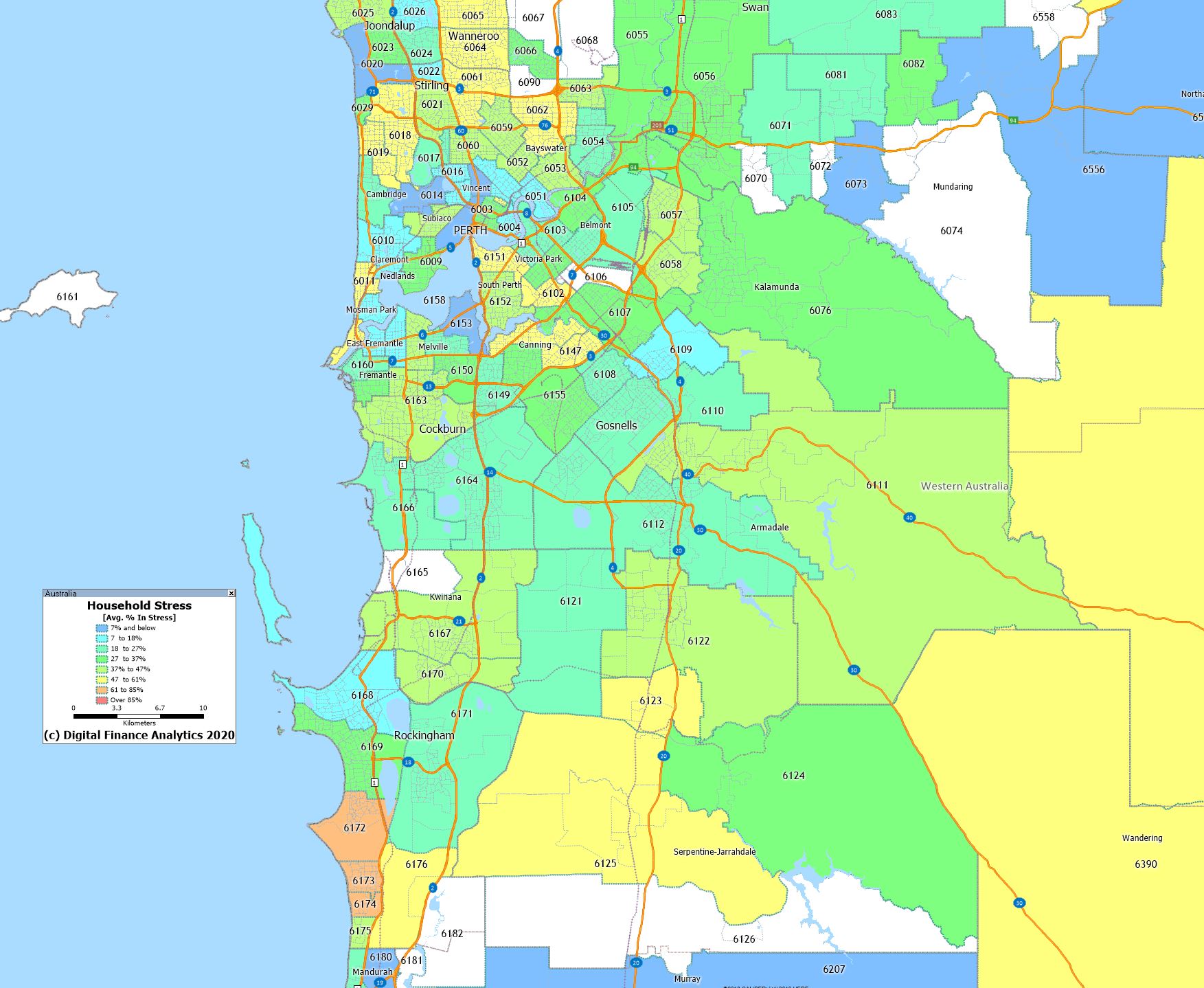

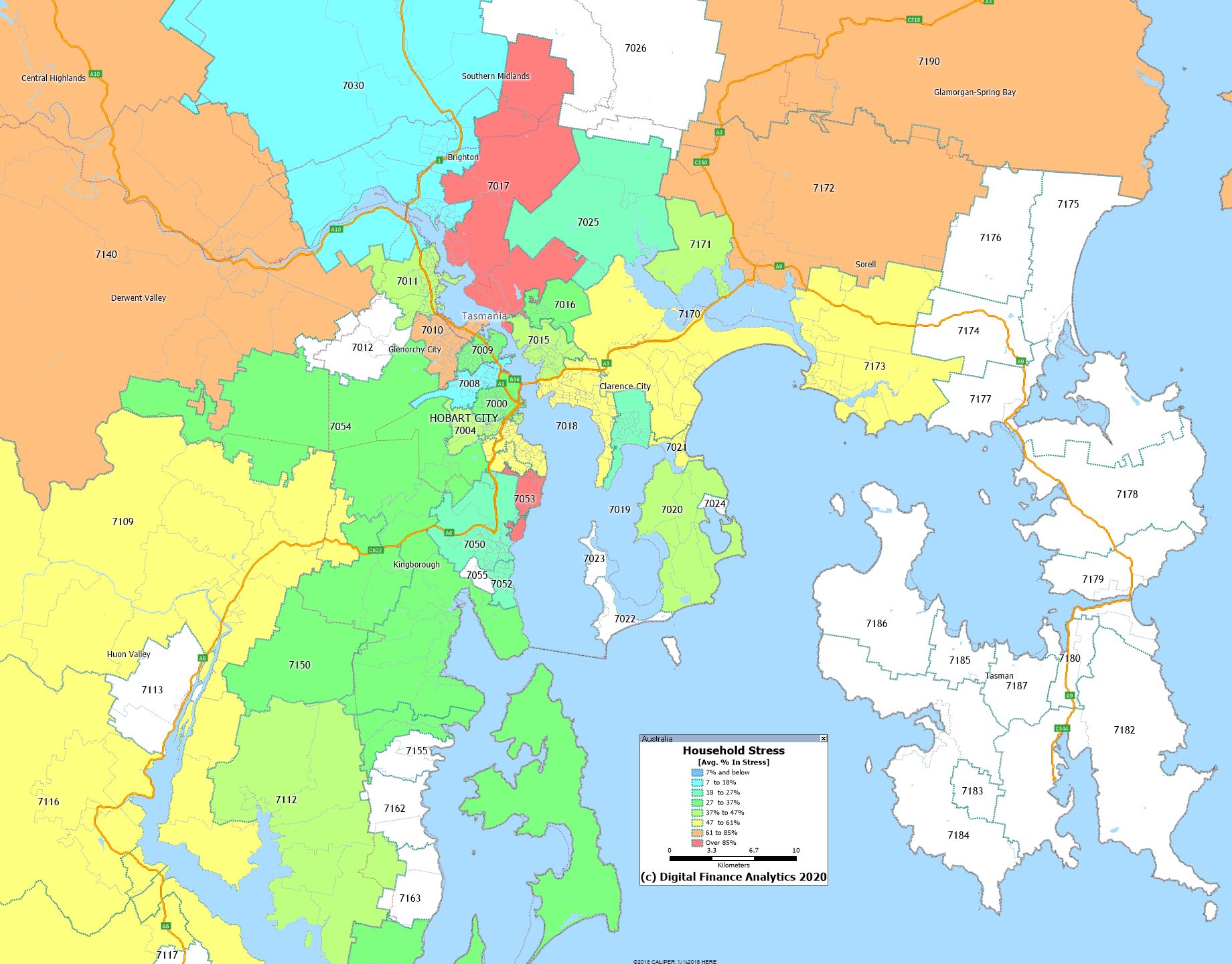

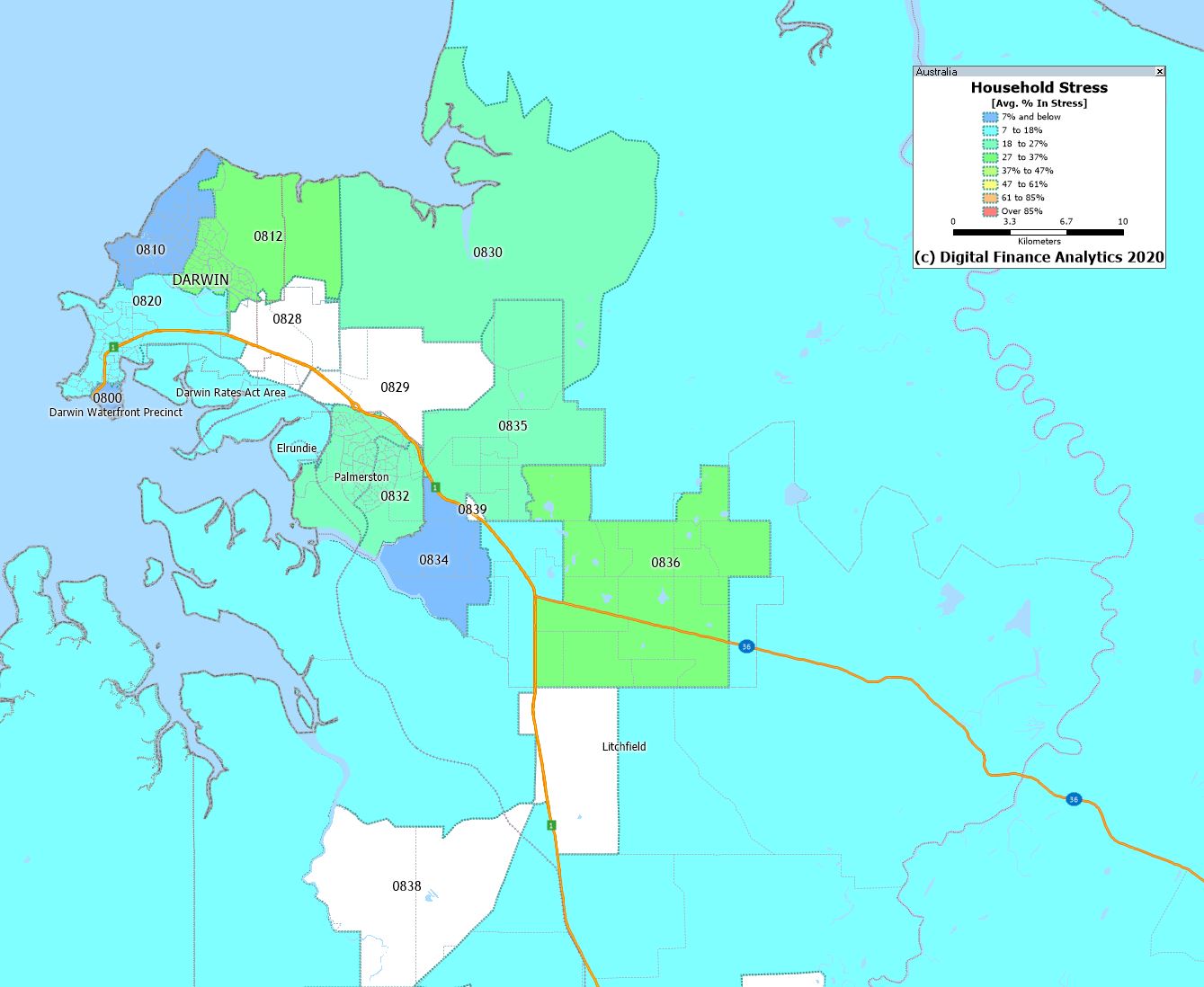

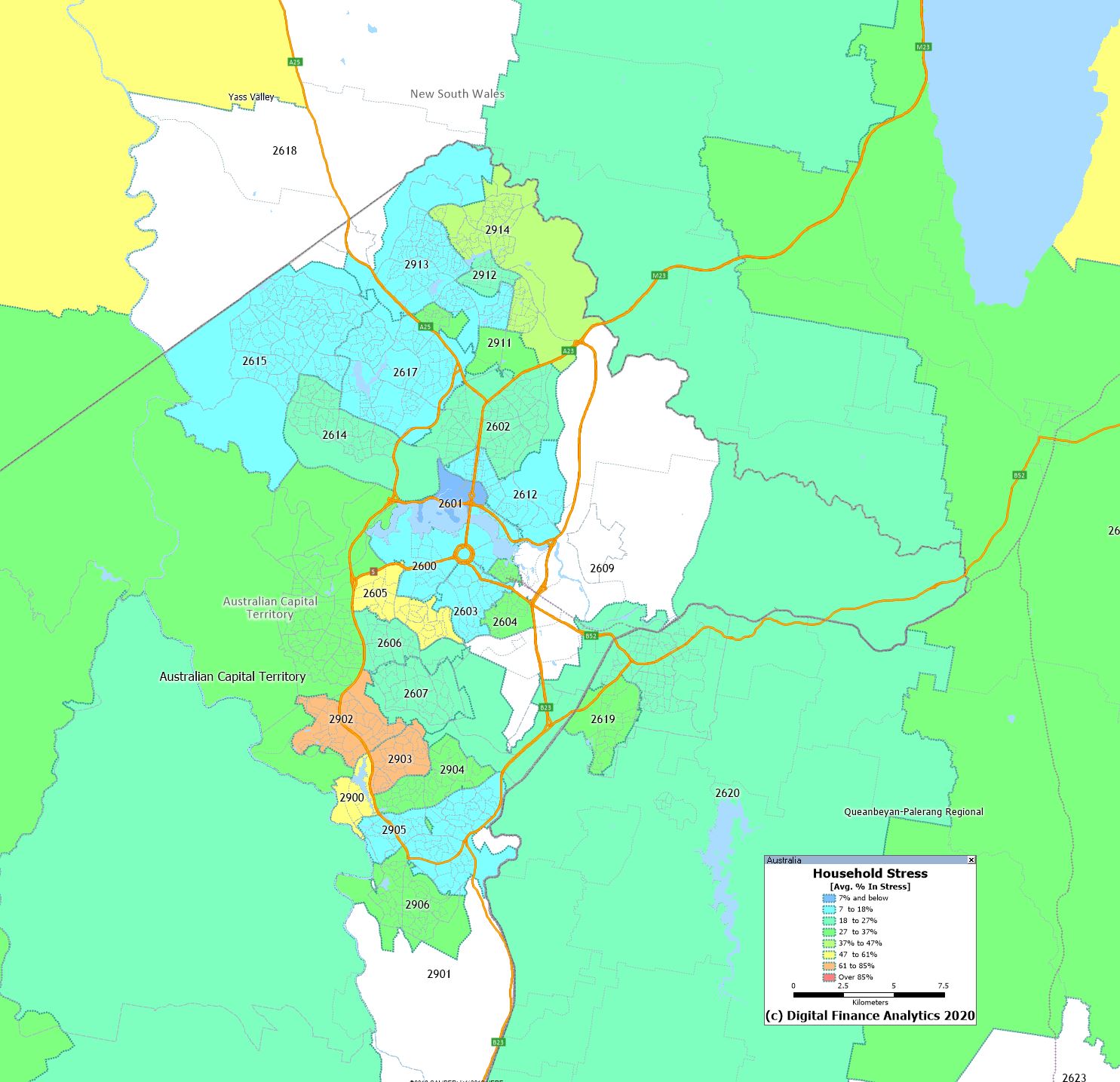

We have had many requests for updated mortgage stress maps, so today we include the latest post code level analysis – with data to end January 2020. We as showing the proportion of households in each state in stress, centered on the main urban centres. You can click on the maps to load and view the original capture.

Economist John Adams and Analyst Martin North discuss the Queensland economy with Campbell Newman, who was at the helm of the state during an attempt to get debt under control.

What happened, and what does this tell us about community expectations, and their appetite for ever more debt?

In our survey of 600 private renters in

different areas of Sydney and Melbourne, we asked: “Many people are

renting privately for longer periods (10+ years). Do you think this is a

positive trend?”

About a third responded in mainly positive terms. Their main reasons were:

For a more in-depth understanding, we

interviewed 60 long-term private renters in low, medium and high-rent

areas in Melbourne and Sydney. Almost all who chose to rent mentioned

flexibility as a key advantage.

“Choosers” highly valued the freedom to move or travel at will. Zygmunt Bauman’s concept of liquid modernity highlights the increasing desire for transience. As he explains:

Transience has replaced durability at the

top of the value table. What is valued today (by choice as much as by

unchosen necessity) is the ability to be on the move, to travel light

and at short notice. Power is measured by the speed with which

responsibilities can be escaped. Who accelerates, wins; who stays put,

loses.

Renters in their own words

Patricia*, who lives in a high-rent part of Melbourne, has always rented.

Well since I came to Australia in 1977, I

rented. I didn’t want to buy. Got close [to buying] a couple of times,

but changed my mind.

I just travel anywhere and everywhere. I

thought […] if you’ve got a house you’re stuck there, and I thought, no.

I work hard for my money, so that money that I work hard for is for me,

not to have a [permanent] roof over my head. […] Renting has been good

for me because I can still do what I want.

Myra lives in a studio apartment in a

high-rent area in Sydney and has no desire to own a home. She is single,

in her mid- to late 30s, and earns well. The possibility of being asked

to vacate did not bother her.

Maybe I’ve been lucky, but every situation

has always sorted itself out. You know a lot of people would have

freaked out if they had to move out […] It didn’t concern me in the

slightest, yeah. I mean not at all. There’s always somewhere to stay. So

it suits my lifestyle. I wouldn’t want to buy [a property], even if I

had the money.

Leanne inherited a third of a house.

Rather than using the proceeds to buy a property, she decided to move to

Melbourne’s inner city (a high-rent area) and continue renting.

So I thought rather than put money into a

house […] I would invest it and I could travel and go to concerts and

live the life I wanted to lead, so that’s basically what I did and I’m

still renting.

Pam was renting in a low-rent area in outer Sydney. She felt her situation required the flexibility of renting:

The relationship was rocky and you can’t predict the future, but I knew it wasn’t going to end up in marriage and kids and all that kind of crap […] We were both working, both earning good money and we could have afforded to buy a house between us […] But for me it was like, no. I don’t know where this [her relationship] is going, so no way, I’m not going to put myself in that predicament and then have to go through court to go, “This is mine, this is yours”, all that crap. But so it was my choice to rent and to stick to it […] I’m not going to rely on anybody else for anything, no way.

Her renter status allowed Pam to make a rapid, clean break.

I just got up one day and walked cos I

knew he was going to ask me to marry him the next day, so I said: “I’m

just going to go to the shops to get a packet of cigarettes.” I left

everything behind. I went for a walk, never went home.

For the families with children who choose

to rent long-term, the key reason is it allows them to live in highly

desirable areas where they cannot afford to buy. Gabrielle and her

partner earn well and live in a high-rent area in Sydney:

Sure it [home ownership] provides you with

security and you don’t have that stress of […] having to move. I get

that, but at the same time, you know for us, for example, if we wanted

to buy we’d be paying four times what we pay at the moment in a mortgage

[…] It doesn’t really make financial sense to go and do that […] You’d

have to live somewhere. So I choose to live in a nice area where my

children are [at school].

They also did not want the burden of a large mortgage:

[…] I have no desire to put myself in a

position where I have a $2 million mortgage and have to work for the

rest of my short life to pay for it […]

Although probably only a small proportion

of people choose to rent long-term, this option may be gaining ground.

Young, well-paid professionals in particular see the flexibility of

private renting as attractive.

Location also seems to be a critical

factor. Most of the choosers rented in desirable inner suburbs of Sydney

and Melbourne, which would otherwise be inaccessible. An estimated one-in-eight private renters are “rentvestors” who rent where they want to live and buy elsewhere to get a foothold in the housing market.

*All names used are pseudonyms.

Authors: Alan Morris, Research Professor, University of Technology Sydney; Hal Pawson, Associate Director – City Futures – Urban Policy and Strategy, City Futures Research Centre, Housing Policy and Practice, UNSW; Kath Hulse, Research Professor, Centre for Urban Transitions, Swinburne University of Technology

We discuss the latest political scene, against the economic backcloth and the spreading virus. Yet the latest poles still give the incumbents plenty of hope. And what of Barnaby?

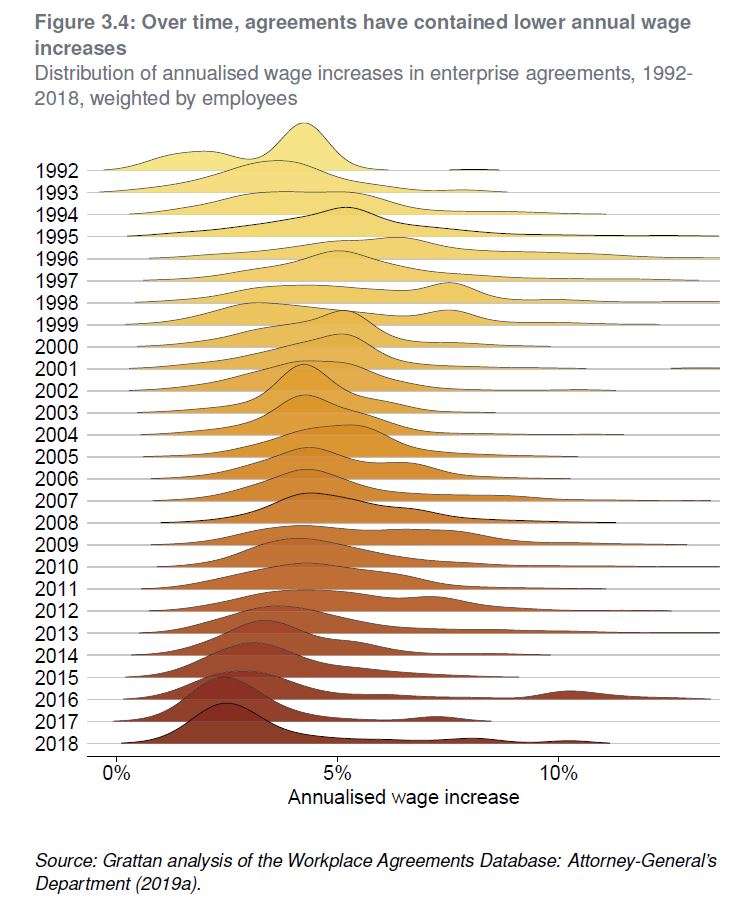

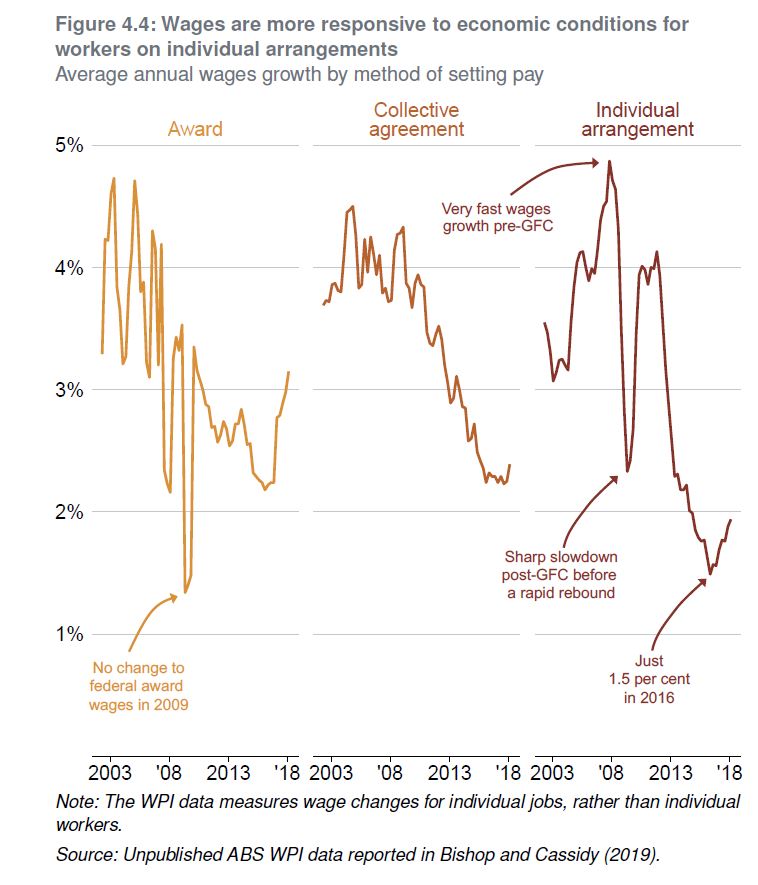

No free lunch: higher super means lower wages uses

administrative data on 80,000 federal workplace agreements made between

1991 and 2018 to show that about 80 per cent of the cost of increases

in super is passed to workers through lower wage rises within the life

of an enterprise agreement, typically 2-to-3 years. And the longer-term

impact is likely to be even higher.

‘This trade-off between more

superannuation in retirement but lower living standards while working

isn’t worth it for most Australians,’ says the lead author, Grattan’s

Household Finances Program Director, Brendan Coates.

‘This new empirical analysis reinforces

that the planned increase in compulsory super, from 9.5 per cent now to

12 per cent July 2025, should be abandoned. Most Australians are already

saving enough for their retirement.’

The paper directly measures the

super-wages trade-off for nearly a third of Australian workers – those

on federal enterprise agreements. But it shows that other workers are

also likely to bear the cost of higher compulsory super in the form of

lower wages growth.

Despite the claims of some in the

superannuation industry, it is unlikely that future super increases will

be different from past increases.

It’s true that wages growth has slowed in

recent years, but nominal wages are still growing by more than 2 per

cent a year, so employers have plenty of scope to slow the pace of wages

growth if compulsory super contributions are increased.

And none of the plausible explanations for

lower wages growth – whether slower growth in productivity,

technological change, globalisation, an under-performing economy, or

weaker bargaining power among workers – helps explain why employers

would foot any more of the bill for higher compulsory super this time

around.

If employers aren’t willing to offer large

pay rises today, it’s hard to imagine why they would pay for higher

super. In fact, if workers’ bargaining power has fallen, employers are

even less likely to pay for higher compulsory super than in the past.

Grattan’s 2018 report, Money in retirement: more than enough, found that the conventional wisdom that Australians don’t save enough for retirement is wrong.

Now this working paper finds that the conventional wisdom that higher super means lower wages is right.

‘Together, these findings demand a rethink of Australia’s retirement incomes system,’ Mr Coates says.

Nucleus Wealth’s Head of Investment Damien Klassen, Chief Strategist David Llewellyn Smith and Tim Fuller, discuss “Will Coronavirus create a Market Hangover?”

Topics include the pandemic spreading as the Chinese new year fast approaches, if the data can be trusted, Australian and macro implications if Chinese growth slows, how similar this is to the Chinese SARS outbreak in 2003, and as always we wrap up with our investment outlook

The information on this podcast contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.

Damien Klassen and Tim Fuller are an authorised representative of Nucleus Wealth Management. Nucleus Wealth is a business name of Nucleus Wealth Management Pty Ltd (ABN 54 614 386 266 ) and is a Corporate Authorised Representative of Nucleus Advice Pty Ltd – AFSL 515796.

Quirks in the superannuation system in Australia means that some who save more will get less. This highlights again the limitations of the current arrangements.