Economist John Adams and analyst Martin North discuss the state of WA with State MP Charles Smith MLC

He was elected at the 2017 Western Australian election to represent the East Metropolitan Region in the Western Australian Legislative Council from 22 May 2017 for the Pauline Hanson’s One Nation party. He was elected for four years, with Legislative Council terms beginning on 22 May 2017. In June 2019, Smith resigned from One Nation to sit as an independent.

We discuss the underlying issues facing the state, after our recent post on Mandurah, and underlying causes of the social issues apparent in many suburbs.

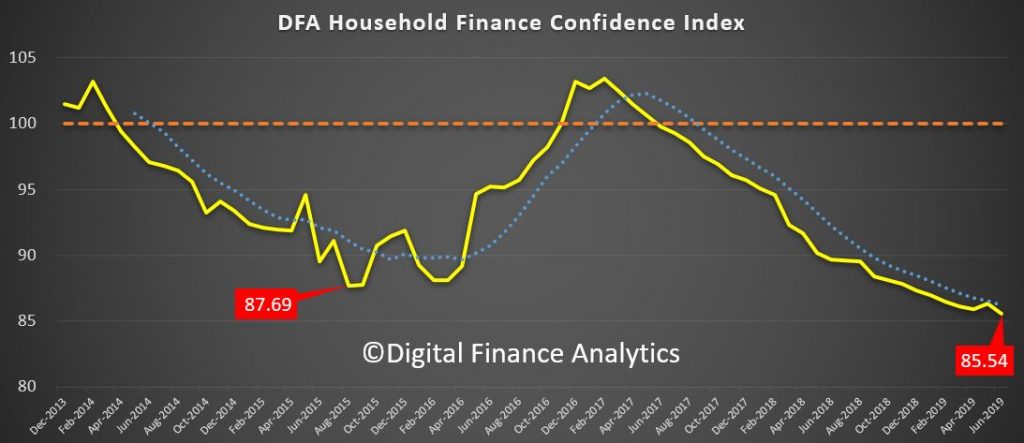

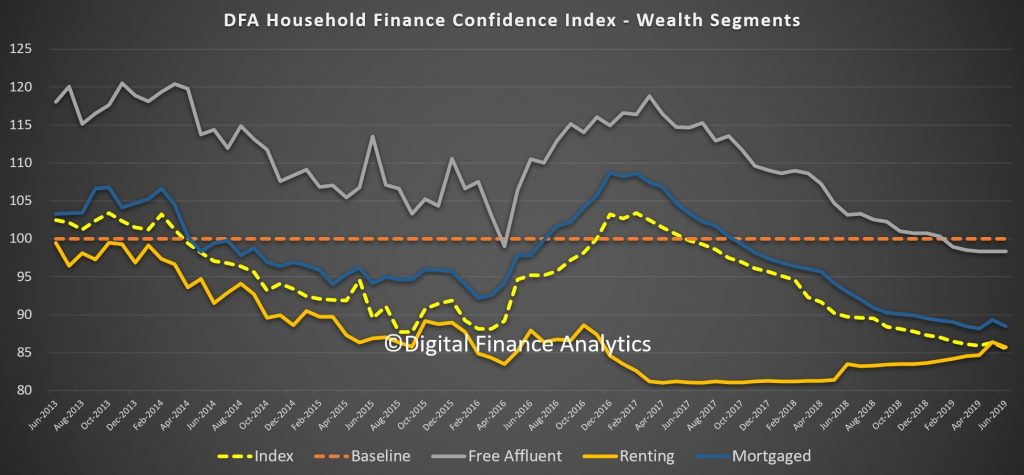

After the slight twitch of positive sentiment following the election in May, the DFA Household Finance Confidence Index fell again, to a new low of 85.54.

Whilst the RBA rate cut may offer some borrowers the prospect of improved cash flow (when the changes propagate through to the regular repayment), just as many households bemoan the continued cuts in savings rates. So, net, net there is no improvement in financial outcomes, and in fact more are concerned that lower RBA rates signals more trouble ahead.

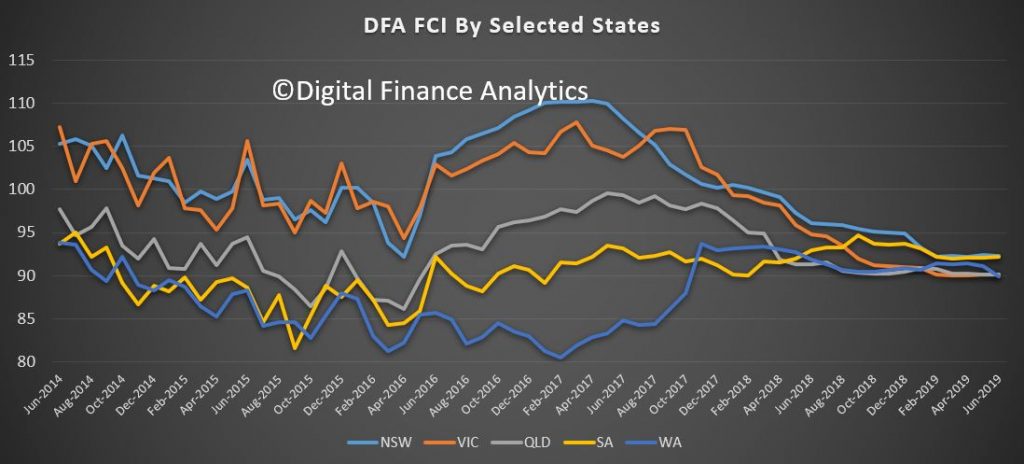

Across the states, WA showed a significant slide in confidence thanks in part to rising mortgage default and delinquencies, and very high underemployment. Most other states are bunched together, whereas a year or two back, VIC and NSW were streets ahead.

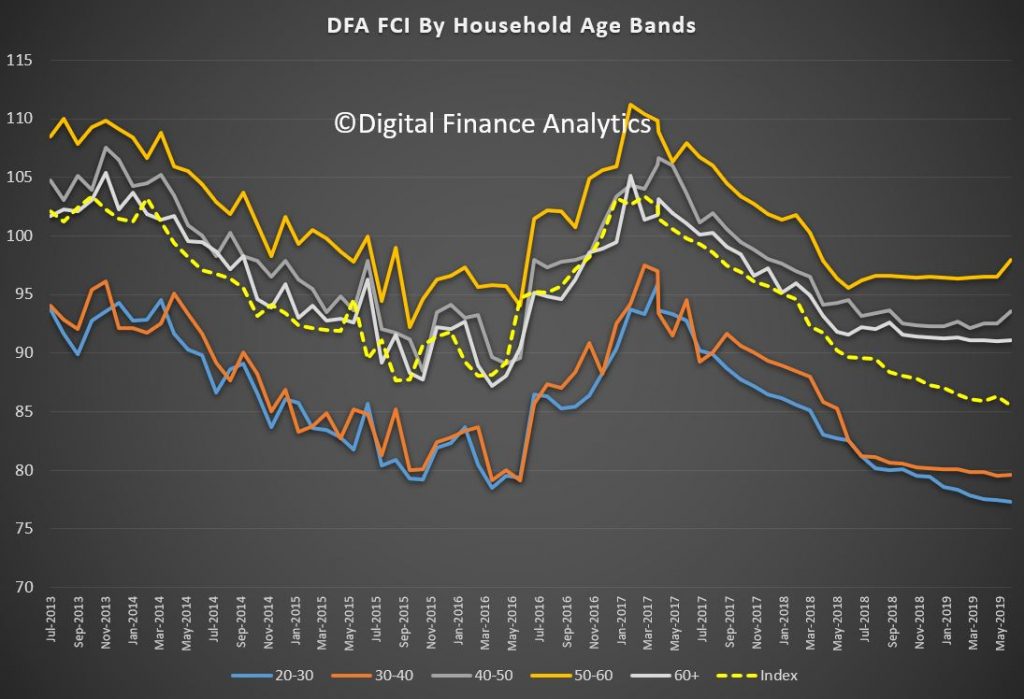

By age, younger households with mortgage debt registered a small improvement, while older households with savings went the other way on lower bank term deposit rates. Many of these will simply hunker down, and spend less, and will not largely benefit from the upcoming tax cuts. Older households resist the temptation to move to higher risk alternative savings vehicles, they too just spend less.

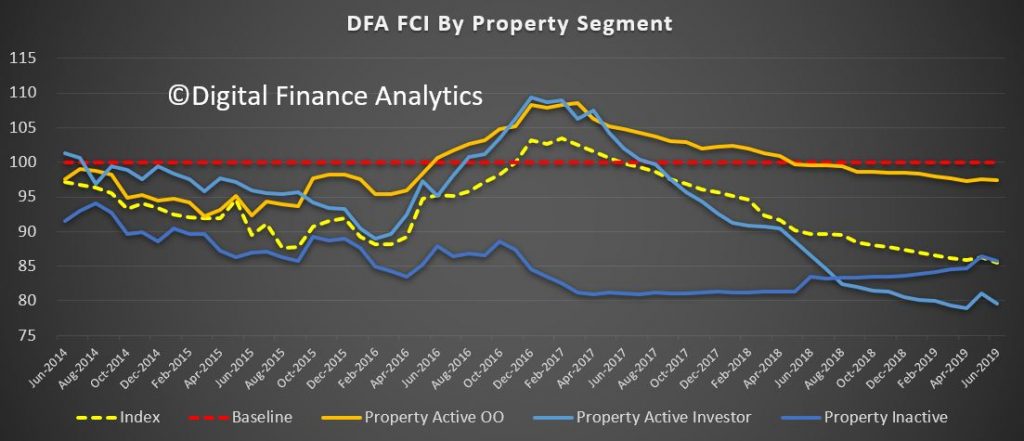

The property segmentation reveals that property inactive and investor households both reported lower levels of confidence, while owner occupied home owners were slightly more positive on the rate cuts news.

All three of our wealth segments remain below neutral on the index, indicating a significant deterioration over the past couple of years. Even those with property and no mortgage remain below the neutral 100 setting.

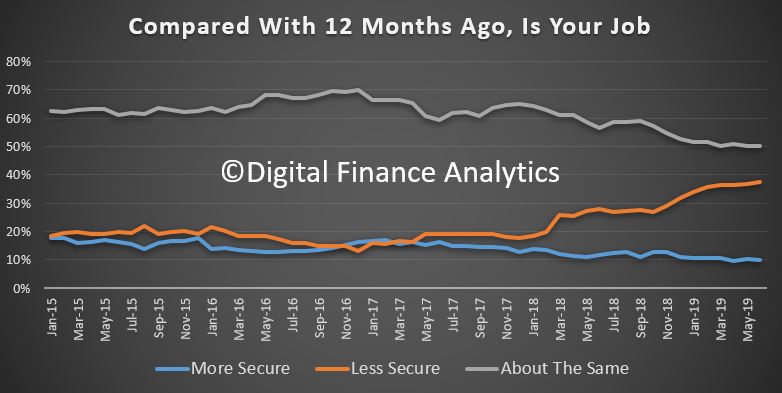

Within the moving parts of the index, job insecurity increased, with 37.4% reported as less secure than a year back, up 0.64% on the previous month. Around half of households saw no change, though underemployment continues to push higher.

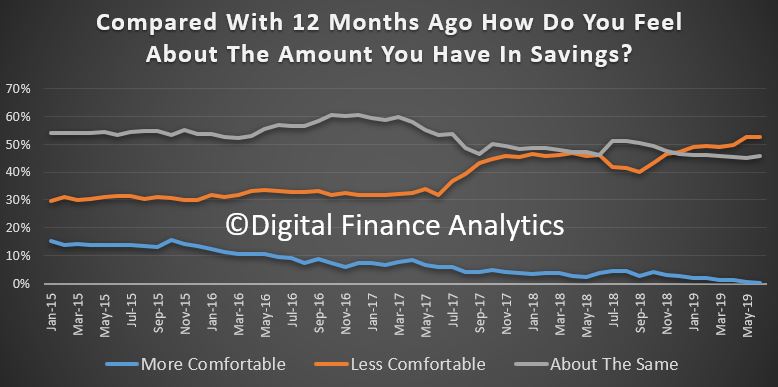

Savings continue to take a battering with more households dipping into them to secure their budgets, and lower returns on bank deposits – especially term deposits. On the other hand, share portfolio holders are fairing a little better – though with higher risks of course. Over 52% are less comfortable than a year ago.

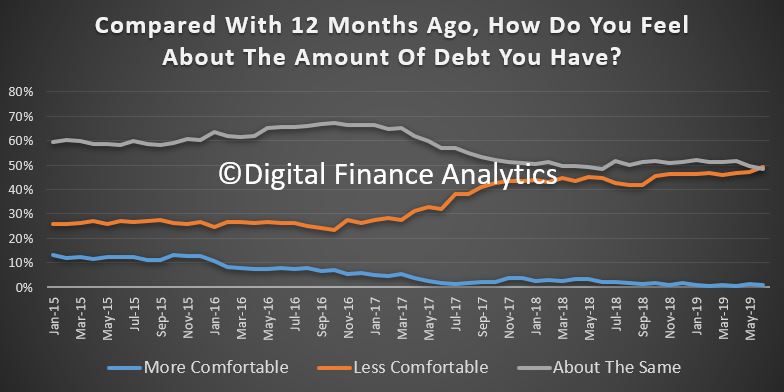

In terms of the debt burden nearly half are less comfortable, despite the rate cuts, while 48% are about the same as a year ago – down 1.46% on last month.

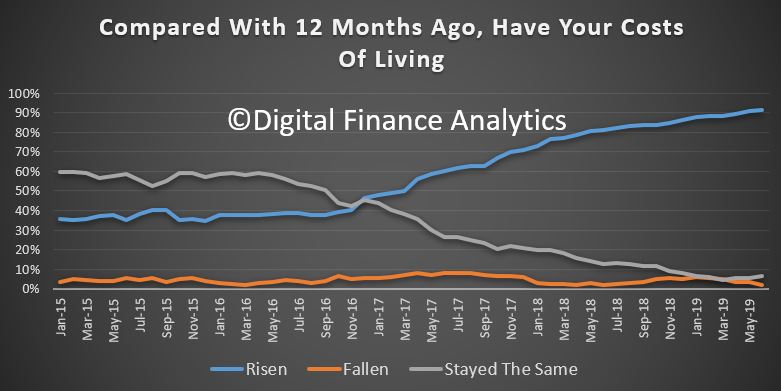

In terms of costs of living, the pain continues, with 91% saying their costs, in real terms are higher than a year ago. Only 1.33% said their costs of living had fallen. Households specifically mentioned higher council rates, fuel costs, electricity, school fees and child care costs.

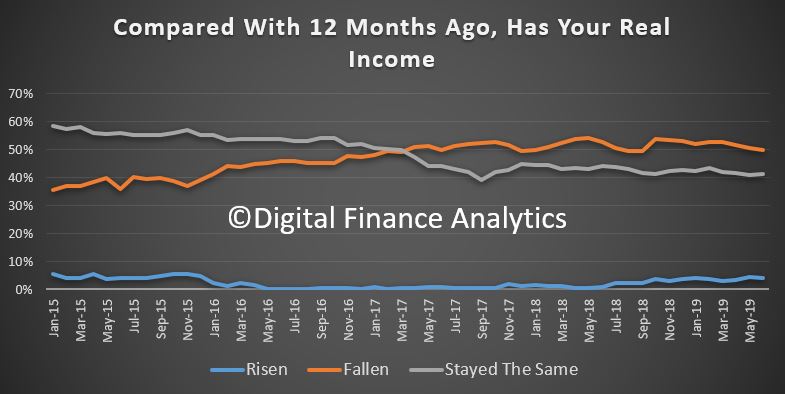

Income remains under pressure, with 4% saying their incomes had increased in real terms in the past year, compared with 50% saying their real incomes had fallen. 41% said their incomes were about the same.

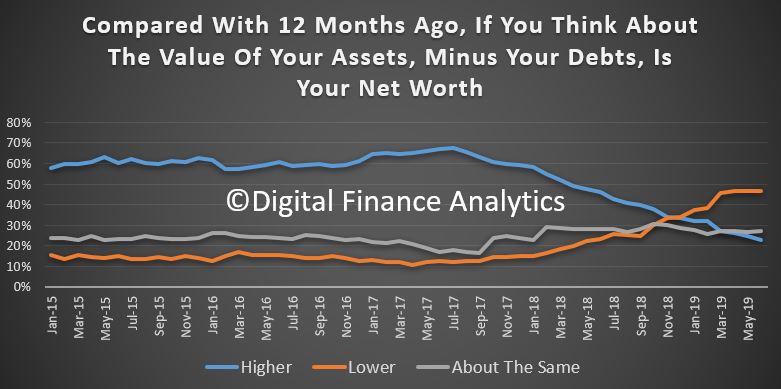

And overall net worth (assets less loans) rose for 23% of households – thanks to higher share prices mainly, while 47% reported a fall in net worth – thanks to property price falls, and reduced savings. 27% reported no change. As yet any recovery in home prices has not fed through into more positive results.

So, more evidence of the pressure on households, and so far the measures taken by the RBA and the Government have had no net positive impact on household confidence. As noted above, even those with property and no mortgage remain below the neutral 100 setting.

As a reminder this data comes from our rolling 52,000 household surveys, with 1,000 new added each week. This is data up to Monday 8th July.

ASIC has released a consultation paper (CP 316) on the first proposed use of its new product intervention power. On this inaugural occasion, ASIC is looking to address significant consumer detriment in the short term credit industry.

Under their recommended Option 1: ASIC would use their product intervention power to:(a)make an industry-wide product intervention order by legislative instrument under s1023D(3) of the Corporations Act to prohibit credit providers and their associates from providing short term credit and collateral services except in accordance with a condition which limits the total fees that can be charged; and(b)if a new model, which seeks to circumvent the industry-wide product intervention order, evolves in response to the prohibition, amend the existing order or introduce a new order to address that model. 71

In ASIC’s view, Option 1 is preferable because:(a) the product intervention order will prevent the use of the short term lending model which is causing significant consumer detriment; (b) it will prevent other credit and collateral services providers from adopting this model; (c) it promotes protection for consumers who require small amount credit contracts but who are provided with short term credit (and services agreements) in reliance on the short term credit exemption; and (d) it is a more comprehensive and timely response than the other options.

The product intervention power allows ASIC to intervene where

financial and credit products have resulted in or are likely to result

in, significant consumer detriment. The new product intervention power

is an important addition to ASIC’s regulatory toolkit. It reinforces

ASIC’s ability to directly confront, and respond to, harms in the

financial sector.

ASIC considers that significant consumer detriment may arise in

relation to a particular model designed to provide short term credit at

high cost to vulnerable consumers. These consumers include those on low

incomes or in financial difficulty.

In its first proposed deployment of this power, ASIC is targeting a

model involving a short term credit provider and its associate who

charge fees under separate contracts. When combined, these fees can add

up to around 990% of the loan amount.

While ASIC is presently aware of two firms currently using this model

– Cigno Pty Ltd and Gold-Silver Standard Finance Pty Ltd – the proposed

product intervention order would apply to any firm using this type of

business model.

Announcing the consultation ASIC Commissioner Sean Hughes said,

‘Sadly we have already seen too many examples of significant harm

affecting particularly vulnerable members of our community through the

use of this short term lending model. Consumers and their

representatives have brought many instances of the impacts of this type

of lending model to us. Given we only recently received this additional

power, then it is both timely and vital that we consult on our use of

this tool to protect consumers from significant harms which arise from

this type of product.’

‘Before we exercise our powers, we must consult with affected and

interested parties. This is an opportunity for us to receive comments

and further information, including details of any other firms providing

similar products, before we make a decision’.

ASIC seeks the public’s input on the proposed intervention order by 30 July 2019. Submissions should be sent to: product.regulation@asic.gov.au.

ASIC anticipates making a decision on whether to make a product

intervention order in relation to short term credit during the course of

August 2019.

All intervention orders subsequently made must be published on ASIC’s

website, and a public notice issued in relation to the intervention.

On 4 April 2019 ASIC published a media release welcoming the approval

of new laws to protect financial service consumers (refer: 19-079MR).

ASIC also published a media release on 26 June 2019 confirming that

it initiated consultation on the administration of its new product

intervention power (refer: 19-157MR).

ASIC was unsuccessful in civil proceedings

in the Federal Court in 2014 involving an earlier use of this short

term lending model by two entities Teleloans Pty Ltd and Finance &

Loans Direct Pty Ltd (refer: 15-165MR).

Research from credit information website, CreditSmart.org.au, has

revealed that one year on from the adoption of Comprehensive Credit Reporting

(CCR), most Australian consumers are still unaware of the changes that are

impacting their credit health, and may not know how it can impact their future

credit applications.

The research found that in the last 12 months, only one in

four consumers checked their credit report. More worryingly, consumers who are

struggling with their credit health said they were just as likely to seek

advice from credit repair or debt management services as they would from their

lender or free financial counsellor.

“Consumers are still largely unaware of credit reporting,

what information is contained in their credit report, and what that means about

their borrowing behaviour and overall credit health,” said Mike Laing, CEO of

the Australian Retail Credit Association (ARCA), which founded CreditSmart.

“Our research has found that while awareness has actually

increased 11% from last year, less than 1 in 3 consumers are aware that credit

reporting has changed. Importantly however, awareness is higher among those

with a real need to know – with one in two consumers who are planning to make a

significant purchase in the next 12 months being aware of the changes,” added

Mr Laing.

The rollout of comprehensive credit reporting has

accelerated rapidly in Australia since last year, with more data shared than

ever before. By September this year, comprehensive credit information for 80%

of consumer loan accounts will be available.

“CCR allows lenders to share and view more detailed credit

information about consumers to provide a clearer view of a consumers’ credit

history. This is a positive move for consumers who have a strong history of

making payments on time.” added Mr Laing.

Consumer awareness highest for users of riskier

credit products

According to CreditSmart, credit cards make up the majority of

accounts currently in the CCR system at around 87%, followed by mortgages at

9%.

Yet, people who hold these mainstream types of accounts are

the least aware of the changes to credit reporting and may not be aware of the

value it adds to their credit history, if they have a strong record of making

payments on time.

It was also found that those consumers with products that

are sometimes seen as riskier, such as leases for household goods (61%), cash

loans (54%) and payday loans (79%), plus personal loans (55%), are all far more

aware of the changes to credit reporting[1] This could indicate the users of

those products have been given more information about the changes, or that they

have taken more time to understand the changes.

Consumers using these riskier products also rated their

credit health as significantly worse than users of home loans and credit cards.

Interestingly, Buy Now Pay Later (BNPL) users have

relatively low awareness of credit reporting changes despite significant

numbers rating their credit health as poor.[2]

Consumer awareness a work in progress

Awareness of credit reporting changes is not the same as

understanding the detail behind their credit report, according to Mr Laing.

“It is easy to understand how consumers may become confused

about what’s important when it comes to credit reporting and their credit

health. There’s a lot of information out there and it’s important to bring it

back to a simple, straightforward message.

“We want consumers to be aware of the importance of their

credit history to their credit health – and how that history may impact their

financial future. The steps are to understand how the credit reporting system

has changed, to get your credit report to see your credit history and to manage

the credit that you have responsibly” added Mr Laing.

For more information on the changes to credit

reporting and where to get your free credit reports you should go to www.creditsmart.org.au, which provides clear information on the credit

reporting system to assist consumers to optimise their credit health.

The ABA made a big splash when relaunching the revised Banking Code of Conduct which starts today, and yes it is a small win for consumers and SME’s. However, we must ask this: since when are such financial service basic hygiene issues as not charging for no service, advising before charging, considering credit card repayment capacity, speaking in plain English and offering suitable low-fee products, seen as so revolutionary?

Frankly put, these are issues which an industry which truly focused on the well-being of its customers would have long ago addressed. They did not, and were dragged towards better outcomes by the Royal Commission and public pressure.

So, yes, important baby steps, but still a massive leap is required to the desired level of customer-centricity. There is nothing bold or innovative here.

Australia’s banks will comply with a strong new code of practice that significantly increases and enshrines customer protections and introduces tough new penalties for breaches from tomorrow.

The ASIC-approved Banking Code of Practice represents the most significant increase to customer protections under a code in the industry’s history.

From 1 July, under the new Banking Code of Practice, banks will no longer:

– Offer unsolicited credit card limit increases – Charge commissions on Lenders Mortgage Insurance – Sell insurance with credit cards and personal loans at the point of sale.

Under the code banks must:

– Offer low-fee or no-fee accounts to low income customers – Have a 3 day grace period on all guarantees to give guarantors enough time to make sure it’s the right option for them – Actively promote low-fee or no-fee accounts to low income customers – Provide reminders when introductory offers on credit cards end – Simpler and fairer loan contracts for small business using plain English that avoids legal jargon – Provide customers a list of direct debits and recurring payments to make it easier to switch banks.

Australian Banking Association Chief Executive Officer Anna Bligh said customers can expect to see a change to banking products and services immediately.

“We’ve completely rewritten the rule book for Australia’s banks. The Banking Code of Practice has strong protections for customers, serious consequences for breaches and strong independent enforcement,” Ms Bligh said.

“Banks understand they need to change their behaviour and this new rule book represents an important step in earning back the trust of the Australian public.

“The new Code will form part of every customer’s relationship with their bank and will be strongly enforced both by an independent body, the Banking Code Compliance Committee, and the Australian Financial Complaints Authority.

“Whether it’s through your credit card, home loan, small business loan or just day to day banking, Australian customers will see tangible benefits from this new Code,” she said

Financial Counselling Australia Chief Executive Officer Fiona Guthrie said the new Code was a major step up in the protections for customers, particularly the most vulnerable, and was an important milestone in restoring community trust in Australia’s banks.

“Codes like this really can make a difference because they go beyond black letter law and instead reflect the standards that an industry voluntarily commits to,” Ms Guthrie said.

“The banking industry released its first version of the banking code over 25 years ago and it is really pleasing to see that each version – and this is the fourth major revision – contains advances in consumer protection.

“Financial counsellors in particular welcome provisions around family violence, stronger protections for guarantors, better promotion of free or low fee accounts and more proactive approaches to people experiencing financial hardship,” she said.

Banks have trained more than 130,000 staff on the new requirements in the code so it can begin operating from tomorrow (1st July 2019). Information about the Code has been translated into Mandarin (simplified Chinese), Arabic, Vietnamese, Tagalog/Filipino, Hindi, Spanish and Punjabi.

The Financial Services Royal Commission asked for further changes to the Code which will be implemented by March 2020.

Amid the ongoing discussion around who should bear the responsibility for assisting vulnerable customers, recent data has revealed further need for targeted care and education, as Australians are falling prey to bank fraud and other financial scams at an alarming rate, via Australian Broker.

According to the KPMG Global Banking Fraud Survey, 61% of banks

worldwide have reported an increase in fraud – both in value and volume –

over the past three years, with Australia being among the countries hit

the hardest.

“We are seeing a disproportionately high volume of scam attempts on

Australians – there were 177,000 scam reports here last year, costing

almost half a billion dollars. This compared to around 85,000 scam

reports in the US and UK, with far bigger populations,” said Natalie

Faulkner, KPMG global fraud lead.

KPMG’s survey found customer awareness is key for detecting fraud and

reducing losses, and the firm called for more to be done to

educate consumers. While branch staff in banks are a major point of

contact, brokers – who now help six in 10 home owners to secure a mortgage – are naturally on the front line of this work.

“Education should be multifaceted to reach different audiences. For

example, many scam victims tend to be the elderly or socially isolated,

so education should not just be through digital channels but also

through television, traditional media and even face-to-face sessions

with vulnerable customer groups,” said Faulkner.

The data also revealed that cyber-related fraud is the most

significant challenge faced worldwide, a reflection of the growth in

digital banking.

“This is set in the context of a changing global banking landscape,

where branch networks are shrinking, volumes of digital payments are

increasing and there is less customer face time,” explained Faulkner.

Open banking –

which will be implemented next week – was mentioned as an emerging

challenge in fraud risk, as it will see banks allowing third parties to

access their customer data.

However, Faulkner noted, “On a positive note, having more

transparency across accounts will enable the banks to know their

customer more holistically and trace funds in fraud detection.”

Mortgage Broker and Financial Planner Chris Bates and I discuss current property market trends, consider the fate of the high-rise sector and answer a viewers question relating to mortgage offset accounts.

Chris can be found at www.wealthful.com.au & www.theelephantintheroom.com.au plus via LinkedIn: https://www.linkedin.com/in/christopherbates

Australians are losing more money to NBN scams, with reported losses in 2019 already higher than the total of last year’s losses, according to the ACCC.

Consumers lost an average of more than $110,000 each month between

January and May this year, compared with around $38,500 in monthly

average losses throughout 2018 – an increase of nearly 300 per cent.

“People aged over 65 are particularly vulnerable, making the most

reports and losing more than $330,000 this year. That’s more than 60 per

cent of the current losses,” ACCC Acting Chair Delia Rickard said.

“Scammers are increasingly using trusted brands like ‘NBN’ to trick

unsuspecting consumers into parting with their money or personal

information.”

Common types of NBN scams include:

Someone pretending to be from NBN Co or an internet provider calls a

victim and claims there is a problem with their phone or internet

connection, which requires remote access to fix. The scammer can then

install malware or steal valuable personal information, including

banking details.

Scammers pretending to be the NBN attempting to sell NBN services, often at a discount, or equipment to you over the phone.

Scammers may also call or visit people at their homes to sign them

up to the NBN, get them a better deal or test the speed of their

connection. They may ask people to provide personal details such as

their name, address, date of birth, and Medicare number or ask for

payment through gift cards.

Scammers calling you during a blackout offering you the ability to stay connected during a blackout for an extra fee.

It is important to remember NBN Co is a wholesale-only company and does not sell services directly to consumers.

“We will never make unsolicited calls or door knock to sell broadband

services to the public. People need to contact their preferred phone

and internet service provider to make the switch,” NBN Co Chief Security

Officer Darren Kane said.

“We will never request remote access to a resident’s computer and we

will never make unsolicited requests for payment or financial

information.”

“If someone claiming to work ‘for the NBN’ tries to sell you an

internet or phone service and you are unsure, ask for their details,

hang up, and call your service provider to check if they’re legitimate.

Do a Google search or check the phone book to get your service

provider’s number, don’t use contact details provided by the sales

person,” Ms Rickard said.

“Never give an unsolicited caller remote access to your computer, and

never give out your personal, credit card or online account details to

anyone you don’t know – in person or over the phone – unless you made

the contact.”

“It’s also important to know that NBN does not make automated calls

to tell you that you will be disconnected. If you get a call like this

just hang up.”

“If you think a scammer has gained access to your personal

information, such as bank account details, contact your financial

institution immediately.”

Do you think you are paying more than you should for energy, banking, insurance, internet and phone services? You are not alone, and you are probably right. From The Conversation.

Companies offer a growing number of deals that supposedly enable you

to choose what is best for you. Every basic economics textbook tells us

greater choice should deliver cheaper prices. But in reality this isn’t

necessarily the case.

So what’s going on?

A big part of the answer is that businesses are taking advantage of

the behavioural phenomenon of “consumer paralysis” to maximise profits.

They provide us with many plans and deals to make us feel like we are

in control, but too many choices actually leads most of us to make a

bad (or no) choice.

Energy pricing

Let’s consider how this works in the context of Australia’s electricity market.

In most areas of the country, residential customers have at least half a dozen retailers to choose from.

Nonetheless, according to the Australian Consumer and Competition Commission, electricity prices and profit margins are among the highest in the world,

and rising. The consumer watchdog calculates that in the decade to 2018

the average residential electricity bill increased by 55% (or 35% in

real terms) – and only a very small part of that had to do with alleged

culprits such as renewable energy.

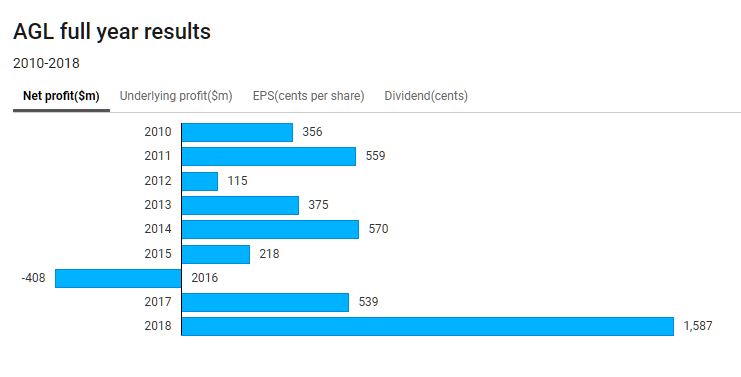

Australia’s biggest electricity company, AGL, made a net profit of A$1.6 billion in 2018 – 194% more than the year before.

Depending on where you live, AGL offers up to 11 energy plans to

residential customers. There’s the “Savers” plan, “Savers Online”,

“Everyday”, “Freedom”, “Standing Offer”, “Essentials”, “Essentials

Plus”, and so on.

Each plan, in turn, has four to eight tariff type options: “Flexible

Price”, “Time of Use Interval”, “5 Day Time of Use”, “Single Rate”, “Two

rate: single rate with controlled load”, “Single Rate Demand Opt-in”,

and so on.

That adds up to literally dozens of price plans from just one

retailer. Other companies are hardly better. For a customer in inner

Sydney, there are more than 350 retail plans to choose from.

All this “choice” gives the appearance of a competitive market, but

its effect is the opposite. It give retailers wriggle room to charge

more, not less.

Experiments in choice behaviour

Many experiments over the past three decades have demonstrated the ubiquity of too much choice leading to consumer paralysis.

One classic experiment was run by psychologists Sheena Iyengar and Mark Lepper

in a San Francisco supermarket in 1999. Customers visiting the store

were given a chance to sample jams. Half the time they were allowed to

taste up to six jams; the other half they could taste up to 24 jams.

Traditional economics says a consumer is much more likely to find a

jam they really like with a sample of 24 rather than six. So offering 24

jams should lead to more jam purchases.

Yet exactly the opposite was found. Of the consumers who chose to

taste jams, only 3% of those who could sample 24 jams ended up buying

jam, whereas 30% (or 10 times more) of those who could sample just six

jams ended up buying.

More choices provided, more paralysis.

More recently, in 2012, Iyengar’s Columbia University colleague Eric Johnson and others reported on an experiment with much greater consequences.

They asked people to choose health insurance coverage from a set of

four or eight options. The options varied on monthly premiums and

deductibles. When given four options, 42% of subjects chose the best

value option. On average their choices cost about $200 more than the

best option on offer.

When given eight options, only 21% chose the best option – no better than simply making a random choice.

Reinforcing psychological biases

Given the massive number of products and plans available in the

energy, banking, insurance, internet and mobile phone sectors, the time

and effort needed to choose the best deal leaves us feeling overwhelmed

and overloaded. In response, we rely on shortcuts (rules of thumb) to

save both time (and our sanity).

But these shortcuts can also cause biases that result in further paralysis, including:

Present bias

– we put much greater weight on the present than the future. Since the

cost of making decisions happens in the present (like the time and

effort to compare options and switch services) while the benefits happen

later (like saving money), we minimise the time we spend making

decisions

Status quo bias – we tend to stick with a chosen option or default, even when a much better option may be available

Loss aversion – we place much greater weight on losses and often overestimate the chance of a bad outcome.

There is considerable evidence pointing to how these biases lead to

consumer paralysis in the retail banking and energy sectors.

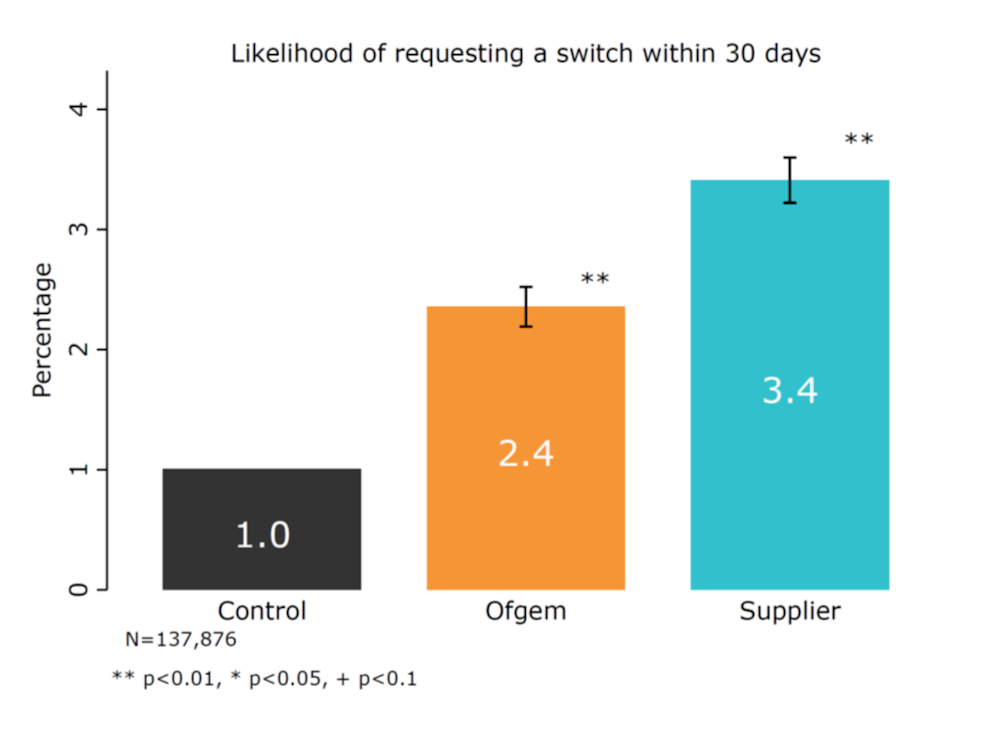

In 2017, Britain’s energy regulator, Ofgem, ran a randomised control trial

involving more than 130,000 electricity customers. Participants

received personalised letters either from Ofgem or their current

provider offering substantially better electricity deals.

The result: compared with the control group in which only 1% switched

tariffs within the next month, 3.4% of those who received an offer from

their electricity provider switched to a better deal. Even when

presented with notable savings, more than 96% stuck with the status quo.

Results of Ofgem’s Cheaper Market Offers Letter (CMOL) trial.

Ofgem

Other Ofgem research

shows that among those who have not switched energy plans, 51% consider

it a hassle they don’t have time for, and 48% worry that things would

go wrong.

Yvette Hartfree and her colleagues at the University of Bristol’s

Personal Finance Research Centre have noted similar fears among bank customers:

“The biggest concern for those considering switching is that something

will go wrong at some point in the process of switching.”

Taking action

We should not be surprised that energy companies and others use an

avalanche of choice to confuse us. It is a brilliant business strategy:

it seems more competitive from a traditional assessment, yet actually

reduces competition.

So what can you do?

On your own, you will need to make a conscious effort to overcome

paralysis. You need to devote the time to carefully compare offers.

Fortunately, you can find tools that can help, such as the Australian government’s energy comparison website.

However, be wary of commercial “switching services” and websites that

provide comparisons. These operations are often being paid by retailers.

Their motives are not necessarily to direct you to the best deal.

What can we do collectively?

One option is government action to ensure switching services are

trustworthy. At a minimum, there should be guidelines that switching

services not take payments from retailers, and only charge you when you

actually save money.

Another option is to form “consumer unions”, which can bargain

collectively to get members better deals. The potential of community

groups to leverage bulk-buying arrangements has been demonstrated in

other contexts. In Victoria’s Gippsland region, for example, local

organisations have banded together to offer discounts on renewable energy technology.

There’s no reason something similar could not be done to overcome the choice problems induced by big energy retailers and the like.

Author: Robert Slonim, Professor of Economics, University of Sydney

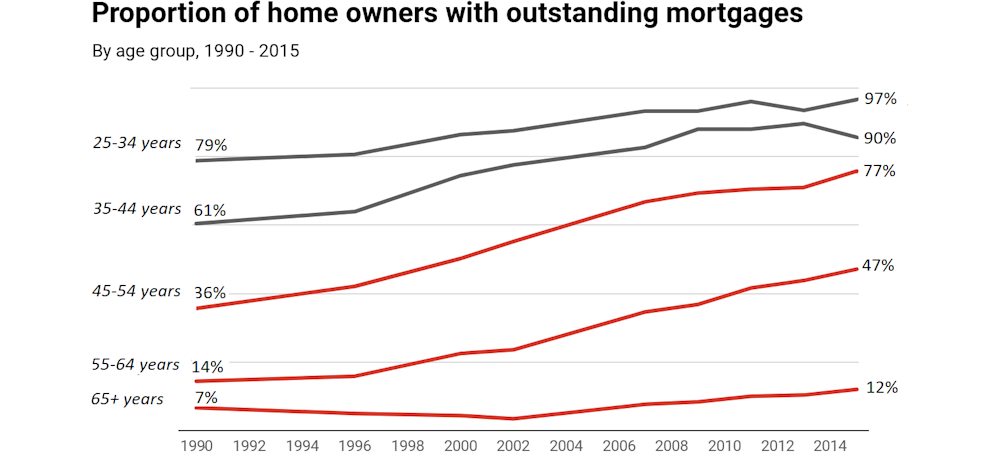

The number of mature age Australians carrying mortgage debt into retirement is soaring.

And on average each mature age Australian with a mortgage debt owes much more relative to their income than 25 years ago.

Microdata from the Bureau of Statistics survey of income and housing

shows an increase in the proportion of homeowners owing money on

mortgages across every home-owning age group between 1990 and 2015. The

sharpest increase is among homeowners approaching retirement.

More mortgaged for longer

For home owners aged 55 to 64 years, the proportion owing money on mortgages has tripled from 14% to 47%.

Among home owners aged 45 to 54 years, it has doubled.

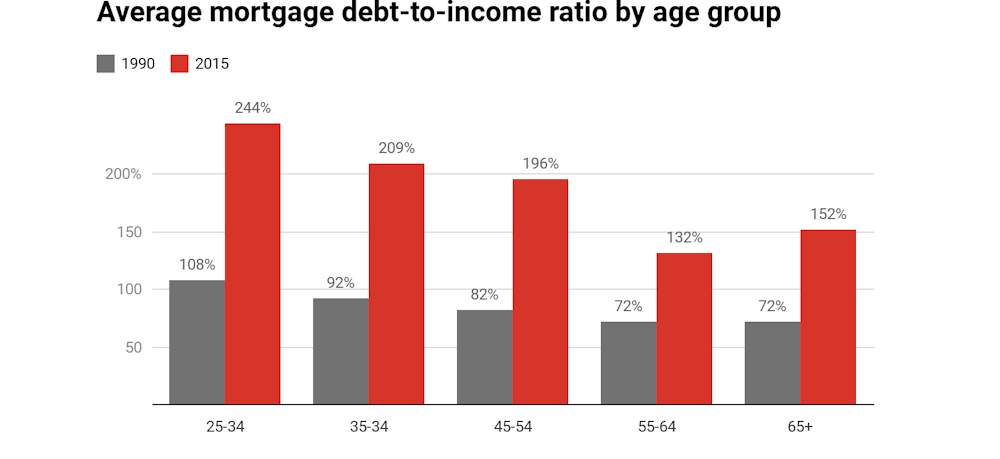

Despite weaker property prices, the ratio remains historically high.

This means households have to borrow more to buy a home. It also delays

the transition into home ownership, potentially shortening the the remaining working life available to repay the loan.

Second, today’s home owners frequently use flexible mortgage products

to draw down on their housing equity as needed for other purposes.

During the first decade of this century, one in five home owners aged

45-64 years increased their mortgage debt even though they did not move house.

Third, older home owners appear to be taking on bigger mortgages or

delaying paying them off in the knowledge that they can work longer than

their parents did, or draw down their superannuation account balances.

Super could be changing our behaviour

For mortgage holders aged 55-64 years, there is evidence to suggest that larger debts prolong working lives.

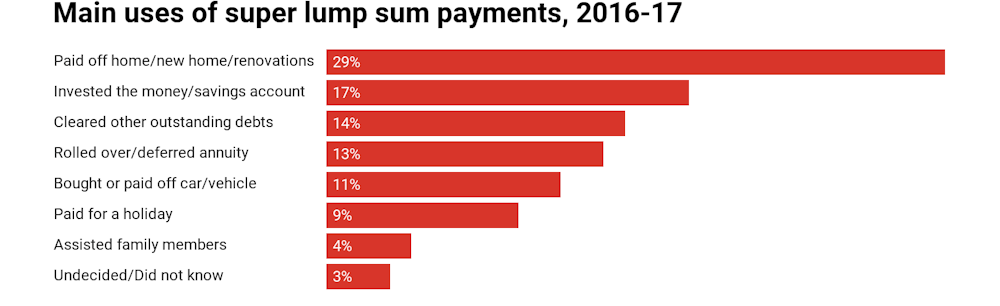

In 2017 around 29%

of lump sum superannuation withdrawals were used to pay down mortgages

or purchase new homes or pay for home improvements, up from 25% four years earlier.

In the Netherlands, where a mandatory occupational pension scheme

along the lines of Australia’s super scheme has been in place for much

longer, over one-half of home owners aged 65 and over are still paying off mortgages.

Internationally, studies have found that indebtedness adds to psychological distress. The impacts on wellbeing are more profound for older debtors, without the ability to recover from financial shocks.

Growing indebtedness will increase after-housing-cost poverty among older Australians and create pressure to boost the age pension.

Mortgage debt burdens late in working life will also expose home

owners to unwelcome risks, as health or employment shocks can ruin plans

to pay off their mortgages.

During the first decade of this century, around half a million Australians aged 50 years and over lost their homes.

Super and government housing assistance could become the safety nets that allow retirees to escape their mortgages.

It wasn’t the intended purpose of superannuation, and wasn’t the

intended purpose of housing assistance. It is a development that ought

to be front and centre of the inquiry into the retirement incomes system announced by Treasurer Josh Frydenberg.

It is a change we’ll have to come to grips with.

Authors: Rachel Ong ViforJ, Professor of Economics, School of Economics, Finance and Property, Curtin University; Gavin Wood, Emeritus Professor of Housing and Housing Studies, RMIT University