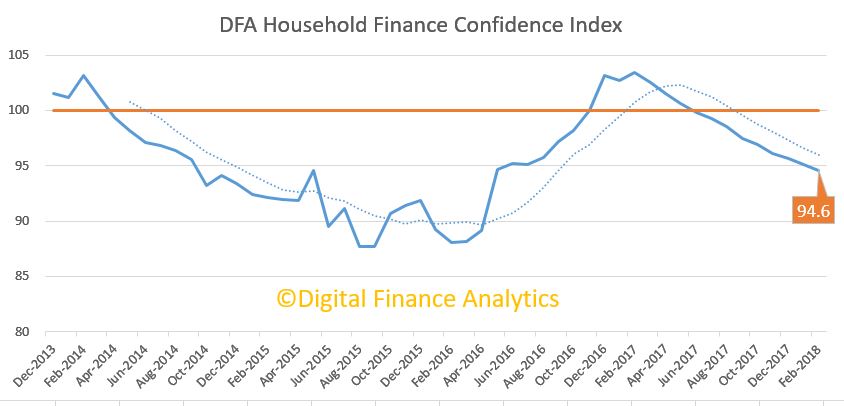

The latest edition of the Digital Finance Analytics Household Finance Confidence Index shows a further drift lower, remaining below the 100 neutral benchmark. It fell to 94.6 in February, down from 95.1 the previous month. This is in stark contrast to improved levels of business confidence as some have reported. Our latest video blog covered the results.

The slide was more significant among those households with investment properties, thanks to higher mortgage rates, concerns about interest only loan resets and lower home prices. In additional net rentals are lower. Owner occupied households also fell just a small amount, mainly because of rising living costs against flat incomes. Those renting, or otherwise excluded from property are the least confident. This continues the long term trend, indicating that property ownership still bolsters confidence to some extent.

The slide was pretty consistent across the states, other than a small lift in WA. Compared with a year ago, confidence levels in NSW and VIC are significantly lower.

We also see a similar story across all the age bands, suggesting the decline in confidence is similarly widely spread.

To understand the reasons for the falls we can look to the index scorecard. Overall, there was a rise of 1.2% in households feeling less secure about their jobs, compared with this time last year, and a small reduction in those feeling more secure.

Those with savings were less comfortable, thanks to continued falls in deposit rates, and recent discussions about deposit bail-in following passage of the recent APRA Act. More significantly, more are dipping into their savings, to maintain lifestyle, and so balances are reducing. Many realise this is not a sustainable position.

Just under half of households remain uncomfortable with the amount of debt they hold, around half saw no change over the past year. Concerns related to rising interest charges which are working through, and also ability to maintain mortgage repayments. Some households have resorted to obtain additional credit, either on a card, or separate loan, to maintain their finances. Again many realise this is not a sustainable position.

Costs of living concerns rose, with 76.7%, up 3.84% on last month, households saying that costs of electricity, fuel, rates, child care and school fees all impacting. Only 2.5% of households said their costs had fallen.

Finally, we saw a fall of 3.7% of households who said their net worth had improved, down to 54.6%, mainly explained by changes in the value of property on one hand, and of share prices on the other. 16% said their net worth had fallen. 28.9% said there had been no change.

Based on our research, we see little on the horizon to suggest that household financial confidence will improve. We expect wages growth to remain contained, and home prices to slide, while costs of living pressures continue to grow. There will also be more pressure on mortgage interest rates as funding costs rise, and lower rates on deposits as banks trim these rates to protect their net margins.

By way of background, these results are derived from our household surveys, averaged across Australia. We have 52,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health. To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

The Financial Services Royal Commission has exposed the pressure selling tactics used by the banks. They draw on simple psychological rules to target vulnerabilities among some of their most loyal customers.

One example is the high-pressure selling of add-on insurance for customers when they sign up to a credit card. The Commonwealth Bank of Australia (CBA) acknowledged that upwards of A$13 million of refunds are likely to be paid to consumers who had been pressured into buying these add-on products.

Another witness at the commission, Irene Savidis, relayed what happened when she tried to cancel this insurance:

they just kind of kept pushing it on me saying, you know, “It’s good for you, it will help you.” I just felt pressured or kind of like, you know, no matter what I said, it was the opposite. So I couldn’t – I felt like I couldn’t cancel it.

These techniques are well established in psychological research as ways to manipulate behaviour. In this single example, we can see how the representative of the CBA used trust, repetition (the more something is repeated, the more we are likely to believe that it is true), authority (the salesperson is perceived to be an expert), and scarcity (act now, or you will miss out). All of these factors are part of the marketers’ bag of tricks.

As much as trust can be useful under certain circumstances, at times it can be dangerous. When we are faced with choices or decisions where we don’t feel confident, we have a tendency to give over our decision making to somebody who we believe has those skills and authority and trust them to do the right thing by us.

How we make decisions under situations of stress

As we can see in the examples from the commission, many of these financial decisions are being made by consumers under already significant financial and psychological stress. We also know that under these conditions none of us make the best decisions.

In psychology, we know that people don’t always think through their decision making in a rational and linear way when placed under situations of stress. This becomes more pronounced when – counter intuitively – people are provided with lots of information related to a topic that they don’t have the ability to fully understand, either because it is complex and confusing, or even simply because it is in an area that they don’t have any experience in.

It’s in these situations that they rely on peripheral information to make their choices – things like colours, previous experience with similar situations, even the aesthetic layout of the information, or the way the person giving them the information is dressed.

When we feel we have less resources, we perform worse on tasks requiring high-level cognitive control, like important decision making. Logical reasoning, the kind that should occur when signing up to a loan, extending our credit, or committing to any major financial agreement, is relatively inefficient in these situations.

Responding to pressure selling techniques

So, how do we respond to the types of techniques that we have seen and any others that might be exposed by the commission over the next 12 months?

We need to accept that our decision making is flawed and not judge ourselves, or others, harshly, when they seem to make irrational decisions, or behave in a way that is counter-intuitive. We need to accept that people are complicated, and will make a decision that conforms to their emotional state of mind, at that point in time.

That said, there are some things people can do to avoid some of these manipulative tactics. One thing is to do your best to slow down when it comes to decision-making. If you do want to buy something, that’s fine, but do it outside the heat of the sales process.

Speak to someone you trust about your plans. Recognise that your emotional brain may already have convinced your rational brain that you are making a good decision, so you need to check in with someone who isn’t emotionally engaged in the decision.

And if the person offering something like add-on insurance creates a sense of scarcity, then identify the feeling, and assume you can walk away. A classic technique of traditional sales is to say something along the lines of, “I can only offer you this now”, but the best response is always to take your time. If they are offering you this today, they are more than likely to offer it to you tomorrow.

One thing that has emerged from the royal commission is the somewhat obvious fact that banks are businesses. Indeed, people should not be fooled into thinking that banks are anything other than profit-driven organisations. Banks know exactly what they are doing when it comes to the use of manipulative techniques to get customers to buy their products.

The hope is that this royal commission will be able uncover and act upon some of the practices verging on illegal, while highlighting some of the more unpleasant and unethical practices that have been occurring.

Author: Paul Harrison, Director, Centre for Employee and Consumer Wellbeing; Senior Lecturer, Deakin Business School, Deakin University; Chiara Piancatelli, PhD Candidate

The irresponsible (if not predatory) lending and the selling of “junk” financial products highlighted by the Financial Services Royal Commission should raise concerns for regulators, educators and parents interested in financial literacy.

Research shows a strong correlation between financial literacy and literacy and numeracy skills. Literacy and numeracy are critical for, among other things, making sense of product disclosure statements and understanding the impact of loan terms and interest rates on the total amount to be repaid.

But teaching financial literacy requires going beyond these skills, by cultivating a healthy scepticism of financial institutions and the capabilities and confidence to make informed financial decisions.

There is a strong relationship between a low socioeconomic background and low financial literacy in both adolescents and adults.

It’s not just disadvantaged and vulnerable groups that struggle with financial decision-making. People who are highly educated in finance also make poor decisions – for instance, by focusing too much on growing their assets and ignoring risks.

But studies show that when regulation is effective and the financial system can be trusted, even consumers with limited financial knowledge and information-processing capabilities have the potential to deal with complex financial decisions.

For example, when considering mortgage protection insurance, applicants stand to benefit from knowing the actual risk of events like serious illness or injury that can affect their ability to meet monthly loan repayments.

Building financial capability

One way to develop better financial literacy is through simulating real-world risks, rewards and decisions in safe and supportive environments. For instance, families can play games like Monopoly and The Game of Life.

Secondary school students also have access to more sophisticated online simulations, such as the ESSI Money Game and the ASX Sharemarket Game.

Hypothetical scenarios like these provide opportunities for role play, where students can practise drawing on evidence and using it to think and reason about situations.

A recent survey of teachers of Year 7-10 commerce students revealed that more could also be done to teach students how to compare and choose between banks and financial products and services, what to do in the case of a financial scam, and how to escalate an unresolved complaint.

A key call to action in these programs is often to open a bank account and activate a savings plan. In the Solve to Save program, parents pay a $10 weekly subscription, which is “automatically refunded” to their child’s nominated Westpac account every week they complete three mathematics exercises.

While the banks may be proud of their investment in these education programs, they serve to position the banks as experts in money matters while cultivating trust and brand loyalty.

What does it really mean to be smart with money?

Misguided trust has exposed vulnerable individuals to the moral hazard of the banks – and underscores the importance of improved financial regulation and education moving forward.

Given that borrowing decisions are complex, multidimensional and often emotional, it’s important to consider any lender’s motives, or “What’s in it for them?” Banks are profit-driven. This means an important question to ask oneself is: “Where can I get information and support that is independent, comprehensive and easy to understand?”

In the current climate, teaching capabilities for a healthy scepticism and personal agency is the way forward.

We also need to change the public perception of what it means to be financially literate. The conventional focus on individual responsibility and wealth accumulation is flawed.

Arguably, this focus has contributed to the need for a Financial Services Royal Commission. Whether you are a bank, a mortgage broker or a consumer, the impact of your decisions on others must be carefully considered.

While education can contribute to preparing all Australians for informed financial participation, the task is challenging.

Authors: Carly Sawatzki, Assistant Professor, University of Canberra; Levon Ellen Blue, Lecturer, Queensland University of Technology

Ten years ago the Australian government launched a National Partnership Agreement on Homelessness (NPAH). It injected A$800 million into homelessness services and A$300 million to build 600 new homes for people experiencing homelessness. It was later announced that another A$400 million would be available under the National Affordable Housing Agreement (NAHA) to build new housing and supported accommodation for the homeless. Total recurrent expenditure (at 2016-17 prices) on homelessness services has increased by 28.8%, from A$634.2 million in 2012-13 to A$817.4 million in 2016-17.

But despite this, the number of people experiencing homelessness and the rate of homelessness have both increased. Our research points to problems in the public housing system as one of the more important causes of these increases.

According to census figures released on Wednesday by the Australian Bureau of Statistics (ABS), the number of homeless people in Australia has risen by 14% to 116,427. The rate of homelessness has increased from 47.6 people per 10,000 of the population in 2011, to 49.8 per 10,000 now. (The ABS defines homelessness here.)

There is some good news: the numbers of Indigenous homeless and homeless children and youth (aged 12-18) have declined by 26%, 11% and 7% respectively since 2011. But on the downside, increases are particularly pronounced in New South Wales (where the homelessness rate rose by 27% and among people aged over 65 (by just over 30%) and overseas-born migrants (by 40%).

Why are we still going backwards?

Changes in Australian housing and welfare systems and wider social and economic developments appear to have more than offset any benefits from the NPAH and NAHA. Our research sheds some light on the role played by Australia’s housing system. Using the internationally recognised and unique Journeys Home longitudinal survey, we find that public housing is the most important factor in preventing homelessness among vulnerable people.

Public housing is particularly effective because it is affordable. It has also traditionally offered a long-term refuge for precariously housed people. This is because public housing leases provide the benefits of security of tenure commonly associated with home ownership.

It is perhaps no accident that NSW was one of the first states to introduce fixed-term tenancies in public housing. This eroded one of the major attributes of tenure, in a state that has seen relatively large increases in homelessness numbers.

The empirical evidence also suggests that community housing fails to provide the same protection for people at risk of homelessness. While community housing is affordable, the security of tenure is weaker, which may explain these findings.

Despite such evidence, the stock of public housing continued to decline between the 2011 and 2016 censuses. State government-initiated transfers of stock to the community housing sector accelerated this trend. In 2013 Australia had a public housing stock of 325,226 dwellings. This declined by 3.2% to 314,864 usable dwellings in 2017.

Where are the additional homeless coming from?

One of the more alarming changes is a sharp increase in the number of homeless people over 65. This partly reflects Australia’s ageing population. However, the increase is such that the elderly’s share of the total homelessness count has also risen.

Furthermore, our research suggests that this trend could become protracted. This is because the homeless elderly have much less chance of escaping into formal housing than younger people experiencing homelessness. We have little understanding of the reasons for this, but gaps in service provision to the aged could be partly responsible.

The other group who feature prominently among the homeless are overseas migrants. They now make up 46% of the homeless, despite representing just 28% of the Australian population. The number of homeless overseas-born migrants has soared by 40% since the 2011 Census, from 38,085 to 53,606 people.

It turns out that homeless overseas-born migrants are concentrated among those living in severely overcrowded dwellings – a little over half of those living in these conditions were born overseas. We know little about these homeless people. Discrimination could be a factor, though some characterise this group as students living in group households who should not be considered homeless. But this is speculation and further study is certainly required.

In view of the latest census results, it is clear to us that governments need to reassess their approach to what is turning into an intractable social problem.

We do not deny that situational factors, such as drug abuse, domestic violence and so forth, are important here. But equally, there is strong evidence that structural problems in our housing market are a significant cause of growth in the numbers of homeless people.

Until these problems are resolved, service provision and support will remain a band-aid masking deeper social and housing system issues.

Gavin Wood, Emeritus Professor of Housing and Housing Studies, RMIT University; Guy Johnson, Professor, Urban Housing and Homelessness, RMIT University; Juliet Watson, Lecturer, Urban Housing and Homelessness, RMIT University; Rosanna Scutella, Senior Research Fellow, Centre for Applied Social Research, RMIT University

The disparity between bank CEO pay and average weekly earnings is contributing to the uncompetitive nature of Australia’s economy, argues progressive think tank The Australia Institute.

The GFC+10: Executive Pay in Australia report released yesterday by the Australia Institute has scrutinised the pay packages of executives at Australia’s biggest companies 10 years on from the global financial crisis.

Homing in on banks, which had “been a particular focus of attention” in recent times, the report found NAB and Commonwealth Bank of Australia bosses respectively earned 108 and 93 times the average weekly earnings in 2017.

“Pay for the NAB CEO peaked in 2004 but even if we ignore that spike the data still show that CEO pay was increasing rapidly during the bulk of the 2000s, as people were expressing the most concern.”

For the chief executive of CBA at the time, the spike in pay was widest in the lead-up to the global financial crisis.

In fact, seven- or eight-figure remuneration packages were “likely to have played an important role in the global financial crisis” wherein chief executives risked long-term performance for short-term gains, the report said.

Such a significant gap in the earnings of average workers compared with top executives also reflected “to a large extent the uncompetitive nature of the modern Australian economy”.

“It has to be stressed that the issue of massive CEO pay is one associated with industry concentration and the dominance of big business in the Australian economy,” it said.

“According to tax office data 390,774 companies reported a positive income and declared taxable income of $281 billion, giving the ‘average’ company an income of $719,201 in 2015.

“An economy dominated by ‘average’ companies could never pay CEOs anything like the amounts going to the CEOs of the top Australian oligopolies and monopolies,” said the report.

While “growth in CEO pay was quite dramatic in the lead up to around 2007 or 2008” and had moderated since then, the report concluded remuneration for these top executives “remains excessive”.

The ACCC has instituted proceedings in the Federal Court against credit reporting body, Equifax Pty Ltd (formerly Veda Advantage Pty Ltd), alleging breaches of the Australian Consumer Law (ACL).

The ACCC alleges that from June 2013 to March 2017, Equifax made a range of false or misleading representations to consumers, including that its paid credit reports were more comprehensive than the free reports, when they were not.

Equifax also allegedly represented that consumers had to buy credit reporting packages for it to correct information held about them, or to do so quicker. In fact, Equifax was required by law to take reasonable steps to correct the information in response to a consumer’s request for free.

In addition, the ACCC alleges that Equifax represented that there was a one-off fee for its credit reporting services, when its agreement provided that customer’s subscriptions to the services automatically renewed annually unless the consumer opted out in advance. We allege this renewal term is an unfair contract term, which is void under the ACL.

In all the circumstances, it is alleged that Equifax acted unconscionably in its dealings with vulnerable consumers including by making false or misleading representations, and using unfair tactics and undue pressure when dealing with people in financial hardship.

“We allege that Equifax acted unconscionably in selling its fee-based credit reporting services to vulnerable consumers, who were often in difficult financial circumstances,” ACCC Commissioner Sarah Court said.

“We allege that Equifax told people they needed to buy credit reporting services from them in situations when they did not. It is important for consumers to know they have the legal right to obtain their credit report and to correct any wrong information for free.”

By law, consumers are entitled to access their credit reporting information for free once a year, or if they have applied for, and been refused, credit within the past 90 days, or where the request for access relates to a decision by a credit reporting body or a credit provider to correct information included in the credit report.

One worrying takeaway from the first week of the Financial Services Royal Commission is how many elderly people are being adversely affected by irresponsible lending.

Such lending is often the result of an agreement with a family member, for example an adult child, to help that person financially by entering into a joint loan. These loans are secured against the older person’s home, which is a huge risk if the loan defaults and the older person cannot service the debt.

To ensure that older people contemplating joint loans are aware of the downside of transactions, there needs to be greater access to legal and financial advice prior to the transaction and better training for bank employees and loan officers about responsible lending obligations and the potential “unsuitabilty” of such loans.

Consideration should also be given to larger penalties for banks that provide unsuitable loans to older people.

On the face of it, there are laws that should safeguard elderly consumers from “getting in over their head”.

When a consumer applies for credit, the National Consumer Credit Protection Act obliges a credit provider to make reasonable inquiries about the consumer’s financial situation and their requirements and objectives.

However, the Consumer Action Law Centre says that “it is common that these steps are not adequately followed by lenders”.

Even if these steps are followed, the legislation does not define “substantial hardship”. There is a presumption that if a consumer must sell their principal residence to pay back a loan, this demonstrates substantial hardship.

Emotional lending

Of particular concern is when an older person is persuaded to enter into a joint loan with a third party, such as their son or daughter. These loans are invariably secured by the older person’s property, with the younger person agreeing to pay off the debt.

If the adult child does not pay off the debt, the older person – who is often asset-rich but income-poor – may be unable to service the loan. The older person’s property will be repossessed by the lender, forcing them to relocate, enter the rental market, or even become homeless.

The loans may arise simply because the older person wants to help their adult child through a difficult financial period. It is understandable that a parent would want to help if a business is failing or a child is at risk of losing their house.

But such loans often arise within an atmosphere of crisis (real or exaggerated), in which the adult child pressures the older person into entering into the loan.

In extreme cases, older people have been told that they will be unable to see their grandchildren if they do not enter into loans.

It is not always that the older person is vulnerable per se, but that they are “situationally vulnerable” because of concern for the well-being of a child, or the desire to maintain relationships.

The reality is that it is often difficult for the older person to refuse.

Karen Cox of the Financial Rights Legal Centre noted at the Royal Commission that these loans are:

outright exploitative … elderly persons [are] left in dire circumstances as a result of a loan for which they’ve seen absolutely no benefit.

Similar comments apply to other financial transactions made for the benefit of a third party such as entering into a “reverse mortgage”. This is where the older person takes out a loan against the equity built up in a home (or other asset), with the money given to a child to buy a house or prop up their business.

What could be done?

Advocates are rightly concerned about the financial consequences for older people who enter into such loans. However, the property does belong to the older person and they are entitled to make whatever decisions they want, including risky ones.

Elderly people should be fully informed of their obligations and the potential consequences, should a transaction goes wrong. Banks could lead the way with this.

One initiative would be for the banks to contribute to legal and financial advice for older people, or subsidise the provision of such advice at community legal centres.

Loan assessors and brokers must also be made aware of the risks of such transactions.

The Australian Bankers Association is introducing enhanced measures to address elder financial abuse and the risks associated with such loans should be emphasised.

Finally, the government should consider tougher penalties against credit providers who disregard responsible lending obligations. Presently, if a bank is found to have lent irresponsibly they will simply compensate the consumer for the loss. Meaningful penalties that deter reckless lending should be considered.

Author: Eileen Webb, Professor, Curtin Law School, Curtin University

Australia has a housing affordability problem. There’s no doubt about that. Unfortunately, one of the reasons the problem has become so entrenched is that the policy conversation appears increasingly confused. It’s time to debunk some policy clichés that keep re-emerging.

Is ‘zoning’ to blame?

It can be tempting to frame the housing affordability problem as all about inadequate new supply. According to this argument, the “demand side” drivers – such as low interest rates and tax incentives for property investment – have combined with population growth in the capital cities to fuel house prices, and new housing construction simply hasn’t kept up.

“Zoning” is often blamed. There is little hard evidence, though, to show systematic regulatory constraint.

Supply is at record highs, and in the right places

According to the cliché, this supply response should have cooled prices. Yet dwelling price inflation has surged even in metropolitan areas where new housing supply has exceeded population growth.

The fallacies of ‘filtering’

One of the great hopes underpinning the supply cliché is that new housing stock improves affordability even if these homes are not affordable for lower-income groups. This faith is based on a theory called “filtering” whereby older housing moves down to the affordable end of the market over time.

The empirical data on filtering are thin. Indeed, the academic literature has historically cast doubt on the theory. However, some commentators continue to claim that American rental housing markets provide evidence that “filtering” can occur in practice.

But whatever might happen in the US, in Australia there’s still no evidence to suggest new housing supply has filtered across the housing stock to expand affordable housing opportunities for low-income Australians, or that it will do so any time soon.

Some commentators cite cooling house prices as evidence that the supply response is taking effect. Whether or not that is so (above and beyond demand-side factors like higher interest rates for investor loans), expect the pipeline to start slowing down. Private sector development is driven by profit and risk and, as we have seen over many years, is characterised by speculative booms and busts.

Developers can turn off the new supply tap much more quickly than they can turn it on. Falling prices, weak consumer sentiment and economic uncertainty mean many developers will not follow through on building approvals until the market recovers.

This means that high levels of supply output are rarely sustained. Recent housing data in Western Australia provide a case in point. WA recorded rising completions in 2014, 2015 and 2016. But 2017 completion figures are expected to show a drop of around a third as prices have shaded off since the end of the mining boom.

Put simply, the market on its own will never solve Australia’s housing affordability problem. Expecting developers to keep building in order to reduce house prices is pure fantasy.

Planning reform is not an affordable housing strategy

They have aimed to: standardise and simplify planning rules; promote mixed use and higher-density housing near train stations; and overcome local political opposition to development through the use of independent expert panels.

Housing targets for both urban infill and new greenfield areas have been a feature of metropolitan plans to drive dwelling approval rates since at least 2000.

These reforms have been effective in overcoming regulatory constraints. The scale of the recent supply response shows clearly that zoning and development assessment processes are not inhibiting residential development approvals in cities like Sydney and Melbourne.

But trying to accommodate Australia’s population growth in towers around railway stations will fail as an affordable housing strategy – even if “zoning” and height rules were completely scrapped.

Rather than narrow deregulation agendas, bigger picture reforms are needed. Aligning infrastructure funding with metropolitan and regional decentralisation is a critical long-term strategy. Reforms to deliver affordable housing in communities supported by new infrastructure are long overdue.

A bigger affordable housing sector is needed

Australia needs a more realistic assessment of the housing problem. We can clearly generate significant dwelling approvals and dwellings in the right economic circumstances. Yet there is little evidence this new supply improves affordability for lower-income households. Three years after the peak of the WA housing boom, these households are no better off in terms of affordability.

In part, this may reflect that fact that significant numbers of new homes appear not to house anyone at all. A recent CBA report estimated that 17% of dwellings built in the four years to 2016 remained unoccupied.

If we are serious about delivering greater affordability for lower-income Australians, then policy needs to deliver housing supply directly to such households. This will include more affordable supply in the private rental sector, ideally through investment driven by large institutions such as super funds. And for those who cannot afford to rent in this sector, investment in the community housing sector is needed.

In capital city markets, new housing built for sale to either home buyers or landlords is simply not going to deliver affordable housing options unless a portion is reserved for those on low or moderate incomes.

Authors: Nicole Gurran, Professor of Urban and Regional Planning, University of Sydney; Bill Randolph, Director, City Futures Research Centre, Faculty of the Built Environment, UNSW; Peter Phibbs, Director, Henry Halloran Trust, University of Sydney; Rachel Ong, Professor of Economics, School of Economics and Finance, Curtin University; Steven Rowley, Director, Australian Housing and Urban Research Institute, Curtin Research Centre, Curtin University

Today we discuss the Impossible Property Equation.

Welcome to the Property Imperative Weekly to 10th March 2018. Watch the video or read the transcript.

In this week’s review of property and finance news we start with CoreLogic who reported that last week, the combined capital cities returned a 63.6 per cent final auction clearance rate across 3,026 auctions, down from the 66.8 per cent across 3,313 auctions the week prior. Last year the clearance rate last year was a significantly higher at 74.6 per cent. Last week, Melbourne returned a final auction clearance rate of 66.5 per cent across 1,524 auctions, down from the 70.6 per cent over the week prior. In Sydney, both volumes and clearance rate also fell last week across the city, when 1,088 properties went to market and a 62.4 per cent success rate was recorded, down from 65.1 per cent across 1,259 auctions the week prior. Across the remaining auction markets clearance rates improved in Canberra and Perth, while Adelaide, Brisbane and Tasmania’s clearance rate fell over the week. Auction activity is expected to be somewhat sedate this week, with a long weekend in Melbourne, Canberra, Adelaide and Tasmania. Just 1,526 homes are scheduled for auction, down 50 per cent on last week’s final results.

In terms of prices, Sydney, Australia’s largest market is a bellwether. There, CoreLogic’s dwelling values index fell another 0.13% this week, so values are down 4.0% over the past 26-weeks. Also, Sydney’s annual dwelling value is down 1.04%, the first annual negative number since August 2012. Within that, the monthly tiered index showed that the top third of properties by value in Sydney have fallen hardest – down 3.2% over the February quarter – whereas the lowest third of properties have held up relatively well (i.e. down 0.9% over the quarter), thanks to a 68% rise in first time buyers. My theory is Melbourne is following, but 9-12 months behind.

The RBA published a paper on the Effects of Zoning on Housing Prices. Based on detailed analysis they suggest that development restrictions (interacting with increasing demand) have contributed materially to the significant rise in housing prices in Australia’s largest cities since the late 1990s, pushing prices substantially above the supply costs of their physical inputs. They estimate that zoning restrictions raise detached house prices by 73 per cent of marginal costs in Sydney, 69 per cent in Melbourne, 42 per cent in Brisbane and 54 per cent in Perth. There is also a large gap opening up between apartment sale prices and construction costs over recent years, especially in Sydney. This suggests that zoning constraints are also important in the market for high-density dwellings. They say that policy changes that make zoning restrictions less binding, whether directly (e.g. increasing building height limits) or indirectly, via reducing underlying demand for land in areas where restrictions are binding (e.g. improving transport infrastructure), could reduce this upward pressure on housing prices.

At its February meeting, the RBA Board decided to leave the cash rate unchanged at 1.50 per cent. Their statement was quite positive on employment, but not on wages growth. They are expecting inflation to rise a little ahead, above 2%. They said that the housing markets in Sydney and Melbourne have slowed and that in the eastern capital cities, a considerable additional supply of apartments is scheduled to come on stream over the next couple of years.

The RBA quietly revised down the household debt to income ratio stats contained in E2 statistical releases and their chart pack. It has dropped by 6% from 199.7 down to 188.4, attributing the change to revised data from the ABS. But it is still very high. By the way, Norway, one of the countries mirroring the Australian mortgage debt bubble, at 223 has just taken steps to tighten mortgage lending further. This includes a limit of 5x gross annual income and a 5% interest rate buffer.

We released our February Mortgage Stress data, which showed across Australia, more than 924,500 households are estimated to be now in mortgage stress, up 500 from last month. This equates to 29.8% of households. In addition, more than 21,000 of these are in severe stress, up 1,000 from last month. We estimate that more than 55,000 households risk 30-day default in the next 12 months, up 5,000 from last month. You can watch our separate video on this. Our surveys showed significant refinancing is in train, to try to reduce monthly repayments. We publish our Financial Confidence Indices next week.

The retail sector is still under pressure, as shown in the ABS trend estimates for Australian retail turnover which rose just 0.3 per cent in January 2018 following a similar rise in December. Many households just do not have money to spend. Separately, the number of dwellings approved rose 0.1 per cent in January, driven by a lift in approvals for apartments. Dwelling approvals increased in Victoria, Tasmania, Queensland and Western Australia, but decreased in the Australian Capital Territory, the Northern Territory, South Australia and importantly New South Wales.

The ABS also released the account aggregates to December 2017. Overall the trend data is still pretty weak. GDP has moved up just a tad, but GDP per capita is growing at just 0.9% per annum, and continues to fall. Much of the upside is to do just with population growth. But net per capita disposable income rose at just 0.4% over the past year. Housing business investment and trade were all brakes on the economy. Real remuneration is still growing at below inflation, so incomes remains stalled. More than two in three households have seen no increase. It rose by 0.3% in the December quarter and was up just 1.3% over the year to December 2017, compared with inflation of 1.9%. In fact, households continue to raid their savings to support a small increase in consumption, but this is not sustainable. The household savings ratio recovered slightly to 2.7% from 2.5% in seasonally adjusted terms. Debt remains very high. These are not indicators of an economy in prime health!

Another crack appeared in the property market wall this week when Deposit Power, which provided interim finance to property buyers, closed its doors leaving an estimated 10,000 residential, commercial and property investors in the lurch about the fate of nearly $300 million worth of deposits. This is after the collapse of New Zealand’s CBL’s insurance, which was an issuer and guarantor of deposit bonds. You can watch my separate video on this important and concerning event.

The public hearings which the Productivity Commission has been running in relationship to Competition in Financial Services covered a wide range of issues. One which has surfaced is the Lenders Mortgage Insurance (LMI) sector. With 20% of borrowing households required to take LMI, and just two external providers (Genworth and QBE LMI), the Commission has explored the dynamics of the industry. They called it “an unusual market”, where there is little competitive pricing nor competition in its traditional form. Is the market for LMI functioning they asked? Could consumers effectively be paying twice? On one hand, potential borrowers are required to pay a premium for insurance which protects the bank above a certain loan to value hurdle. That cost is often added to the loan taken, and the prospective borrower has no ability to seek alternatives from a pricing point of view. Banks who use external LMI’s appear not to tender competitively. On the other hand, ANZ, for example has an internal LMI equivalent, and said it would be concerned about the concentration risk of placing insurance with just one of the two external players, as the bank has more ability to spread the risks. The Commission probed into whether pricing of loans might be better in this case, but the bank said there were many other factors driving pricing. All highly relevant given the recent APRA suggestion that IRB banks might get benefit from lower capital for LMI’s loans, whereas today there is little capital benefit. This will be an interesting discussion to watch as it develops towards the release of the final report. They had already noted that consumers should expect to receive a refund on their LMI premium if they repay the loan.

ASIC told the Productivity Commission that there is now “an industry of referrers” who are often being paid the same amount as mortgage brokers despite doing less work. They said – in our work on [broker] commissions, there were a separate category of people who are paid commission who don’t arrange the loan but just refer the borrower to the lender. It seems to be that professionals — lawyers, accountants, financial advisers — are reasonably prominent among people who are acting as referrers and that strangely the commissions they were paid for just a referral was almost as large as that [for a] mortgage broker doing all the extra [work]. More evidence of the complexity of the market, and of the multiple parties clipping the ticket.

The role of mortgage brokers remains in the spotlight, with both the Productivity Commission sessions this week, and the Royal Commission next week focussing in on this area. In draft recommendation 8.1 of its report, the Productivity Commission called for the ASIC to impose a “clear legal duty” on lender-owned aggregators, which should also “apply to mortgage brokers working under them”. ANZ CEO Shayne Elliott said applying best interest obligations to brokers could help preserve the integrity of the third-party channel and that despite the absence of a legal duty of care, consumers may be under the impression that such obligations already exist. He also said there was merit in considering a fixed fee model as opposed to a volume-based commission paid to brokers. The ANZ chief said that there is “absolute merit” in exploring such a model, and he pointed to the use of a fixed fee structure in Europe.

Industry insiders on the other hand argue that a push to argue a switch from mortgage broker commission payments, which normally includes an upfront fee and a trailing payment for the life of the loan paid by the lender to the broker, to a fixed fee for advice would be “anti-competitive. The discussion of trailing commissions centered on whether there was downstream value being added to mortgage broker clients, for example, annual financial reviews, or being the first port of call when the borrower has a mortgage related question. The interesting question is how many broker transactions truly include these services, or is the loan a set and forget, whilst the commissions keep flowing? There is very little data on this. In the UK, mortgage brokers work within a range of payment models. Many mortgage brokers are paid a commission by lenders of around 0.38% of the total transaction and some mortgage brokers also charge a fee to their customers.

Still on, Mortgage Brokers they say they expect to write more non-conforming loans over the next 12 months according to non-Bank Pepper Money. They commissioned a survey of 948 mortgage brokers which showed that 70 per cent expect to write more non-conforming loans in the coming year, while 66 per cent predict a decline in the number of prime loans written. Surveyed respondents expect the demand for non-conforming loans to rise as a result of tighter prime lending criteria (22 per cent), changing customer needs (21 per cent) and changing legislation/regulations (13 per cent). The survey also found that the number of brokers who have yet to write a non-conforming loan has also reduced, falling by 6 per cent from 18 per cent in 2016 to 12 per cent in 2018.

Another non-Bank, Bluestone Mortgages cut its interest rates by 75 to 105 basis points across its Crystal Blue products. The Crystal Blue portfolio includes a range of full and alt doc products that provide lending solutions to established self-employed borrowers (with greater than 24 months trading history), and PAYG borrowers with a clear credit history. The lender expects the rate reduction, coupled with the 85% low doc option, to drive the uptake of the portfolio. The rate cuts come shortly after the company was acquired by private equity firm Cerberus Capital Management. Parent company Bluestone Group UK is fully divesting its interest in Bluestone Mortgages Asia Pacific as part of the acquisition deal.

The ABS released their latest data on the Assets and Liabilities of Australian Securitisers. At 31 December 2017, total assets of Australian securitisers were $132.5b, up $7.3b (5.9%) on 30 September 2017. During the December quarter 2017, the rise in total assets was primarily due to an increase in residential mortgage assets (up $6.0b, 6.0%) and by an increase in other loans assets (up $0.9b, 6.1%). You can see the annual growth rates accelerating towards 13%. This is explained by a rise in securitisation from both the non-bank sector, which is going gangbusters at the moment, and also some mainstream lenders returning to the securitised funding channels, as costs have fallen. There is also a shift towards longer term funding, and a growth is securitised assets held by Australian investors. Asset backed securities issued overseas as a proportion of total liabilities decreased to 2.6%. Finally, at 31 December 2017, asset backed securities issued in Australia as a proportion of total liabilities increased to 89.8%. The non-banks are loosely being supervised by APRA (under their new powers), but are much freer to lend compared with ADI’s. A significant proportion of business will be investment loans.

It’s not just the non-banks cutting mortgage rates to attract new business. The story so far. Banks were lending up to 40%+ of mortgages with interest only loans, some even more. The regulator eventually put a 30% cap on these loans and the volume has fallen well below the limit. Some banks almost stopped writing IO loans. They also repriced their IO book by up to 100 basis points, so creating a windfall profit. This is subject to an ACCC investigation to report soon. The RBA and APRA both warn of the higher risks on IO loans, especially on investment properties, in a down turn. APRA has confirmed the “temporary” 30% cap will stay for now, although the 10% growth cap in investment loans is now redundant, thanks to better underwriting standards. Banks have now started to ramp up their selling of new IO loans, to customers who fit within current underwriting standards and are offering significant discounts. Borrowers will be encouraged to churn to this lower rate. For example, CBA will cut fixed interest rates for property investors across one-, two-, three-, and four-year terms. The cuts, which range from 5 basis points to 50 basis points, apply to both interest-only investor loans and principal-and-interest investor loans. CBA is also cutting some of its fixed rates for owner-occupiers, including a reduction on owner-occupied principal-and-interest fixed-rate loans by 10 basis points over terms of one to two years, landing at 3.89% for borrowers on package deals. Key rival Westpac also unveiled a suite of fixed-rate changes, including some cuts to fixed-rate interest-only mortgages, another area where banks have been forced to apply the brakes. They also hiked rates across various fixed terms for owner-occupiers. So the chase is on for investor loans now, with a focus on acquiring good credit customers from other banks. Other smaller lenders, such as ING, Mortgage House, and Virgin Money have also dropped some interest-only rates.

Finally, The Grattan Institute released some important research on the migration and housing affordability saying Australia’s migration policy is its de-facto population policy. The population is growing by about 350,000 a year. More than half of this is due to immigration. The pick-up in immigration coincides with Australia’s most recent housing price boom. Sydney and Melbourne are taking more migrants than ever. Australian house prices have increased 50% in the past five years, and by 70% in Sydney. Housing demand from immigration shouldn’t lead to higher prices if enough dwellings are built quickly and at low cost. In post-war Australia, record rates of home building matched rapid population growth. House prices barely moved. But over the last decade, home building did not keep pace with increases in demand, and prices rose. Through the 1990s, Australian cities built about 800 new homes for every extra 1,000 people. They built half as many over the past eight years. So there is no point denying that housing affordability is worse because of a combination of rapid immigration and poor planning policy. Rather than tackling these issues, much of the debate has focused on policies that are unlikely to make a real difference. Unless governments own up to the real problems, and start explaining the policy changes that will make a real difference, Australia’s housing affordability woes are likely to get worse.

So the complex equation of supply and demand, loan availability and home prices, will remain unsolved until the focus moves from tactical near term issues to strategy. Meantime, my expectation is that prices will continue south for some time yet, despite all the industry hype.

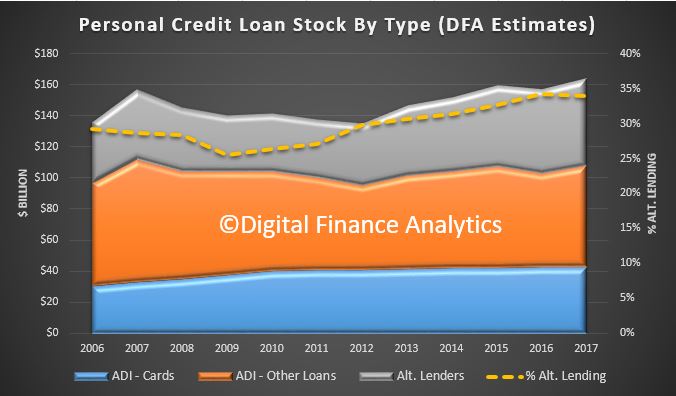

Household debt in Australia continues to rise. But the strongest growth at 15%, is found in the sub prime Alternative Lending Personal Credit sector.

So it is worth considering the personal credit market holistically.

Drawing data from our cure market models we estimate total personal credit to the ~9.2 million Australian households currently amounts to $164 billion. This is separate from the $1.7 trillion secured debt for owner occupied and investment housing.

Within that banks and mutuals (ADI’s) hold $42 billion in credit cards, and $66 billion in personal loans of all types. But this leaves Alternative Lenders, (non-banks) with around $56 billion, or 34% of all personal credit. The chart below shows the relative shares since 2006. The Alternative Lending sector is growing faster than credit from ADI’s.

Relatively, overall personal credit has grown at around 2.6% in the past 3 years. Within that, credit card debt has been static, ADI personal credit rose 2% but Alternative Lending credit rose 5%.

In fact ADI’s have stepped up their personal lending as mortgage lending has eased, with an 8% rise in the past 12 months. We expect this momentum to continue, with a strong focus on vehicle credit, another risk area!

Alternative Lenders include many large well established companies, as well as a rising tide of new online lenders, including P2P loan providers. In fact online has become the predominate origination channel. As they are not banks, ASIC is the primary regulatory body.

But looking in more detail, the sub prime segment of Alternative Lending has growing significantly faster at around 15% per annum over the past three years, compared with 5% for all Alternative Lending. We define sub prime as households with VedaScore/Equifax Score below 622, or a poor credit history, or adverse personal circumstances.

There are a range of products taken by households in the sub prime segment, including unsecured personal loans, Medium Amount Credit Contracts (MACC), Small Amount Credit Contracts (SACC), secured and unsecured car loans or loans on other capital goods, and loans secured by assets, such as cars post purchase.

Our surveys show that a considerable number of highly in debt households with mortgages also hold loans with Alternative Lenders. Such loans might be difficult spot during an assessment of a mortgage loan application, thanks to the negative credit records which are only now morphing into comprehensive credit.

This is a concerning trend and is further evidence of the debt laden state of many households. It also helps to explain the gap between stated finances on a mortgage loan application and the real state of household finances.

The slide was more significant among those households with investment properties, thanks to higher mortgage rates, concerns about interest only loan resets and lower home prices. In additional net rentals are lower. Owner occupied households also fell just a small amount, mainly because of rising living costs against flat incomes. Those renting, or otherwise excluded from property are the least confident. This continues the long term trend, indicating that property ownership still bolsters confidence to some extent.

The slide was more significant among those households with investment properties, thanks to higher mortgage rates, concerns about interest only loan resets and lower home prices. In additional net rentals are lower. Owner occupied households also fell just a small amount, mainly because of rising living costs against flat incomes. Those renting, or otherwise excluded from property are the least confident. This continues the long term trend, indicating that property ownership still bolsters confidence to some extent. The slide was pretty consistent across the states, other than a small lift in WA. Compared with a year ago, confidence levels in NSW and VIC are significantly lower.

The slide was pretty consistent across the states, other than a small lift in WA. Compared with a year ago, confidence levels in NSW and VIC are significantly lower. We also see a similar story across all the age bands, suggesting the decline in confidence is similarly widely spread.

We also see a similar story across all the age bands, suggesting the decline in confidence is similarly widely spread. To understand the reasons for the falls we can look to the index scorecard. Overall, there was a rise of 1.2% in households feeling less secure about their jobs, compared with this time last year, and a small reduction in those feeling more secure.

To understand the reasons for the falls we can look to the index scorecard. Overall, there was a rise of 1.2% in households feeling less secure about their jobs, compared with this time last year, and a small reduction in those feeling more secure. Based on our research, we see little on the horizon to suggest that household financial confidence will improve. We expect wages growth to remain contained, and home prices to slide, while costs of living pressures continue to grow. There will also be more pressure on mortgage interest rates as funding costs rise, and lower rates on deposits as banks trim these rates to protect their net margins.

Based on our research, we see little on the horizon to suggest that household financial confidence will improve. We expect wages growth to remain contained, and home prices to slide, while costs of living pressures continue to grow. There will also be more pressure on mortgage interest rates as funding costs rise, and lower rates on deposits as banks trim these rates to protect their net margins.