In the current housing tax debate a number of studies have come out arguing that while prices will fall (by varying amounts) rents will not be affected. That rents will be unaffected is surprising and (in my view) wrong.

Outside of the heat of an election, the Henry Tax Review’s comprehensive review of the tax system argued for lower taxes on savings, a proposition that most economists would regard as unexceptional. (There is now a (small) school of thought arguing for higher taxes on savings but this author for one does not subscribe to that.)

Specifically, the Henry Review recommended the marginal tax rates on interest and rental income should be 40% lower; for example, the 35% and 45% income tax rates on labour income would be lowered to 21% and 27%. For property investors these rates would also apply to capital gains and net losses, thereby reducing the value of negative gearing.

For ‘ungeared’ investors (those who do not take on debt), the effective tax rate would be lower while for highly geared investors the effective tax rate would be higher, leading to less incentive to leverage (making the Reserve Bank of Australia happy). Overall, the effective tax rate for the “average” investor would be higher.

Now the Henry Review acknowledged that its proposed changes would, by lifting the user cost of capital of investors, lift rents. It therefore explicitly said that its proposed changes would need to be accompanied by measures to both lower the cost of housing by removing supply constraints, and to lift levels of rental assistance for households in the private rental market. In short, it did not see the increases in rents as immaterial.

If the increase in user cost of capital (on investors who are ‘geared’ by borrowing money to invest) with the Labor proposal is higher (roughly double), on what basis could rents not rise? It is not evident to me.

The key component of the user cost of capital, and the one which varies the most over time, is interest rates. When interest rates rise or fall, we expect prices to fall, or rise. But interest rates also change rents, since rent = user cost × value of house.

And what we also see is that a rise in interest rates causes the rent-price ratio (that is, the ratio of home prices to annual rent, also referred to as the rental yield) to rise, while a drop in interest rates will see it fall.

To illustrate, consider Melbourne for the period 1991-2014 when interest rates have fallen significantly and the rent-price ratio has followed suit. This has seen prices increase significantly (4.9% pa in real terms), and faster than the rise in costs (3.2%). In inner areas where there is a significant location premium (over living at the urban fringe), the rise in prices has been fastest (5.8%) as the value of that location premium has been bid up.

That is, most of the change in the rent-price ratio has come from rising prices. On the other hand, in the outer areas, where there is no location premium and the value of a house is the structure plus the cost of land, prices (3.4% pa) have moved in line with costs (3.2% pa) but rents have risen much more slowly (1.4%). That is, rents explain the decline in rent-price ratios.

So, while the assumption of most commentators is that price movements do the work in changing rent-price ratios, and that is so over the short term, over a longer time span, rents do some of the adjustment.

Changes in interest rates are uncontroversial. But the same principles apply to changes in tax if they change the cost of capital, which is why the Henry Review expected rents to rise.

In the case of the Labor’s negative gearing changes, the waters are muddied for some by its proposed exemption on new housing. A couple of points here. Firstly, ABS figures (see Table 8 from ABS5671.0 – Lending Finance, Australia) are quoted to suggest that investors’ purchases are 93% established housing, and only 7% new housing. This significantly understates the role of investors.

The NAB residential property survey has domestic investor purchases of new housing at about 20-30% – that is, domestic investors are already a significant component of the new market (adding to supply!).

Secondly, Henry also expected a change in the mix of landlords to consolidate from one with a large number of small landlords, to one with a smaller number of large landlords. More marginal investors – middle income/low wealth investors – will be the first to vacate the field as their entry point is typically cheaper, old stock not premium new stock.

High income/low wealth investors will have the option of new dwellings. High income/high wealth individuals will benefit from the higher rents and lower prices on established dwellings.

That is, the ownership of the dwelling stock (and tax benefit!) will shift to the top end of income earners. But it is not clear that the special treatment of new housing will add materially, if at all, to supply of new dwellings.

In short, the law of unintended consequences will apply. Logic says that rents will rise, and with the 30% renting in the private market skewed to low income earners, that means housing affordability will have declined for these people.

Author: Nigel Stapledon, Andrew Roberts Fellow and Director Real Estate Research and Teaching Centre for Applied Economic Research, UNSW Australia

The ABC reported that “a Treasury document obtained by the ABC under Freedom of Information (FOI) shows most of the windfall from the property tax break goes to high-income earners. The modelling said more than half of the negative gearing tax benefits go to the top 20 per cent of incomes in Australia. “Negative gearing benefits high-income families,” the document said. The report stated those in the bottom 20 per cent were getting just over 5 per cent of negative gearing tax benefits”.

On the other hand, the Government has continued to argue “mum and dad” investors and Australians on average earnings are the main beneficiaries. “It does not change the fact that two thirds of Australians using negative gearing have a taxable income of less than $80,000,” Treasurer Scott Morrison said. This is of course axiomatic, but misses the point, because the whole idea of negative gearing is to offset interest costs and other losses to reduce total income, and therefore taxable income. Mr Morrison played down the heavily-redacted Treasury submission. “The numbers in the document released by Treasury are not Treasury numbers, but are a summary of a report from an ANU associate professor, Ben Phillips, that Labor uses to justify their negative gearing policy,” he said.

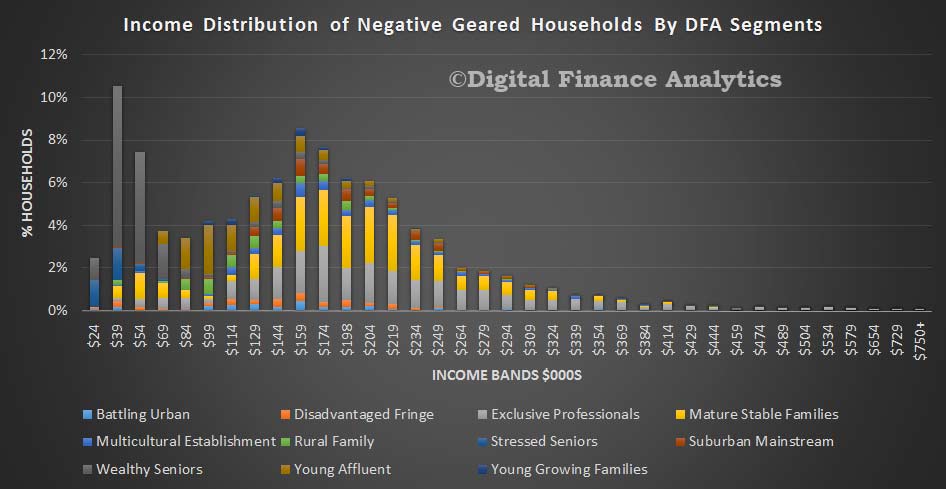

Worth then reflecting on earlier DFA analysis which showed how complex the negative gearing questions is. We pulled data from the DFA household surveys, to examine the distribution of negative gearing. Our segmented surveys, show some of the nuances in behaviour. We start with age distribution. We find that households of all ages may use negative gearing, but more than a quarter are aged 50-59. We see the DFA household segmentation in evidence, with a number of young affluent households active aged 20-29, especially using an investment property as an alternative to buying their own place to live. We discussed this before. As we progress up the age bands, we see a strong representation by the more affluent segments, including mature stable families and exclusive professionals. In later life, wealth seniors are also active, especially in the 60-69 year bands. So negative gearing is being used by households across all age groups.

Our survey suggests that negative gearing, whilst it is spread across the income bands, is indeed concentrated among more affluent households. Four segments, exclusive professionals, mature steady state, wealthy seniors and young affluent households contain the lions share of negative geared investment property. These segments are at different life stages, have different income profiles, and different strategies. For example the young affluent are often using investment property as a potential on-ramp to later owner occupied purchase, whereas wealthy seniors are all about income, and the others more wealth creation.

This analysis shows how complex the true situation is. Prospective changes are likely to impact different segments in diverse ways and there is plenty potential for spill-over impacts and unintended consequences. But the truth is, most negative gearing resides among more affluent households. The current settings are not correct.

It seems that in Australian politics – and this campaign in particular – everyone loves a small business.

Just before this year’s federal budget, Treasurer Scott Morrison said of small businesses: “they are the hope of the side.” Somewhat less pithily, but no less adoringly, Labor’s official policy on small business declares:

“Small businesses make a huge contribution to national prosperity and supporting Australian jobs. Small businesses play a central role in the economy. Over 2 million businesses – sole traders, partnerships, trusts and small employers – have helped underpin 25 years of economic growth.”

In fact, the only thing the major parties seem to disagree on is whether a small business has less than $2 million in annual revenues (the Labor definition) or less than $10 million (the Coalition definition).

But do small businesses, for desperate want of a better term, create “jobs and growth”?

The first relevant fact is that small businesses employ a lot of people. According to figures compiled by Saul Eslake, and discussed in a terrific piece by Adam Creighton in The Australian, business that employ fewer than 20 people account for roughly 45% of private sector employment.

Businesses with 20-199 employees account for about 25%, and businesses with 200+ employees, around 20%.

So small businesses are important employers. Check. Only problem is, they haven’t created a lot of jobs in the last five years. As Creighton pointed out, those small business created 5% of the growth in private sector employment since 2010, while businesses with more than 200 employees created 65% of that growth.

In one important sense, this should not be surprising. When looking at the landscape of firms of different sizes, existing firms exhibit what economists call “survivorship bias”. The very fact that a firm exists today means that it was created, and succeeded.

Big firms were created and really succeeded. So it’s likely that today’s big firms are, on average, more successful than today small firms at, well, getting big. And the way that happens is by, you guessed it, employing more people.

So much for the positive political economy of why politicians are desperate to ingratiate themselves with small businesses. There are a lot of them, hence a lot of potential votes.

But the real question, of course, is what tax policy should be. The Labor party wants to cut the company tax rate from 30% to 25% only for businesses with less than $2 million turnover. The Coalition wants to do that for all businesses, but over 10 years. In the medium term both parties want to cut taxes for mainly for small businesses, albeit to varying degrees.

To answer that question, we first need a quick primer on why everybody (at least until very recently in some cases) agreed that cutting company taxes help workers and the economy more broadly.

Roughly speaking, the amount of “stuff” produced in the economy depends on two inputs: capital and labour. Lowering the company tax rate attracts more capital – especially since Australia is a small, open economy. More capital means more stuff because capital is useful in production.

Moreover, more capital means that the marginal return to more labour goes up, too. That is because, generally speaking, capital and labour are complements in the production process. More of one makes more of the other more valuable at the margin.

Aside: forget all the jibberish you have recently read about dividend imputation and franking credits. That’s a second-order issue – the key is the complementarity between capital and labour.

This increased marginal return to labour means more jobs and higher wages–capital made labour more valuable, and labour captures some of that benefit. This is why Treasury has estimated that two-thirds of the benefit from a cut in company taxes flows to workers.

Now, do small businesses or big businesses use more capital? Answer: big businesses (See here, page 3). So it is big businesses that will increase the amount of capital they use the most from a cut in company taxes. And it is big businesses that will thus drive more employment growth and higher wages.

To sum up. Small businesses employ lots of people. But they haven’t driven much of the job growth in Australia over the past five years. And a company tax cut won’t cause them to stimulate employment as much as it will for bigger businesses.

We should cut company taxes, and we should cut them for all firms. But it makes no sense to favour small businesses over bigger ones.

That’s the economics of the matter. What we are witnessing in this election campaign – on both sides – is pure politics.

Author: Richard Holden, Professor of Economics, UNSW Australia

A number of politicians have struggled this week to explain the Turnbull Government’s proposed changes to superannuation. Given the complexity of the area, that’s not surprising. And this complexity explains why intergenerational “theft” through superannuation has continued for so long.

Transition to retirement (TTR) provisions, introduced by the Howard Government in 2005, were supposed to encourage people to keep working part-time rather than stopping work entirely. Yet most people using a TTR pension have continued to work full time. In practice the provisions have simply been a gift enabling older people to pay less tax than younger people on similar incomes.

No-one has ever explained why we should have an age-based tax system, beyond the politically cynical observation that these provisions were introduced when demographics produced an unusually large number of voters aged 55 to 64. Some of these voters are now objecting vociferously to losing their privileges – but they were never justified in the first place.

The tax breaks of TTR pensions

Transition-to-retirement (TTR) pensions, as they stand today, have three features. They allow people to withdraw money from superannuation from the age of 60 without tax penalties. They allow older people to continue to contribute to superannuation while they withdraw funds. And they bring forward the age at which earnings on accumulated superannuation balances cease to be taxed (the superannuation earnings of younger people are taxed at 15%).

These provisions are a boon to older taxpayers. One benefit is the opportunity for “super recycling”, in which a person continues to work full-time and to consume their wage income, but pays around $5000 a year less income tax. People over 60 can put the maximum amount into superannuation from their pre-tax income, and then withdraw the money immediately. They pay much less income tax because their contributions to super are only taxed at 15%, whereas ordinary earnings are taxed at their marginal tax rate.

The precise benefit of super recycling varies depending on income, as our recent Super Tax Targeting report shows. For workers aged between 60 and 64 who earn between $65,000 and $150,000, super recycling reduces the amount of tax paid by about $5000 a year. To put this in context, a 60-year old earning $75,000 then pays as much income tax as a 40-year old earning $57,000.

There are also big benefits for an older worker who takes a TTR pension and stops paying tax on the earnings of their superannuation well before they retire. Take someone with a superannuation balance of $500,000 – a larger balance than seven in eight Australian taxpayers of that age – and earning a 6% return. A TTR pension reduces the annual tax paid by around $4,500. If they take a TTR pension at age 56, they will save around $40,000 in tax by the time they stop working at 65. If their superannuation balance is higher, the tax benefit is proportionately larger.

Not a transition to retirement scheme at all

All the evidence suggests the TTR pensions are mainly used by high-wealth individuals to reduce their tax bills while they continue to work full-time. In a study published last year the Productivity Commission concluded that:

…the tax concessions embodied in transition to retirement pensions — designed to ease workers to part-time work prior to retirement — appear to be used almost exclusively by people working full-time and as a means to reduce tax liabilities among wealthier Australians.

The misuse of TTR pensions is reflected in the confusion about how many people will be affected by the Government’s changes. The Government estimates that some 115,000 people will be affected by the change.

Critics counter that the changes could affect more than 500,000 super accounts classified as TTR pensions. But many of these almost certainly belong to people who have in fact fully retired, but haven’t bothered to tell their super fund to change the classification of their pension. They have little incentive to get their paperwork up to date, because the TTR pension already provides all the benefits of tax-free super earnings to which retirees are entitled.

However many people are affected, these arrangements bear little resemblance to the now explicit objective for superannuation – “to provide income in retirement to substitute or supplement the Age Pension”. They don’t encourage additional saving. They do little in practice to delay retirement. Instead they are part of an age-based tax system that allows older Australians to pay less income tax than younger Australians with similar incomes.

Reducing the rorts

So the Government’s announcement in the May Budget that it would reduce the extent of these benefits should be no surprise.

The Government proposed to reduce the amount that can be contributed to super from pre-tax income from $35,000 to $25,000. As a result, a 60-year old earning a wage of $75,000 a year would only save $3,700 per year through super recycling rather than $5,800 per year.

However, there may be little change in practice because the Government also proposed yet another complexity that future politicians will also struggle to explain. People will be able to make additional pre-tax contributions if they contributed less than the limit of $25,000 in the previous five years. Although this is supposed to help women with broken work histories catch up on building their super funds, past practice shows that such provisions are primarily used by older men to minimise their tax.

The government also proposed to tax super earnings at 15% unless a person retires (and so forfeits the ability to make additional contributions to superannuation). Those withdrawing money from their superannuation, but also working and contributing to superannuation, will then pay 15% tax on the earnings of their super fund, just like everyone else still working.

Why the Government should stick to its guns

The Government has been attacked over the last week as it emerges that these changes will affect some people “only” earning $80,000 a year, who might be in the top 20% of income earners, but are not in the top 4%. Coalition backbenchers are reportedly concerned that some of their supporters will pay more tax. Financial planners are nervous that they will have less tax planning to offer.

But the outrage misses the vital question: why do such generous tax breaks exist at all? They lead to individuals with above average incomes paying less tax than younger Australians on similar incomes. They do almost nothing to contribute to the ostensible purpose of superannuation.

For more than a decade, superannuation tax concessions have been absurdly generous to older people on high incomes. They are one of the major reasons why older households pay less income tax in real terms today than they did 20 years ago, even though their workforce participation rates and real wages have jumped.

Superannuation tax breaks cost more than $25 billion in foregone revenue, or well over 10% of income tax collections, and the cost is growing fast. Lower-income earners and younger people have to pay more in other taxes – now and in the future – to pay for the tax-lite status of so many older Australians. The proposed changes are just the beginning of much needed reforms to superannuation to end intergenerational theft from the young.

Authors: Brendan Coates, Fellow, Grattan Institute; John Daley, Chief Executive Officer, Grattan Institute

Opposition Leader Bill Shorten’s line of attack during the leaders’ debate focused squarely on the Coalition’s long-term plan to cut the company tax rate from 30% to 25%.

Twice during the debate Shorten said the proposed tax cuts equated to giving A$7.4 billion over ten years to Australia’s big four banks (National Australia Bank, the Commonwealth Bank, ANZ and Westpac).

Is that right?

Checking the source

When asked for a source to support that assertion, a Labor spokeswoman referred The Conversation to modelling conducted by think-tank The Australia Institute.

The Labor spokeswoman said:

Bill was emphasising the clear point of contrast in this election campaign, which is that Malcolm Turnbull wants to spend $50 billion giving huge companies a tax cut while Labor wants to invest in schools, Medicare and growing good jobs.

The Australia Institute modelling

In a press release, The Australia Institute said that for their economic modelling:

The value of company tax provisions was derived from 2015 full year annual reports for the big four banks. That figure summed to $11,123 million. That figure was projected forward to 2026-27 to give the no-change scenario.

To arrive at the figure of $7.4 billion, The Australia Institute modelling assumed bank profit would increase in line with nominal Gross Domestic Product. Under this assumption, the amount of tax payable would also increase in line with nominal GDP. This would give nominal increases of:

2.5% in 2015-16;

4.25% in 2016-17; and

5% in 2017-18 and subsequent years.

As the think tank noted in its press release, the company tax cuts would not affect the big banks until 2024-25. That’s when the 30% company tax rate will fall to 27% for all companies with further reductions of 1% per year, hitting 25% in 2026-27.

The Australia Institute calculated the following results:

On these calculations, the “$7.4 billion over the next ten years” claim is not a fact. But it’s also not an unreasonable guesstimate – although it is, of course, really over the three years from 2024-25 through 2026-27. There is no advantage to the big banks over the first seven of the next ten years.

According to the Australian Taxation Office, the four big banks paid a total of $9.5 billion in company tax in the 2013-14 financial year.

The government has proposed increasing the turnover threshold below which the rate of company tax payable is 27.5%, from $10 million in 2016-17 to $1 billion in 2022-23.

The government’s proposed policy says that the company tax rate for all companies (including the four big banks) with turnover exceeding $1 billion will fall from 30% to 27% in 2024-25, and then by a further one percentage point in 2025-26 and another percentage point (to 25%) in 2026-27.

So, on that basis, The Australia Institute’s maths checks out.

A grain of salt

As with all economic modelling, this modelling and any claims based on it should be taken with a large grain of salt.

Any assumption about the banks’ profit growth over the next ten years is entirely arbitrary, and I have no idea whether it is at all justified. Only time will tell.

If the banks’ profits grew by only 2% per annum over this period, then the benefit to them from the cut in the company tax rate proposed by the Coalition would be “only” $4.8 billion; if they grew by 10% per annum the benefit to them would be $12 billion (over the three years from 2024-25 to 2026-27).

Verdict

Shorten’s statement relies on modelling assumptions made by The Australia Institute think-tank about bank profit growth. It is not a statement of fact but rather a guesstimate. It is not an unreasonable guesstimate, but depends entirely on whether the think tank’s assumptions about bank profit growth come true or not. – Saul Eslake

Review

This article correctly reflects the analysis of The Australia Institute upon which the claim of a “windfall” for the large banks has been based. As the author notes, the baseline figure is a guesstimate based on not unreasonable assumptions about the growth of the economy and the impact of the proposed business tax cuts upon bank profits, albeit seven years out. – Pat McConnell

Author: Saul Eslake, Vice-Chancellor’s Fellow, University of Tasmania; Reviewer, Pat McConnell, Honorary Fellow, Macquarie University Applied Finance Centre, Macquarie University

A long-term plan to cut the company tax rate from 30% to 25% is the centrepiece of the Coalition’s economic plan for jobs and growth. The Coalition maintains the change will boost GDP by more than 1% in the long-term, at a budgetary cost of $48.2 billion over the next 10 years.

But the very Treasury research papers relied on by the Coalition tell a more modest story than the headlines. Using these papers, we show that the net benefit to Australians in the real world will be only about half of the headline benefit, and it will be a long time before we are any better off at all.

The short story

The Government has made two claims about the economic impacts of its plan to cut the company tax rate.

On Budget night Treasurer Scott Morrison said that the tax cuts would:

“… mean higher living standards for Australians and an expected permanent increase in the size of the economy of just over one percent in the long term.”

Later last week, Prime Minister Malcolm Turnbull said:

“The Treasury estimated last year…that for every dollar of company tax cut, there was four dollars of additional value created in the overall economy.”

Sound in theory, but there’s a back story

In theory, cutting the company tax rate boosts the economy in the long term. All taxes distort choices, and thereby drag on economic activity. Taxes on capital often have especially large economic costs because they discourage investment, which is mobile across borders. By some estimates, roughly half of the economic costs of Australian company tax ultimately fall on workers, as lower company profitability leads to lower investment, and therefore lower wages and higher unemployment.

But while the theoretical argument for company tax cuts is straightforward, the real story is more complicated.

The twist: a tax cut for foreign investors

The twist in the tale comes from Australia’s system of dividend imputation, or franking credits. The effect of this system is to make the company tax rate for Australian resident shareholders effectively close to zero. In nearly every other country, company profits are taxed twice: companies pay tax, and then individuals also pay income tax on the dividends, albeit often at a discount to full rates of personal income tax.

But in Australia, the shares of Australian residents in company profits are effectively only taxed once. Investors get franking credits for whatever tax a company has paid, and these credits reduce their personal income tax. Consequently, for Australian investors, the company tax rate doesn’t matter much: they effectively pay tax on corporate profits at their personal rate of income tax.

As a result, although Australia has a relatively high headline corporate tax rate compared to our peers, in practice the comparable tax rate is lower – at least for local investors. As a result, many of the international studies about the impact of cutting corporate tax rates are not readily applicable to Australia.

Local shareholders do get one small benefit from cutting corporate tax rates. If companies pay less tax, then they have more to reinvest, so long as the profits are not paid out to shareholders. Yet in practice, most profits are paid out. Therefore a company tax cut will generate little change in domestic investment.

By contrast, foreign investors do not benefit from franking credits. They pay tax on corporate profits twice: first at the company tax rate, and then as income tax on the dividends. This means that a cut to the company tax rate provides big benefits to them.

This week The Australia Institute pointed out that foreign investors from the United States and other countries that have tax treaties with Australia may not benefit from the company tax cut, because their home governments will collect the gains from any cut to Australia company tax as additional company tax. Yet this would only occur when foreign firms repatriate profits earned in Australia to the home country.

The big reductions in net tax revenue – and therefore the large benefits to companies – are expected when the corporate tax rate is cut from 30% to 25% between 2022 and 2027 for larger companies, including the bulk of businesses that are foreign-owned.

The headline from the Treasury modelling for the 2016-17 Budget is that this cut will ultimately increase GDP by up to 1.2% meaning larger foreign companies are attracted to invest more in Australia. The finding is based on work contained in a Treasury research paper that modelled the long-term impact of a company tax cut.

Activity is not income

However, it is a mistake to assume that all the increase in economic activity will make Australians better off. We often use Gross Domestic Product – the sum of all economic activity – as a short-hand measure for prosperity. But when the benefits disproportionately flow to non-residents, GDP can be misleading. It’s much better to look at Gross National Income (GNI), which measures the increase in the resources available to resident Australians.

Treasury expects that cutting corporate tax rates to 25% will only increase the incomes of Australians – GNI – by 0.8%. In other words, about a third of the increase in GDP flows out of the country to foreigners as they pay less tax in Australia. And because most of the additional economic activity is financed by foreigners, the profits on much of the additional activity will also tend to flow out of Australia.

You don’t get something for nothing

Yet even this increase in GNI of 0.8% is not the best estimate of the improvement in living standards Australians can expect from the Government’s company tax plan. If company taxes are lower, other taxes have to be higher, all other things being equal. In the modelling discussed so far, Treasury first assumes that these revenues can be collected by a fantasy tax that imposes no costs on the economy.

But that’s not what happens in the real world. So the Treasury research paper also models the scenario in which personal income taxes rise to offset the reduced company tax revenue. On this more realistic assumption, Treasury estimates that GNI will increase by just 0.6% in the long term, or roughly $10 billion a year in today’s dollars.

Other wrinkles in the story

Even this more modest Treasury figure may well over-estimate the long-term boost to GNI. In the real world, progressive income taxes impose higher costs than the hike to a hypothetical flat-rate personal income tax that Treasury modelled. Companies may also not increase investment as much as Treasury expects, and those firms that are part of oligopolies in Australia may not increase wages by as much as Treasury assumes.

While these are reasons to expect that the Treasury modelling overestimates the economic benefits of a company tax cut, they are offset by some more conservative assumptions. Treasury believes that tax cuts modestly change how much firms shift profits overseas; it may overstate how much tax cuts flow into additional profits rather than higher wages in those industries that it does recognise as oligopolies; and it may discount the benefits of investors making less distorted choices between debt and equity funding.

The verdict on the first claim

The bottom line is that, on Treasury’s own modelling, a corporate tax cut will increase Australian incomes in the long term by up to 0.6%. The Treasury research paper doesn’t commit itself to a timeframe, but it cites other work that expects the economic benefits of company tax cuts to take 20 years to bear fruit, with half the benefit in 10 years. Given that the important (and expensive) part of the corporate tax cuts only starts to take effect from 2022, Australia will be waiting 25 years for a 0.6% increase in incomes.

This economic benefit needs to be seen in context. If Australian per capita GDP and GNI increase at 1.5% a year (as the budget papers routinely assume), then over 25 years, incomes will rise by 45.1%. Corporate tax cuts mean that instead, incomes will rise by 45.7% – or perhaps a bit less. It may still be worth doing, but it’s not a plot twist that dramatically changes Australia’s story.

Others claim that in the past, company tax cuts have had no measurable effect on the economy. This is disputed – there may well be a link between corporate tax cuts and economic growth. But it’s inevitably hard to see in practice because on Treasury’s own modelling the economic effect of company tax cuts is small relative to other changes.

Not four-to-one, more like dollar for dollar

This brings us to the Government’s second claim. Late last week, Mr. Turnbull said that each dollar in company tax revenue cut would deliver an extra four dollars in GDP.

His claim appears to be drawn from an earlier 2015 Treasury research paper that modelled the economic impact of major Australian taxes, including company tax. The more recent Treasury working paper, released in Budget week, implies a slightly larger $4.30 increase to GDP from each $1 in revenue cut.

But again this misses a big part of the story.

First, this claim is about GDP, and therefore includes the disproportionate increase in the income of foreigners. Our analysis of the Treasury modelling shows that the increase to Australian incomes, or GNI, is only $2.80 per dollar of revenue lost from a corporate tax cut.

Second, when corporate tax is replaced by a still hypothetical but marginally more realistic flat rate income tax – rather than a complete fantasy tax that has no impact on the economy – the increase to Australian incomes is less again: only $1.80 per dollar of revenue lost.

Third, the Prime Minister has framed the boost to the economy in terms of the long-term increase to GDP per dollar of company tax cut. Treasury calculates the revenue “dollar” lost after considering the additional tax revenue that the government hopes to collect from all taxes in twenty years time as incomes rise because of greater investment.

Many people would interpret the Prime Minister’s statement to compare the ultimate benefit per dollar of tax revenue given up in the shorter term. On this basis, the increase to Australian incomes in the long term is only $1.20 for every dollar given up in the short term as a result of corporate tax cuts.

This story ends the same way. Corporate tax cuts may be worth doing, but the outcome is unlikely to set pulses racing.

The journey matters

So far, as the Treasury research paper does, we’ve focused on the long-term economic boost from a company tax cut once the economy has fully adjusted. But the journey to get there also matters.

For a decade, a cut to corporate taxes will reduce national income. Foreigners will pay less tax on the profits from their existing investments in Australia, reducing Australian incomes. Foreigners own about 20% of all capital in the economy, so it’s a big windfall gain for them. We estimate that when a 5 percentage point tax cut for big business is first implemented, national incomes will be reduced by about 0.5%, as a result of the immediate loss in company tax revenues formerly paid by foreign investors.

The benefits to Australians from a corporate tax cut only accumulate slowly as foreigners make additional investments. Treasury cites a paper that estimates that the benefits of corporate tax cuts take 20 years to flow through. Assuming that these benefits increase at a constant rate, Australian income will only be larger than otherwise after about 10 years.

Of course, the upfront costs of a company tax cut over the first decade must be offset against the long-term gains. On our estimates, the loss of income incurred over the first decade will only be offset by higher incomes after about 19 years. If Australians want the modest economic benefits of a corporate tax cut, they will be waiting a long time.

The moral of the story

Company tax cuts are not a knight in shining armour to save the Australian economy. On the basis of the modelling that the government uses to support its case, corporate tax cuts can make a modest contribution, and then over the very long term. That story won’t sell as many copies. Truth, on this occasion, is duller than fiction.

Authors: John Daley, Chief Executive Officer, Grattan Institute; Brendan Coates, Fellow, Grattan Institute

A memo on the subject of housing taxation from the Reserve Bank of Australia (RBA) is stirring up debate on proposed changes to negative gearing and capital gains tax in the election campaign. The memo, dated December 9 2014, does counter the government’s claim that changes to negative gearing will have an adverse effect on housing prices, although this was never its intended purpose.

The memo was in response to the report from the Financial System Inquiry two weeks earlier. The inquiry noted that reducing capital gains tax concessions would “lead to a more efficient allocation of funding in the economy,” that “the tax treatment of investor housing…tends to encourage leveraged and speculative investment,” and that “housing is a potential source of systemic risk for the financial system and the economy”.

The RBA is usually reluctant to comment on areas of government policy outside its remit and hasn’t expressed any views on whether changes are needed to the long-standing tax treatment of housing investment. However, in response to a Productivity Commission inquiry 12 years ago, the RBA pointed out that:

“…taxation arrangements in Australia are more favourable to investors in residential property than are the arrangements in other countries.”

It also went on to note that a higher share of Australian taxpayers are attracted to property investment to lighten their tax burden and reducing investor demand would allow for more demand from first home buyers, without adding to the overall pressure on demand and prices. The RBA submission suggested this could also lead to a more stable housing market.

At that time, housing investors accounted for just over 45% of all lending by Australian financial institutions. In 1999 this was less than 32%, when the Howard government amended the tax treatment of capital gains in a way that made it more generous to investors (in property and other assets).

After falling back to around 36% in the aftermath of the global financial crisis, the share of property loans taken out by investors rebounded to more than 50% in the first half of 2015. The Australian Prudential Regulatory Authority (APRA) has since required banks to tighten their lending standards for property investment loans, now the share of new housing loans going to investors has fallen back to about 45%.

The key point to note here is that the changes enforced by APRA to banks’ lending criteria have also had the effect of dampening investor demand, as Labor’s current policy also intends, without any obvious adverse effects on property prices.

The government’s strict enforcement of foreign investment regulations, designed to prevent foreigners from purchasing established properties (other than in limited circumstances), and the cutting of grants to first-time buyers of established properties while boosting grants to first-time buyers of new dwellings at a state level, have both failed to dampen investor demand for property.

In other words, governments are trying with these policies to reduce demand for the purchase of established dwellings (90% of borrowing by Australian property investors is for the purchase of established dwellings) while encouraging the demand, and therefore building of, new properties. This is exactly what the Opposition’s proposed changes to negative gearing and the capital gains tax discount seek to do.

Labor is trying to make it less attractive for investors to buy an established property after 1 July 2017. As a result, the prices of established dwellings should go up at a slower rate than it would otherwise – and from the standpoint of would-be home-buyers, this is a good thing.

However, the Opposition proposes to “grandfather” existing negatively-geared investors from these changes. This means anyone who has a negatively geared property investment as of 30 June 2017 will still be able to offset the excess of their interest costs over their net rental income against their other taxable income. So there is no reason to expect that investors will seek to sell their investments en masse and that prices of existing properties will fall any more than they have done as a result of the other government measures.

And this is precisely what the memo from the RBA notes:

“only if changes were not grandfathered” would there be a risk of “large scale sale of negatively geared properties.”

The RBA note also raises the possibility that changes to negative gearing could prompt a “potential increase in rents” – a point which the Coalition has been as quick to seize upon. Presumably this concern reflects an assumption that if changes were to be made to existing negative gearing arrangements, those changes would apply to new properties as well as established ones (since the Financial System Inquiry whose recommendations prompted this staff memo didn’t make any distinction between the two).

The Opposition’s policy is to keep existing negative gearing arrangements for investors in new dwellings. There is a risk that it could end up inflating builders’ profit margins, rather than boosting the supply of new housing.

However, to the extent that it does the latter, there is less reason to expect rents to rise. This is because under the Opposition’s policy more would-be home-buyers could fulfil their aspirations. It would reduce the competition they face from investors who negatively gear and this would decrease the demand for rental housing.

The Reserve Bank hasn’t explicitly supported Labor’s negative gearing policy. But it does appear to have rebutted one of the government’s principal arguments against it.

Author: Saul Eslake, Vice-Chancellor’s Fellow, University of Tasmania

In his budget reply speech this week, Opposition leader Bill Shorten said Labor had “very grave concerns about retrospective changes” to superannuation being proposed by the government. The superannuation industry has been even more vociferous. But labelling the changes as “retrospective” in this case is a furphy.

For a decade, some older savers have benefited from superannuation tax breaks that did little to help younger generations. Understandably, they want to keep receiving these benefits. But they are wrong to claim the government’s proposed superannuation changes are retrospective simply because they adversely affect the future returns on their savings.

“Retrospectivity”, a legal concept, applies if government changes the legal consequences of things that happened in the past.

The Commonwealth government proposes two changes to superannuation rules in the 2016 budget. First, funds in excess of A$1.6 million in pension phase (when the fund holder pays no tax on earnings) will have to be moved into a separate account that pays 15% tax on earnings. In effect, retirees will pay no tax on the earnings of assets up to $1.6 million, and 15% tax on earnings after that.

Second, the budget proposes a new lifetime limit of A$500,000 on post-tax contributions to super. This includes any contributions made between 2007 (when reliable records begin) and budget night. If someone has already contributed more than this, there will be no penalty, but they will not be able to contribute any more from their post tax income.

The rationale for both changes is that they align superannuation more closely with its purpose of supplementing or replacing the Age Pension. A person with $1.6 million in a superannuation account, or a person contributing more than half a million from post tax income (in addition to pre-tax contributions), is going to be well over the asset limit for a part Age Pension ($805,000 for a couple home-owner).

The objection is that these changes retrospectively affect superannuation investments made in the past. But lots of changes affect investments made in the past, and no-one suggests they are retrospective. If I bought shares in a company yesterday, I expect that the future earnings on these assets will be subject to my marginal income tax rate. But if my income tax rates change, I would not expect that the old tax rate to be grandfathered to apply to all my future earnings.

This is the appropriate analogy for proposed changes to the earnings of superannuation accounts in excess of $1.6 million. The mere fact that no tax was paid on earnings in the past does not imply that earnings in the future are entitled to be tax free.

The retrospectivity argument is even weaker for the new cap on post-tax contributions. The only constraint is on additional contributions in the future. True, this is based on the amount that has already been contributed, but no adverse consequence flows from historic contributions; the change merely limits future contributions. To draw another analogy, it is not retrospective to change the asset test for the Age Pension merely because assets accumulated in the past are now taken into account for assessing future Age Pension payments.

Alternatively, we can analyse this problem using ethical concepts that are reflected in the legal doctrine of “estoppel”. This applies if a person reasonably relies on a promise of another party, and because of that reliance is injured or damaged.

The proposed changes do not fall foul of this doctrine.

Those who were induced to put more money into super would be a long way in front even if they had paid 15% tax on all earnings in retirement. Most contributions to superannuation are made from pre-tax earnings, and only taxed at 15%. Even those on very high incomes who pay tax of 30% on their contributions are still getting a discount of more than 15 per cent compared to post-tax savings. Once in the super fund, the earnings on those contributions are only taxed at 15% rather than at marginal income tax rates. The only people who could possibly have lost money contributing more to superannuation are those with taxable incomes less than A$19,000 a year – below the income tax-free threshold. If any of them have accumulated more than $1.6 million in superannuation, the ATO should probably be asking them some questions.

Superannuation tax concessions have been absurdly generous to older people on high incomes for over a decade. They have not served the purposes of the system. They are one of the major reasons why households over the age of 65 (unlike households aged between 25 and 64) are paying less income tax in real terms today than they did 20 years ago, even though their workforce participation rates and real wages have jumped. Misguided claims about retrospectivity should not be used as cover so that this older generation continues to gain unjustifiable benefits that will now be denied to younger generations.

Author: John Daley , Chief Executive Officer, Grattan Institute

Australia’s federal government clearly sees its program of annual reductions in the company tax rate as the core element in its plan for “jobs and growth”.

There is now a large – though by no means uncontested – body of evidence to support the contention that reductions in company tax rates can support faster rates of GDP growth and higher wages. It does this by stimulating higher levels of investment and hence higher levels of labour productivity.

But there is very little evidence supporting the favouring of small businesses over large in this regard. The significant preference which both this budget and its predecessor have extended to small businesses appears to owe much more to a desire to bow before small business than to any unambiguous economic rationale.

Small businesses have accounted for only 18% of the increase in employment over the most recent five years for which data are available, while firms with more than 200 employees – which the ABS defines as “large” – have accounted for 52% of the increase in total employment over the past five years, despite accounting for less than 32% of total employment. And large businesses are more likely to engage in “innovative activities” than small ones, especially ones with four or fewer employees.

In other words, if the government wanted to cut company taxes in a way that was most likely to result in increased job creation or higher levels of innovation (assuming that cutting company taxes would have that effect), it should have cut company taxes for large companies ahead of small ones. But that would have been exceedingly difficult, politically, in the current climate.

Mixed messages

The other key element of the government’s ten year enterprise tax plan is the increase in the tax threshold for the second-top marginal rate from $80,000 to $87,000. The government says this will prevent “average full time wage earners … from moving into the second highest tax bracket”. But when you consider the difference between gross and taxable incomes, and that most people use deductions to reduce their taxable income, $87,000 is far from average.

The budget seems to be saying to people with taxable incomes of less than $80,000 – if you want to pay less tax, get yourself a negatively-geared property investment.

The budget is also arguably saying the same thing to people with taxable incomes of more than $250,000, people who have already contributed $500,000 to superannuation over the course of their lifetimes, or people who already have at least $1.6mn in their superannuation accounts. The message is if you put any more into superannuation, we are going to tax you more, but if you put it into a negatively-geared property investment, we won’t touch you, because (in the words of the Treasurer’s Budget Speech), “that would increase the tax burden on Australians just trying to invest and provide a future for their families”.

I am quite comfortable with the budget’s proposed changes to superannuation arrangements. But I can’t see why people – even wealthy people – who are “just trying to invest” through superannuation should be singled out for less generous tax treatment, while people who are doing exactly the same thing through negatively geared property (or other) investments should remain unscathed.

The Treasurer reportedly toyed with the idea of limiting “excesses and abuses” of negative gearing, with caps on claims. This would have more or less exactly paralleled what the budget seeks to do with regard to superannuation.

Combined with the Reserve Bank’s latest cut in official interest rates, the budget’s decisions and non-decisions with regard to income tax cuts, superannuation and negative gearing are likely to encourage more Australians to borrow more money in order to invest in the property market. At a time when Australia has one of the developed world’s highest ratios of household debt to GDP or personal income, and amongst the developed world’s most expensive residential real estate.

Author: Saul Eslake, Vice-Chancellor’s Fellow, University of Tasmania

There are three critical tests for this year’s budget. Is it serious about repairing Australia’s ongoing structural budget deficits? Does it make much of a difference to economic growth? And is it fair?

Budget repair

Over the last year, the bottom line got worse. The long-promised return to surplus receded another year over the horizon. This is the seventh time a budget has forecast a drift back to surplus over the following four years while the outcome for the current year showed minimal improvement over the year before.

Author provided

Also consistent with the history of the last seven years, most of the damage was done by “parameter variations” – changes in the economy that meant the budget didn’t live up to previous expectations.

Author provided

The government has made much of the need to repair the budget through spending reductions rather than tax increases. Overall, however, forecasts assume that most of budget repair will be the result of increasing revenues as a share of GDP. A large component is that nominal wages are expected to rise, leading to higher income tax collections, known by budget nerds as “fiscal drag”, and commonly referred to as “bracket creep”.

Author provided

There’s plenty of room for things to keep going wrong. The largest risk is that nominal wages may be lower than forecast.

Last week the Australian Bureau of Statistics reported much lower inflation than expected. On the day of the federal budget the Reserve Bank responded by cutting interest rates, implying a real risk that unusually low inflation will persist. If it does, then income tax collections will be hit, hurting the budget bottom line, particularly in the last year or two of the budget estimates.

This presents an interesting challenge for Treasury. If an election is called towards the end of this week, then it must release PEFO – the Pre-election Economic and Fiscal Outlook – by around May 20. With inflation lurching south, PEFO may significantly revise the budget bottom line, which will inevitably raise perceptions – probably unfairly – that the government is not firmly in control of economic management.

The other big risk is that export prices fall short of forecasts. The budget assumes an iron ore price of US$55 per tonne. This is close to recent prices, but they were US$40 a tonne just six months ago. If the price drops back US$10 to US$45 per tonne, budget balances are expected to be A$4 billion a year worse off.

Specific measures don’t do much collectively to improve the budget bottom line. As with each of the last seven years, there are substantial gross tax increases and spending reductions, but other decisions largely offset these. Overall, specific measures drag on the budget outcome by $5 billion for the coming year, but improve the last estimated year (2019-20) by $6 billion.

Jobs and growth

The key selling point for the budget is “jobs and growth”. However, there are questions about whether the budget initiatives will matter much to the economy within the next four years.

The largest single initiative is a cut to the corporate tax rate, particularly for small-to-medium businesses. The tax rate will be cut from 28.5% to 27.5%, and by 2019-20 this will apply to businesses with up to $10 million in turnover, up from the current limit of $2 million.

This will doubtless be popular with hundreds of thousands of small businesses. However, given Australia’s dividend imputation scheme, the tax change makes no difference to the amount of tax levied on profits paid out to Australian business owners. A lower tax rate only matters to the budget and the economy when businesses re-invest retained earnings.

However, the overall effect will be small. The tax changes are supposed to reduce tax collected in 2019-20 by A$2 billion – by definition, money retained in businesses and re-invested. This compares with total corporate investment in capital of about A$120 billion a year, and much more in paying for additional staff. The tax change is small beer in comparison.

There may be a larger tankard of beer in reducing tax rates for foreign corporates. But they will receive no benefit until after 2020-21 – well after the next two elections. And recent work has cast doubt on how much of the economic benefit will ultimately benefit Australians.

It is stretching things to believe that other measures will turbo-charge the economy. The budget contains relatively little new infrastructure spending.

Instead there are a lot of plans to do more planning. The most promising economic feature may be a new Youth Jobs PaTH package. This replaces work for the dole with a training, internship and subsidised employment pathway that is at least a little closer to what the literature recognises as best practice.

Fairness

Despite its jobs and growth packaging, the boldest moves in the budget were about fairness. Wide-ranging reforms to superannuation are a big move in the right direction. The current system is poorly targeted, with most of the tax concessions going to the top 20% of taxpayers who need the least help in saving for retirement.

Under the reforms, the top 4% will pay about A$2.6 billion more tax in 2019-20, offset by an additional A$1.8 billion tax concessions for the bottom 28%. These are material changes very different from the tinkering at the edges that has characterised superannuation reform over the last decade.

More controversially, the budget raises the 37% income tax threshold from $80,000 to $87,000. This gives the top 20% of income earners an extra $315 a year.

The fairness of concentrating tax relief on this group depends on the date of comparison. Genuinely middle-income earners (on $45,000 a year) have lost a greater percentage of their income in tax because of bracket creep since the Coalition took office. However, the change in percentage of income paid in tax is more or less the same for all income groups since 2011-12, because lower-income groups received more benefit from carbon tax compensation.

Conclusion

Budget 2016 was much like many of its predecessors over the last seven years. Budget repair was put off till later, and the net impact of budget decisions was small.

Although much was made of individual initiatives, these are unlikely to make much difference to economic growth in the next four years.

Although fairness, like beauty, is in the eye of the beholder, this budget will be easier to defend than some others in recent times.

Authors: John Daley, Chief Executive Officer, Grattan Institute; Danielle Wood, Fellow, Australian Perspectives, Grattan Institute