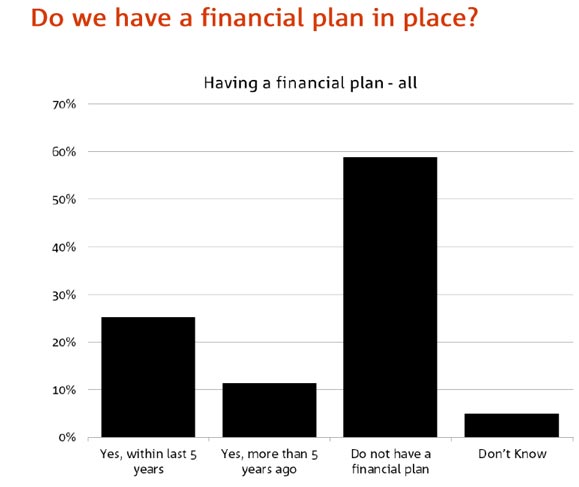

One in two Australians don’t believe they’re doing enough to reach their wealth goals according to new research from MLC, but a boost in confidence and a financial plan may be the key to helping Aussies get on track. However only 1 in 4 had a financial plan within the last 5 years.

The latest MLC Wealth Sentiment Survey released today for the first time identifies the reasons why Australians believe they may not have done enough to reach their goals, finding that self-doubt ranks second to not earning enough money (50% compared with 32%). These two factors were nominated by respondents as more significant than being scared of risk or even spending more than they earn.

Lara Bourguignon, General Manager, Corporate Super, NAB, says the research captures the strong link between confidence and achieving financial goals.

“We often think that getting where we want to go with our money hinges on how much we earn, but self-doubt appears to be a major factor. If we doubt our abilities with our money, it makes sense that we would struggle to achieve our goals.”

Closely tied to the lagging confidence of Australians is the considerable number who do not have a plan to save and invest. Only one in four respondents reported having a financial plan, which MLC says may be a key reason many lack confidence in dealing with money and investments.

“The research highlights an important connection between planning and confidence in reaching financial goals. With so few people having a financial plan, we perhaps shouldn’t be surprised that Australians doubt themselves and don’t believe they have done enough to reach their wealth goals. Having a financial plan is crucial to feeling empowered and getting where you want to go with your money,” said Ms Bourguignon.

For the first time, the survey has also asked Australians to define “wealth”. On average, 33 per cent reported their definition as income, 29 per cent lifestyle wealth, and 24 per cent net worth. The most important aspects of lifestyle wealth were being debt free, having enough for emergencies, and being able to fund our desired lifestyles.

The MLC Wealth Sentiment Survey also identified that while a majority of Australians report a significant shortfall between their anticipated financial needs at retirement and their expected savings and investments, most do not factor their primary residence in calculating their wealth. If Australians included the family home in their wealth, most would have enough once they left the workforce. Despite this, only 11 per cent reported that they planned to sell the family home to fund their retirement.

MLC Quarter 3 Wealth Sentiment Survey – key findings:

- One in two Australians don’t believe they have done enough to reach their wealth goals

- The top reasons nominated are insufficient income and self-doubt

- Australians on average estimate they will need about $818,000 in savings and investments to retire, but expect to retire with only $557,000 (excludes home equity), an average shortfall of $261,000

- Women face a bigger retirement shortfall than men: $297,000 compared with $226,000

- If Australians included the equity in their homes, they would have an additional $442,000 in wealth available for retirement

- Only 11 per cent of respondents say they will sell their homes to fund retirement

- Four in ten respondents said they can achieve their desired lifestyle on less than $100,000 per year

The MLC Quarterly Australian Wealth Sentiment Survey interviews more than 2,000 people each quarter. It aims to assess the investment environment by asking questions related to current financial situation, investment intentions, level of concern related to superannuation and other investments, change in life insurance, and distance to retirement and investment strategy.