The CBA released their 3Q update today. We see the same signs of margin pressure and likely slower growth ahead, as in the recent results from ANZ and Westpac. We think the sector will be under more pressure going forwards. Extra capital requirements will also bear down in coming months. Provisions, at the bottom of the cycle were up.

Unaudited cash earnings for the three months ended 31 March 2015 (“the quarter”) were approximately $2.2 billion. Statutory net profit on an unaudited basis for the same period was also approximately $2.2 billion, with non-cash items treated on a consistent basis to prior periods. This was below market expectations.

Revenue growth was similar to 1H15. Group Net Interest Margin continued to be impacted by competitive pressures by around 3 basis points. Trading income remained strong; Expense growth was higher in the quarter, impacted by growing regulatory, compliance and remediation costs, including those associated with a number of legislative reforms (FATCA, FoFA, Stronger Super, LAGIC), provisioning for the advice review program and ongoing regulatory engagement.

Across key markets, home lending volume growth continued to track slightly below system, consistent with the Group’s underweight position in the higher growth investment and broker segments; core business lending growth remained at mid-single digit levels (pa), household deposits growth was particularly strong in the quarter, with balances growing at an annual rate of over 10 per cent; in Wealth Management, Funds under Administration and Assets under Management grew 7 and 8 per cent respectively in the quarter, reflecting strong investment performance, net inflows and FX gains; insurance inforce premiums increased 3 per cent on the prior quarter; ASB business and rural lending growth remained above system and home loan growth was stronger Credit quality remained sound.

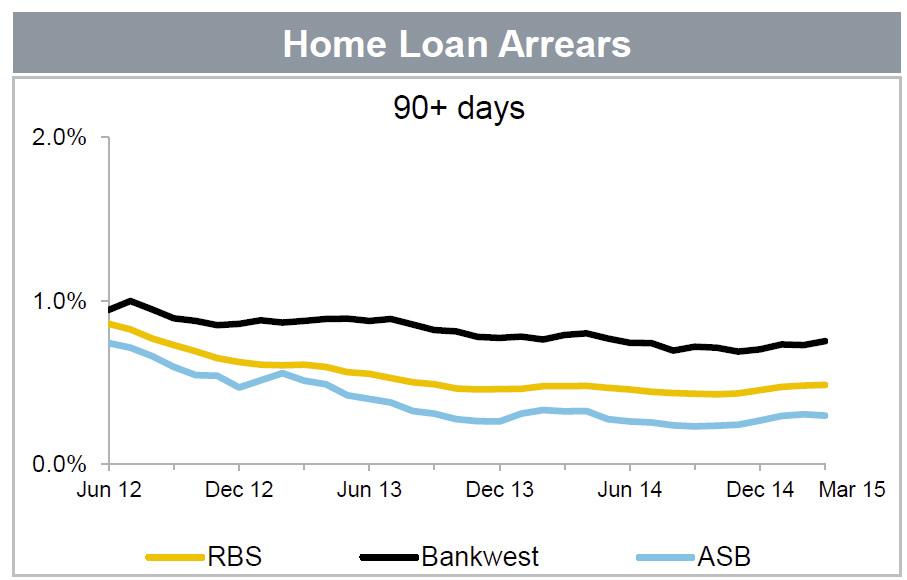

In the retail portfolios, home loan and credit card arrears were broadly flat, whilst seasonal factors contributed to higher personal loan arrears. Troublesome and impaired assets were lower at $6.4 billion. Total loan impairment expense was $256 million in the quarter, up from $204m a year earlier, with strong provisioning levels maintained and the economic overlay unchanged. Home loan arrears were higher in Bankwest than the Australian and New Zealand businesses.

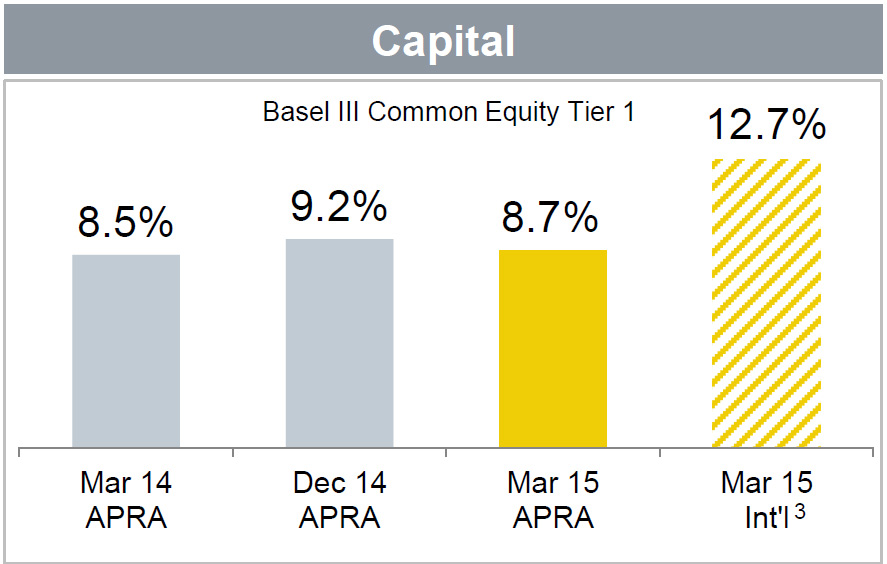

The Group’s Basel III Common Equity Tier 1 (CET1) APRA ratio was 8.7 per cent as at 31 March 2015, an increase of 20 basis points on December 2014 after excluding the impact of the 2015 interim dividend (which included the issuance of shares in respect of the Dividend Reinvestment Plan). The Group’s Basel III Internationally Comparable CET1 ratio as at 31 March 2015 was 12.7 per cent. They will need to raise more capital on these ratios than we expected.

The Group’s Basel III Common Equity Tier 1 (CET1) APRA ratio was 8.7 per cent as at 31 March 2015, an increase of 20 basis points on December 2014 after excluding the impact of the 2015 interim dividend (which included the issuance of shares in respect of the Dividend Reinvestment Plan). The Group’s Basel III Internationally Comparable CET1 ratio as at 31 March 2015 was 12.7 per cent. They will need to raise more capital on these ratios than we expected.

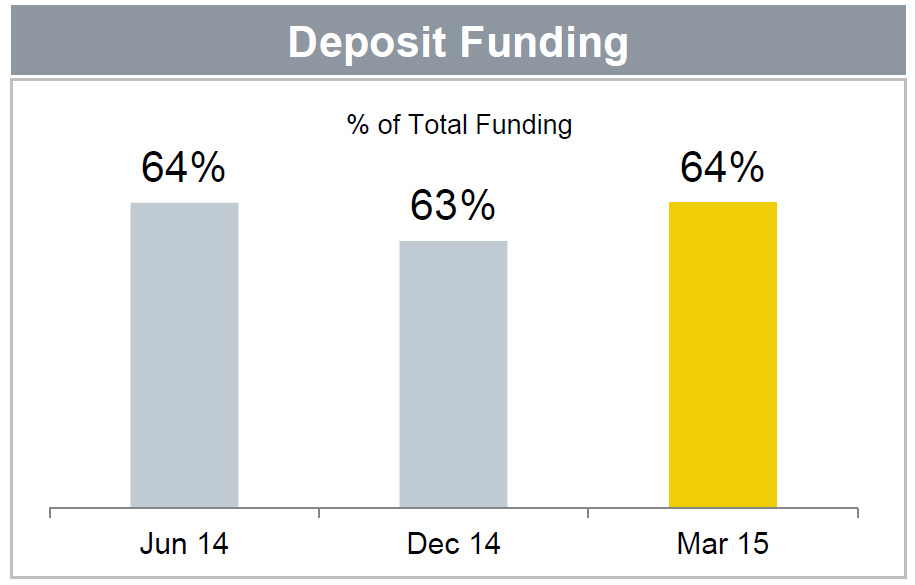

Funding and liquidity positions remained strong, with customer deposit funding at 64 per cent and the average tenor of the wholesale funding portfolio at 3.9 years.

Funding and liquidity positions remained strong, with customer deposit funding at 64 per cent and the average tenor of the wholesale funding portfolio at 3.9 years.

Liquid assets totalled $144 billion with the Liquidity Coverage Ratio (LCR) standing at 122 per cent. The Group completed $8.5 billion of new term issuance in the quarter.

Liquid assets totalled $144 billion with the Liquidity Coverage Ratio (LCR) standing at 122 per cent. The Group completed $8.5 billion of new term issuance in the quarter.