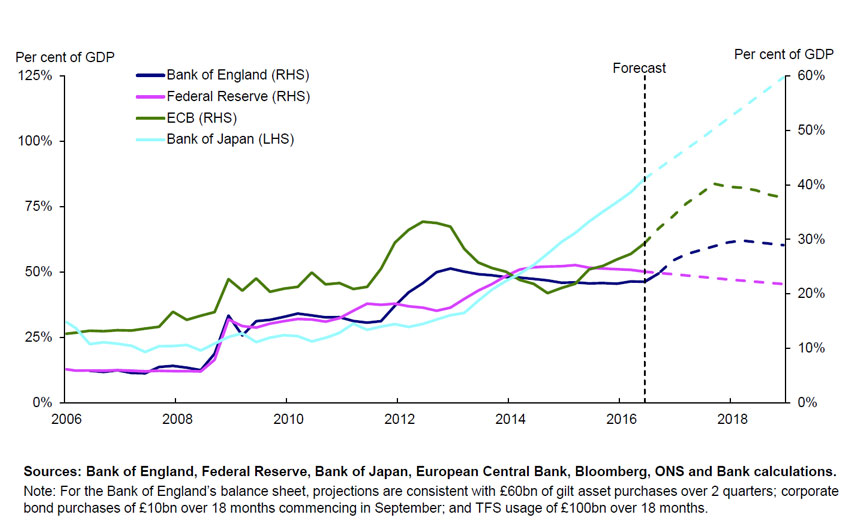

There has been astonishing growth in the balance sheets of Central Banks in recent years, as attempts have been made to deal with fallout from the GFC nearly eight years ago. Globally we estimate the total assets of central banks are now north of US$17 trillion. But it is worth thinking about the implications of this expansion, in both policy and economic terms. In some geographies money has been “created”, leading to asset bubbles when coupled with low interest. But even in markets where “QE” has not been used, Central banks are still more active, and larger. Here is some data on USA, Australia and European central banks underscoring the absolute rate of growth.

A speech given by Minouche Shafik, Deputy Governor, Markets & Banking, Bank of England explores some of the issues.

Gone is the pre-crisis ideal of minimalist central banks with small balance sheets, narrowly defined objectives and tools, and a bias toward non-intervention. Today, major central banks have greater responsibilities and a wider range of tools at our disposal. Our balance sheets are larger and for the most part continuing to increase.

I’d like to use these remarks to offer a number of reflections on these developments, using the Bank of England’s recent experience by way of example, and focussing on four themes.

My first theme is that the broadening of our responsibilities and range of tools at our disposal has facilitated a more joined up approach to how we set monetary policy and pursue financial stability.

Second, the increase in size of our balance sheet has been a necessity of the times we live in. Deep structural forces have combined to depress the level of interest rates at which the economy would be in equilibrium, obliging us to rely evermore on monetary policies that were once considered unconventional. This requires us to operate with multiple instruments in multiple markets meaning that our impact on the financial system – the central bank’s footprint – is larger.

Third, we are aware that some of our policies have spillovers and side effects, but we take steps to address them where feasible to do so within our mandate. We know that a bigger footprint means we need to be mindful of our step.

Finally, despite our bigger size, there are some things central banks cannot do. To generate sustainably strong growth over the medium term, monetary and financial stability policy must be part of a balanced package that also includes the government’s economic policies and, given strong global interconnections, international policy co-ordination.