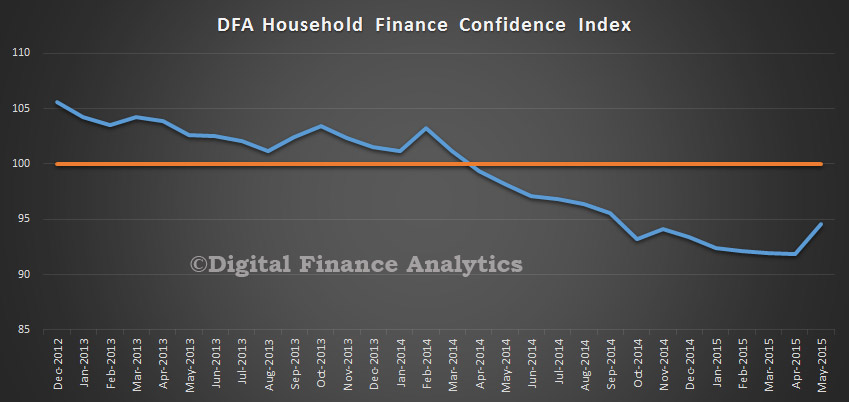

The latest edition of the DFA Household Finance Confidence Index was released today. The latest data to end May shows there was an improvement over the last month, partly in response to the budget and the RBA rate cut, but the overall score is still well below a neutral setting. The score moved from 91.87 to 94.6.

The results are derived from our household surveys, averaged across Australia. We have 26,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health.

The results are derived from our household surveys, averaged across Australia. We have 26,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health.

To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

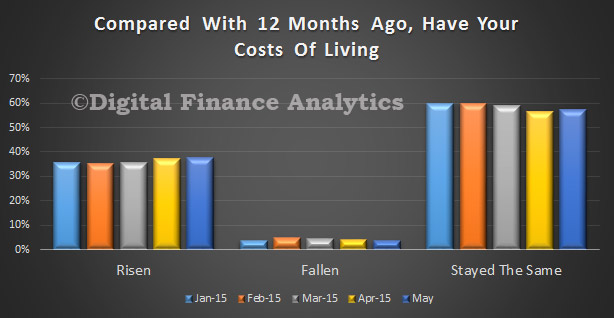

Looking at the drivers of the index, for all Australia, we see that costs of living are rising, with 37.64% of households seeing a rise in the last 12 months (up from 37.2%), and more than half seeing no improvement in costs of living. Elements which are driving this include fuel costs, rising council charges and costs of imported goods.

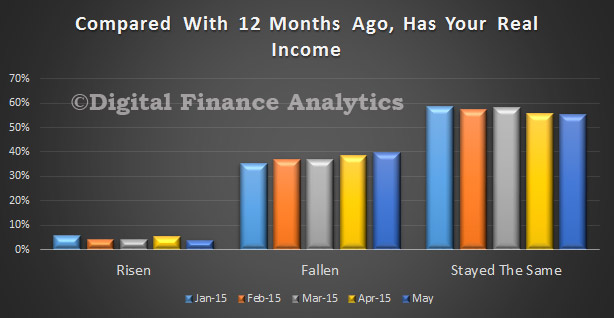

Turning to income 3.8% of households have seen a real increase in the last year, compared with 5.5% last month. 39.9% of households have experienced a fall, compared with 38.4% last month, and 55.5% of households stayed the same compared with 55.8% last month.

Turning to income 3.8% of households have seen a real increase in the last year, compared with 5.5% last month. 39.9% of households have experienced a fall, compared with 38.4% last month, and 55.5% of households stayed the same compared with 55.8% last month.

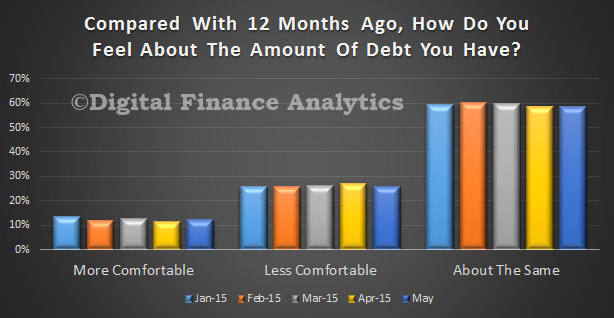

Looking at household debt, 12.3% of households are comfortable with their debt levels, up from 11.4% last month. Households who are uncomfortable with their debt levels fell to 25.8% from 27.2% last month. The change was directly linked to the RBA Cash Rate cut in May, and an expectation that rates will fall further. Those with high credit card debts were significantly more likely to be is the less comfortable category. Those households with interest only mortgages were disproportionally more comfortable than those with a p&i loan.

Looking at household debt, 12.3% of households are comfortable with their debt levels, up from 11.4% last month. Households who are uncomfortable with their debt levels fell to 25.8% from 27.2% last month. The change was directly linked to the RBA Cash Rate cut in May, and an expectation that rates will fall further. Those with high credit card debts were significantly more likely to be is the less comfortable category. Those households with interest only mortgages were disproportionally more comfortable than those with a p&i loan.

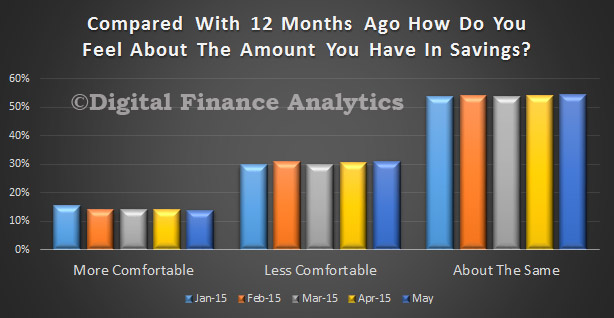

Turning to savings, those who are more comfortable fell from 13.9% to 13.7%. We saw a rise in households who were less comfortable (from 30.4% to 30.9%) and more than half saw no change. One element of note was that households are tapping to their savings to fill the gap left by slow income growth, against costs and spending. Low deposit rates are encouraging some households to spend some of their savings.

Turning to savings, those who are more comfortable fell from 13.9% to 13.7%. We saw a rise in households who were less comfortable (from 30.4% to 30.9%) and more than half saw no change. One element of note was that households are tapping to their savings to fill the gap left by slow income growth, against costs and spending. Low deposit rates are encouraging some households to spend some of their savings.

On job security, there was a slight rise in those feeling more comfortable (from 16.2% to 16.8%). Interestingly those employment in small businesses saw a significantly larger positive swing, offset by lower levels of security in larger companies. The worst deterioration were in WA and QLD.

On job security, there was a slight rise in those feeling more comfortable (from 16.2% to 16.8%). Interestingly those employment in small businesses saw a significantly larger positive swing, offset by lower levels of security in larger companies. The worst deterioration were in WA and QLD.

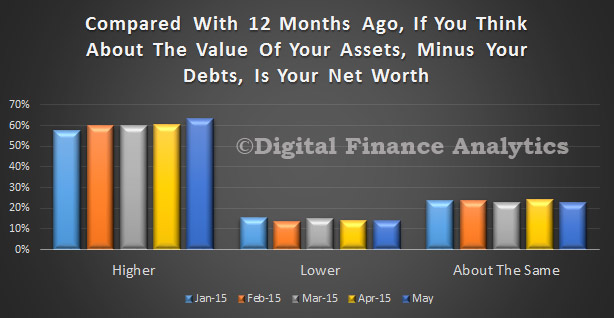

63.1% of households saw their net worth rising, up from 60.5% last month, thanks primarily to further rises in real estate (especially in Sydney and Melbourne) and shares. A slightly smaller proportion of households saw their net worth falling (down from 14.2% to 13.86%), the majority of those households who reported a fall were not property active, living in rented accommodation, and more reliant on Centrelink support than average. We also note a skew to rises in net worth in the main urban centres on the east coast, and higher than average income. Households in WA scored the highest fall this month.

63.1% of households saw their net worth rising, up from 60.5% last month, thanks primarily to further rises in real estate (especially in Sydney and Melbourne) and shares. A slightly smaller proportion of households saw their net worth falling (down from 14.2% to 13.86%), the majority of those households who reported a fall were not property active, living in rented accommodation, and more reliant on Centrelink support than average. We also note a skew to rises in net worth in the main urban centres on the east coast, and higher than average income. Households in WA scored the highest fall this month.

So overall, we see the continuing trend of lower income, higher costs, those households with property and shares enjoying offsetting net worth growth, but others not participating to the same extent. The budget may have moved the dial a bit, but the RBA rate cut had more impact.

So overall, we see the continuing trend of lower income, higher costs, those households with property and shares enjoying offsetting net worth growth, but others not participating to the same extent. The budget may have moved the dial a bit, but the RBA rate cut had more impact.

Note that this data is averaged across the states, though we note some significant differences between WA (overall confidence lower) and NSW (overall confidence higher), thanks mainly to differential movements in house prices and employment prospects. We do not published the detailed segment and state based analysis in this post. This detail is available to our paying clients!