The Financial Stability Board (FSB), in consultation with the Basel Committee on Banking Supervision (BCBS) and national authorities, today published the 2016 list of global systemically important banks (G-SIBs).

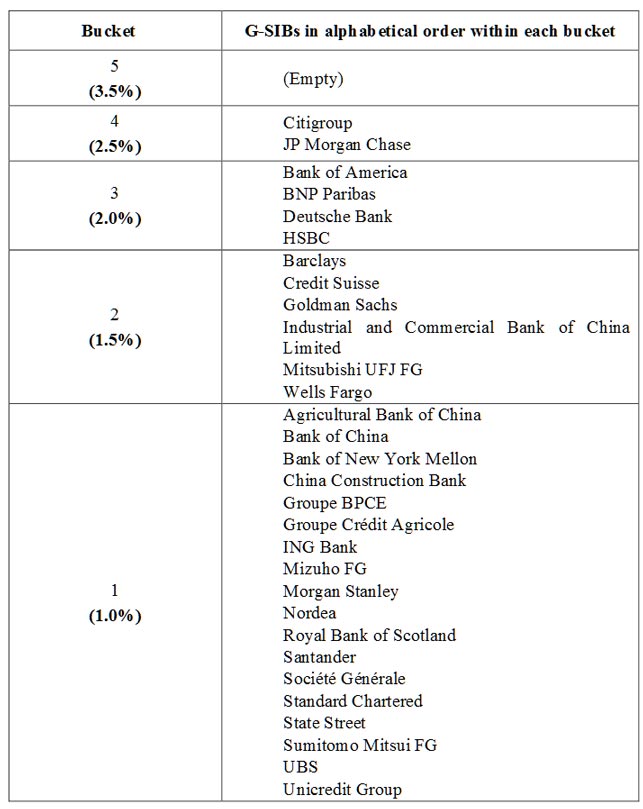

The 2016 list comprises the same 30 banks as the 2015 list. Four banks moved to a higher bucket, and three banks moved to a lower bucket. The changes in the allocation across buckets of the institutions on the list reflect the combined effects of data quality improvements, changes in underlying activity, and the use of supervisory judgement.

G-SIBs are subject to:

- Higher capital buffer requirements: Since the November 2012 update, the G-SIBs have been allocated to buckets corresponding to the higher capital buffers that they would be required to hold by national authorities in accordance with international standards. Higher capital buffer requirements began to be phased in from 1 January 2016 for G-SIBs that were identified in November 2014 (with full implementation by 1 January 2019). The capital buffer requirements for the G-SIBs identified in the annual update each November will apply to them as from January fourteen months later. The assignment of G-SIBs to the buckets in the list published today determines the higher capital buffer requirements that will apply to each G-SIB from 1 January 2018.

- Total Loss-Absorbing Capacity (TLAC) requirements: G-SIBs will be required to meet the TLAC standard, alongside the regulatory capital requirements set out in the Basel III framework. The TLAC standard will be phased-in from 1 January 2019 for G-SIBs designated in the 2015 list (provided that they will continue to be designated as G-SIBs thereafter).

- Resolvability requirements: These include group-wide resolution planning and regular resolvability assessments. The resolvability of each G-SIB is also reviewed in a high-level FSB Resolvability Assessment Process (RAP) by senior regulators within the firms’ Crisis Management Groups.

- Higher supervisory expectations: These include supervisory expectations for risk management functions, risk data aggregation capabilities, risk governance and internal controls.