APRA released the latest ADI Property Exposure data to September 2016 today. ADIs residential term loans to households were $1.46 trillion as at 30 September 2016. This is an increase of $106.5 billion (7.9 per cent) on 30 September 2015. The number of loans rose from 5,469,000 to 5,665,000, a rise of 3.6% year on year.

Owner-occupied loans were $949.0 billion (64.9 per cent), an increase of $108.6 billion (12.9 per cent) from 30 September 2015; and investor loans were $512.3 billion (35.1 per cent), a decrease of $2.0 billion (0.4 per cent) from 30 September 2015.

ADIs with greater than $1 billion of residential term loans held 98.7 per cent of all such loans as at 30 September 2016. These ADIs reported 5.7 million loans totalling $1.44 trillion. Of these: the average loan size was approximately $255,000, compared to $244,000 as at 30 September 2015; and $564.8 billion (39.2 per cent) were interest-only loans.

Looking at new approvals, ADIs with greater than $1 billion of residential term loans approved $372.1 billion of new loans in the year ending

30 September 2016. This is an increase of $5.8 billion (1.6 per cent) on the year ending 30 September 2015. Of these new loan approvals: owner-occupied loan approvals were $250.3 billion (67.3 per cent), an increase of $29.9 billion (13.6 per cent) from the year ending 30 September 2015; investment loan approvals were $121.8 billion (32.7 per cent), a decrease of $24.2 billion (16.6 per cent) from the year ending 30 September 2015:

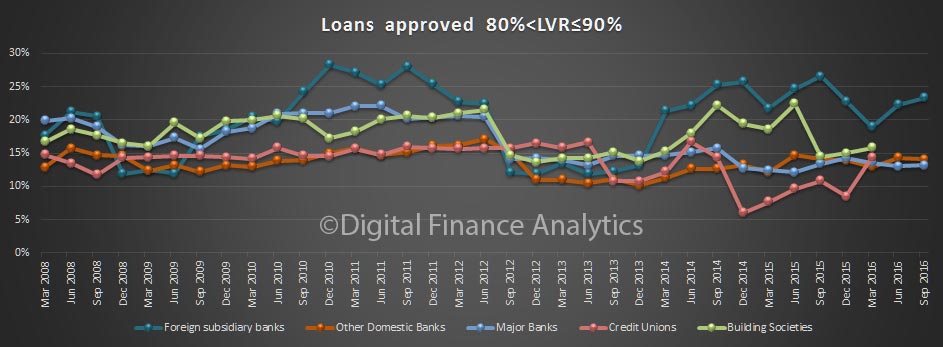

$51.8 billion (13.9 per cent) had a loan-to-valuation ratio (LVR) greater than 80 per cent and less than or equal to 90 per cent, an increase of $2.9 billion (5.9 per cent) from the year ending 30 September 2015

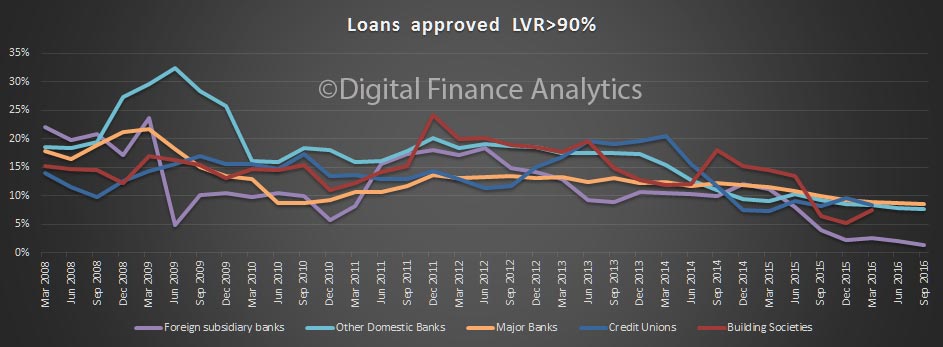

$31.5 billion (8.5 per cent) had a LVR greater than 90 per cent, a decrease of $7.7 billion (19.5 per cent) from the year ending 30 September 2015; and

$31.5 billion (8.5 per cent) had a LVR greater than 90 per cent, a decrease of $7.7 billion (19.5 per cent) from the year ending 30 September 2015; and

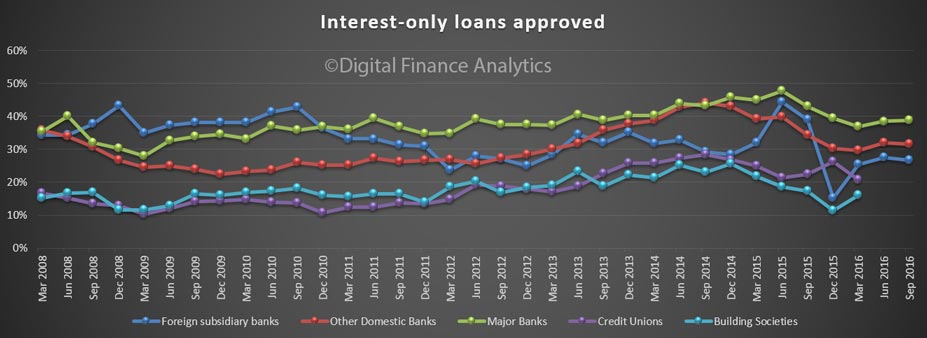

$135.2 billion (36.3 per cent) were interest-only loans, a decrease of $23.9 billion (15.0 per cent) from the year ending 30 September 2015. Major banks are writing the largest proportion of interest only loans.

$135.2 billion (36.3 per cent) were interest-only loans, a decrease of $23.9 billion (15.0 per cent) from the year ending 30 September 2015. Major banks are writing the largest proportion of interest only loans.

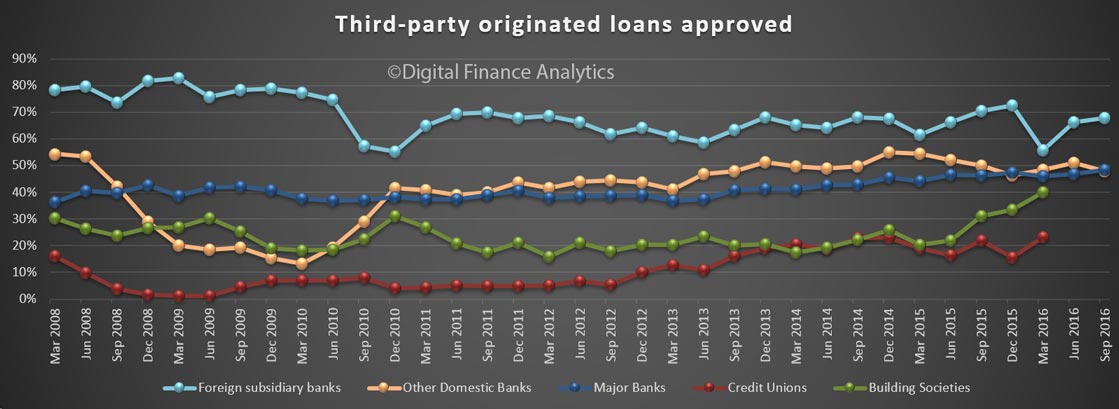

The proportion of new loans via brokers continues to grow, with foreign banks having the largest share, but domestic banks are now above 50%.

The proportion of new loans via brokers continues to grow, with foreign banks having the largest share, but domestic banks are now above 50%.

We note that the number of credit unions and building societies captured in the data has fallen to the point where their discrete data is no longer being reported.

We note that the number of credit unions and building societies captured in the data has fallen to the point where their discrete data is no longer being reported.