The latest OECD commentary on Australia makes interesting reading. In particular they argue that interest rates should be raised, and fiscal rather than monetary support should play the leading role. Tax reform should be a core element of structural policy.

“Economic growth is projected to pick up to 3% by 2018. The decline in resource-sector investment will tail off and the non-resource sector will be supported by a steady increase in household consumption and investment as wages and employment rise.

Further falls in unemployment will help reduce inequality and are not expected to generate strong inflationary pressures.

Further falls in unemployment will help reduce inequality and are not expected to generate strong inflationary pressures.

Monetary policy tightening is expected to commence towards the end of 2017 and this is appropriate given likely monetary-policy developments elsewhere, the cyclical development of the domestic economy and the need to unwind tensions from the low-interest environment, notably in the housing market, which has in many places experienced rising prices for some time. The government envisages fiscal consolidation.

In the event of disappointing growth, however, fiscal rather than monetary support should play the leading role given the housing-market concerns and fiscal leeway. Tax reform should be a core element of structural policy. There is space for fiscal loosening given the low public-debt burden. Returns would be high for accelerated in infrastructure development and investing in skills, an area where Australia falls short of top-performing countries. Active measures to increase transfers to households could help address inequality, thereby making the recovery more inclusive.

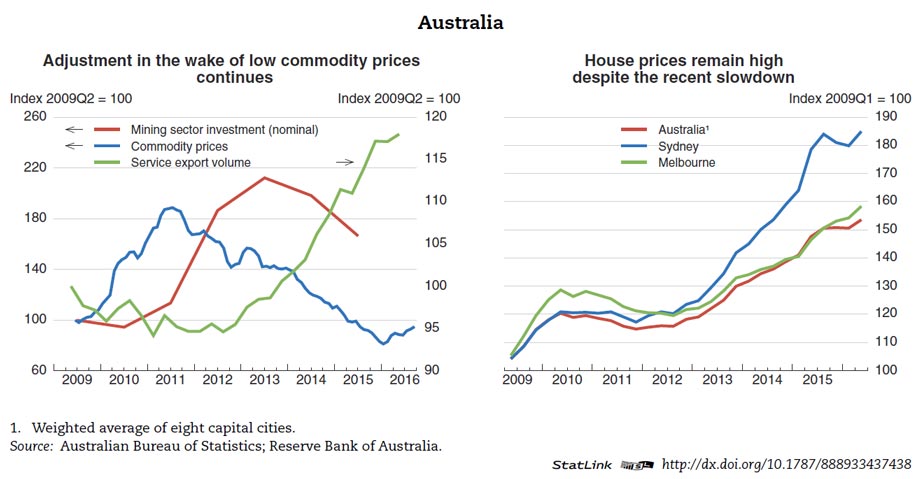

Reallocation towards non-resource sectors continues

Global iron ore and, especially, coal prices have risen, and new liquefied-natural-gas (LNG) production is coming on stream. Nevertheless, resource-sector investment and employment continue to decline. Non-resource output and employment, assisted by currency depreciation, continues to strengthen, notably services exports. However, non-resource investment has yet to pick up. House prices and mortgage credit continue to grow, though macro-prudential tightening has recently helped lessen the pace of increase. Consumer price inflation remains low.

Continued policy support for economic adjustment and productivity growth is required

In August 2016, the Reserve Bank decreased its policy rate by 25 basis points to 1.50%, the second reduction in 12 months. No further easing is projected, and rate increases are projected to begin towards the end of 2017 as spare capacity fades. Fiscal consolidation of around ½ percentage point of GDP is projected, as envisaged by the government. Despite the employment of macro-prudential measures to cool the housing market, the net gain from monetary easing has narrowed. Significant housing market concerns remain and there is growing discord between financial market developments and rest of the economy due to the low-interest-rate environment.

General-government debt has risen but from a low level and the debt-to-GDP ratio, currently around 45%, is projected to begin to fall. There is already fiscal space to respond to an unanticipated downturn in activity. There is room for spending increases, notably an acceleration in the public investment programmes underway in telecommunications, roads and public transport systems.

Boosting productivity and combatting exclusion remain important structural challenges. Implementation of the National Innovation and Science Agenda, a wide ranging package to boost innovation, continues. Also, some tax reforms are underway, notably efforts to better target pension (“superannuation”) taxation by assisting low-income earners and lowering taxpayer support for retirement accounts. Reductions in corporate tax rates are also proposed. However, the reforms fall short of a major shift in taxation as recommended in OECD Economic Surveys, which stress the importance of efficient tax bases, such as the Goods and Services Tax and land tax. In the greenhouse-gas-reduction policy area, a welcome safeguard mechanism has begun operating that discourages firms from offsetting emission reductions achieved via the Emission Reduction Fund.

A gradual pick-up in growth with sizeable uncertainties

Output growth is projected to strengthen to about 3% by 2018. LNG production will boost exports and negative effects from shrinking mining investment will diminish. Rebalancing towards non-mining sectors will drive a gradual pick-up of overall activity, helped by supportive macroeconomic policies. Employment growth should result in a further decline in the unemployment rate. Household consumption growth is expected to remain solid, aided by further downward adjustment in the household saving ratio to the historical average. The pick-up in aggregate demand is not projected to generate significant inflationary pressure, due to remaining economic slack.

Australia has experienced 25 years without recession, but there are risks looking forward. Commodity market developments, particularly those linked to the Chinese economy, remain an important source of uncertainty and risk. Domestically, non-resource investment may remain lacklustre, damping growth prospects. Also, the housing market remains a risk, as an acceleration in price adjustment would weaken consumption demand and construction activity”.