IF YOU’RE already starting to feel the mortgage pinch, this is bad news. New economic modelling shows mortgage defaults are set to rise over the next 12-18 months, and those who will be most affected will surprise you.

The research conducted by Digital Finance Analytics, based on its extensive household surveys, shows those falling behind in their mortgage repayments will continue to increase thanks to low wage growth and employment changes. This is despite record low interest rates.

This news follows a warning by Moody’s Investors Service that mortgage delinquencies have already hit a three-year high across the country.

“Incomes are just not growing and that is creating considerable difficulties for many households,” Principal of Digital Finance Analytics, Martin North told news.com.au.

“What I’m predicting is that incomes are going to remain static for the next 12-18 months … That means that households are in this difficult situation were they can just about afford their mortgages, but things like the general cost of living, which is going up faster than incomes, is going to create considerable pressure on many households.”

Western Australia and Queensland mining areas will bear the brunt, with New South Wales, Victoria and ACT being the best placed.

WHO IS MOST AT RISK?

First home buyers will unsurprisingly be in the firing line, as they are entering the housing market now when prices are so inflated and going in with the assumption that their income will grow.

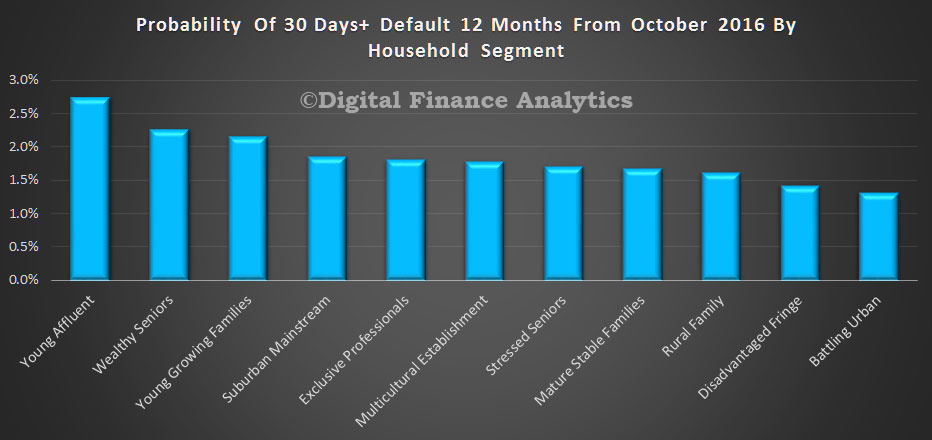

However, interestingly, those hit the hardest will be affluent young buyers and wealthy seniors. Disadvantaged households on the edge of cities, and battling urban households are at lower risks of default.

“People with large mortgages, so young affluent buyers who bought in Bondi, for example, are finding it much more difficult to keep that property out of default because their income is not growing. Even in the more affluent areas in the states where there is a greater economic momentum, you still have the hot spots of difficulty,” Mr North told news.com.au.

“Interestingly, it is not necessarily the more stressed households — the ones you would expect out on the fringe. And the reason for that is those households never got the pay rises and they never got the big mortgages because they couldn’t afford to.”

Wealthy seniors who own property will also face more mortgage stress due to a combination of stagnating income and lower returns from deposits and the sharemarket.

Mr North said he is concerned this could spell disaster for the economy.

“The reason is we have never had household debt as high as it is. This is new territory,” he told news.com.au.

“We’ve got this very high level of debt and we’ve got very flat incomes so it could work out in a rather bad way.”

He said retail spending and financial stability are going to take a hit as Australians will not have the discretionary income to spend and the performance of our major banks is heavily reliant on mortgages.