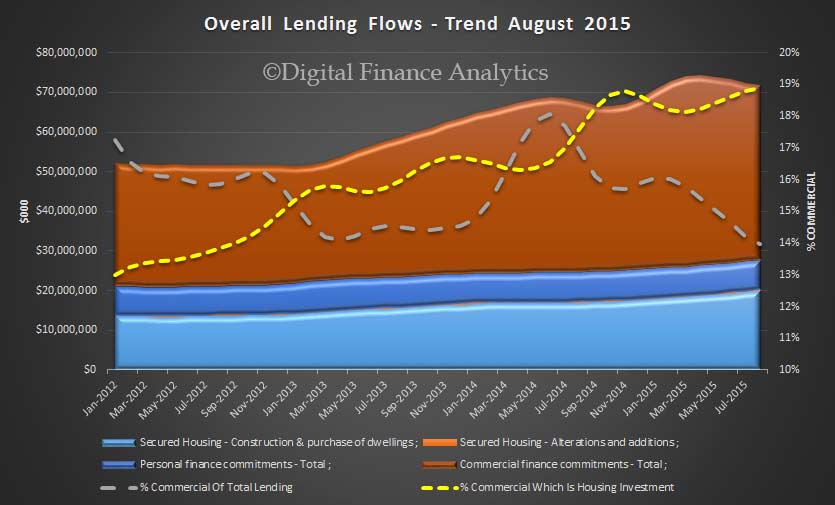

According to data released by the ABS, lending for housing is still very strong, though with some re-balancing away from lending for investment purposes. Total housing lending rose 0.63% seasonally adjusted to a new record of $1.49 trillion, of which $1.38 trillion sits with the banks, the rest is from the non-bank sector. However commercial lending fell using our preferred trend measurements. We do not think the current regulatory settings are right, because flows are still too strong in the housing sector. Of significant note is the relative fall in the proportion of lending going to business down to 14%; and the ongoing rise in the proportion of lending to business which relates to investment housing lending, up to 19%. Both indicators of a sick economy.

The ABS says that in August, the total value of owner occupied housing commitments excluding alterations and additions rose 1.9% in trend terms, and the seasonally adjusted series rose 6.1%. Investment housing commitments fell 0.2%. The trend series for the value of total personal finance commitments fell 0.8%. Fixed lending commitments fell 0.9% and revolving credit commitments fell 0.5%. The trend series for the value of total commercial finance commitments fell 2.1%. Revolving credit commitments fell 2.5% and fixed lending commitments fell 1.9%. The trend series for the value of total lease finance commitments rose 1.6% in August 2015

The ABS says that in August, the total value of owner occupied housing commitments excluding alterations and additions rose 1.9% in trend terms, and the seasonally adjusted series rose 6.1%. Investment housing commitments fell 0.2%. The trend series for the value of total personal finance commitments fell 0.8%. Fixed lending commitments fell 0.9% and revolving credit commitments fell 0.5%. The trend series for the value of total commercial finance commitments fell 2.1%. Revolving credit commitments fell 2.5% and fixed lending commitments fell 1.9%. The trend series for the value of total lease finance commitments rose 1.6% in August 2015

But as you dig into the data, some interesting themes emerge. So we will run through the main findings in some detail, using data from the two ABS series. We will focus on the housing sector.

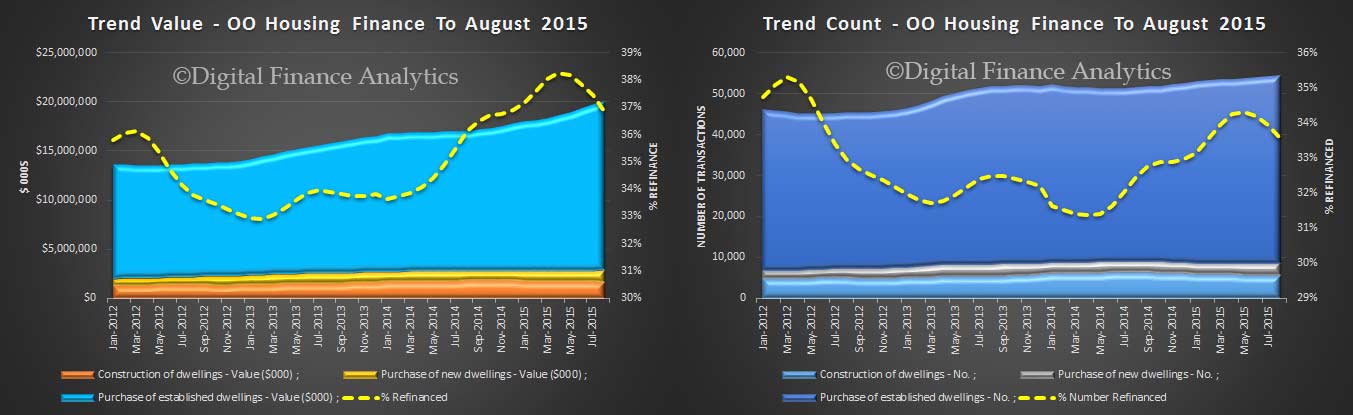

Recent heavy discounting and incentives have lead to a significant rise in owner occupied lending. The bulk relates to the purchase of existing property, lending for construction fell again. We also see a relative slight fall in the proportion of loans refinancing existing borrowing, but the proportion is still, by value at the strongest it has been since 2012. Overall more then 20% of transactions are for refinance purposes. Many of the banks have attractive low cost offers to switch, so we expect to see significant (though unproductive) churn in home loans, as banks fight for owner occupied share.

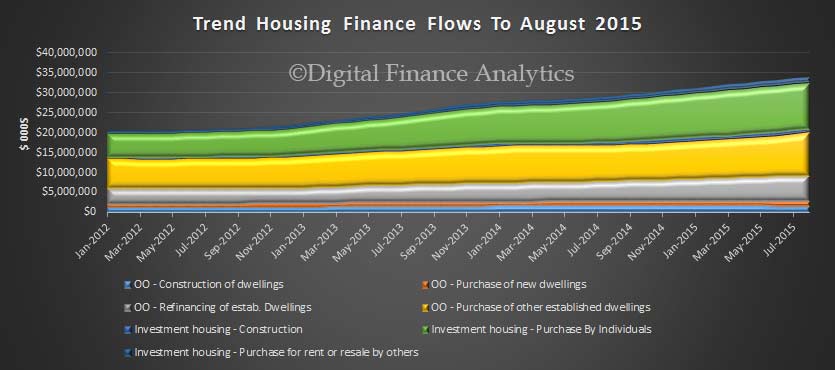

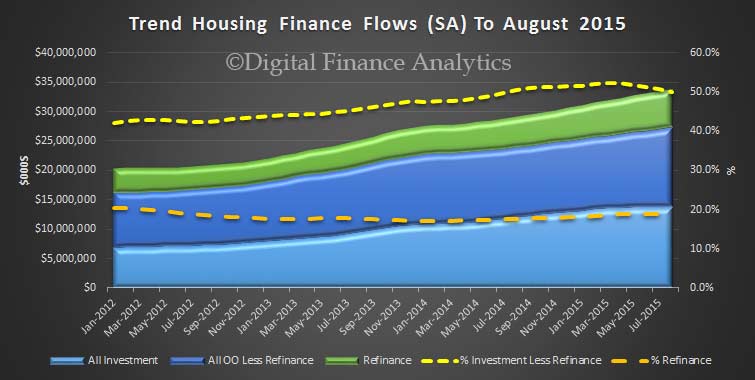

Investment lending continues to be a significant element in the numbers.

Investment lending continues to be a significant element in the numbers.

If you remove refinanced loans from the calculation, 50% of new loans were for investment purposes, a slight drop from the 52% in February, but still very strong.

If you remove refinanced loans from the calculation, 50% of new loans were for investment purposes, a slight drop from the 52% in February, but still very strong.

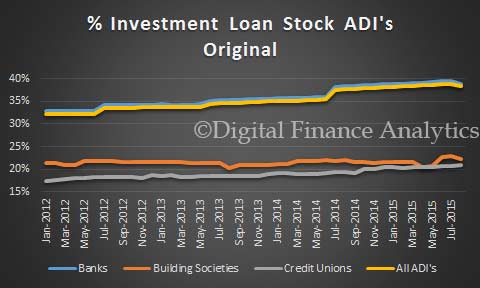

Looking at investment loans by lender type, we see the banks leading the way, with their stock of investment loans sitting in the high thirties. The chart also clearly shows the adjustments lenders made in their categories, from Jun 2014, (this is an artificial hike, as they did not re-baseline their loans in earlier years). We see growth in the stock of loans for investment purposes held by building societies and credit unions, but at a lower level than the banks.

Looking at investment loans by lender type, we see the banks leading the way, with their stock of investment loans sitting in the high thirties. The chart also clearly shows the adjustments lenders made in their categories, from Jun 2014, (this is an artificial hike, as they did not re-baseline their loans in earlier years). We see growth in the stock of loans for investment purposes held by building societies and credit unions, but at a lower level than the banks.

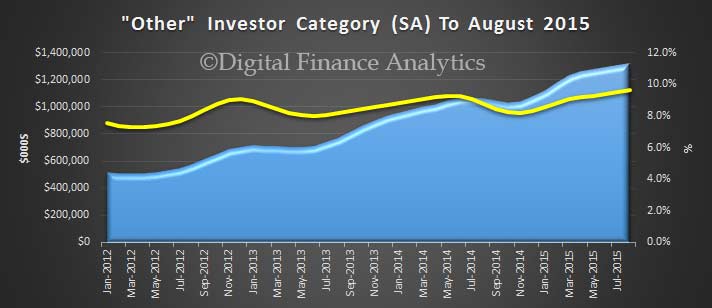

Within the investment sector, we see a rise in investment loans to entities other than individuals. These will include companies and self-managed superannuation funds.

Within the investment sector, we see a rise in investment loans to entities other than individuals. These will include companies and self-managed superannuation funds.

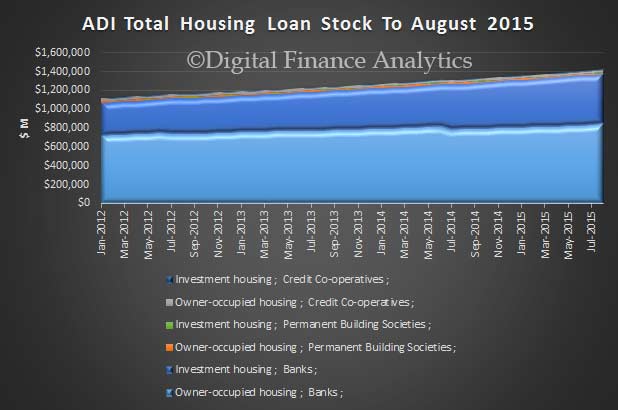

As previously highlighted the stock of housing continues to rise.

As previously highlighted the stock of housing continues to rise.

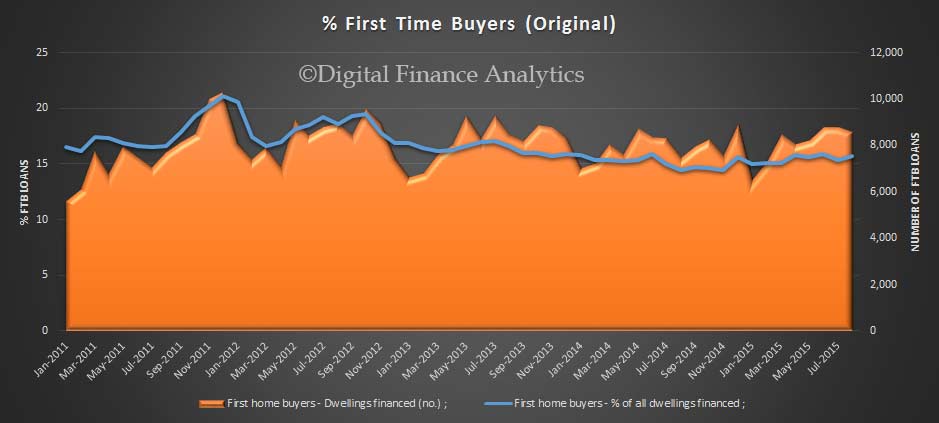

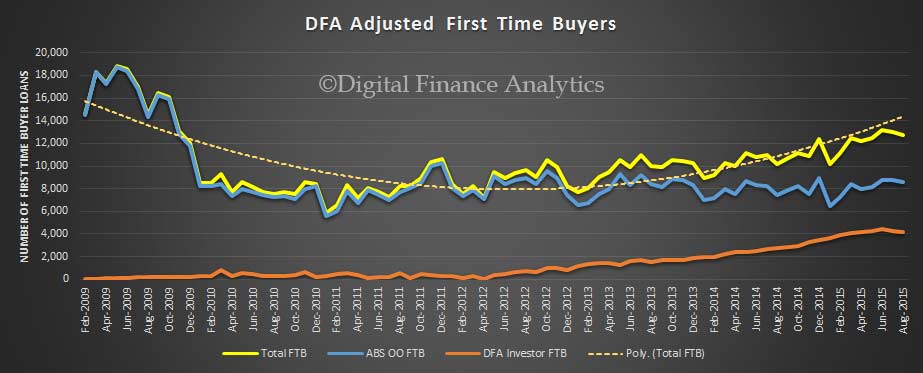

Next we look at first time buyers. In original terms, the number of first home buyer commitments as a percentage of total owner occupied housing finance commitments rose to 15.7% in August 2015 from 15.4% in July 2015. However, the absolute number of first time buyer loans was lower in the month, down 2.4% on July. The average loan rose from $341,000 to $346,000, illustrating again that purchasers are reacting to higher prices by getting larger loans, despite apparently tighter lending criteria. Not sure how this works!

Next we look at first time buyers. In original terms, the number of first home buyer commitments as a percentage of total owner occupied housing finance commitments rose to 15.7% in August 2015 from 15.4% in July 2015. However, the absolute number of first time buyer loans was lower in the month, down 2.4% on July. The average loan rose from $341,000 to $346,000, illustrating again that purchasers are reacting to higher prices by getting larger loans, despite apparently tighter lending criteria. Not sure how this works!

If we then overlay the data from the DFA household surveys, we see that investment first time buyers are still active, but in slightly lower numbers, so overall, the number of first time buyer loans last month fell a little.

If we then overlay the data from the DFA household surveys, we see that investment first time buyers are still active, but in slightly lower numbers, so overall, the number of first time buyer loans last month fell a little.

One thought on “Housing Finance Still Strong In August”