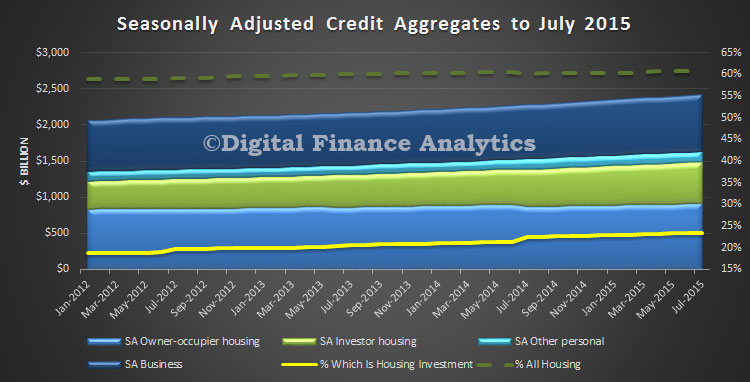

The latest RBA credit aggregates to end July 2015 show continued momentum in the home lending sector, up 7.4% in the year to July, compared with business lending up 4.8% and personal credit up 0.9%. Lending for housing comprised more than 60% of all lending on the books. 23.5% of all lending goes to investment housing. As APRA said recently, we hope it is as “safe as houses“. Total lending for housing is a seasonally adjusted $1,476.1 billion, up $8.5 billion, up 0.58% on the previous month.

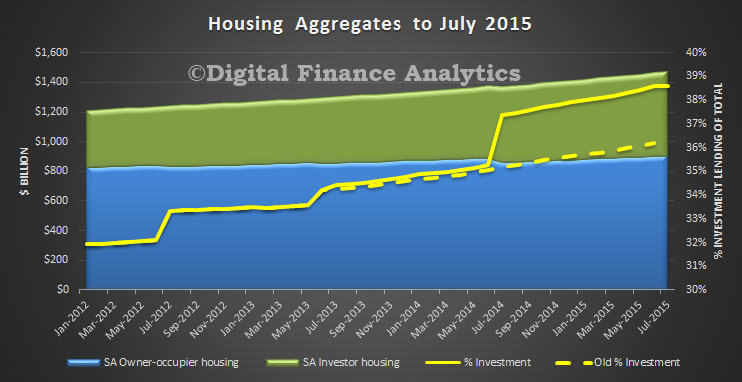

We need to point out that the various restatements by the banks (including NAB and ANZ), especially between the owner occupied and investment categories has had quite an impact on the numbers. In the month, lending for investment grew 3.6bn, up 0.64% to $569.8 billion in the month, whilst owner occupied lending grew 4.9 billion to $906.4 billion, up 0.54%. Overall growth for investment lending was an adjusted 10.2% on total balances. This includes both ADI’s and others lenders. However, there was a significant movement shown from July 2014, where the restatements kick in, and we see that on the old basis investment housing was 36.2% of all lending for housing, whereas on the new basis, it has now risen to 38.6%. A sizable change. A record, and given the intrinsically higher risks in investment loans, a concern.

We need to point out that the various restatements by the banks (including NAB and ANZ), especially between the owner occupied and investment categories has had quite an impact on the numbers. In the month, lending for investment grew 3.6bn, up 0.64% to $569.8 billion in the month, whilst owner occupied lending grew 4.9 billion to $906.4 billion, up 0.54%. Overall growth for investment lending was an adjusted 10.2% on total balances. This includes both ADI’s and others lenders. However, there was a significant movement shown from July 2014, where the restatements kick in, and we see that on the old basis investment housing was 36.2% of all lending for housing, whereas on the new basis, it has now risen to 38.6%. A sizable change. A record, and given the intrinsically higher risks in investment loans, a concern.

Given all the noise in the numbers, it is hard to conclude other than home investment lending remains buoyant – in line with the DFA household surveys and expectations. We will report on the APRA monthly banking stats shortly, were individual bank movements can be analysed.

Given all the noise in the numbers, it is hard to conclude other than home investment lending remains buoyant – in line with the DFA household surveys and expectations. We will report on the APRA monthly banking stats shortly, were individual bank movements can be analysed.