The IMF released their Regional Economic Outlook for Asia Pacific to April 2015 today. China’s growth is predicted to fall, Australia’s to rise a little, on a comparative basis, our banks hold lower capital than many across the region, and the IMF stress the importance of macroprudential measures to reign in house prices, and fiscal stimulus to support economic growth. A few selected highlights:

Asynchronous monetary policies in major advanced economies in response to divergent cyclical conditions have contributed to large and rapid exchange rate realignments. Robust growth and the prospect of higher interest rates in the United States, coupled with the start of quantitative easing in the euro area and further monetary stimulus in Japan, have caused the value of the major reserve currencies to diverge sharply. While the dollar has gained substantially against most other currencies, rising about 9½ percent on a trade-weighted basis since the end of June 2014, the yen has fallen by about 10½ percent in nominal effective terms over the same period, and the euro has been broadly unchanged.

Against this backdrop, a number of Asia and Pacific currencies have appreciated in nominal effective terms since mid-2014. This reflects somewhat greater stability of Asian currencies relative to the dollar than implied by the share of the United States in these countries’ gross trade. In contrast, the currencies of commodity exporting Australia, Malaysia, and New Zealand have depreciated in nominal effective terms

(Figure 1.7).

Changes in real effective exchange rates have been broadly in line with changes in their nominal counterparts. However, using weights based on domestic value added in exports, appreciations of most Asian currencies have been less pronounced, suggesting a more modest erosion

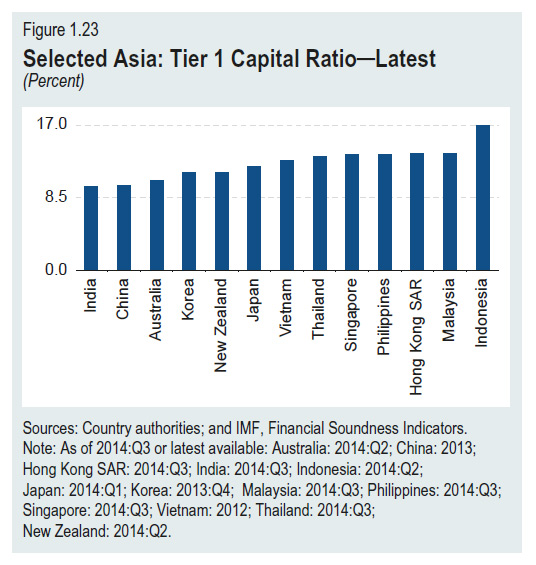

Bank balance sheets have strengthened across most of Asia. Bank profitability has been high in many countries and, together with injections of new Basel III–compliant equity, has contributed to an increase in Tier 1 capital (Figure 1.23). Note that Australia is at the lower end of Tier 1.

While still outperforming most other large economies, China’s growth rate is expected to continue to edge lower over the medium term as rebalancing proceeds. Growth is projected to ease to 6.8 percent in 2015 and to 6.3 percent in 2016 as the correction in the residential and related sectors continues to drag on investment.

The downturn in the global commodity cycle will continue to affect Australia’s economy, with related investment coming off historic highs. However, supportive monetary policy and a weaker exchange rate will underpin nonresource activity, helping to edge up growth in 2015 to 2.8 percent, rising to 3.2 percent in 2016 (broadly unchanged from projections in the October 2014 WEO).

In Australia and New Zealand, consumers gain from the oil price windfall while forgone mining receipts and royalties have a negative effect on mining companies and the fiscal accounts.

In addition to strong microprudential supervision and regulation, protecting financial stability will require proactive use of macroprudential policies to increase resilience to shocks and contain the buildup of systemic risk associated with changes in financial conditions. In fact, greater reliance on macroprudential policies may be needed where the fi nancial cycle is not well synchronized with the real economy cycle (Australia, Hong Kong SAR, Korea), which may be more likely in the presence of strong unconventional monetary policies in the major economies. To avert overheating or overinvestment in real estate that could threaten the stability of financial systems, eliminating the preferential tax treatment of real estate (for example, by raising taxes on real estate capital gains) and tightening regulations on credit financing for real estate development and purchase (for example, imposing binding loan-to-value limits and debt-service-to-income ceilings) are advised. Macroprudential policies and capital flow measures should not substitute for appropriate macroeconomic policy reactions to volatile capital flows and asset price swings.

On the other hand, fiscal stimulus, or a slower pace of consolidation, may be appropriate for economies facing temporary adverse terms-of-trade shifts or where output is below the full-capacity level (Australia, Korea). But care should be taken to ensure that stimulus is reversed during cyclical upturns and to avoid conflating weaker potential growth with a temporary growth dip.