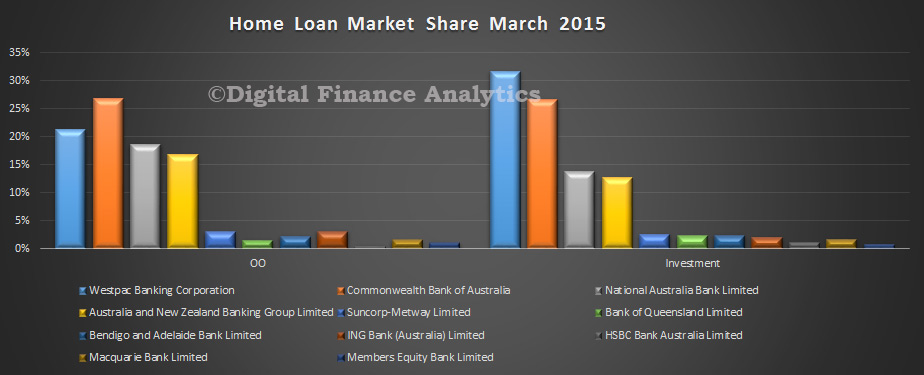

APRA published their monthly banking statistics for March. Overall housing lending was $1.336 trillion by the banks (the RBA number of $1.45 trillion includes the non banks). This was a rise of 0.59% in the month, with owner occupied loans lifting 0.46% and investment loans 0.84%. Investment loans accounted for 35.1% of all loans in the month. Looking at the individual bank data, there was little change, with CBA holding the largest share of owner occupied loans, and Westpac, investment loans. Macquarie continues its growth path.

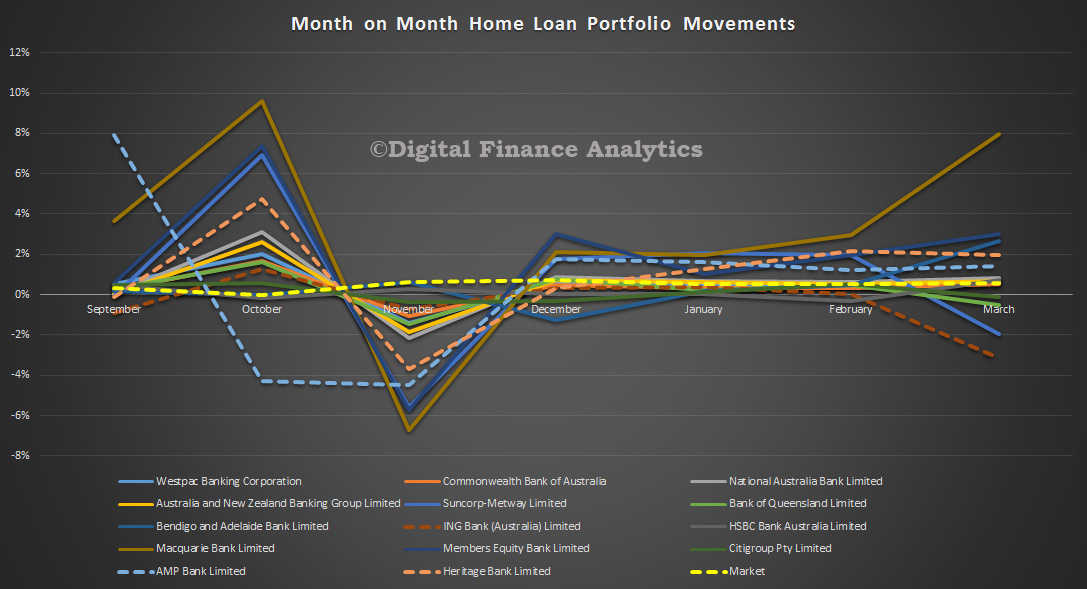

Looking at the portfolio movements, ING and Suncorp both lost portfolio share, whilst Macquarie continues to expand at pace. Members Equity and Bendigo/Adelaide also grew well above the market average.

Looking at the portfolio movements, ING and Suncorp both lost portfolio share, whilst Macquarie continues to expand at pace. Members Equity and Bendigo/Adelaide also grew well above the market average.

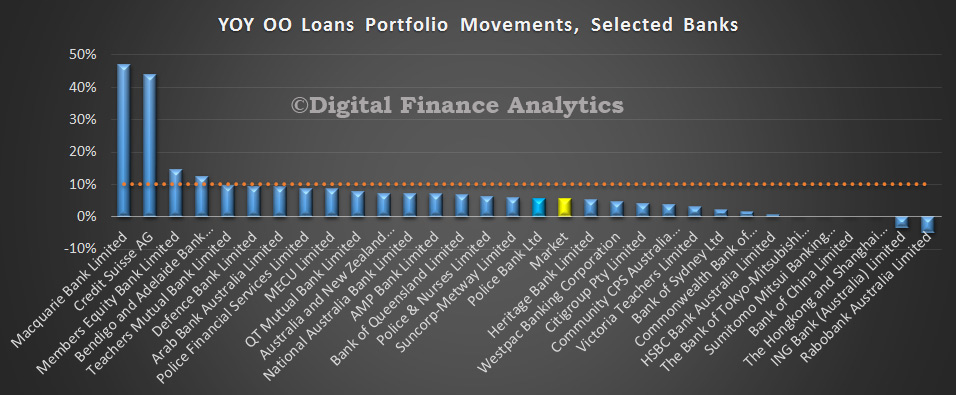

Looking at the annual growth rates, for owner occupied loans, Macquarie led the way (partly thanks to acquisition) and ANZ was the major with the largest growth.

Looking at the annual growth rates, for owner occupied loans, Macquarie led the way (partly thanks to acquisition) and ANZ was the major with the largest growth.

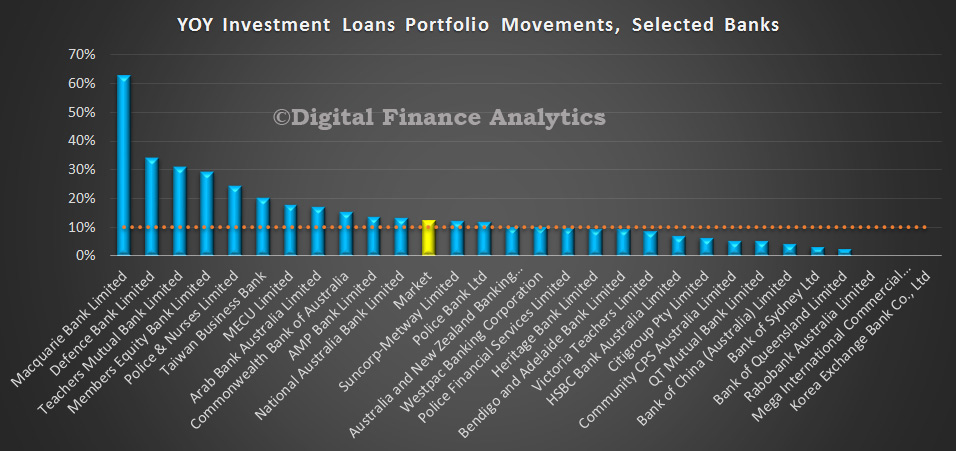

On the investment lending side, where there is more interest in not exceeding the 10% “alert” level, we see that ANZ and Westpac were at 10%, whilst CBA and NAB were above the 10% mark. Macquarie and Members Equity continue to grow their investment lending book well above system. No doubt the regulators are having a quiet word! As APRA said, “strong growth in lending to property investors — portfolio growth materially above a threshold of 10 per cent will be an important risk indicator for APRA supervisors in considering the need for further action”

On the investment lending side, where there is more interest in not exceeding the 10% “alert” level, we see that ANZ and Westpac were at 10%, whilst CBA and NAB were above the 10% mark. Macquarie and Members Equity continue to grow their investment lending book well above system. No doubt the regulators are having a quiet word! As APRA said, “strong growth in lending to property investors — portfolio growth materially above a threshold of 10 per cent will be an important risk indicator for APRA supervisors in considering the need for further action”

Talking about APRA, their supervisory lens also includes serviceability buffers – “loan affordability tests for new borrowers — in APRA’s view, these should incorporate an interest rate buffer of at least 2 per cent above the loan product rate, and a floor lending rate of at least 7 per cent, when assessing borrowers’ ability to service their loans. Good practice would be to maintain a buffer and floor rate comfortably above these levels”. So how come we do not get any reporting on this dimension? As discussed before, this should be addressed.

Talking about APRA, their supervisory lens also includes serviceability buffers – “loan affordability tests for new borrowers — in APRA’s view, these should incorporate an interest rate buffer of at least 2 per cent above the loan product rate, and a floor lending rate of at least 7 per cent, when assessing borrowers’ ability to service their loans. Good practice would be to maintain a buffer and floor rate comfortably above these levels”. So how come we do not get any reporting on this dimension? As discussed before, this should be addressed.

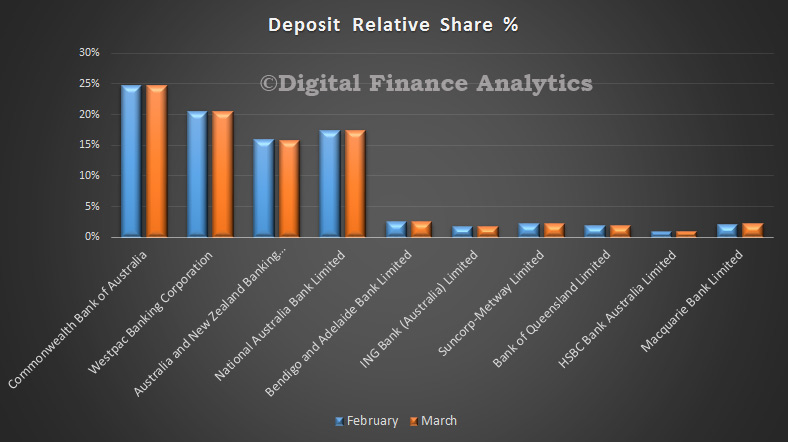

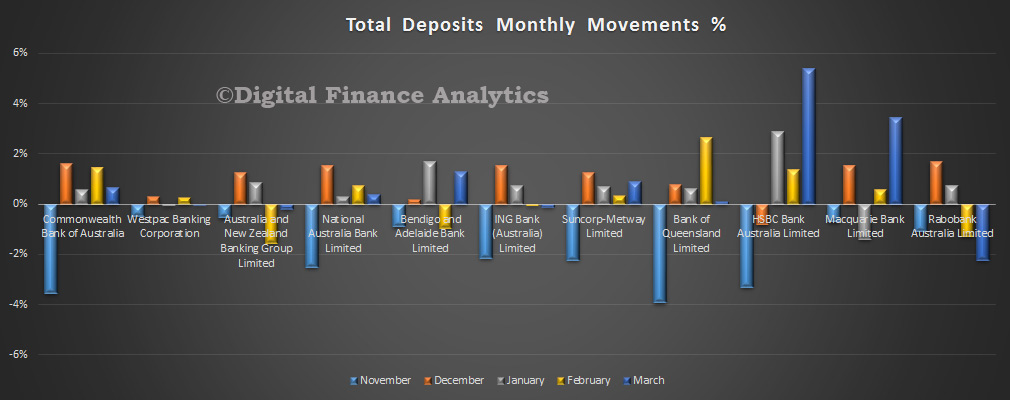

Deposits grew at 0.47%, so slower than lending, indicating that some banks are relying more on other funding avenues to support growth. Deposits rose by $8.6 billion to a total of 1.8 trillion. There was little relative movement amongst the major players in terms of share, though we do see deposit repricing in hand, with rates continuing to falling.

Individual movements are charted below for selected banks.

Individual movements are charted below for selected banks.

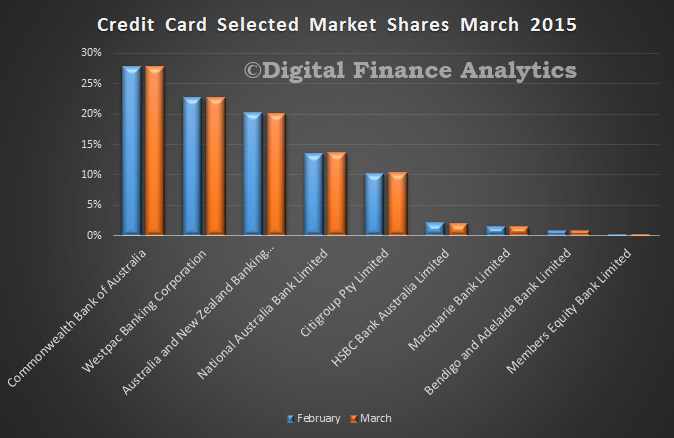

Finally, the credit card portfolio grew by $169 million in the month, and sits at $41,6 billion. Little change in the market shares reported this month.

Finally, the credit card portfolio grew by $169 million in the month, and sits at $41,6 billion. Little change in the market shares reported this month.