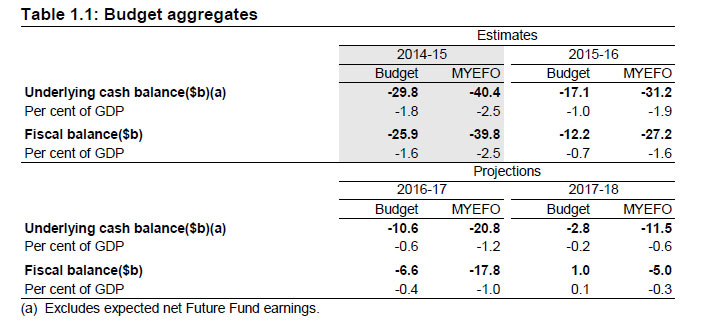

The Government published their mid-term review today. Since May, two key factors have primarily driven the $43.7 billion deterioration in the budget over the forward estimates: the impact of the economy on tax receipts and payments; and the impact of the Senate’s decisions. Primarily as a result of the collapse in iron ore prices by over 30 per cent and weaker than expected wage growth, tax receipts have been revised down by $31.6 billion. Government payments have also been affected. Delays in passing legislation and negotiations with the Senate have cost the budget more than $10.6 billion over the forward estimates, keeping debt and interest payments higher for longer. An underlying cash deficit of $40.4 billion is now expected in 2014-15 (2.5 per cent of GDP), narrowing to a deficit of $11.5 billion (0.6 per cent of GDP) by 2017-18.

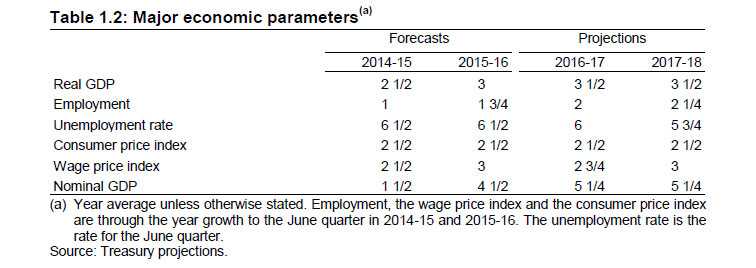

Overall, the outlook for real GDP growth is unchanged since Budget. Real GDP is forecast to grow at 2½ per cent in 2014-15, before increasing to near-trend growth of 3 per cent in 2015-16. This reflects the expectation of solid growth of real activity in the economy continuing.

Overall, the outlook for real GDP growth is unchanged since Budget. Real GDP is forecast to grow at 2½ per cent in 2014-15, before increasing to near-trend growth of 3 per cent in 2015-16. This reflects the expectation of solid growth of real activity in the economy continuing.

However, the changes to the economic outlook since the Budget are driven by the sharper than expected fall in the terms of trade, including significant falls in prices of iron ore and coal, and weaker wage growth. While the forecasts for solid real GDP growth are unchanged, the prices we receive for our production have declined significantly. Accordingly, nominal GDP growth in 2014-15 is expected to be weaker than forecast at Budget, at 1½ per cent. This would be the weakest nominal GDP growth in a financial year in over 50 years.

Iron ore prices have unexpectedly fallen by over 30 per cent since the Budget. MYEFO assumes a free-on-board iron ore price of US$60 per tonne over the next two years, which compares with a spot price of US$95 at Budget. The fall in iron ore prices has led to company tax receipts being revised down by $2.3 billion in 2014-15 and $14.4 billion over the forward estimates. At the same time weaker wage and employment growth are expected to lower individuals’ income tax receipts by $2.3 billion in 2014-15 and $8.6 billion over the forward estimates. Weaker wage and employment growth will also increase payments for existing government programmes. Excluding policy changes, total taxation receipts have been revised down by $6.2 billion in 2014-15 and $31.6 billion over the forward estimates. This brings the total writedown in tax receipts since the Government was elected to over $70 billion. To avoid detracting from economic growth, the Government has let the impact on the budget from sharply lower iron ore prices and slower wage growth flow through to the bottom line, rather than taking decisions to cut expenditure dramatically or increase tax.

Iron ore prices have unexpectedly fallen by over 30 per cent since the Budget. MYEFO assumes a free-on-board iron ore price of US$60 per tonne over the next two years, which compares with a spot price of US$95 at Budget. The fall in iron ore prices has led to company tax receipts being revised down by $2.3 billion in 2014-15 and $14.4 billion over the forward estimates. At the same time weaker wage and employment growth are expected to lower individuals’ income tax receipts by $2.3 billion in 2014-15 and $8.6 billion over the forward estimates. Weaker wage and employment growth will also increase payments for existing government programmes. Excluding policy changes, total taxation receipts have been revised down by $6.2 billion in 2014-15 and $31.6 billion over the forward estimates. This brings the total writedown in tax receipts since the Government was elected to over $70 billion. To avoid detracting from economic growth, the Government has let the impact on the budget from sharply lower iron ore prices and slower wage growth flow through to the bottom line, rather than taking decisions to cut expenditure dramatically or increase tax.

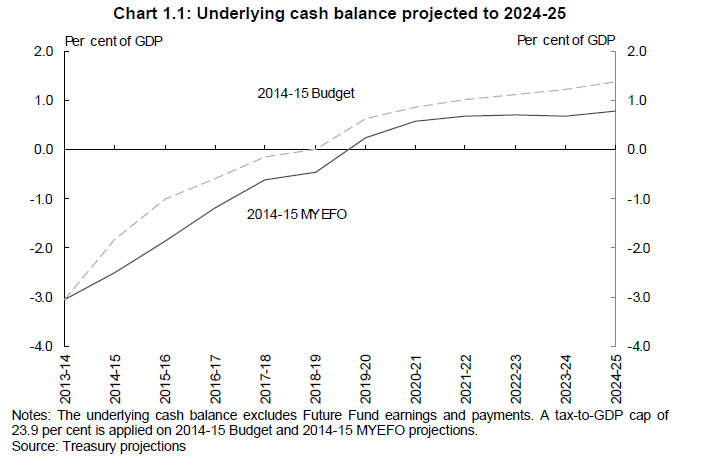

The 2013-14 MYEFO showed that, without action, the budget would not return to surplus for a decade, and debt would reach $667 billion by 2023-24 and still be rising. Despite the deterioration in the fiscal outlook over the forward estimates, the medium-term outlook for the budget is considerably better than a year ago. Debt is now projected to be nearly $170 billion lower than it would have been by 2023-24 and to be falling. The underlying cash balance is projected to reach surplus in 2019-20, with the surplus reaching 0.8 per cent of GDP by the end of the medium term, including future tax relief being incorporated from 2020-21. This remains a considerable improvement from the 2013-14 MYEFO projections.