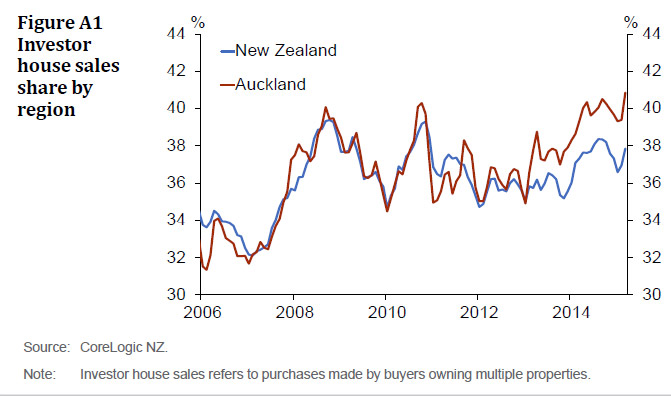

In the May Stability Report the RBNZ have drilled into the Investment Property sector. They say they will be publishing more detailed data, but the current article makes interesting reading. Housing investors have consistently accounted for over one-third of property purchase transactions over the past decade, with the share rising slightly following the introduction of loan-to-value ratio (LVR) restrictions in October 2013 (figure A1). Sales to investors in the Auckland market have picked up in line with the rise in sales activity since November, and this is likely to be contributing to recent strength in Auckland house prices. Investors are also a key source of new mortgage credit demand, with property investors accounting for approximately one-third of new mortgage lending over the six months ended March 2015.

Although New Zealand has not experienced a financial crisis associated with the housing market, a range of international evidence suggests that defaults on investor lending tend to be significantly higher than for owner occupiers during severe downturns. For example, Irish investor mortgage default rates were around 20 percent higher than total mortgage default rates in the two years following the GFC. Default probabilities were estimated to have been significantly higher than owner-occupiers at any given LVR. Evidence from the UK and the US also finds that default rates were relatively high among investors in severe downturns. The Reserve Bank’s proposal to apply higher risk weights to investor lending, and introduce a differential LVR threshold for investors relative to owneroccupiers in Auckland, is consistent with this evidence.

A key driver of the higher default propensity of residential property investors is higher debt-to-income ratios (income gearing) relative to owner-occupiers. For example, an investor who has borrowed to buy four houses will end up with much larger negative equity relative to their labour income, if house prices fall, than an owner-occupier with just one house and a similar LVR. Higher income gearing reduces the incentive for the investor to continue servicing the outstanding loans, resulting in a greater tendency for investors to default when they have negative equity.

Another possible reason for the higher risks associated with investor lending is that investor house purchases have, in some countries, tended to be concentrated in areas with high expected capital growth. These expectations are often based on recent house price appreciation.

Evidence from the US suggests that increases in house prices prior to the GFC were particularly pronounced in regions where the investor share of house purchases increased. In turn, areas with rapid house price inflation experienced relatively large house price falls in the aftermath of the crisis.

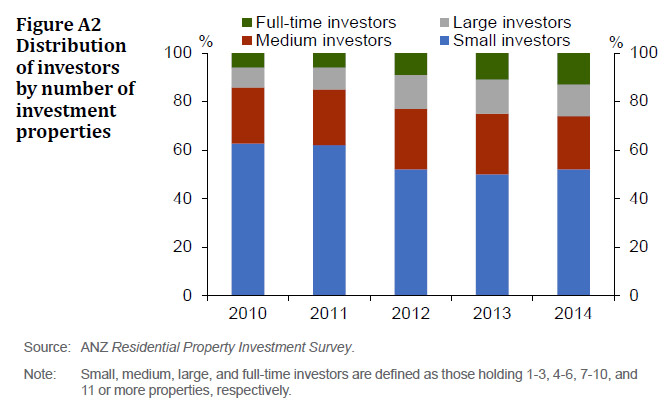

In New Zealand, a significant proportion of property investors have large portfolios, implying a large degree of gearing relative to their underlying labour income. For example, the 2014 ANZ Residential Property Investment Survey shows that 26 percent of surveyed investors held seven or more investment properties (figure A2). Around half of investor commitments are at LVRs of more than 70 percent. Preliminary Reserve Bank survey data suggests that investors tend to make greater use of interest-only loans, which may partly reflect investors’ ability to offset mortgage expenses against personal income for tax purposes. As a result, investor loans are likely to retain a higher level of gearing over the long term than their owner-occupier counterparts.

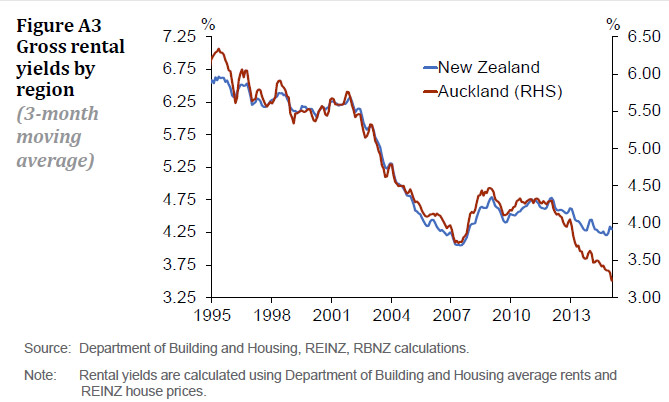

The risks associated with investor lending are likely to be greatest in the Auckland region. Rapid house price appreciation in Auckland has compressed rental yields, and this is likely increasing income gearing among Auckland investors. Auckland rental yields are at record lows, while national yields are close to their 10-year average (figure A3). Relatively strong capital gain expectations among Auckland investors may explain why they are willing to accept such low rental yields. According to the 2014 ANZ Residential Property Investment Survey, investors in Auckland expected house price inflation to average 12 percent per annum in the region over the coming five years, compared to 8 percent nationwide. CoreLogic data also show that investors in the Auckland region are more likely to use mortgage finance than investors outside the Auckland region.

The risks associated with investor lending are likely to be greatest in the Auckland region. Rapid house price appreciation in Auckland has compressed rental yields, and this is likely increasing income gearing among Auckland investors. Auckland rental yields are at record lows, while national yields are close to their 10-year average (figure A3). Relatively strong capital gain expectations among Auckland investors may explain why they are willing to accept such low rental yields. According to the 2014 ANZ Residential Property Investment Survey, investors in Auckland expected house price inflation to average 12 percent per annum in the region over the coming five years, compared to 8 percent nationwide. CoreLogic data also show that investors in the Auckland region are more likely to use mortgage finance than investors outside the Auckland region.