Interesting statement from the Bank of Canada, their central bank.

During this time of heightened public health measures intended to limit the transmission of COVID-19, some consumers and businesses are choosing not to use cash to limit potential exposure. Refusing cash could put an undue burden on people who depend on cash as a means of payment. The Bank strongly advocates that retailers continue to accept cash to ensure Canadians can have access to the goods and services they need.

This is important, and like the Reserve Bank of New Zealand who also recently underscored the importance of cash in the economy, it reinforces the importance of keep real money available.

The Australian Statistician announced on 16 March the commitment of the ABS to provide the community and governments with access to additional, more up-to-date information on the economic responses of individuals and businesses to the coronavirus, COVID-19.

This preliminary retail turnover data release is the first in a series of additional product releases over the coming months to help measure the economic impact of coronavirus. This release provides the preliminary estimate for Australian retail turnover for the month of February. This estimate will be subject to revision with the final monthly estimate published 3 April, 2020 in Retail Trade, Australia (Cat no 8501.0). Future preliminary retail turnover estimates will be published around two weeks prior to the advertised release date of Retail Trade, Australia (Cat no 8501.0).

Australian retail turnover rose 0.4 per cent, based on preliminary figures, in February 2020, seasonally adjusted, according to the latest Australian Bureau of Statistics (ABS) Retail Trade figures.

The preliminary figures indicate a rise in food will be slightly offset by falls in industries such as clothing, footwear and personal accessories and other retailing. While some businesses (e.g. those that rely on tourism) reported that coronavirus negatively impacted turnover, a range of other businesses saw limited impacts from coronavirus in February.

In a press conference this morning, Prime Minister Scott Morrison upgraded the travel ban on Australians to level four for the entire world in the wake of the coronavirus outbreak. This is the first such ban in Australian history.

A human biosecurity emergency has been declared under the Biosecurity Act by the Governor-General.

“The travel advice to every Australian is do not travel abroad. Do not go overseas. That is very clear instruction,” he said. Domestic air travel though will not be cancelled as it is “low risk”.

Scott Morrison said the country will not go into lockdown during the COVID-19 pandemic, saying the situation will last at least six months.

Prime Minister Scott Morrison said non-essential indoor gatherings of persons more than 100 have been now banned.

The health advice is that schools should remain open, Morrison said.

However, to reduce the risk of transmission to aged care residents, visits will be limited to a short duration and will only allow a maximum of two visitors at one time per day.

He criticised (rightly) the panic buying chaos across the nation. ” Stop it. It is not sensible, it is not helpful and I have to say it is has been one of the most disappointing things I have seen in Australian behaviour in response to this crisis,” he said.

He flagged further economic measures will emerge soon with the government is considering further economic measures that will deal with the impact of the coronavirus on the Australian economy, particularly on small businesses and individuals.

Chief Medical Officer Brendan Murphy said there are about 450 cases of COVID-19 in Australia, with increasing numbers each day. There is only “limited community transmission”.

Australia has completed more than 80,000 tests, with additional supplies being secured.

“Further supplies are being secured and that includes having domestic solutions to the supply issues that relates to the supply issues that relates to the testing equipment.”

Growth through 2020 is now estimated at 1.5% with minus 1% in the first half ( minus 0.7% and minus 0.3% respectively in the March and June quarters) and 2.5% in the second half. This is recession territory.

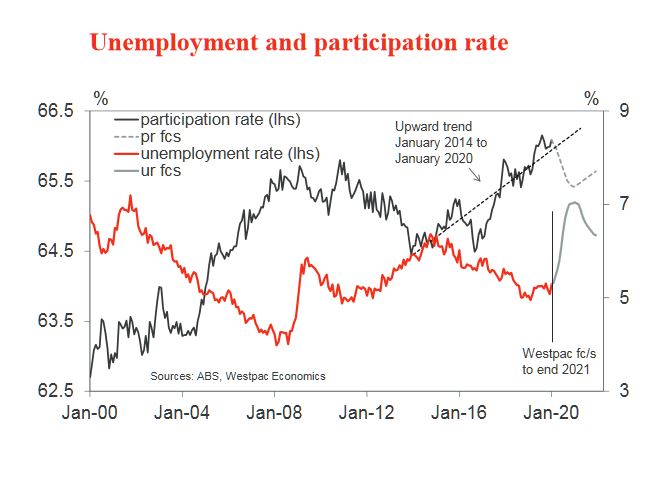

Just last week they had set the forecast peak in the unemployment rate at around 5.8%- 6%, up from the current level of 5.3%.

But now the unemployment rate is now forecast to reach 7% by October 2020 (up from the previous estimate of 5.8%-6.0%) due to the larger negative shocks to the labour intensive sectors such as recreation; tourism; education; renovations and additions; and dwelling construction. This lift in the unemployment rate is despite reducing the participation rate from 66.1% to 65.4% as a discouraged worker effect – that is, as workers respond to a deteriorating labour market the participation rate is likely to decline.

They add: please note that these forecasts are not based on Australia following a European style full lock down. Not surprisingly, the forecasts are subject to downward revision in the event of such an occurrence.

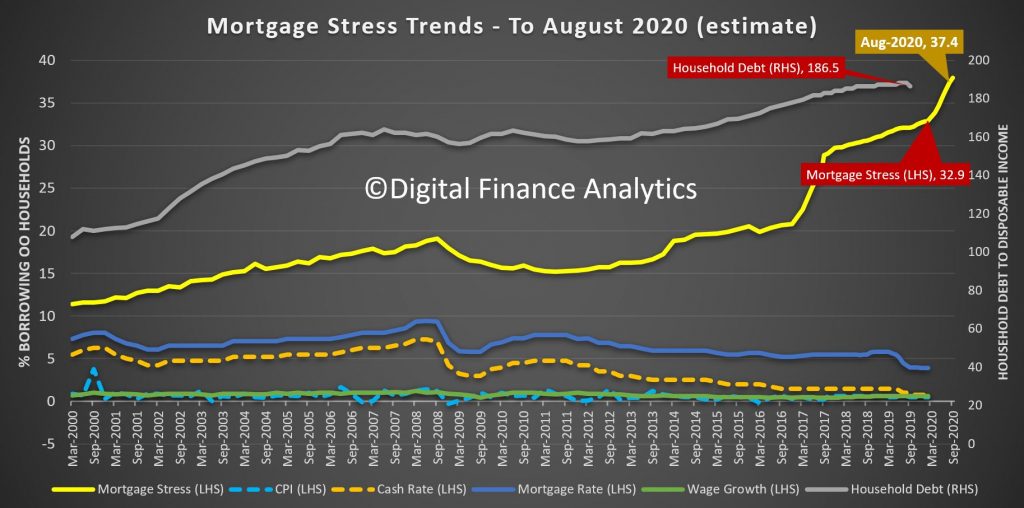

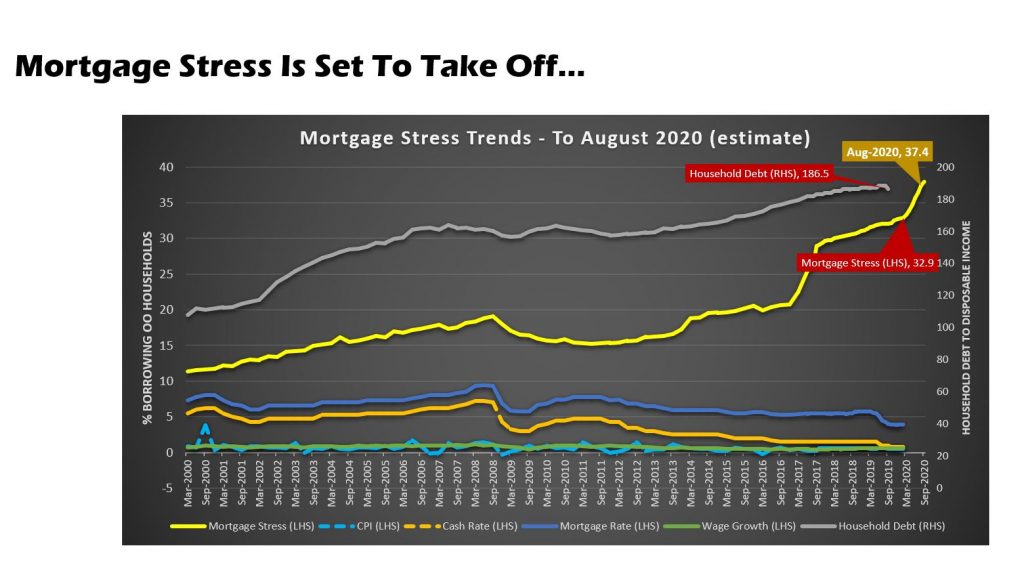

This is consistent with our modelling – mortgage stress will rise in the months ahead as unemployment rises.

Now the question becomes, to what extent with the banks forego mortgage repayments, and not foreclose, and to what extent will the Government supports households directly? The mortgage debt mountain could bite deep and early.

Its also worth noting that we are already seeing a rise in financial stress among those renting – here the protections currently are very limited, and will need to be increased.

Our own modelling is based on the assumption the crisis will run for at least 6 months. Overnight a UK report suggested 18 months is more likely, given the lead time to a vaccine.

UK Treasury and the Bank are coordinating closely in order to ensure that our initiatives are complementary and that they will, collectively, have maximum impact, consistent with the Bank and HM Treasury’s independent responsibilities.

Although the magnitude of the economic

shock from Covid-19 is highly uncertain, activity is likely to weaken

materially in the United Kingdom over the coming months. Temporary, but

significant, disruptions to supply chains and weaker activity could

challenge cash flows and increase demand for working capital from

companies.

The CCFF will provide funding to

businesses by purchasing commercial paper of up to one-year maturity,

issued by firms making a material contribution to the UK economy. It

will help businesses across a range of sectors to pay wages and

suppliers, even while experiencing severe disruption to cashflows.

The facility will offer financing on terms

comparable to those prevailing in markets in the period before the

Covid-19 economic shock, and will be open to firms that can demonstrate

they were in sound financial health prior to the shock. The facility

will look through temporary impacts on firms’ balance sheets and cash

flows by basing eligibility on firms’ credit ratings prior to the

Covid-19 shock. Businesses do not need to have previously issued

commercial paper in order to participate.

The scheme will operate for at least 12

months and for as long as steps are needed to relieve cash flow

pressures on firms that make a material contribution to the UK economy.

The Bank will publish further details of the operation of the CCFF in a

Market Notice on Wednesday 18 March. The Bank will implement the

facility on behalf of the Treasury and will put it into place as soon as

possible.

By providing an alternative source of

finance for a wide range of companies, the scheme will help to preserve

the capacity of the banking system to lend to other companies, including

small and medium-sized enterprises, which rely on banks. Last week,

the Bank of England boosted this capacity by:

launching a new Term Funding Scheme

with additional incentives for lending to SMEs (TFSME). This will, over

the next 12 months, offer four-year funding to banks of at least 5% of

participants’ stock of real economy lending at interest rates at, or

very close to, Bank Rate. Additional funding will be available for

banks that increase lending, especially to small and medium-sized

enterprises (SMEs).

reducing the UK countercyclical

capital buffer rate to 0% of banks’ exposures to UK borrowers with

immediate effect. This extended banks’ capacity to lend to businesses by

up to £190bn.

Taken together the actions announced by HM

Treasury and the Bank of England will help UK businesses and households

to bridge a temporarily difficult period and thereby to mitigate any

longer-lasting effects of Covid-19 on jobs, growth and the UK economy.

HM Treasury and the Bank will take all

further necessary steps to support the UK economy and financial system,

consistent with its statutory responsibilities.

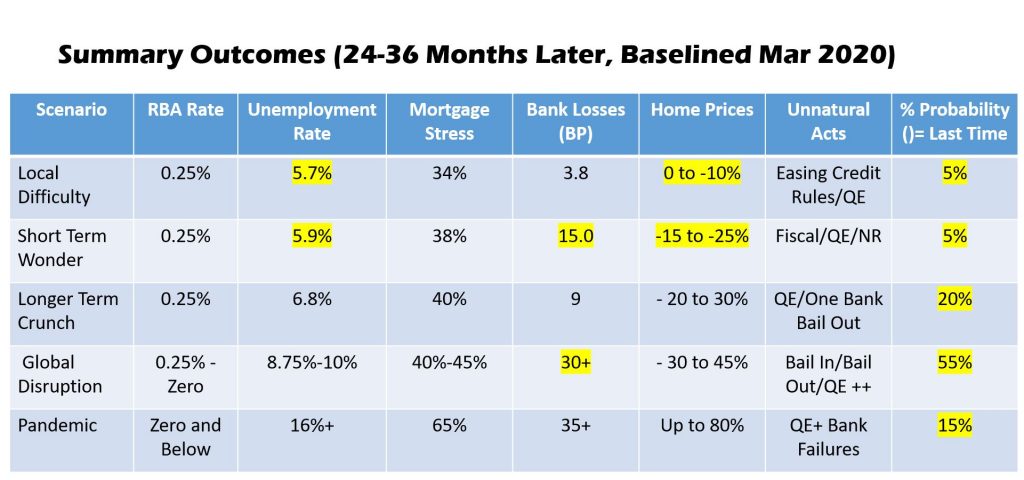

We have updated our scenarios, driven from our core market models.

The drivers are rising unemployment, and business failure thanks to the impact of the virus. We discussed these scenarios in our live stream event last night. This is the full version with live chat. The show starts formally at 32 minutes.

We estimate that mortgage stress is set to rise significantly in the months ahead as household cash-flows are interrupted.

Alternatively we have also released a shorter edited version, without chat here: