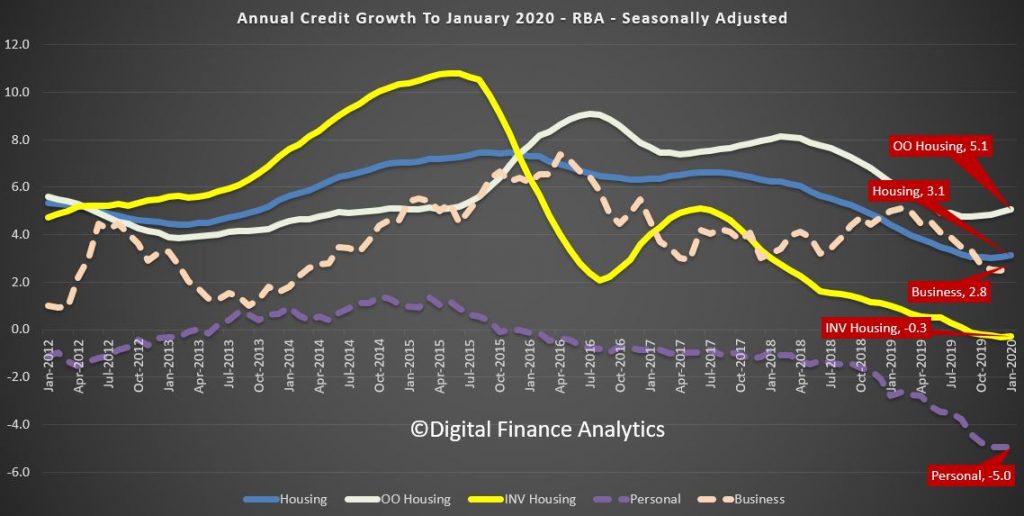

The latest data from the RBA, the credit aggregates to end January 2020 were released today. Total credit grew by 0.3% last month, compared with 0.2% in December. This gives an annual rate of 2.5%, compared to 4.2% in January 2019.

The annual series shows that owner occupied housing rose 5.1%, investment housing lending is down 0.3% and overall housing at 3.1%, up from a low of 3% in November, so hardly stellar.

Business credit rose by 0.5% in January, compared with 0.2% in December, giving an annual rise of 2.8% compared with 5% a year ago. That was the biggest mover.

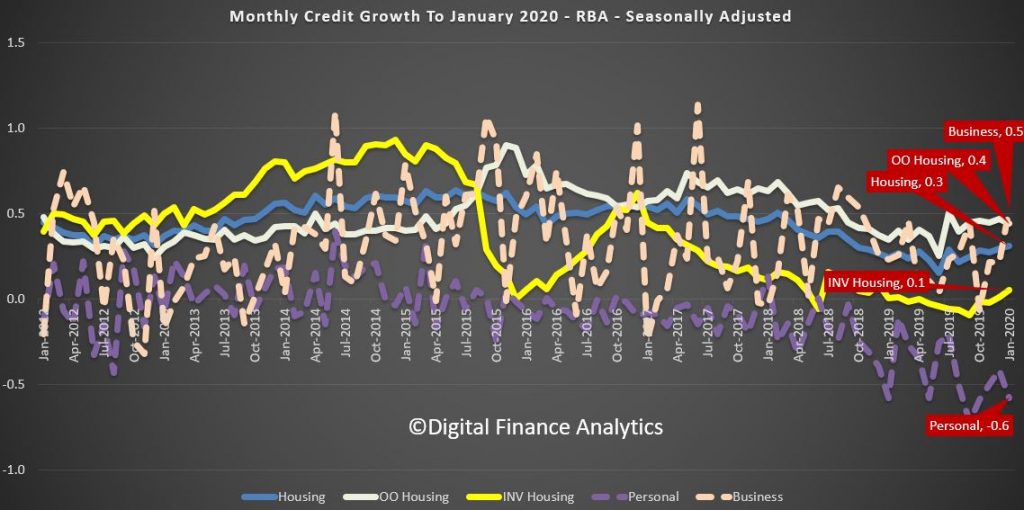

The monthly series are always noisy, and the RBA seasonally adjusts the results without explanation, so we have to take their word for the results.

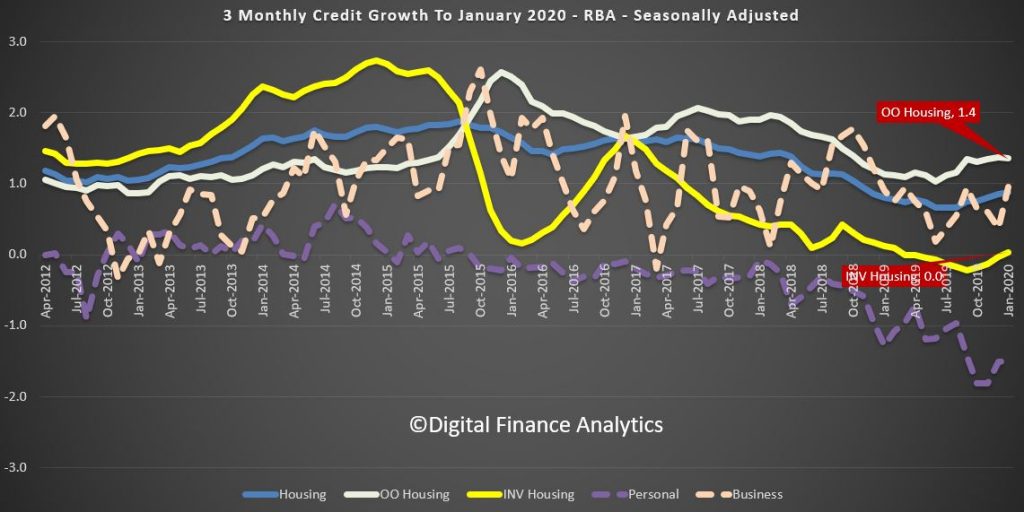

The 3 month rolling series shows a small uptick in investment lending to zero percent, while owner occupied lending was up to 1.4%, so weak growth only. Business was a little stronger, and personal credit fell at a slower rate of minus 1.5%.

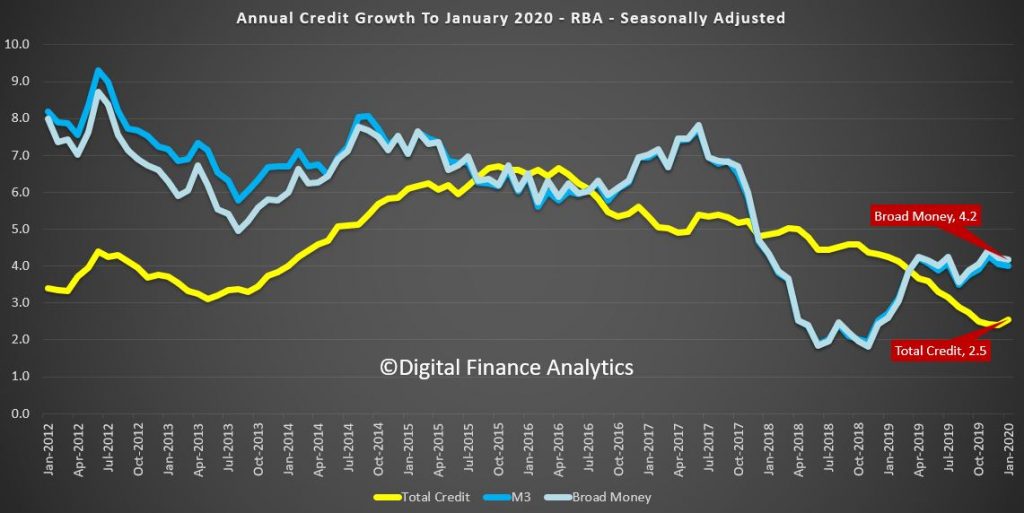

The broader credit and money supply metrics showed that over the past year total credit rose at 2.5%, slightly higher than last month, while broad money fell a little to 4.2%

Overall the credit weakness continues to bite. We will see what the new loan data tells us when its released in a couple of weeks, as the net weak numbers could be masked by larger repayments from households seeking to deleverage in these uncertain times.

Finally the RBA notes:

All growth rates for the financial aggregates are seasonally adjusted, and adjusted for the effects of breaks in the series as recorded in the notes to the tables listed below. Data for the levels of financial aggregates are not adjusted for series breaks, and growth rates should not be calculated from data on the levels of credit. Historical levels and growth rates for the financial aggregates have been revised owing to the resubmission of data by some financial intermediaries, the re-estimation of seasonal factors and the incorporation of securitisation data. The RBA credit aggregates measure credit provided by financial institutions operating domestically. They do not capture cross-border or non-intermediated lending.

Since the July 2019 release, the financial aggregates have incorporated an improved conceptual framework and a new data collection. This is referred to as the Economic and Financial Statistics (EFS) collection. For more information, see Updates to Australia’s Financial Aggregates and the July 2019 Financial Aggregates.

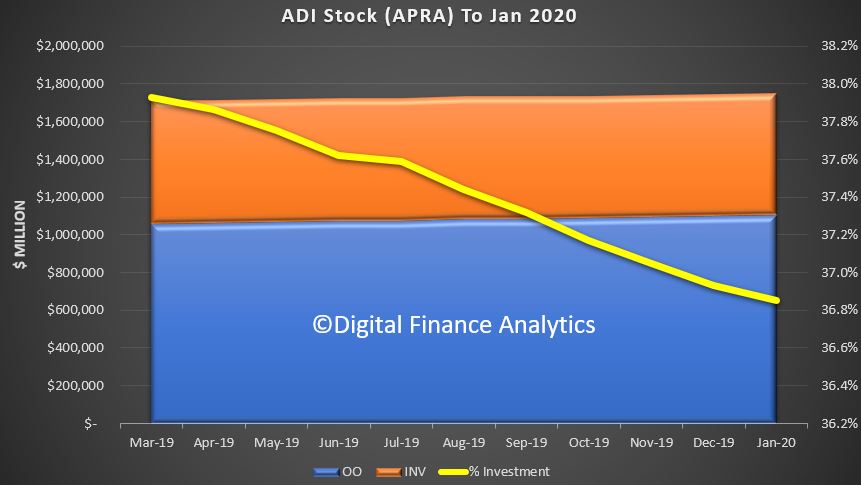

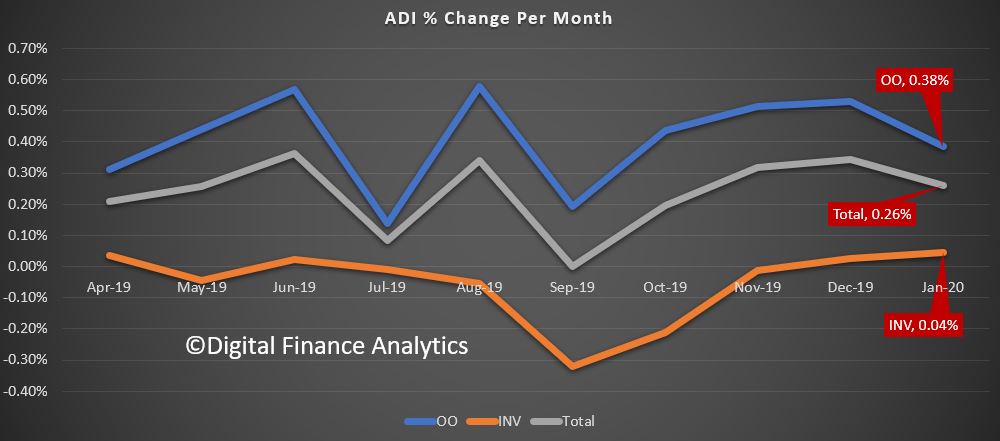

APRA released their monthly stats showing total reported balances for each bank to the end of January 2020.

Total balances grew by 0.26%, to $1.75 trillion dollars, with loans for owner occupation up 0.38%, to $1.1 trillion dollars and investment loans up 0.04% to $0.64 trillion dollars. Investment loans made up 36.9% of the portfolio.

These are net balances, after repayments and new loans, and refinancing between banks.

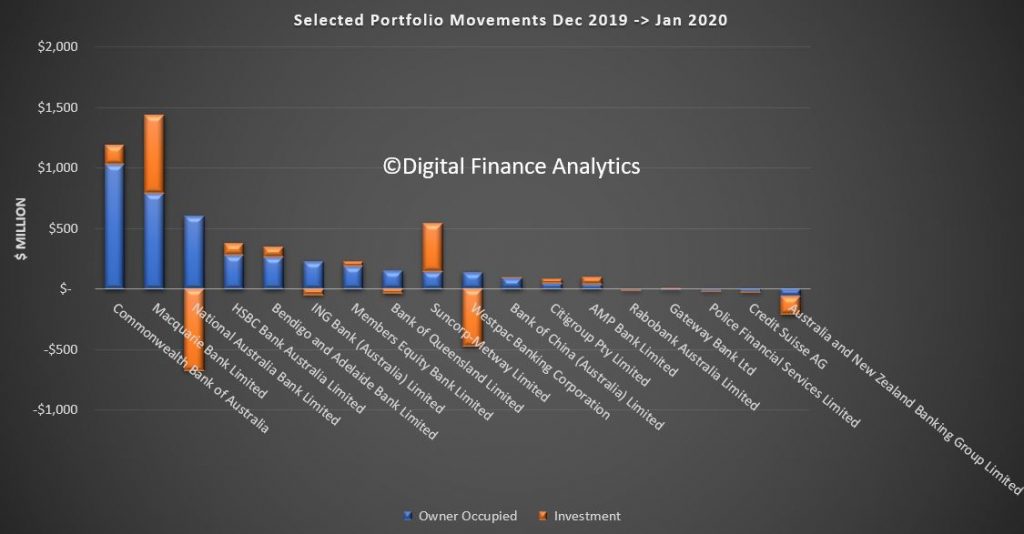

The individual movements between banks shows that CBA and Macquarie Bank are leading the growth, while NAB, and Westpac dropped investment loan balances, ANZ dropped both types, while Suncorp accelerated their investment lending. Macquarie still leads in investment lending however.

This suggests ongoing weakness in credit growth – and we will examine the RBA data shortly, also out today. But clearly individual lenders are executing different strategies, and the portfolio changes highlight the net impact.

You may suddenly be getting a security error on our site. This is caused by a hosting SSL failure. They are working on the issue, which is impacting many sites being hosted, not just DFA.

The education sector in Australia is highly leveraged towards China.

As a result of the current travel ban their finances are at risk. So they are finding ways around the ban, with the approval of the Government, who is trading off public health against economics. In other words, our health is being put at risk.

I discuss this troubling episode with Salvatore Babones, Adjunct Scholar at the Centre for Independent Studies, and Associate Professor University of Sydney.

Australia’s six dual-sector universities are calling on federal, state and territory governments to work together to implement landmark recommendations reforming the tertiary education system – in order to better meet the needs of students and the changing world of work.

The plea for action will be made during a speech today at Universities Australia’s Higher Education Conference. Australia’s economy depends on workers with future-ready skills and access to retraining throughout their working lives. According to recent figures, of the 1.1 million jobs to be created by 2021, 96 per cent will require skills acquired through both higher education and vocational education training (VET).

Over ten years since the Bradley Review proposed a more coherent tertiary education system, connections between the vocational and higher education sectors have instead weakened due to increasingly entrenched differences between systems of governance, funding and regulation.

In 2019, the Australian Government released the final report of The COAG Review of the Australian Qualifications Framework which recognised that students need more flexibility in combining vocational and higher education to access skills and knowledge they need to be successful. Australia’s six dual-sector Vice-Chancellors said that federal, state and territory governments must begin to implement the recommendations of this crucial review as a matter of urgency.

The Vice-Chancellors outlined a path forward in their 2019 report, Reforming Post-Secondary Education in Australia, which called for:

reforms to the Australian Qualifications Framework (AQF), particularly to support learner-centred pathways across the continuum of AQF qualifications;

modernisation of VET qualifications so competencies focus on broad and future skills needs;

a coherent funding framework for higher education and VET, spanning the roles of the Commonwealth, states and territories; and

extension of work-based learning, including apprenticeships, into new industries and occupations in both VET and higher education through partnerships with firms, industries and the labour movement.

“We need policy reforms that create greater connections between vocational and higher education systems, which in turn will create a more coherent, comprehensive and modern set of opportunities for Australian students,” said spokesperson for the Vice-Chancellors, Professor Peter Dawkins.

“The AQF review was a great start to this reform agenda and we were delighted with the response from the Federal Minister of Education. We now need the Australian Government, and all state and territory governments, to get behind it through COAG. Setting up the necessary government body to implement the recommendations as a staged approach would be a great start.

“We need to act now to safeguard Australia’s economy and create new opportunities for our workforce,” Professor Dawkins said.

The Vice-Chancellors of Australia’s six dual-sector universities are:

Professor Simon Maddocks – Charles Darwin University

Professor Nick Klomp – CQ University

Professor Helen Bartlett – Federation University

Mr Martin Bean – RMIT University

Professor Linda Kristjanson – Swinburne University of Technology

The New Zealand Reserve Bank has launched a new future-proofed payment settlement system, replacing New Zealand’s inter-bank settlement system and central securities depository.

The new platform replaces a

20-year-old system with two separate systems, ESAS 2.0 and NZClear 2.0. The new

platform comprises the Real Time Gross Settlement (RTGS) and Central Security

Depository (CSD) applications supplied by SIA – a European technology and

banking infrastructure leader and its wholly owned subsidiary Perago.

Infrastructure support services are supplied by Datacom Systems Limited.

The extent of change is

significant, says Assistant Governor/Chief Financial Officer Mike Wolyncewicz.

“Every day, transactions

with a value of more than $30 billion are settled, so there has been a focus on

getting this right, and not rushing out a replacement until we were confident

that it was ready.

“The buy-in from the

industry has been fantastic. This week’s successful changeover is the result of

months of rigorous testing and we appreciate the cooperation of the system’s

key users.”

The Reserve Bank’s payment

settlement system is used by 57 member organisations including banks,

custodians, registries and brokers. This equates to around 600 users of the

system, from New Zealand, Australia and Asia.

“Our members now have access

to far more modern, future-proofed and leading edge systems for them to manage

their day-to-day interactions with the Reserve Bank,” Mr Wolyncewicz says.

The systems replacement

follows a strategic review of the incumbent payment and settlement systems

operated by the Reserve Bank, completed in 2014 in anticipation of the need to

align with today’s operational and technological standards.

The Australian government touts compulsory income management as a way to stop welfare payments being spent on alcohol, drugs or gambling. Via The Conversation.

The Howard government introduced the BasicsCard

more than a decade ago. About 22,500 welfare recipients now use it,

mostly in the Northern Territory. Now the Coalition government has big

plans for a more versatile Cashless Debit Card, trialled on about 12,700 people in four regional communities in Western Australia, South Australia and Queensland.

The 2016 Indue Cashless Debit Card.

indue.com.au

These trials aren’t complete, nor the findings compiled, but a string of senior ministers, including Prime Minister Scott Morrison, have indicated they are already sold on expanding the program.

Over the past year we have conducted the first independent, multisite study

of compulsory income management in Australia. It has involved 114

in-depth interviews at four sites: Playford (BasicsCard) and Ceduna

(Cashless Debit Card) in South Australia; Shepparton (BasicsCard) in

Victoria; and the Bundaberg and Hervey Bay region (Cashless Debit Card)

in Queensland. We also collected 199 survey responses from around

Australia.

Proponents of compulsory income management

champion its potential to “provide a stabilising factor in the lives of

families with regard to financial management and to encourage safe and

healthy expenditure of welfare dollars”, as the then social services

minister, Paul Fletcher, said in March last year.

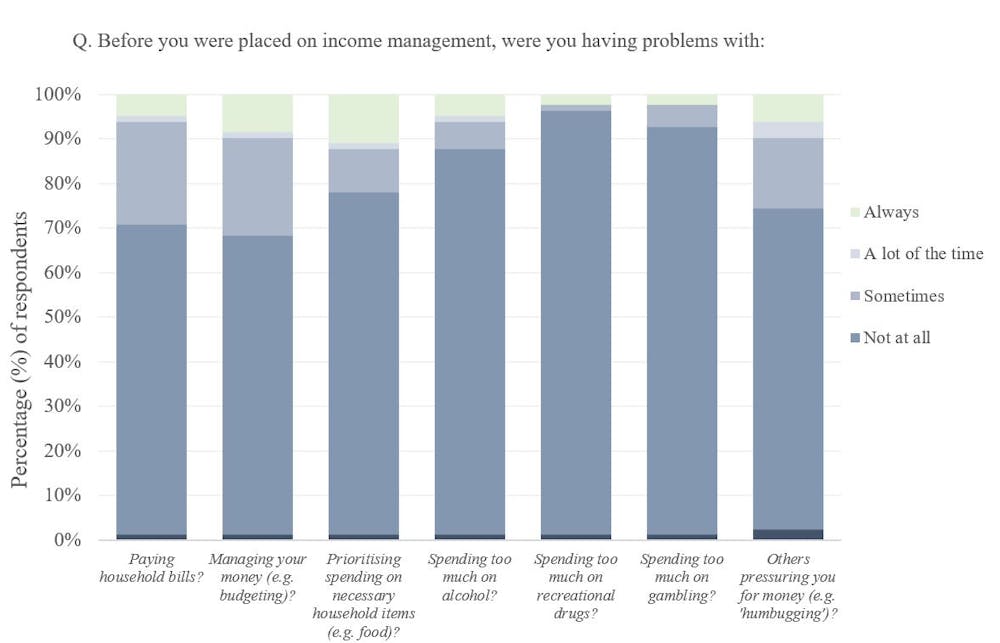

Our study found some individuals

experience these benefits. But most face extra financial challenges.

These include not having enough cash for essential items, being unable

to shop at preferred outlets, being unable to buy second-hand goods, and

cards being declined even when they are supposed to work.

Survey respondents reported a range of challenges related to compulsory income management.

Hidden Costs: An Independent Study into Income Management in Australia

In Playford, Jacob* told us about being on

the BasicsCard, which can only be used with merchants that have agreed

to not allow cardholders to buy excluded goods.

The limits on where he could shop made it harder for him to manage his finances.

“I couldn’t make decisions about saving

money,” he told us. He and his wife used to catch the train to shop at

the Adelaide markets, for example, but vendors there couldn’t take the

BasicsCard.

The Cashless Debit Card is intended to

overcome the limitations of the BasicsCard. It’s like a debit card

except it can’t be used to withdraw cash or at businesses that sell

prohibited items.

But Emma*, a single mother in the

Bundaberg and Hervey Bay area, told of her struggles to make basic

purchases using the card. It often failed – even at businesses that

purportedly accepted it – and her family went without. She also felt

excluded from the markets and second-hand retailers where she used to

shop.

Her greatest stress, however, was rent.

Emma* said she had always been on time with rental payments until the

Cashless Debit Card. She described one occasion when, two days after

paying the rent, the money “bounced back” into her account. When she

rang the card’s administrator (card payment company Indue), she was told: “It’s just a minor teething issue, just keep trying.”

The extra stress from “worrying about

which payments were going to get paid” was considerable. Others shared

similar experiences.

Social (dis)integration

Supporters of compulsory income management

claim it brings people back into the community by combating addiction

and encouraging pro-social behaviour and economic contribution. As

federal Attorney-General Christian Porter said in 2018:

“The cashless debit card can help to stabilise the lives of young

people in the new trial locations by limiting spending on alcohol, drugs

and gambling and thus improving the chances of young Australians

finding employment or successfully completing education or training.”

However, our study found the card can also

stigmatise and infantilise users – pushing people without these

problems further to the margins.

One of the problems is that compulsory

income management is routinely applied based on where a person lives and

their payment type, and not on any history of problem behaviour. The

large majority of our respondents indicated they did not have alcohol,

drug or gambling issues.

The majority of survey respondents had been managing finances well before compulsory income management.

Hidden Costs: An Independent Study into Income Management in Australia

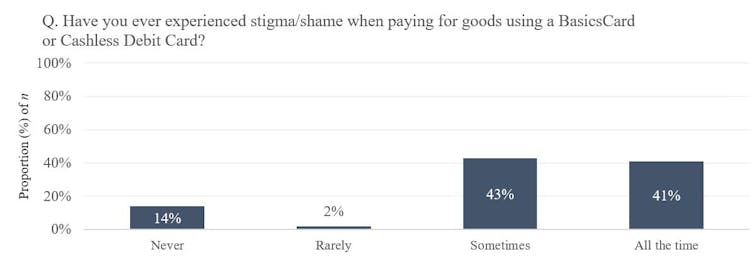

But as Ray* in Ceduna explained, having the card meant others viewed him as a problem citizen.

I’m embarrassed every time I have to use

it at the supermarket, which is about the only place I do use it. I sort

of look around and see who’s behind me in the queue. I don’t want

anybody to see me using it.

This was a common experience across the interview sites.

Maryanne* in Shepparton told about being judged for shopping for groceries with her BasicsCard.

I got called a junkie and I said: ‘I’m not

a junkie, do you see any marks or anything?’ They were like: ‘No, but

you have a BasicsCard.’ I said: ‘What’s that got to do with it?

Centrelink gave it to me. I can’t do nothing.’

Stigma was a common concern among survey participants.

Hidden Costs: An Independent Study into Income Management in Australia

A path forward

The overwhelming finding from our study is

that compulsory income management is having a disabling, not an

enabling, impact on many users’ lives. As the policy has been extended,

more and more Australians with no pre-existing problems have been caught up in its path.

This does not mean a genuine voluntary

scheme could not be maintained, but it would need to sit alongside

evidence-based measures to tackle poverty.

Names have been changed to protect individuals’ privacy.

Authors: Greg Marston, Head of School, School of Social Science, The University of Queensland; Michelle Peterie, Research Fellow, The University of Queensland; Phillip Mendes, Associate Professor, Director Social Inclusion and Social Policy Research Unit, Monash University; Zoe Staines, Research fellow, The University of Queensland

In mid-February around 1-in-6 Australian businesses (15%) have already been affected by the coronavirus, also known as COVID-19. This new threat to business comes after over a quarter of Australian businesses (28%) said they have been affected by the extensive bushfires over the last few months according to a special Roy Morgan Snap SMS Survey of 1,170 Australian businesses.

Coronavirus hits Education,

Manufacturing and Wholesale industries hard

A little over a week after the Australian

Government stopped all direct commercial flights to China in early February the

coronavirus (COVID-19) is already striking several industries.

Around two-fifths of Manufacturers are already

reporting being affected and closely followed by a third of Education &

training businesses and those in the Wholesale industry.

Other industries to already be feeling the

effects of the coronavirus include Accommodation & Food services which

includes travel and tourism businesses, Community services, Administrative

& Support services and Property & Business services.

Respondents to the survey described in their own words the impact the coronavirus was already having and these responses fell into a few broad categories including the issue of workers, or students, being quarantined and kept away from work/study; the impact on supply lines for the import or export of goods and parts to and from China; the decline in forward bookings from Chinese tourists and cancellations by customers in Asia as well as the general hit to confidence which includes a weaker stock-market as well as lower foot traffic in stores due to a combination of the aforementioned.

Bushfires/Floods strike

Tourism, Retail and Property & Business services industries

A deeper analysis of the industries most

heavily impacted by the bushfires/floods shows that over 40% of businesses in

the Accommodation and Food services sector, which includes travel and tourism,

say they have been affected either ‘A great deal’ or ‘Somewhat’.

Around a third of businesses in the Retail and

Property & Business services industries have been affected while there have

also been disproportionately large impacts on Manufacturing, Transport, Postal

and Warehousing, Public administration & defence, Education & training

and Recreation & personal.

Businesses in the East Coast States of Victoria

(39%), NSW (31%) and Queensland (23%) have been the most heavily affected by

the bushfires/floods. In contrast only 14% of businesses in Tasmania and 11% of

businesses in both South Australia and Western Australia have been affected at

all.

Further details on how the recent bushfires

affected Australian businesses can be found here.

Roy Morgan Chief Executive Officer

Michele Levine says the long bushfire season has finally ended with

drought-breaking rains in recent weeks however the new threat of coronavirus is

a growing threat to the recovery of the Australian economy:

“The new threat of coronavirus (COVID-19) that

has emerged in recent weeks is already hitting the business community in much

of Australia – and in several states including Western Australia, South

Australia and Tasmania – has already had a bigger impact than the bushfires..

“The Australian Government halted all flights

from China in early February and that ban is still in place on a week-to-week

basis as the spread of COVID-19 in China is being monitored.

“Already feeling the effects are Manufacturing

businesses which rely on China for the importation of many parts, Education

& training – China is the largest source of foreign students in this $35+

billion industry and Wholesale which imports many goods manufactured in China

for sale at Australian retail outlets.

“The Tourism industry is also in the firing

line as Chinese tourists (the largest inbound tourism market) are barred from

visiting Australia until further notice. In addition, the all-round impact of

the coronavirus is having an increasing impact on general confidence which in

turn has a negative effect on retail foot traffic. We’ve already seen

restaurants close due to the decline in customers particularly in places

heavily reliant on Chinese-owned businesses such as Chinatown.

“It is hard to predict exactly how the full

impact of the coronavirus will be felt in the Australian economy over the next

few months although it’s safe to say that the negative economic ‘shock’ is set

to grow after outbreaks of the virus have been seen in such diverse places as

South Korea, Iran and Italy over the last few days.”

Businesses affected by the bushfires/floods cf. coronavirus

around Australia by State

Source: Roy Morgan Special

Snap SMS Poll of Australian businesses in February 2020, n=1,170. Base:

Australian businesses.

Australia’s

first neobank, Volt,

is partnering with Australia’s largest global retailer, the Cotton On Group,

to introduce team members and customers to the Volt experience.

It

will be the first partnership of this type between a neobank and major retailer

in Australia, putting both companies at the forefront of digital innovation in

the retail banking sector and taking an important step to support the financial

literacy and good spending and saving habits of millennials.

Cotton

On team members, and in time Cotton On Perks members, will be introduced to the

Volt Savings Challenge in an effort to help them create better financial

habits. The Volt Savings Challenge encourages customers to set targets and

sends gentle reminders for weekly saving, tracking their progress over a 6 week

period by which time the savings ‘habit’ should be embedded behaviour.

According to Steve Weston, CEO & Co-Founder of Volt, the partnership is also heavily centered on a deep philosophical and values alignment between the two customer-focused companies.

CEO Steve Weston and the Volt Team

“Both

Volt and the Cotton On Group are built upon a foundation of delivering great

value to customers, a foundation that starts with a commitment to genuinely solve

customer pain points whilst dealing ethically and transparently with customers,

staff, and suppliers,” said Mr. Weston. “We feel really comfortable partnering

with a company that’s as customer-focused as we are.

“The

partnership will help us continue to show millions of Australians how to

quickly develop and improve their savings and spending habits with Volt. We

recently introduced to our waitlist a “no catches” 2.15 per cent variable

interest rate, which complements our savings challenges that are designed to

help people become financially healthy and masters of their own money.

“We

look forward to bringing this experience to many more Australians in the coming

years,” Mr Weston concluded.

The

Cotton On Group is partnering with Volt to bring a roadmap of innovation and

value to customers in Australia by introducing banking services tailored to

millennials that provide a supportive environment for healthy savings habits,

said Brendan Sweeney, General Manager, E-Commerce, who leads the Group’s digital

and loyalty strategy.

“Our

millennial team and customers are highly engaged, digital-first and have told

us that they are looking for trusted partners who can help them achieve their

financial goals,” said Mr. Sweeney.

“We

really like the Volt approach of simplicity, trust, and great value coupled

with a digital customer experience designed to help customers understand their

finances and achieve their goals. We look forward to making the Volt experience

available to our team members and customers over the coming months.”

The

Cotton On Group partnership follows others Volt has signed including PayPal.

The partnership strategy is an important element in delivering competition to

the banking sector.