Australians saved rather than spent most of the budget tax cuts, almost doubling the proportion of household income saved, leaving spending languishing. Via The Conversation.

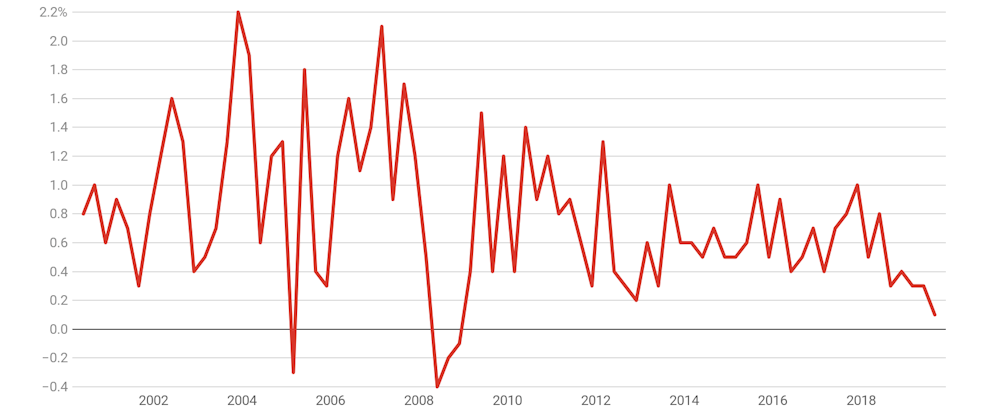

The September quarter national accounts show that in the first three months of the financial year real household spending grew by just 0.1%, the least since the global financial crisis.

Over the year to September, inflation-adjusted spending grew by a

mere 1.2%, also the least since the financial crisis. Australia’s

population grew by 1.6% in that time, meaning the volume of goods and

services bought per person went backwards.

Separate figures released by the Federal Chamber of Automotive Industries on Wednesday show November new car sales were down 9.8% on November 2018.

By the end of November the Tax Office had issued more than 8.8.

million tax refunds totalling A$25 billion, 30% more than a year before.

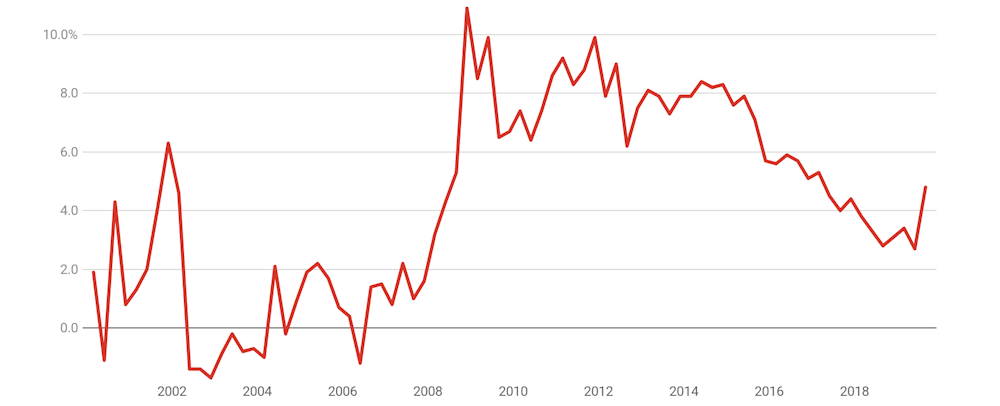

Instead of being largely spent, they were mostly saved, pushing up

the household saving ratio from 2.7% to 4.8%, its highest point in more

than two years.

Treasurer Josh Frydenberg put the best face on the result, saying

whether they had been spent or saved, the cuts had put households in a

stronger position.

The government’s goal has always been to put more money into the

pockets of the Australian people, and it’s their choice as to whether

they spend or save that money

Separately calculated retail figures show that in the three months to September the volume of goods and services bought fell 0.1%.

The disposable income households had available to spend grew an

outsized 2.5%, driven by what the Bureau of Statistics said were the budget tax cuts.

Growth at GFC lows

The Australian economy grew just 0.4% in the three months to

September, down from 0.6% in the June quarter, and 0.5% in the March

quarter.

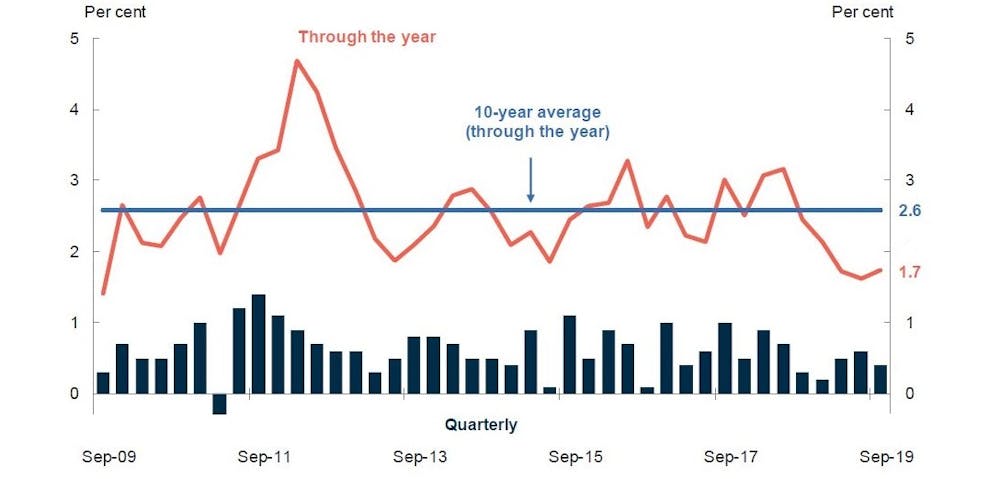

Over the year to September it grew 1.7%, well short of the budget forecasts, which in year average terms were 2.25% for 2018-19 and 2.75% for 2019-20.

After taking account of population growth, GDP per person grew not at

all in the September quarter. Over the year to September living

standards grew a bare 0.2%.

Gross domestic product per hour worked, which is a measure of

productivity, fell 0.2% during the quarter and fell 0.2% over the year.

Company profits were up 2.2% in the quarter and 12.7% over the year.

Wage and superannuation payments grew at about half those rates: 1.2%

and 5.1%.

Housing investment was down 1.7% over the quarter and 9.6% over the year.

What household spending growth there was was concentrated on

essentials, led by health and rent. So-called discretionary or

non-essential expenditures fell, led down by spending on cars, dining

out and tobacco.

Consumption growth by category, quarterly

Treasury definitions of discretionary and non discretionary spending.

ABS, Commonwealth Treasury

The economy was kept afloat by a surge in government spending. It

grew 0.9% in the quarter and 6% over the year. Growth in government

spending and investment together accounted for 0.3 of the quarter’s 0.4

points of economic growth.

Government and mining to the rescue

Mining production grew 0.7% over the quarter and 7.4% over the year. A

mining-fuelled surge in exports (which eclipsed imports for the first

time since the 1970s) contributed almost as much to economic growth as

government spending.

Drought-affected farm production fell 2.1% over the quarter and 6.1% over the year.

Business investment fell 4% in the quarter and 1.7% over the year,

led down by a 7.8% fall in mining investment in the quarter and a 11.2%

fall over the year, as liquefied natural gas projects came to

completion. Non-mining investment fell 0.4%.

Asked whether the December budget update would contain tax measures

designed to boost business investment, the treasurer said he was in

discussions with business. The update is expected in the week before

Christmas.

There’s little evidence in today’s figures of the “gentle turning point” spoken about hopefully by the Reserve Bank governor as recently as Tuesday.

If things don’t pick by the bank’s first board meeting for the year in February, it is a fair bet it will cut its cash rate again. By then it will know what the treasurer did (or didn’t) do in the budget update and whether we decided to spend over Christmas.

Author: Peter Martin, Visiting Fellow, Crawford School of Public Policy, Australian National University

John Adams commemorates December 3rd, a fateful day in Australian history, yet an event which marks an important point in the development of democracy. Lest we forget.

The Eureka Stockade, rebellion (December 3, 1854) was when gold prospectors in Ballarat, Victoria, Australia sought various reforms, notably the abolition of mining licenses and clashed with government forces. The rebels’ hastily constructed a fortification in the Eureka goldfield.

Slowing global economic growth, trade tensions and geopolitical risks will lead to subdued demand growth in global shipping in 2020, Fitch Ratings says in a new report. The sector outlook remains negative. Although all shipping segments have demonstrated more prudent capacity growth in recent years, which supported a better supply-demand balance, a longer record of responsive capacity management is needed to improve the sector’s resilience.

Free global trade is vital for shipping

as about 80% of world trade in goods is carried by the international

shipping industry. The main sector risk is that protectionist measures

may escalate into a protracted trade war and damage the prospects for

global trade and GDP growth. While some upside is possible if the trade

tensions between the US and China ease, the downside risks, including

expected slower GDP growth in China, soft trade growth and Brexit

uncertainty, will continue to weigh on demand.

The sector will

also need to cope with rising costs related to new regulation capping

sulphur content in marine fuel (International Maritime Organisation

(IMO) 2020), which is likely to negatively affect shippers’ credit

metrics. This regulation will probably increase operating costs (if

shippers choose to use more expensive low-sulphur fuel) and/or capex (if

they install scrubbers that remove sulphur from the exhaust or purchase

new LNG-fuelled vessels). Shippers are unlikely to fully pass through

all the associated costs to customers due to their limited bargaining

power in the oversupplied market. We expect most shipping companies to

use low-sulphur fuel.

We forecast global container volumes to

grow by about 2.5% in 2020. While this represents a small increase from

2019, it is well below the average growth rate of about 4.5% over the

past eight years. Trade restrictions, if they remain unresolved, are

likely to have a negative impact on global container volumes of about 1%

in 2020, according to AP Moller-Maersk. We expect better capacity

management in global container shipping with fleet capacity increasing

by 3.3% in 2020, slower than 3.6% in 2019. Container freight rates in

2020 are likely to remain at levels similar to those in 2019.

We

expect dry-bulk trading volumes to grow by 3% in 2020, up by more than

1.5pp on 2019. This improvement will be driven by higher iron ore and

other commodities volumes. Iron ore volumes are expected to slowly

recover following the Vale dam incident in Brazil and challenging

weather at Australian ports in 2019. Fleet additions are likely to match

this growth in volumes, and freight rates are likely to increase as

dry-bulk shippers will be better positioned to pass on some of the

higher fuel costs.

Global tankers’ supply and demand are likely

to grow by 2.5% and 3.5%, respectively, in 2020, supporting a better

supply-demand balance. This will help freight rates to stay at levels

comparable to annual averages in 2019, which represents a recovery from

their troughs in the middle of 2018. The impact of IMO 2020 on tanker

shipping companies is likely to be mixed, as rising compliance costs may

be mitigated by increased tanker demand to transport compliant fuel.

However, lingering trade and geopolitical tensions and political risk

may depress long-term tanker demand

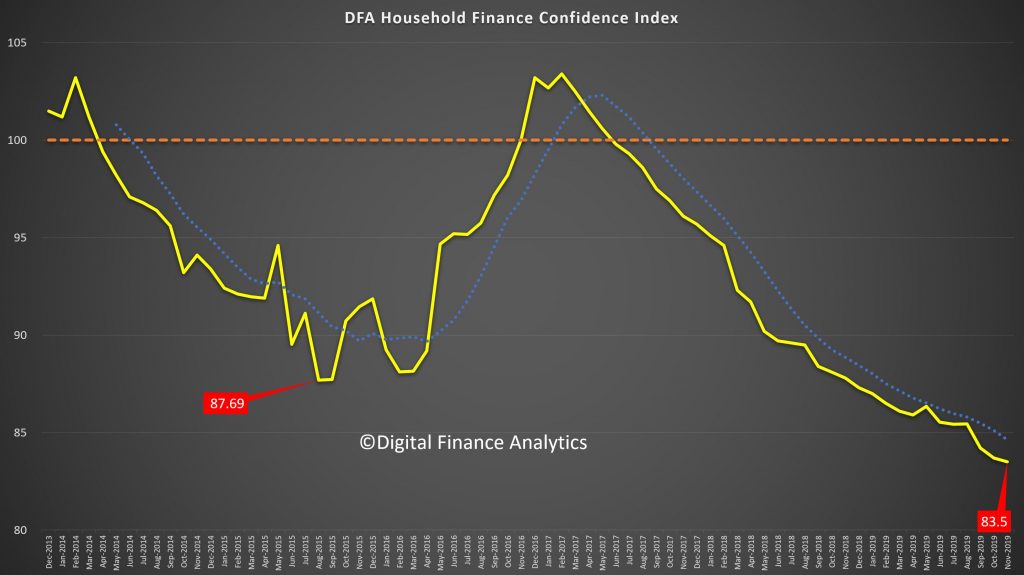

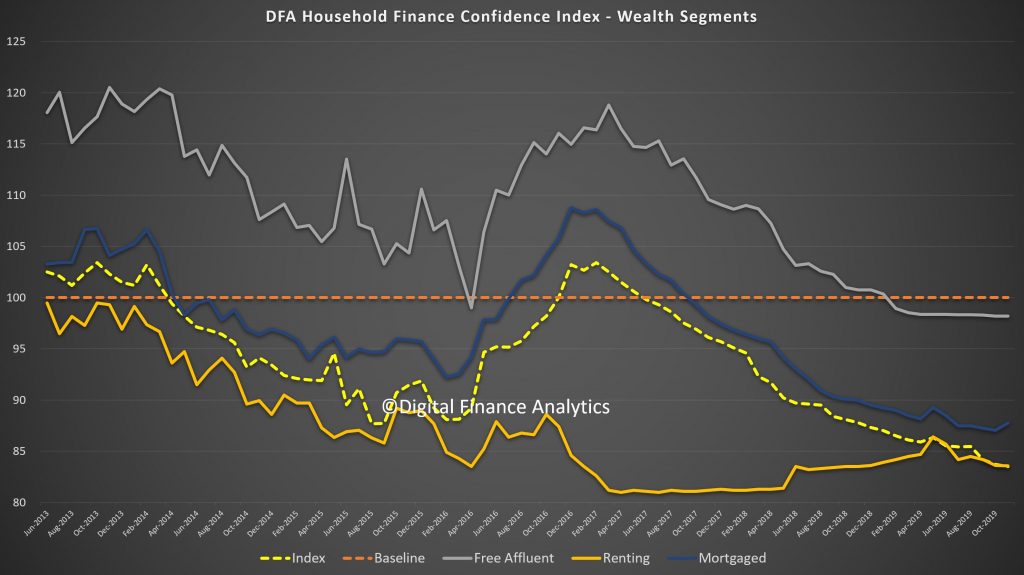

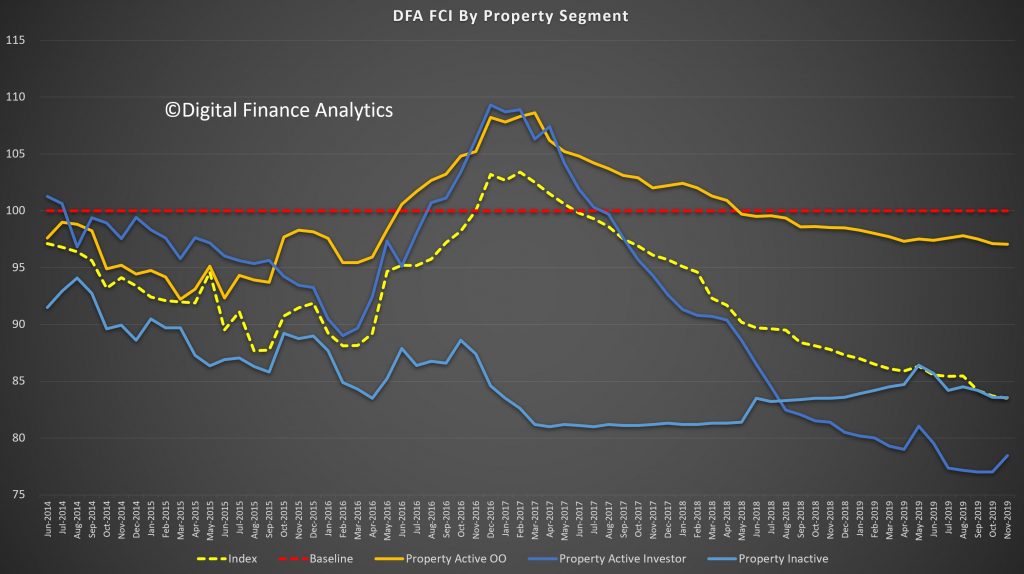

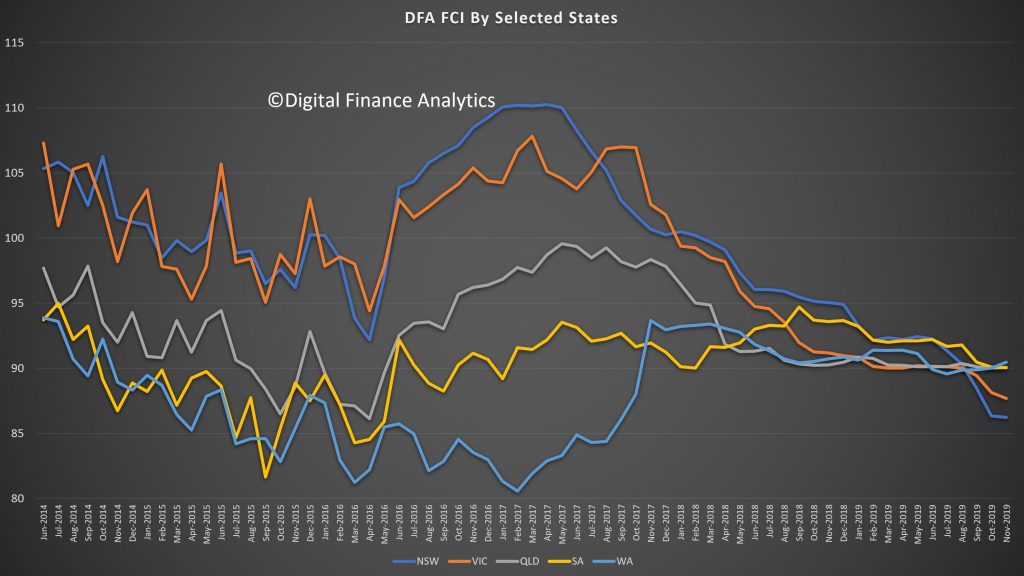

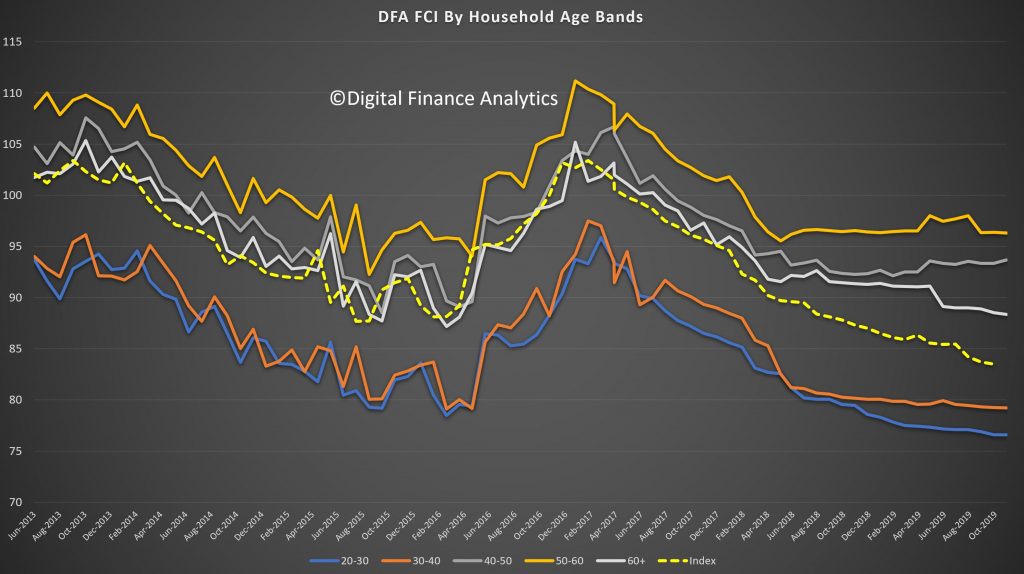

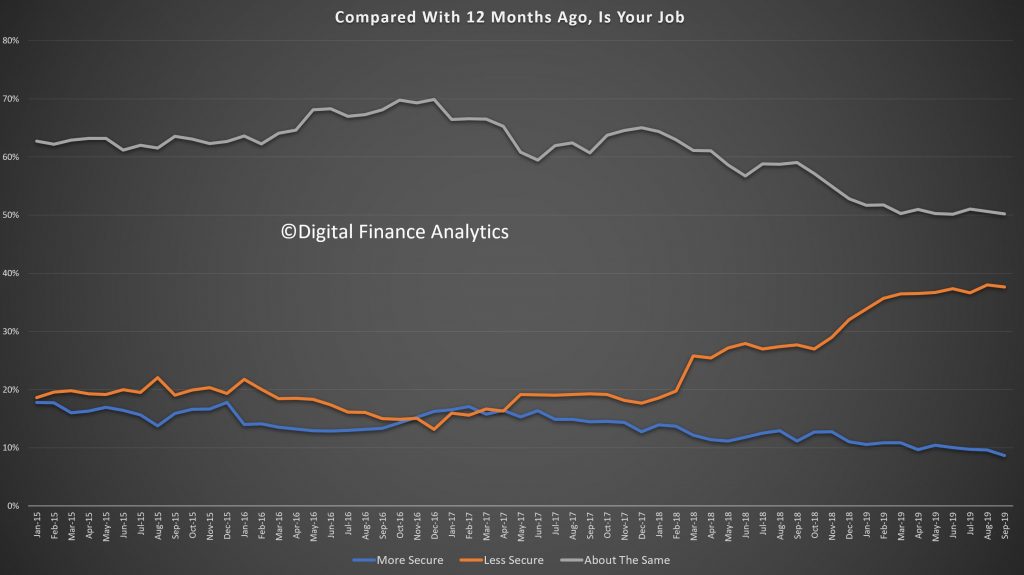

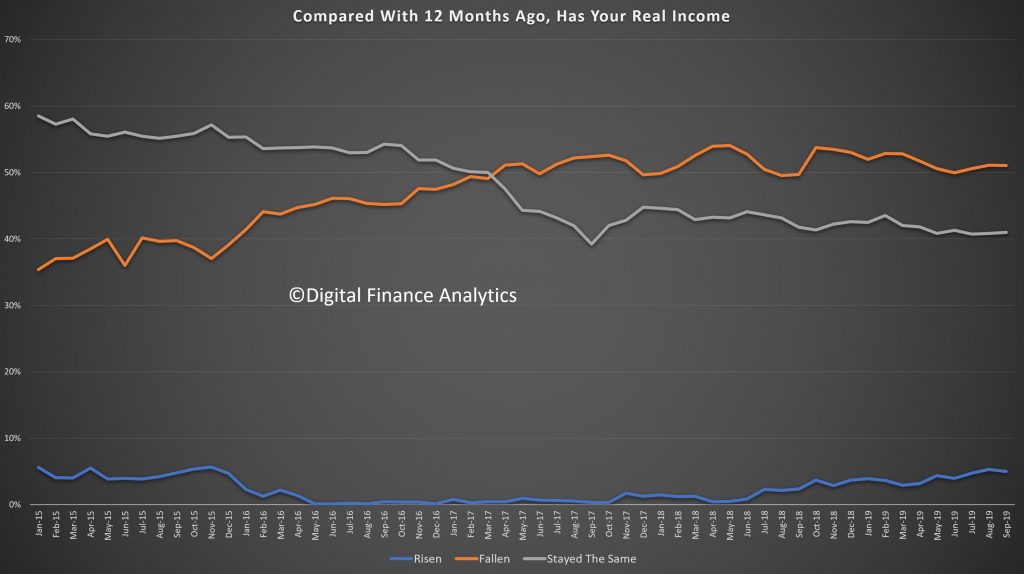

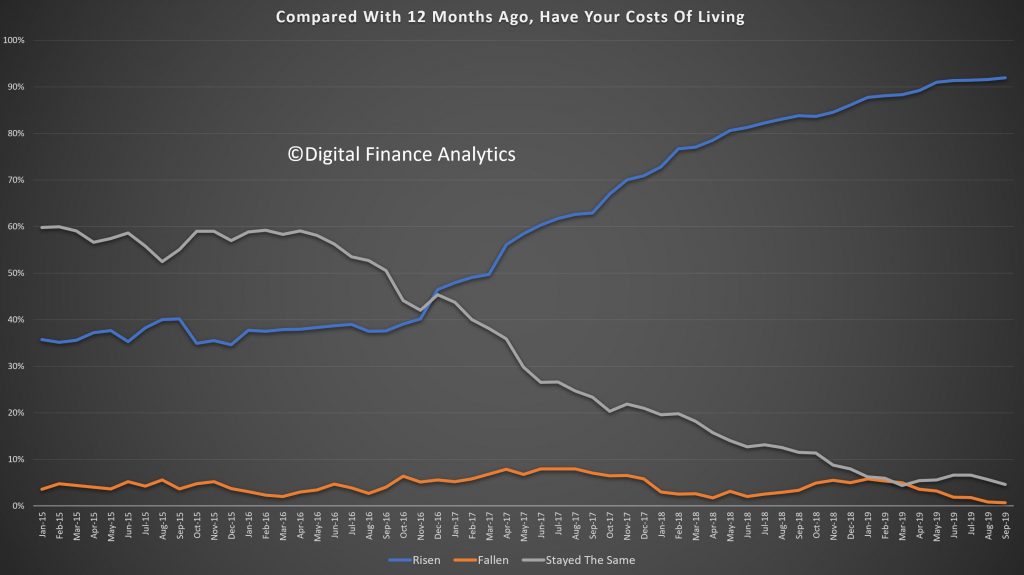

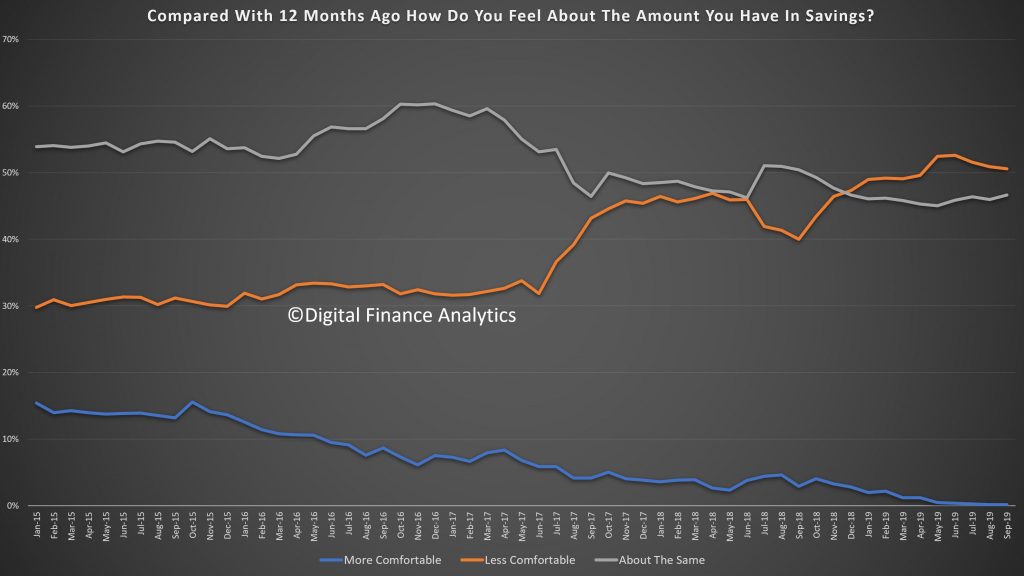

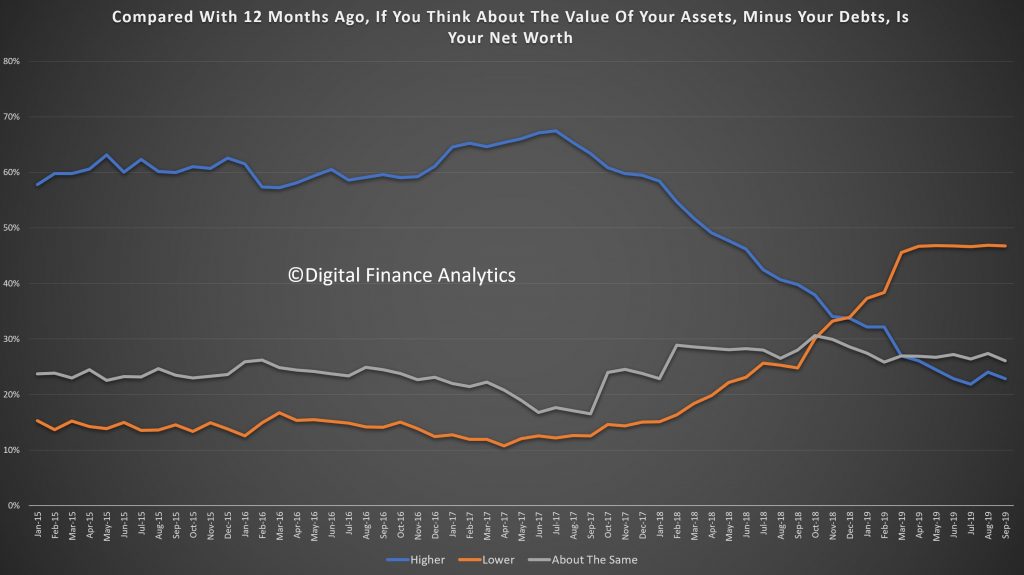

We continue to release the data from our household surveys to end November 2019. Today we look at our Household Financial Confidence Index, which examines how households are feeling about their financial status, relative to a year ago.

The index dropped again to 83.5, which is a new low in the series, and well below the previous 87.69 back in 2015. This level of concern suggests households will be keeping their wallets firmly in their pockets, so expect more retail weakness and household consumption easing lower ahead. The one “bright” spot was that more households are now believing their net worth is higher, thanks to the perceived recovery in home prices, and recent stock market highs, though offset by lower returns on deposits, flat incomes in real terms and rising costs. Recent rate cuts and tax refunds do not seem to have touched the sides!

The declines in confidence are broad based, with those mortgage free still below neutral, while those with a mortgage still more negative, and those in the rental sector (without property) even more down than that.

The news about rising home prices as impacted property investors, despite the continued weakness in rental income, thus we see a rise from very low levels for this cohort, from 77.01 to 78.45 in the month. On the other hand, property active owner occupied households were a little less positive, moving from 97.1 to 97.05. Property inactive households also drifted lower.

Across the states there was a significant decline in NSW, from 88.4 to 86.2, and this is connected with rising household budget pressures, and large mortgages in Sydney, plus the fires and drought across the state. VIC fell a little too, while there was a small rise in WA.

Across the age bands, those aged 20-30 reported the largest fall, thanks to pressure on incomes and rising costs. A number of new first time buyers who bought in recent months reside here. On the other hand, older cohorts are a little more positive this month, thanks to recent stock market rises, and some better home price news. We note, for example the headline of 6% plus rises in prices across Sydney have been interpreted by households in ALL post codes as appropriate to them – which shows the impact of a tricky headline, remembering that price rises are much higher in the more affluent upmarket postcodes.

Turning to the moving parts within the index, job security is under pressure, thanks to underemployment, weakness in retail and construction, and the upcoming holidays. 7.8% felt more secure than a year ago, down from 8.23% last month. 38.65% said they were less secure compared with 38.12% last month.

Incomes remain under pressure, with just 4.3% saying in real terms their incomes were higher than a year back, down from 5.3% last month. Pressure on household budgets is a pincer movement, as incomes are compressed (and returns from some investments and deposits fall). But costs of living are rising. In fact 94.2% reported higher costs than a year back, thanks to higher prices for fuel, electricity, school fees, childcare, and every needs. Only 1.3% said their costs of living had fallen.

Debt remains a major issue for many households, despite the rate cuts. Some households are paying down their mortgage faster than required, and are using the lower rates, and tax refunds for this. In an era of uncertainty, this is not a surprise. We also see a rise of households under pressure turning to payment options like AfterPay to support their purchases. Just 2% of households were more comfortable with their debt levels than a year ago, while 48% were less comfortable.

Some households have been building their savings (using lower mortgage rates and tax refunds) to build resilience for later. However, lower interest rates on deposits are creating its own pressures, while those with stocks and shares are seeing some dividend pressures too. Around 20% of households have insufficient funds to cover a month without work. Just 0.42% of households were more comfortable than a year ago, 49% were less comfortable and 45% about the same.

Finally, net worth – assets less liabilities, reacted to the higher reported home prices so that 27% say their net worth was better than a year ago up from 24% last month, while 43% were lower, and 24.65% about the same. Net worth was also boosted by high stock market prices and exchange rate movements.

So in conclusion, the household sector remains under pressure, and as a result financial confidence is bruised beyond immediate repair, that is until such time as wages growth really starts to accelerate in real terms. In addition the broader discussions about lower cash rates and quantitative easing are also helping to degrade confidence. The only bright spot, real or illusory, is the recovery in home prices (which are of course not uniform across the main centres and post codes). On this front, households are hoping for the best. We will see.

Financing conditions and the housing market. Council members discussed trends in credit and recent developments in the housing market. Growth in housing credit remains subdued overall, with credit to investors particularly weak. Owner-occupier loan commitments and housing turnover in Sydney and Melbourne have picked up, suggesting that a strengthening in credit growth is likely. Mortgage lending standards have been broadly unchanged recently. Overall, near-term risks related to the housing market have lessened as housing market conditions nationally have improved. Members discussed the potential for the current weakness in apartment construction to place upward pressure on prices in some cities over time unless construction picks up. They also discussed the tight credit conditions for small businesses and the reduced risk appetite by many lenders for lending to small business.

Responsible lending. Members discussed ASIC’s plans to release updated guidance on responsible lending provisions in the coming weeks. The guidance will maintain the current principles-based approach that recognises lenders’ flexibility to determine what is reasonable in individual circumstances. It will also assist lenders to better understand their obligations and reduce the risk of non-compliance. The guidance will also address the confusion around the requirements that apply to small business. It will confirm that responsible lending requirements do not apply to loans made predominantly for business purposes, regardless of the type of security offered for the loan. Council members stressed that the flow of credit is fundamentally important to the functioning of the Australian economy and discussed the concern that lenders’ risk appetite for some types of lending may have swung too far towards caution.

Cyber risk initiatives. The Council met with representatives of the Department of Home Affairs and the Australian Cyber Security Centre (ACSC) to review the current cyber security environment. They also discussed key initiatives to improve cyber resilience, including the development of the Government’s 2020 Cyber Security Strategy, and application to the financial sector. Council agencies, the Department of Home Affairs and the ACSC will continue to cooperate to improve the preparedness of the financial sector.

Resolution planning. APRA provided an update on its work to enhance plans for the resolution of individual financial institutions that become distressed. These plans aim to protect the interests of depositors and maintain functions that are critical to the economy or the financial system during times of stress. The Council discussed the work being undertaken by APRA to remove potential operational barriers to resolving a financial institution. They also considered possible operational arrangements that could provide liquidity assistance to authorised deposit-taking institutions (ADI) that do not have self-securitised loans available to access liquidity in the event of severe liquidity stress.

Non-ADI lending. The Council undertook its annual review of non-bank financial intermediation. Overall, financial stability risks arising from non-ADIs appear limited given the sector’s small size and its minimal links with the banking system. While growth in non-ADI credit for housing has continued to exceed that for ADIs, it remains a small share of total housing lending. The Council welcomed the improvement in data coverage of non-ADI lending following the recent enhancement of APRA’s data collection powers.

Policy and other developments. Members discussed a number of developments, including the ACCC’s residential mortgage product price inquiry, AUSTRAC’s court action against Westpac, changes to APRA’s structure and trans-Tasman developments.

The

Australian Treasurer and representatives of the ACSC, AUSTRAC and the

Department of Home Affairs attended for selected sessions.

Council of Financial Regulators

The

Council of Financial Regulators (the Council) is the coordinating body for

Australia’s main financial regulatory agencies. There are four members: the

Australian Prudential Regulation Authority (APRA), the Australian Securities

and Investments Commission (ASIC), the Australian Treasury and the Reserve Bank

of Australia (RBA). The Reserve Bank Governor chairs the Council and the RBA

provides secretariat support. It is a non-statutory body, without regulatory or

policy decision-making powers. Those powers reside with its members. The

Council’s objectives are to promote stability of the Australian financial

system and support effective and efficient regulation by Australia’s financial

regulatory agencies. In doing so, the Council recognises the benefits of a

competitive, efficient and fair financial system. The Council operates as a

forum for cooperation and coordination among member agencies. It meets each

quarter, or more often if required.

Saxo

Bank, a leading global

multi-asset facilitator of capital markets products and services, has today

released its 10 Outrageous

Predictions for 2020. The

predictions focus on a series of unlikely but underappreciated events

which, if they were to occur, could send

shockwaves across financial markets.

While these predictions do not

constitute Saxo’s official market forecasts for 2020, they represent a

warning of a potential misallocation of risk among investors who typically see

just a one percent likelihood to these events

materialising. It’s an exercise in considering the full extent of

what is possible, even if not necessarily probable. Inevitably the outcomes

that prove the most disruptive (and therefore outrageous) are those that are a

surprise to consensus.

Commenting

on this year’s Outrageous Predictions, Chief Economist at Saxo

Bank, Steen Jakobsen said:

“This

year’s Outrageous Predictions all play to the theme of disruption, because our

current paradigm is simply at the end of the road. Not because we want it to

end, but simply because extending the last decade’s trend into the future would

mean a society at war with itself, markets replaced by governments, monopolies

as the only business model and an utterly partisan and a highly fragmented and

polarised public debate.

“It’s

an environment where negative yields are now used to discriminate against

access to mortgages for low income households, the elderly and students as

regulatory capital requirement demands make credit hurdles too high for that

group to get credit. Instead, they rent at twice the price of owning –

a tax on the poor if ever there was one, and a driver of inequality. This,

in turn, risks leaving an entire generation without the savings needed to own

their own house, typically the only major asset that many medium and lower

income households will ever obtain. Thus, we are denying the very economic

mechanism that made the older generations ‘wealthy’ and risk driving a

permanent generational wealth gap.

“We

see 2020 as a year where at nearly every turn, disruption of the status quo is

an overriding theme. The year could represent one big pendulum swing to

opposites in politics, monetary and fiscal policy and, not least, the

environment. In politics, this would mean the sudden failure of populism,

replaced by commitments to “heal” instead of to divide. In policymaking, it

could mean that central banks step aside and maybe even slightly normalise

rates, while governments step into the breach with infrastructure and climate

policy-linked spending.”

The Outrageous Predictions

2020 publication is available here with headline

summaries below:

1. Australia’s

nominal GDP to 8% on MMT

In 2020, economic red

flags point to more downside ahead for the Australian economy. In Q1 of 2020,

retail sales and cash register activity plunge to their lowest level since the

1991 recession and houses become more unaffordable, with Sydney and Melbourne

being ranked among the world’s most expensive cities for housing. In

Australia’s five biggest cities, more than 30% of average earnings are absorbed

by mortgage repayments, leading to lower consumption and higher consumer

stress.

The Australian economy

could get a lift from the improving China credit impulse next year, but it is

unlikely to be a game-changer as China’s credit transmission is still too slow.

On the top of that, domestic monetary policy is also constrained as the effective

zero-bound approaches and has limited positive effects on the real economy. RBA

governor Philip Lowe was very vocal in 2019 on the limits of monetary policy

and repeatedly explained that further rate cuts have only a marginal effect on

GDP growth — arguing that fiscal stimulus is the only way to bring relief if

the economy continues to weaken.

As consumer confidence

and employment begin to plunge in early 2020, the government decides to embark

on an MMT-inspired economic policy aimed at restoring confidence, stimulating

GDP growth and attracting investment. This is the largest fiscal stimulus

programme in Australia for at least 30 years. It leads to a massive increase in

public spending in infrastructure, the health system and education, as well as

the implementation of ambitious programmes to reduce the cost of living,

provide affordable housing, reduce taxation and address environmental issues.

The strong rise in

fiscal spending contributes to a jump in consumption and investment, almost

doubling Australia’s nominal GDP rate to 8% in 2020. The business community

applauds this bold new economic policy stance. Confidence and risk appetite are

back. After being hit by a perfect storm that drove the Australian dollar down

nearly 20% versus the greenback since early 2018, the AUD is among the best

performing currencies in 2020.

2. The

sudden arrival of stagflation rewards value over growth

The iShares MSCCI World

Value Factor ETF leaves the FANGS in the dust, outperforming them by 25%.The

world has now come full circle from the end of the Bretton Woods system, when

it effectively shifted from a gold-based USD to a pure fiat USD system, with

trillions of dollars borrowed into existence — not only in the US but all over

the world. Each credit cycle has required ever lower rates and greater doses of

stimulus to prevent a total seizure in the US and global financial system. With

rates at their effective lower bound, and the US running enormous and growing

deficits, the incoming US recession will require the Fed to super-size its

balance sheet beyond imagination to finance massive new Trump fiscal outlays to

bolster infrastructure in hopes of salvaging his election chances. But a

strange thing happens: wages and prices rise sharply as the stimulus works its

way through the economy, ironically due to the under-capacity in resources and

skilled labour from prior lack of investment. Rising inflation and yields

in turn spike the cost of capital, putting zombie companies out of business as

weaker debtors scramble for funding. Globally, the USD suffers an intense

devaluation as the market recognises that the Fed will only accelerate its

balance sheet expansion while keeping its policy rate punitively low.

3. ECB

folds and hikes rates

European banks on the

comeback trail as the EuroStoxx bank index rises 30% in 2020.Despite the recent

introduction of the tiering system, which has helped to mitigate the negative

consequences of negative rates, banks are still facing a major crisis. They are

confronted with a challenging economic and financial environment: marked by

structurally ultra-low rates, an increase in regulation with Basel IV — which

will further reduce the banks’ ROE — and competition from fintech companies in

niche markets. In an unprecedented turn of events, in early January 2020, the

new president of the ECB, Christine Lagarde — who has previously endorsed

negative rates — executes a volte-face and declares that monetary policy has

overreached its limits. She points out that maintaining negative deposit

interest rates for a longer period could seriously harm the soundness of the

European banking sector. In order to force euro area governments, and notably

Germany, to step in and to use fiscal policy to stimulate the economy, the ECB

reverses its monetary policy and hikes rates on January 23, 2020. This first

hike is followed by another a short time later that quickly takes the policy

rate back to zero and even slightly positive before year-end.

4. In energy, green is not the new

black

The ratio of the VDE

fossil fuel energy ETF to ICLN, a renewable energy ETF, jumps from 7 to 12. The

oil and gas industry came roaring out of the financial crisis after 2009,

returning some 131% from 2008 until the peak in June 2014 as China pulled the

world economy out of its historic credit-led recession. Since then, the

industry has been hurt by two powerful forces. The first was the advent of US

shale gas and rapid strides in globalising natural gas supply chains via LNG.

Then came the US shale oil revolution, which saw the US become the world’s

largest oil and petroleum liquids producer. The second force has been the

increasing political and popular capital behind fighting climate change,

causing a massive surge in demand for renewable energy. The combined forces of lower

prices and investors avoiding the black energy sector have pushed the equity

valuation on traditional energy companies to a 23% discount to clean energy

companies. In 2020, we see the tables turning for the investment outlook as

OPEC extends production cuts, unprofitable US shale outfits slow output growth

and demand rises from Asia once again.And not only will the oil and gas

industry be a surprising winner in 2020 — the clean energy industry will

simultaneously suffer a wake-up call.

5.

South Africa electrocuted by ESKOM debt

USDZAR rises from 15 to

20 as the world cuts credit lines to South Africa. The very bad news is the

South African government announcement late this year that in order to continue

to bail out troubled utility ESKOM and keep the nation’s lights on, the budget

next year is projected to balloon to its worst in over a decade at 6.5% of GDP,

a sharp deterioration after the government managed to stabilise finances at a

near constant -4% of GDP for the last few years. Worse still, the World Bank

estimates that its external debt has more than doubled over that period to over

50% of GDP. The ESKOM fiasco may be the straw that will break the back of

creditors’ willingness to continue funding a country that hasn’t had its

financial or governance house in order for decades. Other uncreditworthy EMs

will be drawn into the abyss as well in 2020, with the most differentiated

performance across EM economies in years. The country teeters toward default.

6. US

President Trump announces America First Tax to reduce trade deficit

A tax on all

foreign-derived revenue scrambles supply lines and spikes inflation. US 10-year

inflation-protected treasuries yield 6% in 2020 thanks to a rush of investor

interest as the CPI rises. The year 2020 starts with reasonable stability on

the trade policy front after the Trump administration and China manage at least

a temporary détente on tariffs, currency policy and purchases of agricultural

goods. But early in 2020 the US economy struggles for air and US trade deficits

with China fail to materially improve, while Chinese purchases of agricultural

products can’t realistically increase further. Eyeing polls showing a

resounding defeat in the 2020 US Presidential election, Trump quickly grows

restive and his administration drums up a new approach in a last-ditch effort

to steal back the protectionist narrative: the America First Tax. Under the

terms of this tax, the US corporate tax schedule is completely reconstructed to

favour US-based production under the claimed principles of “fair and free trade”.

The plan cancels all existing tariffs and instead slaps a flat value-added tax

of 25% on all gross revenues in the US market that are sourced from foreign

production. This brings stinging protests from trading partners for what are

really just old tariffs in new clothes, but the administration counters that

foreign companies are welcome to shift their production to the US to avoid the

tax.

7.

Sweden breaks bad

A massive and pragmatic

attitude shift washes over Sweden as it gets to work to better integrate its

immigrants and overstretched social services, driving a huge fiscal stimulus

and steep rally in SEK. As often seems the case in Swedish policymaking, just

as they took progressive taxation too far and collapsed the economy in the

early 90’s, they have now taken political correctness on immigration so far

that they have become politically incorrect. They are ignoring the large and

growing contingent of Swedes who are questioning that policy, shutting them out

of the debate. A parliamentary democracy should allow all groups of reasonable

size a voice in the debate, but the traditional main parties of Sweden have

taken the unusual collective decision to ignore the anti-immigration voice

which has grown to represent more than 25% of the Swedish voters. The

justification and intentions were good: openness and equality for all and

safeguarding the Swedish open economic model. But anything taken too far can

overwhelm, and to survive, all models need to be able to change when facts

change. The other Nordic countries now talk of “Sweden conditions” as a threat,

not as a model of best practice. Sweden is now in recession and with its small

open economy status is extremely sensitive to the global slow down. This sense

of crisis, social and economic, will create a mandate for change.

8.

Democrats win a clean sweep in the US 2020 election, driven by women and

millennials

The 2020 US election

puts the Democrats in control of the presidency and both houses of Congress.

Big healthcare and pharma stocks collapse 50%. The polls going into 2020 don’t

look promising for Trump, and neither does the electorate. The marginal Trump

voter in 2016 and in 2020 is old and white, a demographic that is fading in

relative terms as the largest generation in the US now is the maturing

millennial generation of 20-40-year-olds, a far more liberal demographic.

Millennials and even the oldest of “generation Z” in the US have become

intensely motivated by the injustices and inequality driven by central bank

asset market pumping and fears of climate change, where President Trump is the

ultimate lightning rod for rebellion as a climate change denier. The vote on

the left is thoroughly rocked by dislike of Trump – with suburban women and

millennials showing up to express their revulsion for Trump. The Democrats win

the popular vote by over 20 million, grow their control of the House, and even

narrowly take the Senate. Medicare for all and negotiations for drug pricing

bring a massive haircut to the industry’s profitability.

9.

Hungary leaves the EU

Hungary has been an

impressive economic success since it joined the EU in 2004. But the 15-year

marriage now seems in trouble after the EU initiated an Article 7 procedure

against the country, citing Hungary’s – or really PM Orbán’s — ever-tighter

restrictions on free media, judges, academics, minorities and rights groups.

The push back from Hungary’s leadership is that the country is only protecting

itself: mainly protecting its culture from mass immigration. It’s an

unsustainable status quo, and the two sides will find it tough to reconcile in

2020 as the Article 7 procedure moves slowly through the EU system. PM Orbán is

even openly talking about how Hungary is a ‘blood brother’ with the renegade

Turkey as opposed to a part of the rest of Europe, a big shift in rhetoric, a

change of tone which coincides with EU transfers all but disappearing over the

next two years. Hungary’s currency, the forint (HUF) is on the back foot and

reaches a much weaker level of 375 in EURHUF terms as the markets fear the

disengagement or reversal of capital flows as EU companies reconsidered their

investment in Hungary.

10.

Asia launches new reserve currency in move away from US dollar dependence

An Asian, AIIB-backed digital reserve currency

takes the US dollar index down by 20% and tanks the US dollar 30% versus gold.

To confront a deepening trade rivalry and vulnerabilities from rising US

threats to weaponise the US dollar and its control of global finances, the

Asian Infrastructure Investment Bank creates a new reserve asset called the

Asian Drawing Right, or ADR, with 1 ADR equivalent to 2 US dollars, making the

ADR the world’s largest currency unit. The move is clearly aimed at

de-dollarising regional trade. Local economies multilaterally agree to begin

conducting all trade in the region in ADRs only, with major oil exporters

Russia and the OPEC nations happy to sign up due to their growing reliance on

the Asian market. The redenomination of a sizable chunk of global trade away

from the US dollar leaves the US ever shorter of the inflows needed to fund its

twin deficits. The USD weakens 20% versus the ADR within months and 30% against

gold, taking spot gold well beyond USD 2000 per ounce in 2020.

Fidelity International cross-asset specialist Anthony Doyle has warned that the returns over the next decade won’t be anything close to the stellar performance seen over the last 10 years. Via InvestorDaily.

During

a media briefing in Sydney on Tuesday (3 December), Mr Doyle said 2009

to 2019 has been a “phenomenal decade” for Australian investors.

However, he said that he would be shocked if “we generated anywhere near

these returns” over the coming ten years.

“Particularly for a

balanced fund, for example, the default option for most Aussie super

funds. The returns over the next decade are unlikely to be anything like

what we have seen over the past decade.”

The fund manager

explained that lower returns are the result of a record-low cash rate

and that investors are now having to move further down the risk curve in

order to find returns that were once generated by defensive assets like

cash. He also warned that the miracle of compound interest could soon

be a thing of the past in a low-rate environment.

“Something has

gone seriously wrong in the economy,” Mr Doyle said. “After 28 years of

uninterrupted economic growth, the commodities boom, low unemployment, a

fiscal surplus and a current account surplus for the first time in

years, our cash rate is the same as the Bank of England’s. The fact that

our cash rate is the same as the UK’s tells me something has gone wrong

in the Australian economy.”

Hours

after Mr Doyle’s presentation the RBA left the official cash rate on

hold at its final meeting of the decade. Governor Philip Lowe noted that

interest rates are very low around the world and a number of central

banks have eased monetary policy over recent months in response to the

downside risks and subdued inflation.

“Expectations of further monetary easing have generally been scaled back,” he said.

“Financial

market sentiment has continued to improve and long-term government bond

yields are around record lows in many countries, including Australia.

Borrowing rates for both businesses and households are at historically

low levels. The Australian dollar is at the lower end of its range over

recent times.”

While the RBA left rates on hold at 0.75 per cent

on Tuesday, some economists believe the central bank will reduce rates

to 25 basis points, a number flagged by Mr Lowe during a speech last

week.

“Our current thinking is that QE becomes an option to be

considered at a cash rate of 0.25 per cent, but not before that,” the

Reserve Bank governor said. “At a cash rate of 0.25 per cent, the

interest rate paid on surplus balances at the Reserve Bank would already

be at zero given the corridor system we operate. So from that

perspective, we would, at that point, be dealing with zero interest

rates.”

However, Fidelity’s Anthony Doyle believes Mr Lowe’s comments have been widely misread by the market.

“Many

had already been expecting a reduction to 50 basis points in February

and then QE after that. I think he was far more bullish in his speech

and was trying to get the message across that we are a long way from

QE.”

The cash rate has been cut in half over 2019, from 1.50 per

cent to 75 basis points. Mr Doyle believes the RBA will be reluctant to

cut rates any further. He noted that the pickup in house prices in

Sydney and Melbourne could flow through to boost economic growth in the

new year.

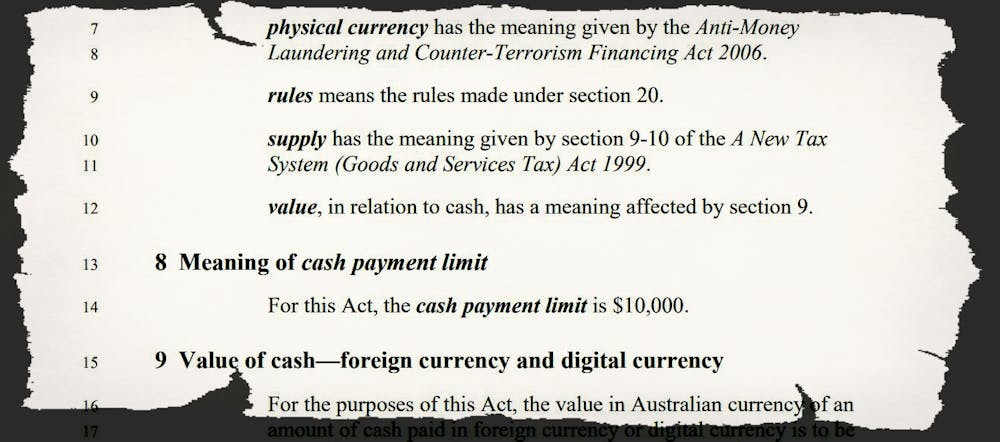

This Act places restrictions on the use of cash or cash-like products

within the Australian economy. The Act imposes criminal offences if an

entity makes or accepts cash payments in circumstances that breach the

restrictions.

The proposed limit is A$10,000. Section 8 would make it an offence to make or accept cash payments of $10,000 occurring either as one-offs or in a linked sequence.

In parliament the minister said the $10,000 limit would not apply to

person-to-person transactions, such as private sales of cars.

But these exceptions are not included in the the Bill. What is

included is the phrase “specified by the rules”. Section 20 puts those

rules in the minister’s hands. Future ministers may narrow exceptions

and change rules.

It would remain legal to withdraw and hold more than $10,000. The stated intent of this Bill is to modify the use of cash, not the holding of cash.

All Australians will continue to be able to deposit and withdraw cash

in excess of $10,000 into and from their accounts, and to store more

than $10,000 of their money outside a bank.

Cash overboard

What’s proposed would limit competition (Visa, Mastercard, and PayPal would face a lesser competitor, for example) and limit long-held rights.

Everyday behaviour at present protected by the law would be criminalised.

In some cases, and perhaps many, the onus of proof would be reversed, with an “evidential burden” imposed on cash-using defendants.

Each partner in a partnership, each committee member of an

incorporated association and each trustee of a trust or superannuation

fund might become individually culpable for their entity’s use of cash.

Oddly, “bodies corporate and bodies politic” are treated differently

(Part 3), and the government itself cannot be prosecuted, an uneven

application of the law which has attracted little attention.

In my submission to the Senate inquiry (Submission 146) I argue the provisions would, among other things:

undercut the ability of banks to head off a banking crisis by providing a trusted and useful form of money

funnel more financial traffic through the equivalent of private toll roads

remove a guaranteed and always available fallback from electronic transactions

increase societal ill-ease and polarisation as citizens realise

their rights have been eroded for not particularly compelling stated

reasons.

Each point and many presented in other submissions need serious consideration, including in public Senate hearings.

The rationale presented

The speech to parliament introducing the bill was built around the hardly-new observation that cash payments can be “anonymous and untraceable”.

The government’s Black Economy Taskforce produced no detailed analysis but recommended the ban as a means of fighting tax avoidance, to:

make it more difficult to under-report income or charge lower prices and not remit good and services tax.

The speech also asserted that “more crucially”

the ban

would fight organised crime syndicates, although organised crime was not

mentioned in the part of the taskforce report that dealt with the

problem the limit was meant to address.

The guarantee dishonoured

Every pound note and then every dollar note issued by the

Commonwealth Bank and then Reserve Bank of Australia bears this

unconditional promise signed by the head of the bank and the head of the

treasury:

This Australian note is legal tender throughout Australia and its territories.

The bank’s website suggests the promise is ongoing:

All previous issues of Australian banknotes retain their legal tender status.

Its note printing arm was mortified earlier this year at the apparently accidental omission of the last letter “i” from the word “responsibility” on the new more secure $50 note.

The Bill before the Senate contains many and much more serious errors.

Cash has been one of the few things we can absolutely rely on,

whatever our status, situation or access to other payment means.

Removing (and dishonouring) that guarantee, while criminalising

reliance on it, should not be done lightly in a mad rush to an arbitrary

date.

Until now public debate about the proposal has been light, but concern is growing, even among quiet Australians.

Each Senator should ensure that last “i” in responsibility isn’t missing here either.

Author: Mark McGovern, Visiting Fellow, QUT Business School, Economics and Finance, Queensland University of Technology