The end of the working month heralds another set of credit stats from both the RBA and APRA. The RBA reports via their Credit Aggregates, which is all credit stock in the system, while APRA reports on the banks (ADI’s) and also provides some individual lender loan stock data. And which ever way you look at it, credit growth is still anaemic, as the “great deleveraging” continues. And given the weak credit impulse, home prices may also be growing more slowly than many are claiming, though that is another story, for another day.

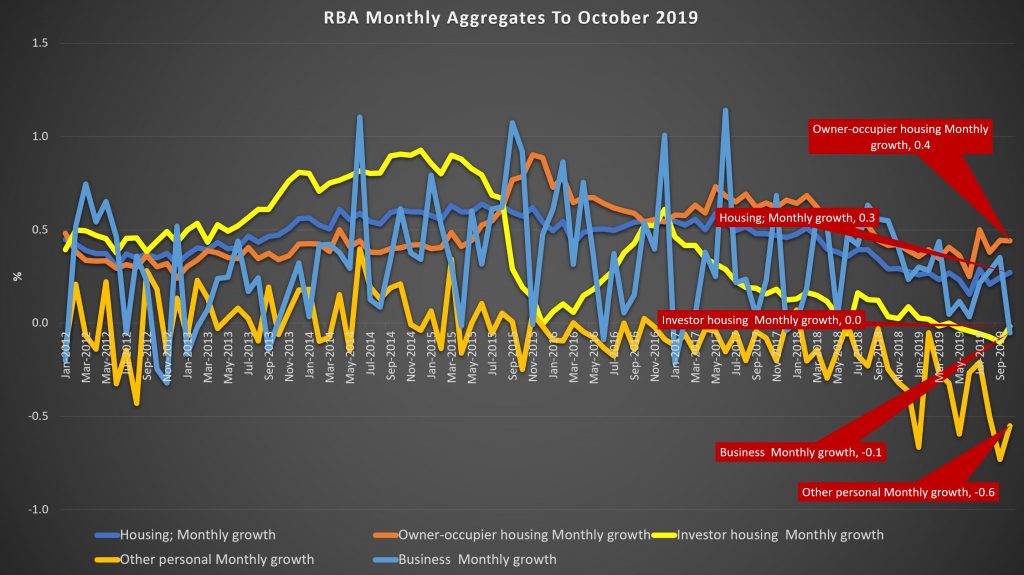

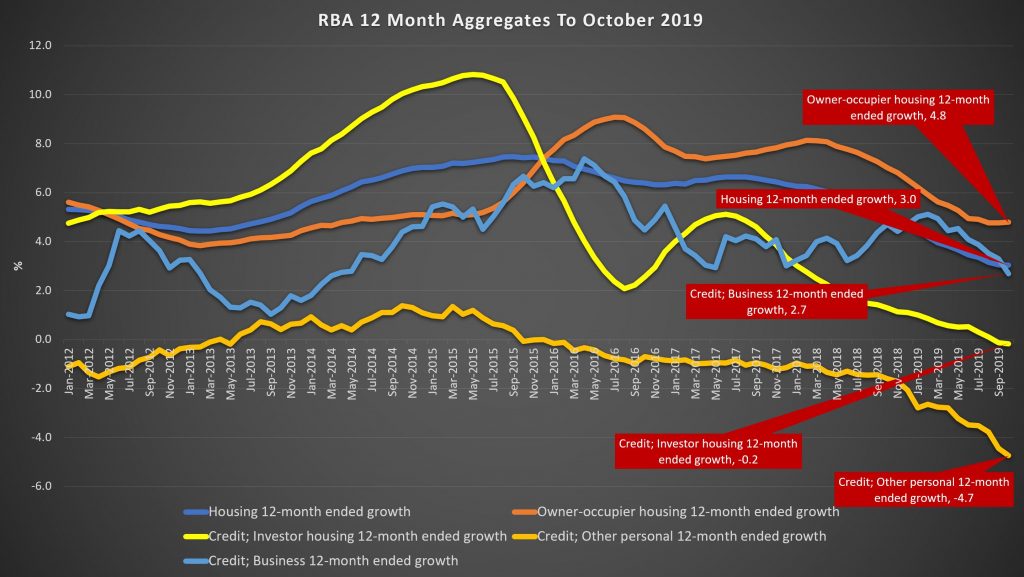

The RBA said that housing credit growth overall was 0.3% higher in October, compared with 0.2% in September. This translates to an annual rate of 3% to October (3.1% last month), compared with 5% just a year back.

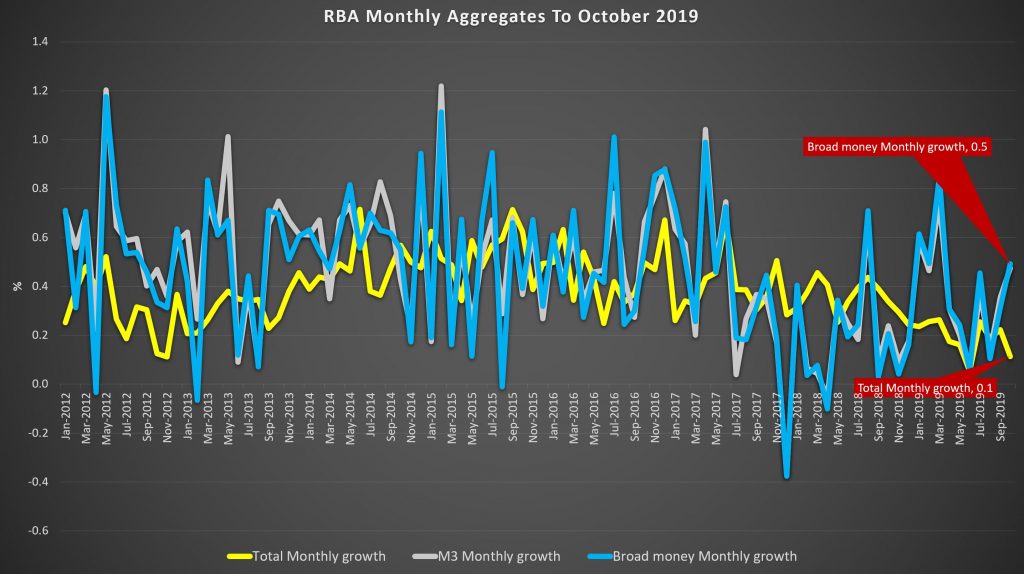

Monthly owner occupied lending rose 0.4% while investor housing lending was flat. Personal credit fell another 0.6% in the month, and business lending was down 0.1%. As a result total credit rose just 0.1%, down from 0.2% last month. Broad money was higher though.

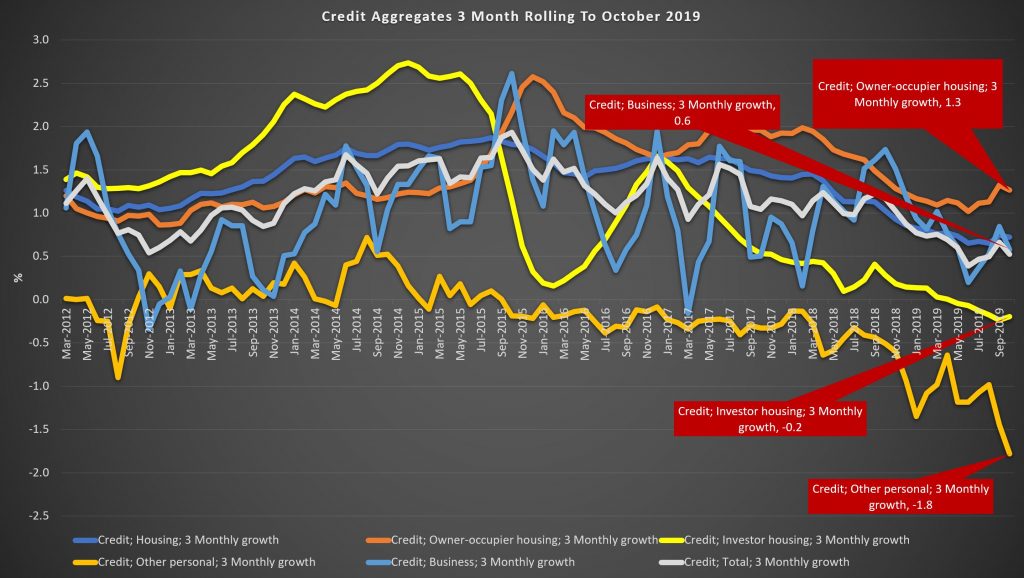

Over a rolling 3 months view, owner occupied credit grew 1.3% while investor credit was down 0.2%, other personal credit was down 1.8% and business credit was up 0.6%.

Looking across the rolling 12 month view, housing credit growth dropped from 3.1% to 3%, with owner occupied lending at 4.8% and investor lending down 0.2%. Business credit was 2.7% higher, and personal credit dropped by 4.7%.

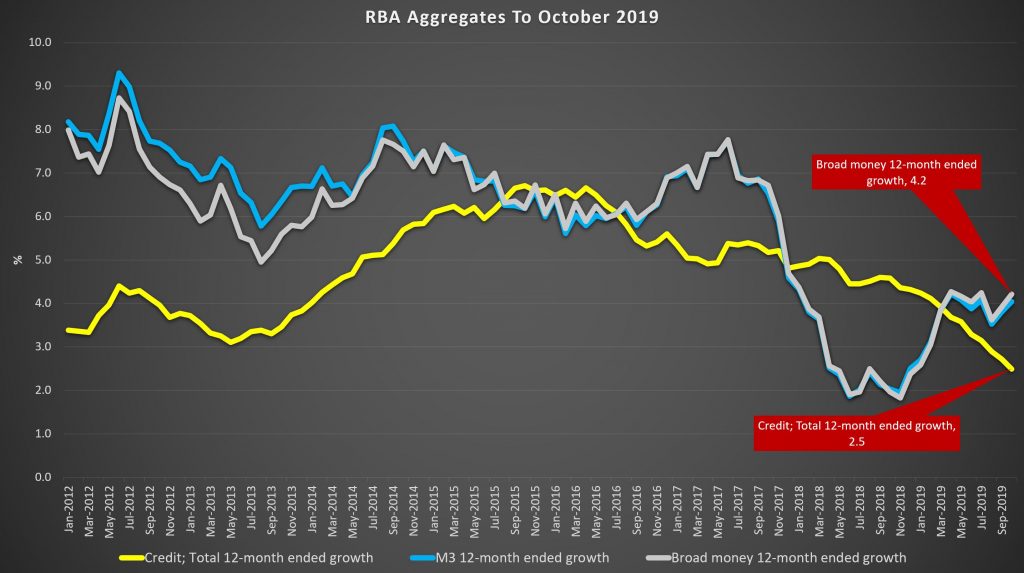

As a result, total credit was just 2.5%, as lower as its been for many years, although broad money rose 4.2%.

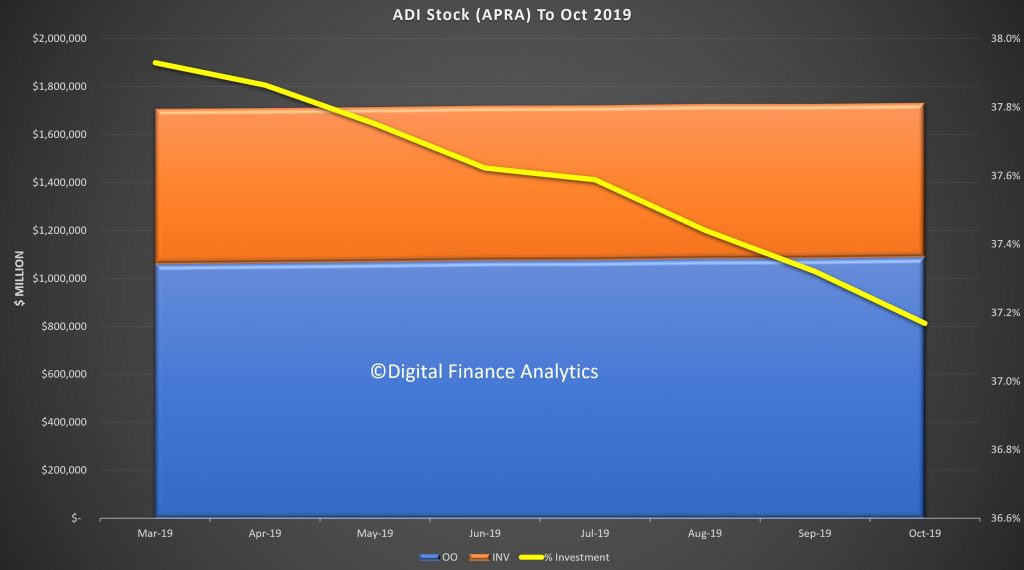

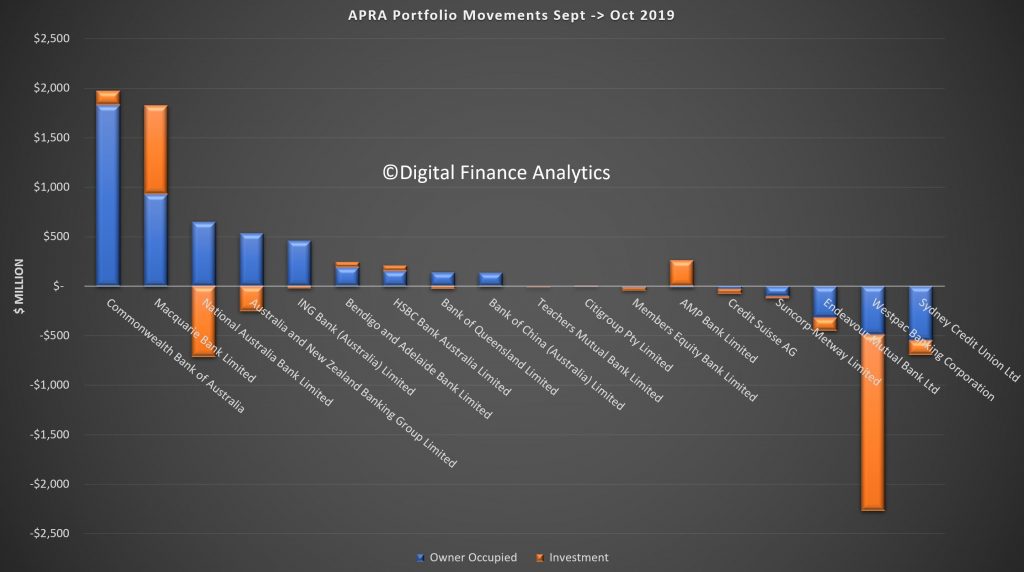

APRA’s new data series continues to contain some surprises. Total lending stock by the banks rose to $1.73 trillion, up 0.2% in the month.

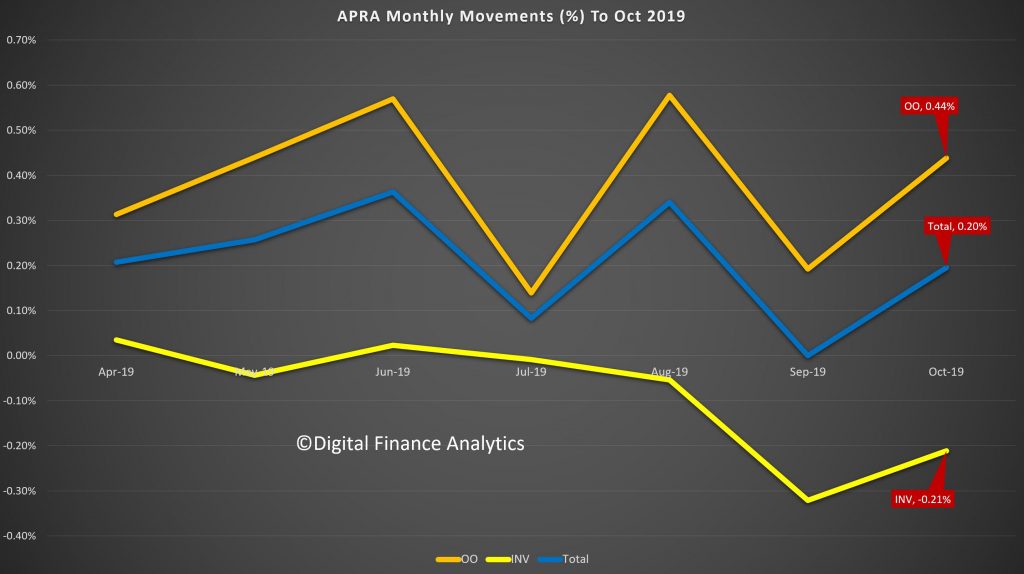

The share of investor loans continues to fall, to around 37.2%, and this is explained by investor loan stock falling by 0.21% in the month, compared with a rise of 0.44% for owner occupied loans. The series still looks a bit weird, so we wonder if there are still reporting issues.

The individual banks stocks of loans varied, with CBA extending their book (consistent with our industry research, as one of the easier lenders at the moment), along with Macquarie – both of which grew both investor and owner occupied pools. NAB and ANZ dropped investor loans, but extended owner occupied loans. But Suncorp and Westpac dropped BOTH investor and owner occupied loan balances (assuming the reporting is correct – lets see if we get a reversal next month).

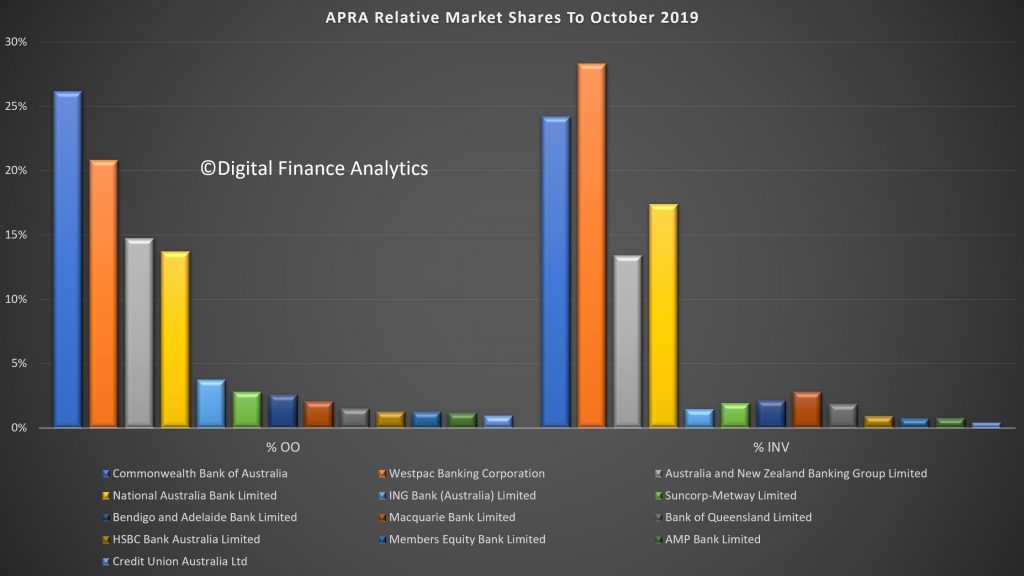

Finally, market shares hardly changed, with CBA the largest owner occupied lender and Westpac the largest investor loan provider.

Given the weak credit growth, this puts into sharp contrast the reported rises in home prices. We know transaction volumes remain low, but our industry contacts indicate a stronger pipeline of applications. Despite this the run-off of existing loans is translating to low net growth.

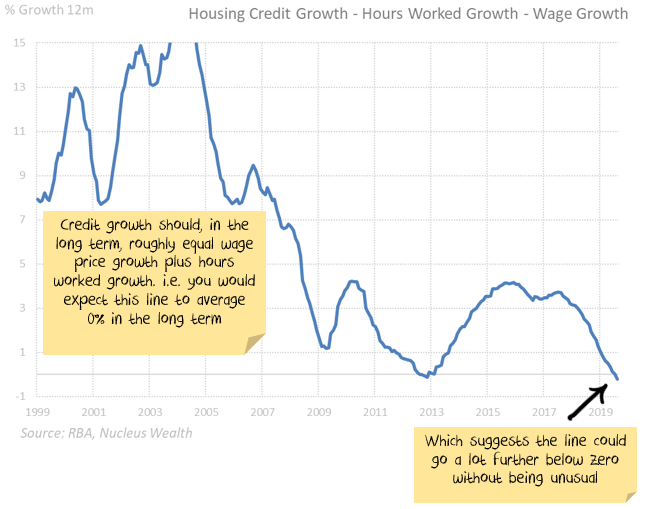

Even then, loan growth is still strong relative to income growth. But actually the most significant element is the fall in business credit, as more sectors come under pressure.

These results appear to be at odds with the RBA’s glass half full view of the economy, and may indicate more weakness in the GDP out-turn next week.

Damien Klassen from Nucleus Wealth penned this recently. It is an excellent summary of the critical issue in play – Can rising house prices drive the rest of the economy on their own without a construction boom? Note the disclaimer below.

I’ve written a few times recently about the imbalances in the Australian economy and how messed up the Australian housing cycle

is. It looks as if the Australian economy is hanging on to positive

growth based on one factor. Without that factor, there is significant

economic downside. The one economic question that matters:

Can rising house prices drive the rest of the economy on their own without a construction boom?

There are three main areas to indicate if this is the case. Two have come out with more negative data since I last posted. One is a glass half empty: better current conditions, worse future conditions.

Upside Case

Can rising house prices drive the rest of the economy on their own without a construction boom?

For

the optimists, the answer is a resounding yes. House prices have not

only stopped falling but have risen over the last few months. Buyer

queues are out the door for limited supply which will inevitably mean

rising house prices. And Morrison’s 95% lending for first home buyers

hasn’t even begun yet. Investors will follow first home buyers, which

will lead prices higher and then upgraders will start buying again.

Rising property prices will mean consumers will start spending once

more, construction will recommence, and a new Australian economic growth

cycle will begin.

It would appear that the Federal Government has this belief.

Downside Case

Can rising house prices drive the rest of the economy on their own without a construction boom?

The

poorer arguments mounted by pessimists tend to have a moral angle:

house prices are too high for children to afford, they will have to come

down to a level that an ordinary person on a regular salary can afford.

If that occurs, house prices will fall 30-40%. While these arguments

are compelling from a social justice perspective, or on a long term

basis, the same arguments have been valid for 15 years. Timing is

important:

Other

weak arguments base the downturn on extrapolating no intervention from

governments. We know the current government is hell-bent on intervening

in the housing market.

The

better argument is that even if construction approvals rebound,

employment would fall for at least another year as the construction

decisions made over the past two years affect the number of people

employed. And construction approvals are not rebounding.

Rising

unemployment in Perth led to a 10% house price fall in the 2012-2017

period while Sydney/Melbourne house prices boomed. What is to stop the

same fate for Australia as a whole?

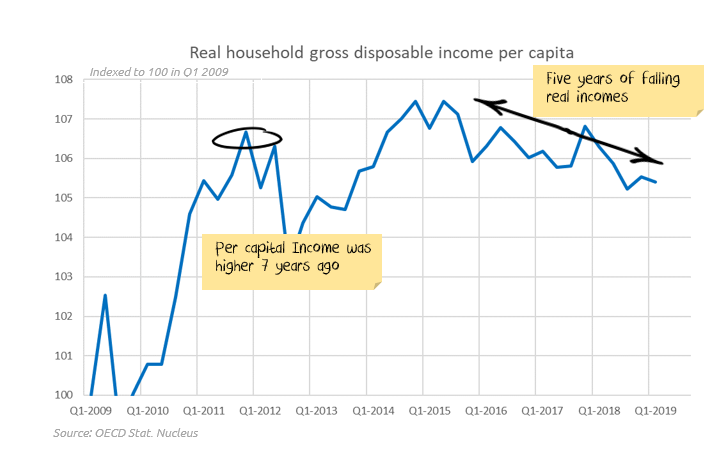

Per capita income has gone nowhere for 7 years, so it is hard to see any rescue coming from that front:

If

rising unemployment does mean house prices fall further, then there are

a range of probable adverse effects. There are some seriously negative

economic effects if the effects snowball. And we won’t even get started

about the impact on a fragile Australian housing market if an

international shock (Brexit, Trade wars, Hong Kong unrest, corporate

debt accidents, European recession) hits.

It doesn’t need to be one or the other

You

don’t need to buy into the entire negative story to be cautious. If

employment holds up, then the positive story has a chance (assuming

benign international conditions). But, if unemployment rises, then

Australia won’t need a global shock to see house prices resume a

downward path.

When

presented with an asset class that has limited upside in positive

scenarios and significant downside in adverse scenarios, I usually opt

to avoid the asset class and look for returns elsewhere.

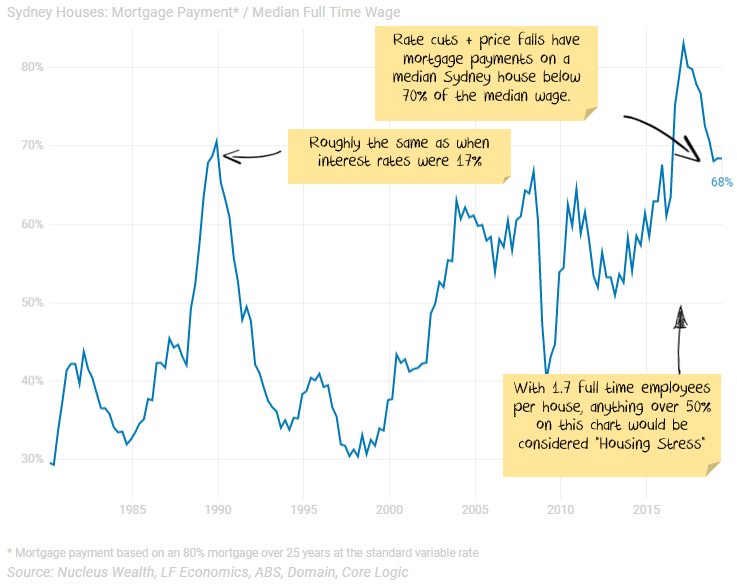

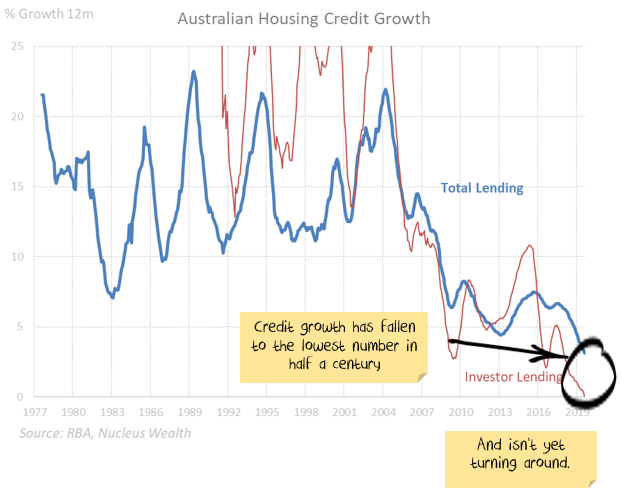

Update 1: Australian Credit growth:

The

Royal Commission into banking reversed the credit boom and was enough

to see house prices down around 10%. This came even while most other

factors affecting house prices were still positive.

Will

the Morrison government manage to get the already over-levered

Australian households to take on even more debt? If I am too bearish,

particularly in the short term, this is where you will see the effects.

So far there are none:

On

the regulatory front, the Westpac v ASIC responsible lending court case

win for Westpac has the potential to lead to easy lending conditions.

ASIC is taking the case to the Federal court, so we are in limbo for

some time.

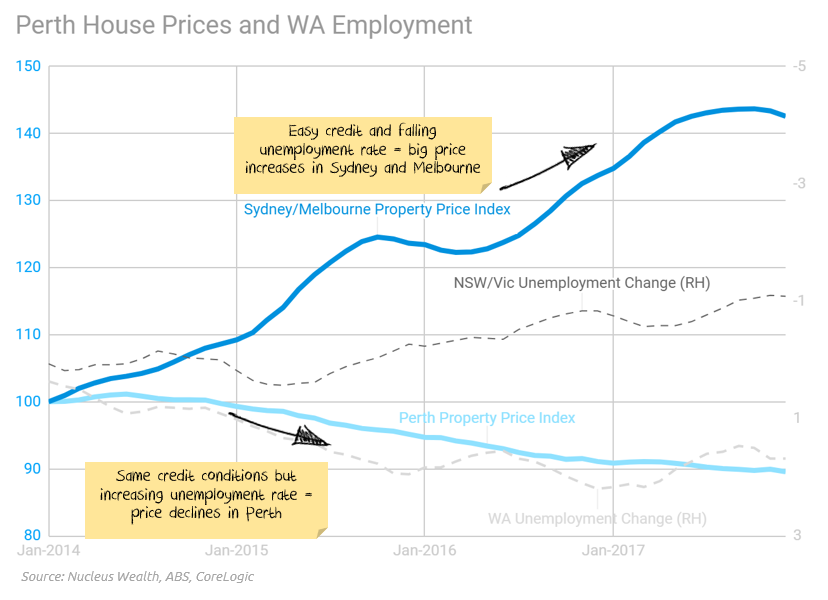

Update 2: Unemployment

There

is not enough space here to go into the detailed links between house

prices and unemployment. Indicatively, during the 2012 to 2017 housing

boom years, the Perth market faced mostly the same factors as

Sydney/Melbourne except for (a) slightly weaker population growth and

(b) rising unemployment. And Perth property prices fell more than 10%

while the rest of Australia boomed.

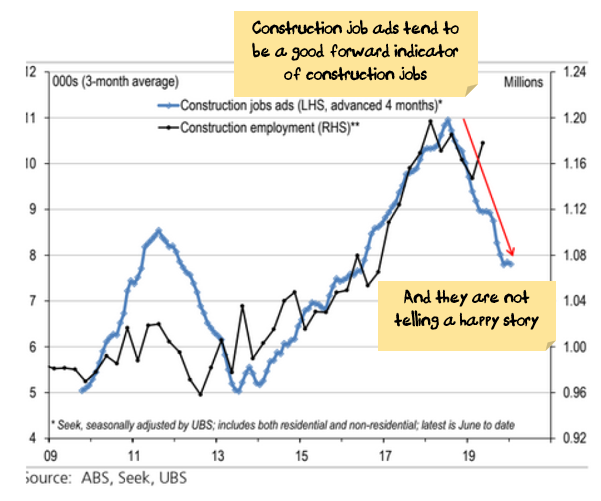

We are expecting considerable job losses in the construction sector.

Having

said that, construction jobs have been resilient so far. Forward

indicators (job ads and approvals) continue to point to sizeable job

losses.

Source: ABS, Seek, UBS

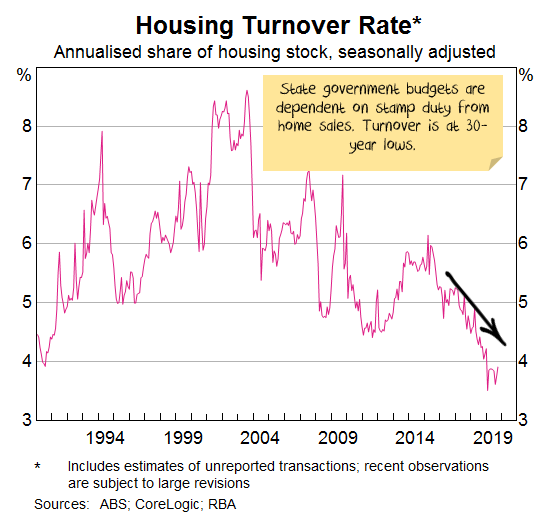

Add

to this scenario, job losses from state government austerity as budgets

have been struck by falling transaction numbers in the housing market:

Finally,

any global shock (trade wars, recessions, debt crises) is likely to be

transmitted to the housing market through higher unemployment.

Update 3: Foreign Buyers

Foreign demand was substantial for both the boom and the bust:

China

cracking down on its capital account and deteriorating relations

between Australia and China suggests foreign investment will remain low.

The question is whether Hong Kong unrest translates to increased demand for Australian property.

The Answer

So, the answer to the one question

Can rising house prices drive the rest of the economy on their own without a construction boom?

will be found in whether increases in unemployment remain contained.

I’m skeptical. But if I’m wrong, the charts above will be where we will see the signs.

Recent data suggest my skepticism is warranted.

Disclaimer

This blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Nucleus Advice Pty Ltd – AFSL 515796.

The Australian Securities and Investments Commission (ASIC) and

Australian Prudential Regulation Authority (APRA) have committed to

strengthen engagement, deepen cooperation and improve information

sharing.

The agencies today published an updated Memorandum of Understanding (MoU).

The updated MoU follows on from the recommendations of the Royal

Commission into Misconduct in the Banking, Superannuation and Financial

Services Industry[1]. APRA and ASIC are also working closely with Government on the legislative changes required to implement these recommendations.

ASIC Chair James Shipton said the updated MoU builds on the open and

collaborative relationship across all levels of the agencies.

‘ASIC and APRA will continue to proactively engage and respond to

issues efficiently to deliver positive outcomes for consumers and

investors.

‘The MoU facilitates more timely supervision, investigations and

enforcement action and deeper cooperation on policy matters and internal

capabilities.’

APRA Chair Wayne Byres said enhanced cooperation reinforced the twin

peaks model of regulation that has operated in Australia for more than

20 years.

‘ASIC and APRA share an interest in protecting the financial

wellbeing of the Australian community and achieving a fair, sound and

resilient financial system,’ Mr Byres said.

‘Strengthening engagement is a key priority of the ASIC Commissioners

and APRA Members. We will continue to work closely together to enhance

regulatory outcomes and achieve our respective mandates.’

This MoU, which will be reviewed on a regular basis, is only one

aspect of how ASIC and APRA are establishing closer cooperation. Led by

ASIC Commissioners and APRA Members, the agencies are regularly meeting

under a revised engagement structure and working together on areas of

common interest, including data, thematic reviews, governance and

accountability. Both agencies are committed to detecting prudential and

conduct issues early and working to revolve them efficiently and

effectively.

The updated MoU is available on the ASIC website here.

The final best interests duty bill for mortgage brokers has been tabled in Parliament, outlining the role brokers need to take when helping a borrower from 1 July 2020. From The Adviser.

The amended Financial Sector Reform (Hayne Royal Commission Response—Protecting Consumers (2019 Measures)) Bill 2019 has been tabled in Parliament today (28 November).

The key features of the new law are:

mortgage brokers must act in the best interests of consumers in relation to credit assistance in relation to credit contracts;

where

there is a conflict of interest, mortgage brokers must give priority to

consumers in providing credit assistance in relation to credit

contracts;

mortgage brokers and mortgage intermediaries must not accept conflicted remuneration;

employers,

credit providers and mortgage intermediaries must not give conflicted

remuneration to mortgage brokers or mortgage intermediaries; and

the circumstances in which these bans on conflicted remuneration apply are to be set out in the regulations.

Notably,

the duty to act in the best interests of the consumer in relation to

credit assistance is a principle-based standard of conduct that applies

across a range of activities that licensees and representatives engage

in.

As such, what conduct satisfies the duty will depend on the

individual circumstances in which credit assistance is provided to a

consumer in relation to a credit contract.

The duty does not

prescribe conduct that will be taken to satisfy the duty in specific

circumstances. Instead, it is the responsibility of mortgage brokers to

ensure that their conduct meets the standard of “acting in the best

interests of consumers” in the relevant circumstances.

However, the new duty will mean that there could be circumstances

where the mortgage broker may not have acted in a consumer’s best

interests even if the responsible lending obligations were complied

with. For example, even if a home loan product is ‘not unsuitable’,

recommending it to the consumer might not be in the consumer’s “best

interests”, the accompanying documentation reads.

The penalty for breaking this duty for both credit representatives and licensees is 5,000 penalty units.

Examples of the duty in action – white label called in question

In the explanatory materials, there are examples of steps that may need to be taken for this new duty. These include:

prior to recommending any home loan product or other credit contract to a consumer based on consideration of that consumer’s particular circumstances, the mortgage broker may need to consider a range of products (including the features of those products), form a view about which products are in the consumer’s best interests and then inform the consumer of the range and the options it contains;

any recommendations made would be expected to be based on consumer benefits, rather than benefits that may be realised by the broker; that is, a broker should not recommend a loan by prioritising factors that cannot be substantiated as delivering benefits to that particular consumer (such as the broker’s relationship with the lender), over factors and features which affect the cost of the product or are more relevant to the consumer;

in cases where critical information is not obtained when inquiring about a consumer’s circumstances, the broker could be expected to refrain from making a recommendation about a loan where there is a consequent risk that the loan will not be in the consumer’s best interests.

Interestingly, the new duty also

outlines that “a broker would not suggest, from their aggregator’s

panel of lenders, a white label home loan that has the same features as a

branded product from the same lender, but with a higher interest rate,

because it would not be in the best interests of the consumer to pay

more for an otherwise similar product”.

The explanatory materials go on to outline that during a periodic review, a broker “would not suggest that the consumer remain in a credit contract without considering whether this would be in the consumer’s best interests”.

“For

example, it may be a breach of the duty if the broker suggested the

consumer remain in their current home loan when they could refinance to a

cheaper product as the broker did not want to incur the consequent

liability to the lender when their commission payments were clawed

back,” it reads.

Helping consumers understand their decision implications

The

materials also outline that there may be situations where the

consumer does not properly understand the implications of different

choices and so the broker may have to assist them to understand why a

particular loan is or is not in their best interests, which could inform

the brokers’ actions.

An example given is if a consumer asks the

broker if they should take out an interest-only home loan on a property

they are looking to buy. The home loan will have a higher interest rate

than a principal and interest home loan. The broker helps the consumer

to understand the difference in cost of the two home loans, and other

differences in the way in which they operate, including that the

consumer will only build equity if the property’s value increases or

they make additional repayments, and the implications of moving to

higher repayments at the end of the interest-only period.

Another

example is if a consumer asks the broker if they should take out a home

loan with an offset account as they have heard this can save them money,

even though the interest rate is slightly higher. The broker helps the

consumer to understand what is in their best interests, based on the

difference between the higher interest rate and the savings that

consumer could reasonably expect through utilisation of the offset

account.

Comments from Frydenberg

At the second reading this afternoon (28 November), Treasurer Josh Frydenberg said: “[T]he

bill introduces a best interests duty for mortgage brokers that will

ensure that consumers’ interests are prioritised when a mortgage broker

provides credit assistance, as regulated by the National Consumer Credit

Protection Act 2009. In practice this will mean that, in accordance

with Commissioner Hayne’s recommendations, a duty will apply in relation

to the provision of consumer credit assistance and not business

lending.

“The

government is also reforming mortgage broker remuneration, and the bill

provides for a regulation making power to this end. The regulations will

require the value of upfront commissions to be linked to the amount

drawn down by borrowers instead of the loan amount; ban campaign and

volume based commissions and payments; and cap soft dollar benefits.

“Further,

the period over which commissions can be clawed back from aggregators

and mortgage brokers will be limited to two years, and passing on this

cost to consumers will be prohibited.

“After

careful consideration, the government decided to delay consideration of

aspects of Commissioner Hayne’s recommendations for mortgage

brokers—namely moving to a borrower-pays remuneration structure. We will

be doing a review with the Council of Financial Regulators and the

Australian Competition and Consumer Commission (ACCC). That will be

carried out in three years time.

“Implementation

of these reforms, as recommended by the royal commission, is a critical

component of restoring trust and confidence in Australia’s financial

system and is part of the Morrison government’s plan for a stronger

economy.”

The government will also introduce the Financial

Sector Reform (Hayne Royal Commission Response – Stronger Regulators

(2019 Measures)) Bill 2019. The Bill implements a further four

additional commitments the Government announced at the time of

responding to the Royal Commission and will ensure that ASIC can

effectively enforce existing laws.

“The government is taking

action on all 76 recommendations contained in the Final Report of the

Royal Commission and, in a number of important areas, is going further.

Restoring trust in Australia’s financial system is part of our plan for a

stronger economy,” Mr Frydenberg said.

Broadcast on Thursday 28th November 2019, Nucleus Wealth’s Head of Investment Damien Klassen, Head of Operations Tim Fuller, and founder of Digital Finance Analytics, Martin North discuss “Australia’s Housing Market Dilemma.”

According to an article in InvestorDaily, RBA Governor Philip Lowe has poured water on the prospects of quantitative easing (QE), saying Australia “shouldn’t forget about fiscal policy” to prevent a recession.

“QE is not on the agenda at this time,” Governor Lowe told at the annual dinner of the Australian Business Economists.

Interest

rates will have to hit 0.25 per cent before the RBA considers QE –

something that economists are predicting by mid-2020. But Governor Lowe

doesn’t think QE will be necessary, saying that the Australian economy

is in a good position and that the RBA will achieve its goals.

“At

the moment, though, we are expecting progress towards our goals over

the next couple of years and the cash rate is still above the level at

which we would consider buying government securities.”

However,

Governor Lowe hinted again that he would prefer the use of fiscal policy

rather than monetary policy to ward off a recession, citing a report

from the Committee on the Global Financial System (CGFS), which he

recently chaired.

“The

report also notes that there may be better solutions than monetary

policy to solving the problems of the day,” Governor Lowe said.

“It

reminds us that when there are problems on the supply-side of the

economy, the use of structural and fiscal policies will sometimes be the

better approach. We need to remember that monetary policy cannot drive

longer term growth, but that there are other arms of public policy than

can sustainably promote both investment and growth.”

Governor Lowe

also said that the willingness of central banks to provide liquidity

could reduce the incentive for financial institutions to hold their own

adequate buffers and create an “inaction bias” from prudential

regulators or fiscal authorities.

“If this were the case, it could lead to an over-reliance on monetary policy,” he said.

The

sentiments about quantitative easing have been echoed by fund managers.

Sarah Shaw, chief investment officer at 4D infrastructure and Chris

Bedingfield, principal at Quay Global Investors have urged the

government to instead allocate investment in infrastructure to create

jobs and boost productivity.

Ms Shaw noted the need to replace

roads, bridges and other structures with better planned

“forward-thinking” infrastructure is high.

“If you think about the

need for infrastructure spend that I’m talking about, if you put a

number on it, it’s maxed at $4 trillion by 2040 of infrastructure

capacity that’s needed,” she said.

“If you think about that and

you’re in an interest rate environment as low as it is today, if you’re

not borrowing to invest in a much-needed infrastructure, then there’s

something wrong.”

She added she looks for companies that are

locking in fixed term bet to invest for future cash flows, because “now

is the time to do it” with the current low cash rate.

“Why shouldn’t countries be doing that?” Ms Shaw queried.

“I’ll

give you an example: China during the GFC, biggest form of quantitative

easing – 35,000 kilometres of high-speed rail. That’s the sort of

quantitative easing that we should be looking at here in Australia.”

VanEck has predicted there will be more rate cuts in 2020.

As discussed with John Adams in our recent post, we did not come away with the same conclusion, and Westpac, for example is forecasting QE will hit during 2020.