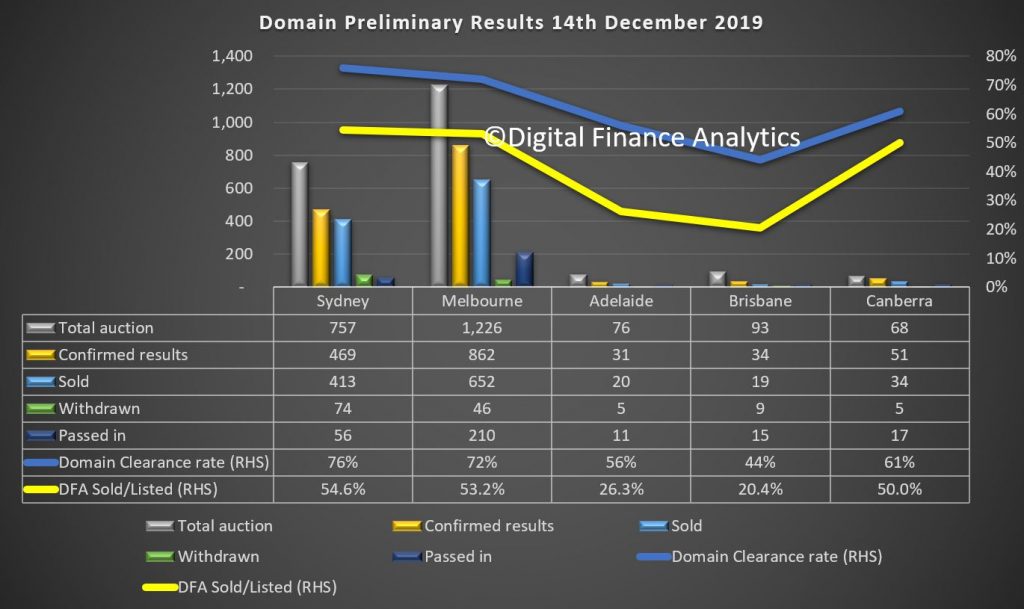

Domain released their preliminary results for today. This is the last report from them until end January 2020. In addition, they did not send the detailed breakdown they normally do.

So I generated my own chart to show the results.

The current sold over listed ratio is significantly lower than their calculated clearance rates.

The IMF published their latest preliminary findings at the end of an official IMF staff visit (or ‘mission’) to Australia. They recommend preparing for risk from a rapid housing credit upswing, by introducing loan-to-value and debt-to-income limits, and possibly a sectoral countercyclical capital buffer targeting housing exposures. Plus transitioning from a housing transfer stamp duty to a general land tax to improve efficiency by easing entry into the housing market and promoting labor mobility, while providing a more stable revenue source for the States. Such reforms could be complemented by reducing structural incentives for leveraged investment by households, including in residential real estate.

Economic growth has gradually improved

from the lows in the second half of 2018 but has remained below

potential.

Growth has been supported by public spending, including on infrastructure,

and net exports, which have held up well despite headwinds from global

policy uncertainty and China’s economic slowdown. However, domestic private

demand has remained weak amid subdued confidence, with a widening output

gap. In addition, the ongoing drought has been a drag on economic growth.

Wage growth has remained sluggish, reflecting persistent labor market

slack, and inflation and measures of inflation expectations have dropped to

below Australia’s 2 to 3 percent target range. Following a marked

adjustment over the past two years, housing prices have started to recover,

particularly in Sydney and Melbourne.

Growth should continue to recover at a gradual pace.

Following growth of about 1.8 percent in 2019, the economy is expected to

expand by 2.2 percent in 2020.Private domestic demand is

expected to recover slowly, supported by monetary policy easing and the

personal income tax cuts. An incipient recovery in mining investment is

also expected to contribute to growth. In addition, the house price

recovery will likely reduce the drag on consumption from earlier, negative

wealth effects. That said, residential and non-mining business investment

are expected to take longer to recover. Over the medium term, growth is

expected to reach the mission’s estimate of potential growth of about 2½

percent, supported by infrastructure spending and structural reforms. With

continued labor market slack, underlying inflation will likely stay below

the target range until 2021.

Risks to the outlook remain tilted to the downside.

· On the external side, Australia is especially exposed to a

deeper-than-expected downturn in China through exports of commodities and

services. A renewed escalation of U.S.-China trade tensions could further

impair global business sentiment, discouraging investment in Australia. A

sharp tightening of global financial conditions could squeeze Australian

banks’ wholesale funding and raise borrowing costs in the economy.

· On the domestic side, private consumption could be weaker should a

cooling in labor markets squeeze household income. Adverse weather

conditions, including a more-severe-than-expected drought, could further

disrupt agriculture, dampening growth. On the upside, looser financial

conditions could re-accelerate asset price inflation, boosting private

consumption but also adding to medium-term vulnerabilities given high

household debt levels.

With below-potential growth, weakening inflation expectations, and

continued downside risks, the macroeconomic policy mix should remain

accommodative.

· Monetary policy has been appropriately accommodative, and continued

data-dependent easing will be helpful to support employment growth,

inflation and inflation expectations.

· The consolidated fiscal stance is appropriately expansionary for

FY2019/20. Fiscal policy will be supportive for demand via reductions in

personal income and small business corporate taxes, additional

infrastructure spending, and the government’s announced support measures

for small- and medium-sized enterprises (SMEs). However, fiscal policy

aggregated across all levels of government will be contractionary in

FY2020/21, as state-level infrastructure investment is expected to decline.[1] States should reconsider this and attempt to at least maintain their

current level of infrastructure spending as a share of GDP to continue

addressing infrastructure gaps and supporting aggregate demand.

The authorities should be ready for a coordinated response if downside

risks materialize.

Australia has substantial fiscal space it can use if needed. In addition to

letting automatic stabilizers operate, Commonwealth and state governments

should be prepared to enact temporary measures such as buttressing

infrastructure spending, including maintenance, and introducing tax breaks

for SMEs, bonuses for retraining and education, or cash transfers to

households. In case stimulus is necessary, the implementation of budget

repair should be delayed, as permitted under the Commonwealth government’s

medium-term fiscal strategy. In addition, unconventional monetary policy

measures such as quantitative easing may become necessary in such a

scenario as the cash rate is already close to the effective lower bound.

The macroprudential policy stance remains appropriate but should stand

ready to tighten in case of increasing financial risks.

Australian banks remain adequately capitalized and profitable, but

vulnerable to high exposure to residential mortgage lending and dependent

on wholesale funding. While the risk structure of mortgage loans has been

significantly improved, renewed overheating of housing markets and a fast

pick-up in mortgage lending remain risks in a low-interest-rate

environment. The Australian Prudential Regulation Authority (APRA) should

continue to expand and improve the readiness of the macroprudential

toolkit. This should include preparations, for potential use in the event

of a rapid housing credit upswing, for introducing loan-to-value and

debt-to-income limits, and possibly a sectoral countercyclical capital

buffer targeting housing exposures.

Strong reform efforts to bolster the resilience of the financial sector

should continue.

The mission supports the authorities’ plan to further enhance banks’

capital framework, including strengthening their loss-absorbing capacity

and resilience. In addition, encouraging banks to further lengthen the

maturity structure of their wholesale funding would help mitigate ongoing

structural liquidity risks. The authorities’ commitment to implement the

recommendations made by the Hayne Royal Commission by end-2020 is welcome.

The improvement in lending standards further enhances financial sector

resilience, and reducing the uncertainty in the enforcement of responsible

lending obligations would prevent excessive risk aversion in the provision

of credit. The authorities should implement the APRA Capability Review’s

recommendations to strengthen APRA’s resources and operational flexibility,

enhance its supervisory approach in assessing banks’ governance and risk

culture, and strengthen enforcement efforts. In addition, reinforcing

financial crisis management arrangements and strengthening the AML/CFT

regime should remain priorities, in line with the findings of the 2018

Financial Sector Assessment Program (FSAP).

Housing supply reforms remain critical for restoring affordability.

More efficient long-term planning, zoning, and local government reform that

promote housing supply growth, along with a particular focus on

infrastructure development, including through “City Deals”, should help

meet growing demand for housing.

Efforts to boost private investment and innovation should be stepped

up.

Non-mining business investment, including R&D, has been sluggish,

contributing to lower productivity growth. Reducing domestic policy

uncertainty, supporting SMEs’ access to finance, and accelerating

structural reforms would help to improve the investment environment.

Building on reforms in the 2015 Harper Review, Australia can further

improve product market regulations, including by simplifying business

processes through the work of the Deregulation Taskforce. The ongoing

policy priority on skills and education reforms is welcome to improve the

environment for innovation, and consideration should be given to faster

implementation of the recommended measures in the Australia 2030: Prosperity through Innovation report. Government

initiatives to relieve SME financing constraints are welcome, including the

Australian Business Securitization Fund and the Australian Business Growth

Fund. Incentives for banks to lend more to businesses, including through

reducing the concentration in mortgages, can help support business

investment, as can the promotion of venture capital. Supporting new

investment through tax measures, possibly including targeted investment

allowances, as well as further improving the effectiveness of government

R&D support for younger firms, would also be helpful.

Australia’s continued efforts supporting international cooperation are

welcome.

The mission welcomes the authorities’ support to enhance the effectiveness

of the WTO and pursuit of the Regional Comprehensive Economic Partnership

(RCEP), which aims to liberalize trade and improve quality and

environmental standards and labor mobility throughout the Asia and Pacific

region. Developing a national, integrated approach to energy policy and

climate change mitigation, and clarifying how existing and new instruments

can be employed to meet the Paris Agreement goals, would help reduce policy

uncertainty and catalyze environmentally-friendly investment in the power

sector and the broader economy.

Further reforms can help to promote female labor market participation

and reduce youth underemployment.

There is scope to increase full-time employment for Australian women and

addressing persistently high underemployment particularly among youth. The

2018 Child Care Subsidy program and the forthcoming Mid-Career Checkpoint

program are expected to support women in work. This could lay the

foundation for a broader review of the combination of taxes, transfers, and

childcare support to reduce disincentives for female labor force

participation. Pursuing ongoing reforms in vocational training can help

reduce youth underemployment.

Broad fiscal reforms would help promote efficiency and inclusiveness.

Australia should continue to reduce distortions in its tax system to

promote economic efficiency and in doing so should be mindful of

distributional consequences considering income inequality. Recent reforms

in personal and corporate income taxes have helped to improve the

efficiency of the tax system. A further shift from direct to indirect taxes

could be made by broadening the goods and services tax (GST) base and

reducing the statutory corporate income tax rate for large firms. The

impact of these reforms could be made less regressive for households

through targeted cash transfers. Transitioning from a housing transfer

stamp duty to a general land tax would improve efficiency by easing entry

into the housing market and promoting labor mobility, while providing a

more stable revenue source for the States. Such reforms could be

complemented by reducing structural incentives for leveraged investment by

households, including in residential real estate.

The mission would like to thank the authorities and counterparts in the

private sector, think tanks, and other organizations for frank and

engaging discussions.

The

Conservatives are set to win an overall majority of 86 in the general

election, according to an exit poll for the BBC, ITV and Sky News.

The

survey taken at UK polling stations suggests the Tories will get 368

MPs – 50 more than at the 2017 election – when all the results have been

counted.

Labour would get 191, the Lib Dems 13, the Brexit Party none and the SNP 55.

The Green Party will still have one MP and Plaid Cymru will lose one seat for a total of three, the survey suggests.

The first general election results are due before midnight (UK time), with the final total expected to be known by Friday lunchtime.

In

the exit poll, voters are asked to fill in a mock ballot paper as they

leave the polling station indicating how they have just voted.

The exit poll was conducted by Ipsos Mori at 144 polling stations, with 22,790 interviews.

Exit

polls have proved to be very accurate in recent years. In 2017 it

correctly predicted a hung Parliament, with no overall winner, and in

2015 it predicted the Conservatives would be the largest party.

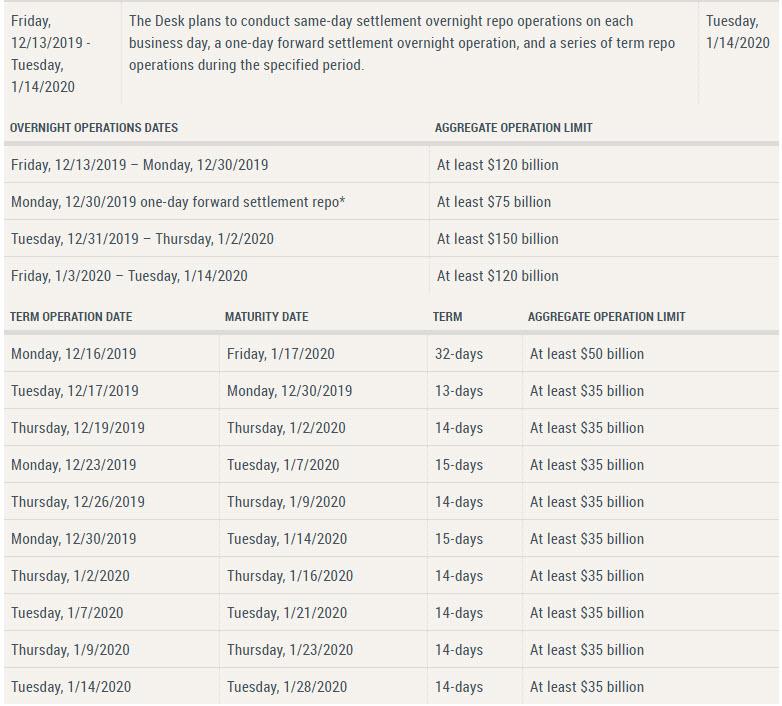

The Open Market Trading Desk (the Desk) at the Federal Reserve Bank of New York has released the schedule of repurchase agreement (repo) operations for the monthly period from December 13, 2019 through January 14, 2020. In accordance with the most recent FOMC directive, the Desk will conduct repo operations to ensure that the supply of reserves remains ample and to mitigate the risk of money market pressures around year end that could adversely affect policy implementation.

The Desk will continue to offer two-week term repo operations twice per week, four of which span year end. In addition, the Desk will also offer another longer-maturity term repo operation that spans year end. The amount offered in this operation will be at least $50 billion.

Overnight repo operations will continue to be held each day. On December 31, 2019 and January 2, 2020, the overnight repo offering will increase to at least $150 billion. In addition, on December 30, 2019, the Desk will offer a $75 billion repo that settles on December 31, 2019 and matures on January 2, 2020.

The Desk intends to adjust the timing and amounts of repo operations as needed to mitigate the risk of money market pressures that could adversely affect policy implementation, consistent with the directive from the FOMC.

So, the NY Fed will continue to offer two-week term repo operations twice per week, four of which run across the end of the year end. Plus, they will also offer another longer-maturity term repo operation that spans year end. The amount offered in this operation will be at least $50 billion.

And they leave the door open to more if need by saying “intends to adjust the timing and amounts of repo operations as needed to mitigate the risk of money market pressures that could adversely affect policy implementation, consistent with the directive from the FOMC.”

So in essence, as well has growing the size its overnight repos to $150 billion, the Fed will run nine term repos covering the year-end turn from Dec 16th to Jan 14th, 8 of which will amount to $35 billion and the first will be $50 billion, for a total injection of $365 billion in the coming month.

This is what the Fed Balance Sheet might look like. If this is not QE, I do not know what is….

On 10 December, Deutsche Bank AG hosted an investor day following the announcement this summer of its more radical shift in strategy. Via Moody’s.

We see the bank as being on track to achieving the majority of the plan’s targets, in particular with regard to the proposed de-risking, downsizing and cost-cutting measures, while achievement of the revenue growth targets may prove more challenging. Continued fast and steady progress in achieving the new goals and repositioning DB’s business model will be important to maintaining its current credit strength, which we believe will continue to be supported by its clean balance sheet and solid capital and liquidity metrics during execution.

Within the bank’s capital release unit (CRU), its key wind-down unit, the bank expects risk-weighted assets (RWAs) to decline toward €52 billion by the end of 2019, down 28% year over year, while it expects leverage exposures to fall to €120 billion, a decline of 57% year over year. This includes the effect of DB’s transaction agreement with BNP Paribas on DB’s global prime finance and electronic equities business, supporting further swift de-risking and downsizing of the CRU, as well as help financing the group’s restructuring program out of its own financial resources. DB expects adjusted costs to be €21.5 billion in 2019, and reiterated its target of €19.5 billion of adjusted costs in 2020 and €17 billion in2021.

Notwithstanding continued strong credit-positive cost control, management also guided for lower revenue growth, largely owing to lower interest rates negatively affecting its private bank franchise. DB now expects group revenue to be around €24.5 billion by 2022, a slight reduction from the earlier €25 billion target. This includes a cumulative negative revenue effect of €1.2 billion during the restructuring period. However, DB has already initiated measures aimed at offsetting approximately two-thirds of this revenue strain. Sustained execution success will therefore rely on DB’s ability to rebuild and stabilize core bank revenue against the backdrop of the increasingly challenging macroeconomic environment.

Despite the meaningful restructuring-related charges to date, DB maintained its Common Equity Tier 1 (CET1) ratio at 13.4% as of 30 September 2019, a solid buffer above the recently lowered European Central Bank CET1 capital ratio requirement of 11.59%. In addition, DB’s €243 billion liquidity reserve is well in excess of the requirements stipulated by the liquidity coverage ratio, which was 139% as of 30 September 2019 (its net buffer was €59 billion). DB expects its corporate bank unit to report compound revenue growth of 3% during the 2018-22 restructuring period, unchanged from the July announcement. DB aims to build on its strong global transaction banking, cash management and securities service franchises,as well as grow lending to German corporate customers.

DB expects costs to remain virtually flat as it retains client-facing staff and continues to invest in its franchise. Revenue growth will be supported by focusing on the aforementioned focus areas, as well as passing on negative interest rates to partly compensate for challenges in the euro area.

The investment bank unit aims to achieve 2% compound revenue growth, with an increase expected during the 2019-22 period. DB cited stronger-than-anticipated client retention and a rise in top 100 institutional client revenue as supporting its goals over the next few years. The investment bank unit’s profitability should further benefit from the announced cost-cutting measures over time, of which parts will have to be reinvested in technology and infrastructure to maintain leading positions in credit, foreign exchange, fixed income and currencies in Asia-Pacific and Europe, Middle East and Africa. The private bank will suffer most from the even lower interest rate environment. The bank now expects compound revenue growth to be flat over the 2018-22 period, a reduction from the 2% target set out in July. Private banking will remain key to extracting synergies from the integration of the DB franchise with the former Postbank, converting low-margin deposits into fee-producing investment products through collaboration with asset and wealth management, as well as the corporate bank.

The bank expects its asset management unit’s revenue to report a compound annual growth rate of 1% during the period. The reduced target takes into account lower equity market forecasts and a continued strain on margins in the asset management industry. The unit aims to extract a further €150 million of gross cost synergies by 2022, moving its cost-to-income ratio to below 70% (the bank’s asset management unit target is around 65%). Assets under management increased by 9% to €754 billion, driven by positive market performance and another quarter of positive net new money flows. The CRU has been able to downsize exposures faster than anticipated. Quickly reducing the CRU’s revenue and profitability drag to achieve fast and steady progress in reaching the new goals and repositioning DB’s business model will be important to maintaining its current credit strength, as well as safeguarding its capital adequacy metrics.

On Monday the Australian government will release the Mid-Year Economic and Fiscal Outlook (MYEFO). This will – as required by the Charter of Budget Honesty – provide an update on the key assumptions made in this year’s budget, and track the implications of decisions made since the budget for the projected surplus. Via The Conversation.

There are two things you can count on about MYEFO.

First, the government will have to pare back its forecasts for economic growth, wages growth and employment growth.

Second, no matter what the economic reality is, the forecast for a budget surplus will remain.

The government has made economic

management – as measured by the rather dubious criterion of budget

balance – the central plank of its electoral strategy. As the Australian

National University’s 2019 Australian Election Study

revealed, voters preferred the government’s economic policies to

Labor’s by a wide margin (47% to 21%, with 17% thinking there was no

difference). On the management of government debt, the margin was 44% to

18%.

But the economy isn’t doing very well. GDP annual growth is 1.7%, not the 2.75% forecast in the budget. The unemployment rate is 5.3%, compared to the forecast of 5.0%. Wage growth is 2.2%, not the 2.75% forecast.

Iron ore supplements

The forecast budget surplus for the fiscal

year to June 2020 will be made to hang together, thanks to a

higher-than-forecast iron ore price.

That price – which determines the dollar

value of Australia’s biggest export and hence the tax revenue it

generates – is not reflected in the GDP figure, which only takes into

account volumes.

The iron-ore price is now US$92.50 a tonne. The budget assumed the average price would be $US88 for the 2020 budget year, thanks to a reduction in the international supply of iron ore caused by a tailings dam bursting in January at the Córrego do Feijão mine near the town of Brumadinho in southeastern Brazil.

The dam’s collapse released a tsunami of sludge that destroyed farms, houses, roads and bridges, and killed 272 people.

The river of sludge released by the dam spill in Brumadinho, Minas Gerais, Brazil, January 26 2019.

Antonio Lacerda/EPA

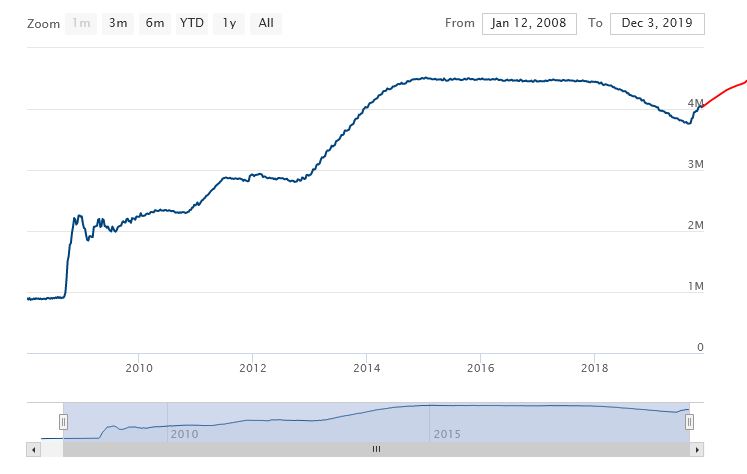

Ensuing mine shutdowns reduced iron ore

output from operator Vale (the world’s biggest iron ore miner) by about a

third. This in turn led to the price of iron ore this year being very

high, as the following chart illustrates.

The Australian government sensibly assumed

the Brazilian mine would come back online and the ore price would

revert to $US55 per tonne by March 2020.

But just think about the 2020-21 fiscal year. The government’s own sensitivity analysis

shows for the full 2020-21 budget year a difference in the iron ore

price of US$10 a tonne translates to a A$3.7 billion difference in the

budget bottom line.

That has helped this year, but it also

shows how dependent the budget’s relatively small A$7.1 billion

“underlying cash balance” is on a commodity price that’s out of our

control.

Yet, given the political non-negotiability

of the surplus, we can expect assumptions that stretch credulity to

maintain a surplus forecast.

Some action?

This is all against a backdrop of calls

for fiscal stimulus from the governor of the Reserve Bank of Australia,

the Business Council, every mainstream economist and recently Australia’s top chief executives.

But any stimulus meaningful enough to

boost the ailing economy would blow the budget surplus. And the

assumptions have already been stretched to breaking point, so there’s

very little room for the government to manoeuvre.

The government will probably announce some

sort of “investment allowance” – where companies get a modest tax break

for specific types of investments in the short term. As I have argued before,

this will do something to boost investment and the economy generally,

but not nearly as much as a full-scale reduction in the company tax rate

to 25% for all businesses.

But the government can’t afford to do a proper tax cut because of its devotion to a wafer-thin surplus.

The danger of too little action

In the end, what the government ends up

announcing will really be an allocation of responsibilities. It will

determine how much of the work of economic recovery it will do itself,

and how much it will want to palm off to the Reserve Bank.

The downside of the former is losing the budget surplus.

The downside of the latter is that the

Reserve Bank will have no choice but to cut the cash rate to 0.25% in

early 2020 and then embark upon a bond-buying program – i.e.

“quantitative easing” or “QE”.

As even Reserve Bank governor Philip Lowe

has himself admitted, more aggressive monetary policy brings with it the

(further) risk of asset-price bubbles and financial instability.

Right now the government is putting all its chips on the surplus. Will that turn out to be a good bet? Time will tell.

2020 will reveal much about the future of

the Australian economy and whether we manage to escape dramatic problems

like a recession.

We live in interesting times – but perhaps more in the “Ancient Chinese curse” kind of way than any of us would like.

Author: Richard Holden, Professor of Economics, UNSW

In the latest from Nucleus Wealth, Head of Investment Damien Klassen, and Head of Operations Tim Fuller, chat with Economist and Hon. Prof. of the University College of London, Steve Keen.

Topics include credit creation and its limits, weighing up its pro’s and con’s, central banks reaching the end of the road for interest rate cuts with debt being at near record highs, the drivers of weak demand and inflation globally, Modern Monetary Theory (MTT) and its differences with Keynesian Stimulus, which countries are closest to incorporating MMT, Steve’s ideas for central banks depositing directly into citizens bank accounts and “Universal Basic Carbon.” Nucleus Wealth is a Melbourne based investment house that can help you reach your financial goals through transparent, low cost, ethically tailored portfolios.

Disclaimer: The information on this podcast contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen and Tim Fuller are an authorised representative of Nucleus Wealth Management. Nucleus Wealth is a business name of Nucleus Wealth Management Pty Ltd (ABN 54 614 386 266 ) and is a Corporate Authorised Representative of Nucleus Advice Pty Ltd – AFSL 515796