We discuss recent development in the proposed cash transaction ban, with the help of a recent Saturday paper article and CBA’s systems failures today. Cash is king!

While the ATM and EFTPOS merchant services are working and debit and credit cards are working, some debit card payments may be affected.

But BPAY services including PAY-ID payments not available and Cardless Cash not available. In addition some in-branch service, some call centre services and business services on CommBiz were hit.

The CommBank app and NetBank are available with limited functionality.

A small number of branches have closed.

They said “We are experiencing higher than normal volume of calls to our contact centres which means there are longer wait times. Some of our contact centre services are also impacted limiting what services we can provide”.

Now, consider the situation where cash is less available. Sometime good old cash is still king!

The Australian Prudential Regulation Authority (APRA) has advised that it will not appeal the Federal Court decision to dismiss APRA’s court action against IOOF entities, directors and executives.

The case examined a range of legal questions relating to superannuation law and regulation that had not previously been tested in court, relating to the management of conflicts of interest, the appropriate use of superannuation fund reserves and the need to put members’ interests above any competing priorities.

APRA had initiated the action last December due to its view that IOOF entities, directors and executives had failed to act in the best interests of their superannuation members. Before taking the court action, APRA had sought to resolve concerns with IOOF over several years but considered that it was necessary to take stronger action – through use of directions, conditions and court action – after concluding the company was not making adequate progress, or likely to do so in an acceptable period of time.

After receiving the judgment on 20 September, APRA reviewed the reasons for the decision and concluded that it will not appeal the matter.

APRA Deputy Chair Helen Rowell said the judgment nevertheless raised some issues of wider importance for APRA in its supervision of superannuation trustees. APRA is considering any further action that may need to be taken in relation to these, such as revising its prudential standards or seeking legislative amendments, to ensure that member interests are protected to the maximum extent possible.

APRA notes that, notwithstanding the decision not to appeal the judgment, additional licence conditions that APRA imposed on IOOF in December remain in force and APRA’s strengthened supervision focus on ensuring that IOOF implements the changes needed to comply with these conditions continues.

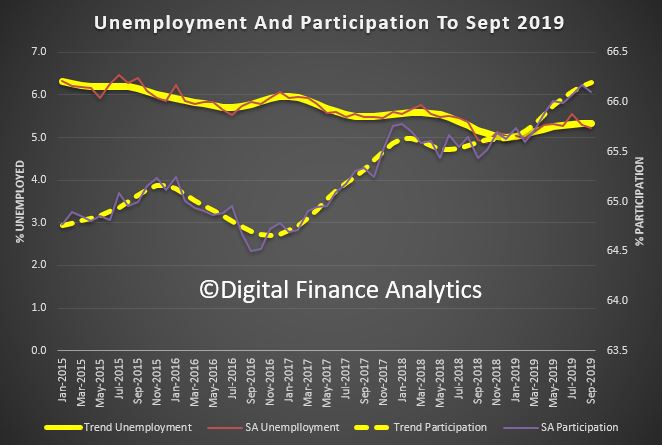

Australia’s trend unemployment rate remained steady at 5.3 per cent in September 2019, according to the latest information released by the Australian Bureau of Statistics (ABS).

“All of Australia’s key trend measures remained steady in September 2019, with the unemployment rate at 5.3 per cent and the participation rate at 66.2 per cent.” said ABS Chief Economist Bruce Hockman.

Employment and hours

In September 2019, trend monthly employment increased by around 20,200 people. Full-time employment increased by about 9,000 people and part-time employment increased by about 11,300 people.

Over the past year, trend employment increased by about 300,000 people (2.4 per cent), which continued to be above the average annual growth over the past 20 years (2.0 per cent). Full-time employment increased by 2.1 per cent and part-time employment increased by 2.9 per cent over the past year.

The trend monthly hours worked increased by 0.1 per cent in September 2019 and by 1.8 per cent over the past year. This was slightly above the 20 year average year-on-year growth of 1.7 per cent.

Annual Employment Change Over 20 Years (%)

Underemployment and underutilisation

The trend monthly underemployment rate remained steady at 8.4 per cent in September 2019, an increase of 0.1 percentage points over the past year. The trend monthly underutilisation rate remained steady at 13.7 per cent, an increase of 0.2 percentage points over the past year.

States and territories trend unemployment rate

The monthly trend unemployment rate remained steady in half of the states and territories in September 2019. Unemployment rate changes occurred in the Northern Territory (up 0.2 percentage points), Queensland and South Australia (up 0.1 percentage points) and Western Australia (down 0.1 percentage points).

Over the year, unemployment rates fell in Western Australia and the Australian Capital Territory, and increased in Victoria, Queensland, South Australia, Tasmania and the Northern Territory.

Seasonally adjusted data

The seasonally adjusted unemployment rate decreased by less than 0.1 percentage points to 5.2 per cent in September 2019, while the underemployment rate decreased by 0.2 percentage points to 8.3 per cent. The seasonally adjusted participation rate decreased by less than 0.1 percentage points to 66.1 per cent, and the number of people employed increased by an estimated 14,700.

The net movement of employed in both trend and seasonally adjusted terms is underpinned by around 300,000 people entering and leaving employment in the month.

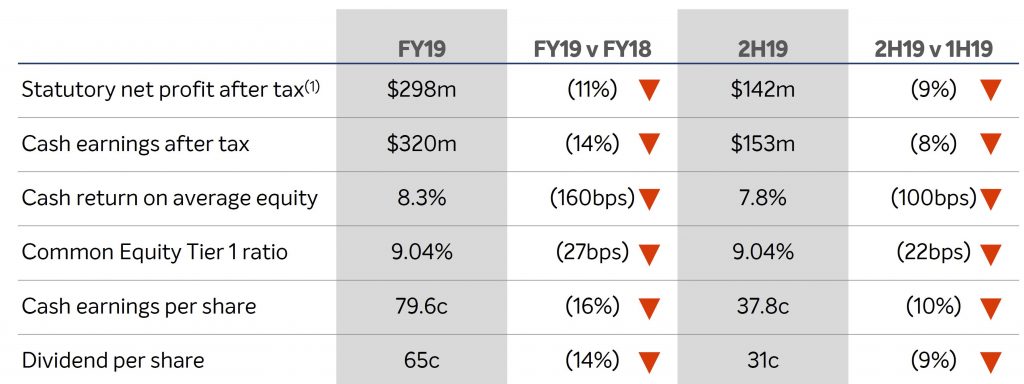

Bank of Queensland today announced FY19 cash earnings after tax of $320 million, down 14 per cent on FY18. Statutory net profit after tax decreased by 11 per cent to $298 million. Basic cash earnings per share was down 16 per cent to 79.6 cents per share. We expect many banks to report a similar story ahead.

The Board has announced a final dividend of 31 cents per share, for a full year dividend of 65 cents per share. This is a reduction of 11 cents per share from FY18. The final dividend payout ratio of 82% was consistent with the interim dividend payout ratio.

They described this as “Disappointing results reflect challenging operating environment”, reflecting a challenging operating environment characterised by slowing credit demand, lower interest rates, a rise in regulatory costs and changes impacting non-interest income.

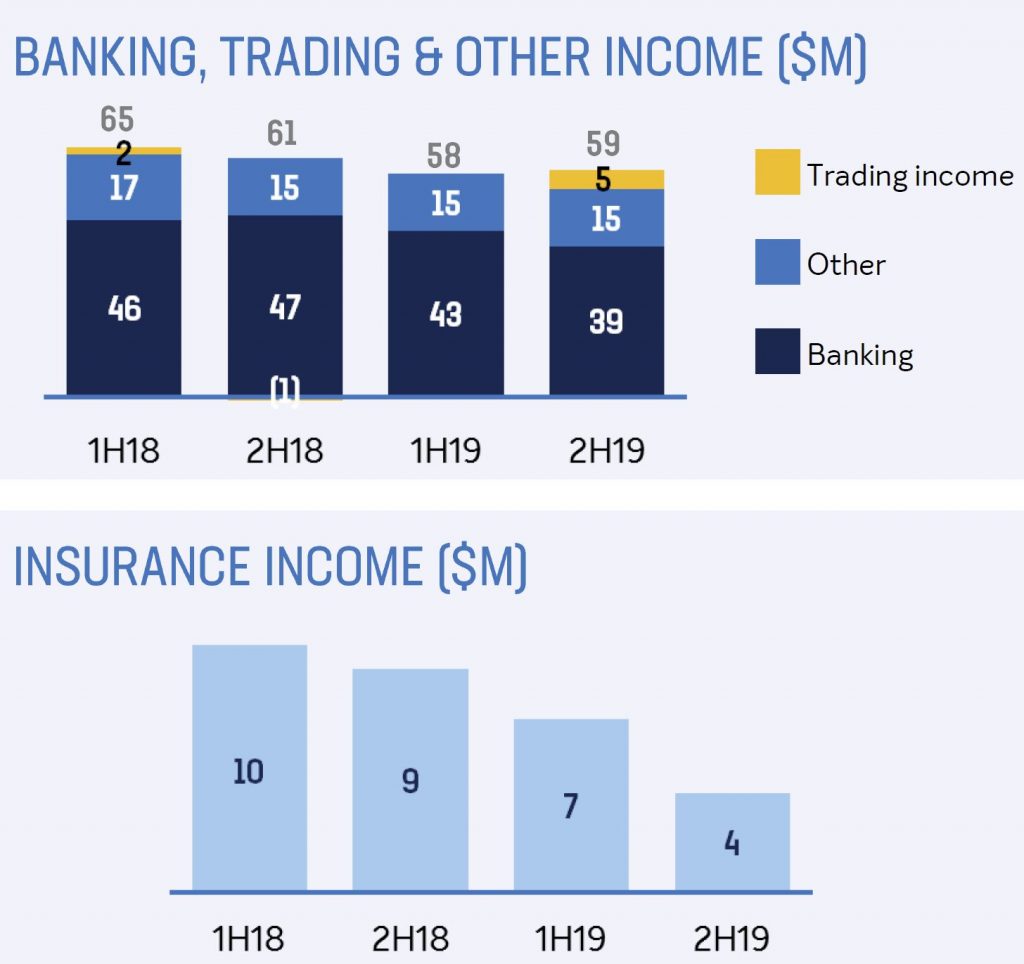

Total income decreased by $21 million or two per cent from FY18.

Net interest income decreased $4 million, driven primarily by a five basis point reduction in net interest margin to 1.93 per cent. This reduction is attributable to the declining interest rate environment and continued strong competition for loans and deposits.

Non-interest income decreased 12 per cent or $17 million, driven by declines in Banking, Insurance and Other income but partially offset by improved Trading income. Banking income reduced $11 million due to lower fee income and a change in arrangements related to BOQ’s merchant offering. Insurance income reduced $8 million or 42 per cent due to changes in the insurance sector which ultimately impacted distribution of St Andrew’s consumer credit insurance through its corporate partners.

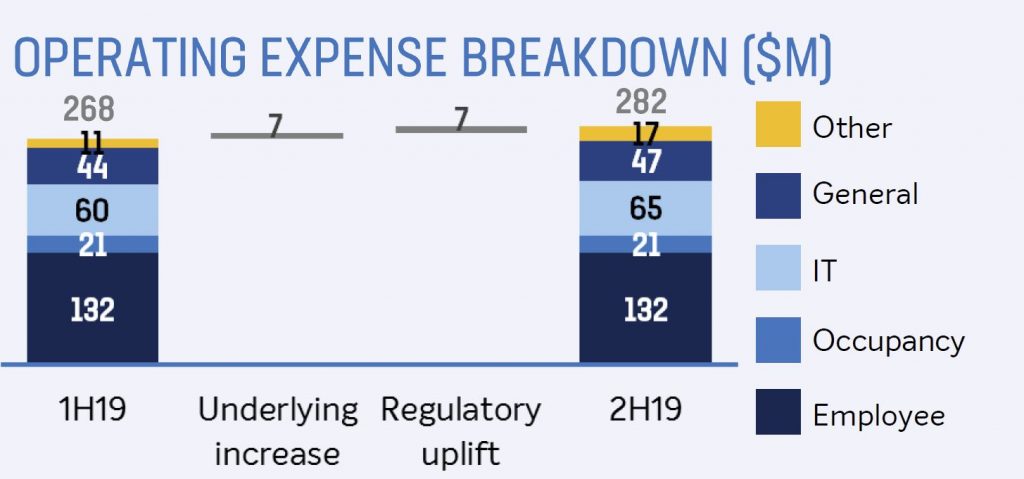

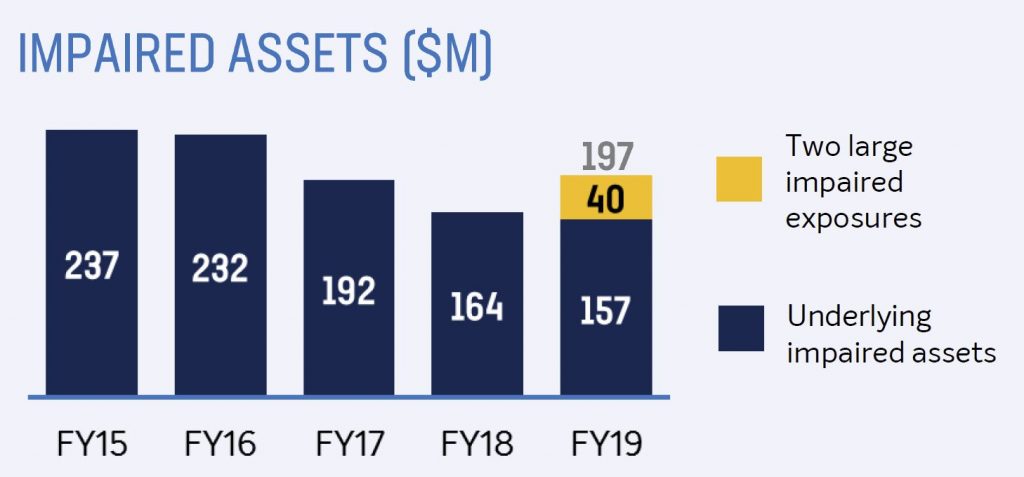

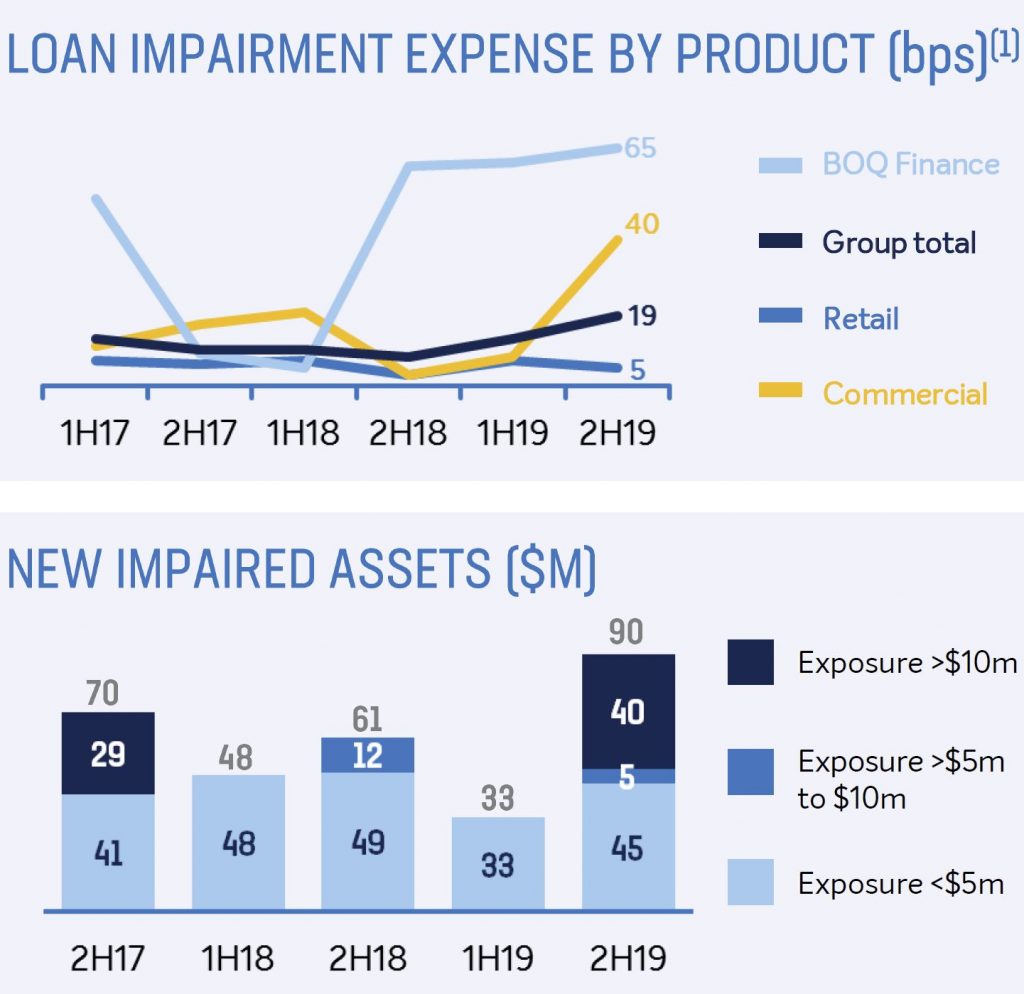

In line with the guidance provided at the 1H19 result, operating expenses increased by $23 million or four per cent from FY18. The increase in expenses was more pronounced in the second half, due to an increase in business deliverables addressing regulatory and compliance requirements. While loan impairment expense increased $33 million to $74 million, equivalent to 16 basis points of gross loans, underlying asset quality remains sound with impairments and arrears remaining at low levels.

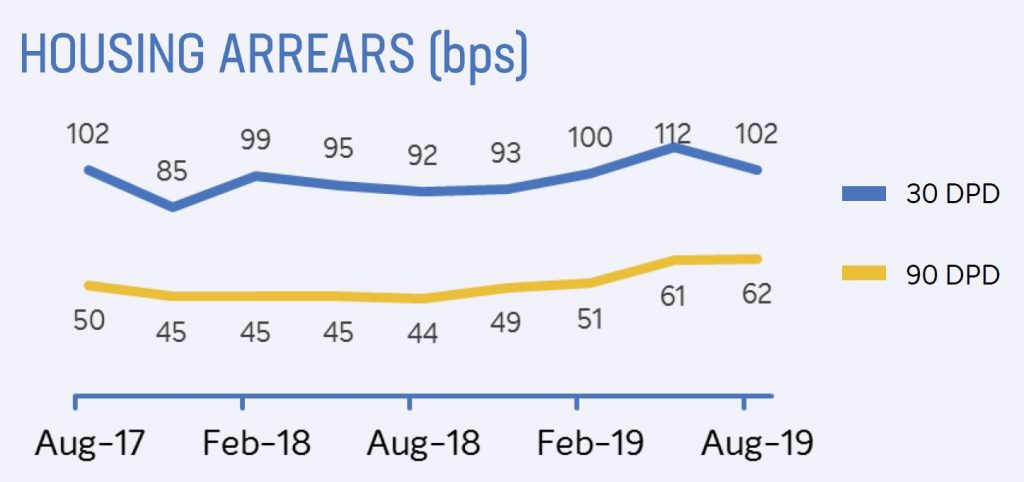

Housing loan arrears over 90 days rose, while 30 day fell.

Implementation of BOQ’s new AASB 9 collective provision model drove an increase in collective provisions due to changes in BOQ’s portfolio and a weaker economic outlook. The increase in collective provisions contributed $22 million of the loan impairment expense uplift.

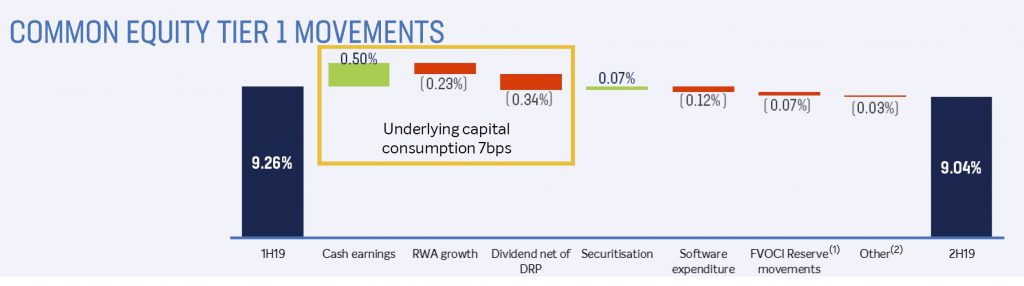

BOQ remains appropriately capitalised with a Common Equity Tier 1 ratio of 9.04 per cent, which is a decrease of 27 basis points from FY18. The reduction was driven by a combination of asset growth being tilted to more capital intensive business lines, increased capitalised investment, reduced earnings and lower participation in the dividend reinvestment plan.

Overall lending growth of two per cent was achieved over the year.

Continued growth momentum was evident in BOQ’s niche business segments. The BOQ Finance portfolio achieved growth of $667 million or 15%, while BOQ Specialist grew lending balances by $756 million across its commercial and housing loan portfolios which are focused on the medical segment. Virgin Money also delivered a consistently strong level of housing loan growth, with the portfolio growing by $914 million to over $2.5 billion.

A key imperative remains rebuilding the foundation for growth in BOQ’s retail bank, which saw a further contraction of $1.4 billion in its residential housing loan book.

Solid progress has also been made across a number of key foundational investments during the year. BOQ’s core technology infrastructure modernisation program has continued to track to plan, with implementation continuing through FY20. This will deliver a more modern, cloud-based technology environment which will allow for improved change capability.

During the year, work began on development of a new mobile banking application for BOQ customers, with a launch expected in 2020. Lending process improvements have also been a key focus to improve customer experience, particularly for home loan applications. A number of regulatory projects have also progressed during the year to address various regulatory and industry changes. These are all critical investments that will support BOQ’s transformation and future aspirations.

Investment in the implementation of a new Virgin Money digital bank has also progressed during the year, with a customer launch planned for 2020. This will require $30 million of capitalised investment during FY20 to complete the phase one build which will deliver a transaction and savings account offering to customers. This is an investment in long term value creation for this iconic brand which has demonstrated success in attracting customers across its existing product suite. It is also anticipated that this investment in a new digital banking platform will be leveraged across the Group in the years ahead.

Commenting on the results and outlook for BOQ, new Managing Director & CEO George Frazis said that there are challenges ahead, however fundamentally, BOQ is a good business.

“Our capital is well positioned for ‘unquestionably strong’, we have a good funding position and our underlying asset quality is sound. “There are numerous opportunities ahead for a revamped BOQ and I will be working closely with the executive leadership team to complete our strategic and productivity review, with a market update on our plans in February 2020,”

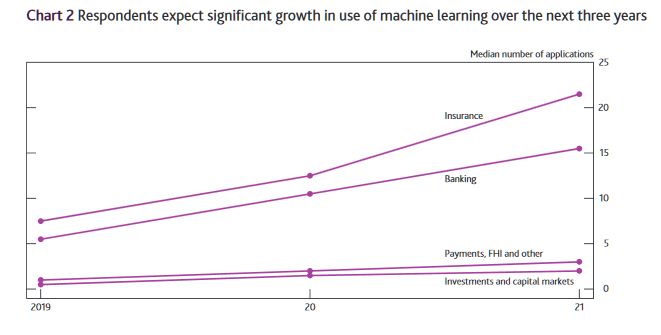

The Bank of England (BoE) and Financial Conduct Authority (FCA) have a keen interest in the way that ML is being deployed by financial institutions.

They conducted a joint survey in 2019 to better understand the current use of ML in UK financial services. The survey was sent to almost 300 firms, including banks, credit brokers, e-money institutions, financial market infrastructure firms, investment managers, insurers, non-bank lenders and principal trading firms, with a total of 106 responses received.

In the financial services industry, the application of machine

learning (ML) methods has the potential to improve outcomes for both

businesses and consumers. In recent years, improved software and

hardware as well as increasing volumes of data have accelerated the pace

of ML development. The UK financial sector is beginning to take

advantage of this. The promise of ML is to make financial services and

markets more efficient, accessible and tailored to consumer needs. At

the same time, existing risks may be amplified if governance and

controls do not keep pace with technological developments. More broadly,

ML also raises profound questions around the use of data, complexity of

techniques and the automation of processes, systems and

decision-making.

The survey asked about the nature of deployment of ML, the business

areas where it is used and the maturity of applications. It also

collected information on the technical characteristics of specific ML

use cases. Those included how the models were tested and validated, the

safeguards built into the software, the types of data and methods used,

as well as considerations around benefits, risks, complexity and

governance.

Although the survey findings cannot be considered to be statistically

representative of the entire UK financial system, they do provide

interesting insights.

The key findings of the survey are:

ML is increasingly being used in UK financial services. Two thirds of respondents report they already use it in some form. The median firm uses live ML applications in two business areas and this is expected to more than double within the next three years.

In many cases, ML development has passed the initial development phase, and is entering more advanced stages of deployment. One third of ML applications are used for a considerable share of activities in a specific business area. Deployment is most advanced in the banking and insurance sectors.

From front-office to back-office, ML is now used across a range of business areas. ML is most commonly used in anti-money laundering (AML) and fraud detection as well as in customer-facing applications (eg customer services and marketing). Some firms also use ML in areas such as credit risk management, trade pricing and execution, as well as general insurance pricing and underwriting.

Regulation is not seen as a barrier but some firms stress the need for additional guidance on how to interpret current regulation. Firms do not think regulation is a barrier to ML deployment. The biggest reported constraints are internal to firms, such as legacy IT systems and data limitations. However, firms stressed that additional guidance around how to interpret current regulation could serve as an enabler for ML deployment.

Firms thought that ML does not necessarily create new risks, but could be an amplifier of existing ones. Such risks, for instance ML applications not working as intended, may occur if model validation and governance frameworks do not keep pace with technological developments.

Firms use a variety of safeguards to manage the risks associated with ML. The most common safeguards are alert systems and so-called ‘human-in-the-loop’ mechanisms. These can be useful for flagging if the model does not work as intended (eg. in the case of model drift, which can occur as ML applications are continuously updated and make decisions that are outside their original parameters).

Firms validate ML applications before and after deployment. The most common validation methods are outcome-focused monitoring and testing against benchmarks. However, many firms note that ML validation frameworks still need to evolve in line with the nature, scale and complexity of ML applications.

Firms mostly design and develop ML applications in-house. However, they sometimes rely on third-party providers for the underlying platforms and infrastructure, such as cloud computing.

The majority of users apply their existing model risk management framework to ML applications. But many highlight that these frameworks might have to evolve in line with increasing maturity and sophistication of ML techniques. This was also highlighted in the BoE’s response to the Future of Finance report. In order to foster further conversation around ML innovation, the BoE and the FCA have announced plans to establish a public-private group to explore some of the questions and technical areas covered in this report.

The major capital cities are seeing

property prices shoot back up thanks to interest rate cuts and an easing

of lending buffers. With auction clearance rates back near all time

highs, is the property downturn now well or truly over or will a new

round of frenzied bidding result in more debt-fuelled instability.

In this episode, Adam Creighton, economics editor of The Australian pits noted bear Martin North, who believes property prices could fall as much as 40 per cent, against Nerida Conisbee, chief economist of realestate.com.au.

Global growth is forecast at 3.0 percent for 2019, its lowest level since 2008–09 and a 0.3 percentage point downgrade from the April 2019 World Economic Outlook.

Growth is projected to pick up to 3.4 percent in 2020 (a 0.2 percentage point downward revision compared with April), reflecting primarily a projected improvement in economic performance in a number of emerging markets in Latin America, the Middle East, and emerging and developing Europe that are under macroeconomic strain.

Yet, with uncertainty about prospects for several of these countries, a projected slowdown in China and the United States, and prominent downside risks, a much more subdued pace of global activity could well materialize. To forestall such an outcome, policies should decisively aim at defusing trade tensions, reinvigorating multilateral cooperation, and providing timely support to economic activity where needed. To strengthen resilience, policymakers should address financial vulnerabilities that pose risks to growth in the medium term. Making growth more inclusive, which is essential for securing better economic prospects for all, should remain an overarching goal.

Australian growth is downgraded to 1.7%

Bearing in mind our dependency on iron ore, they say: Iron ore prices increased 6.7 percent between February 2019 and August 2019. Widespread disruptions—including the Vale dam collapse in Brazil and tropical cyclone Veronica in Australia— coupled with record-high steel output in China pushed iron ore prices to five-year highs during the first half of 2019. However, the normalization of previously disrupted operations and escalating trade tensions between the United States and China triggered a sharp correction in August, partially offsetting the gains since the beginning of the year.