A former Macquarie banker says hazy guidelines around lending will cause problems for the next six months following the Westpac case, predicting the big four banks will corner ASIC and demand clearer standards, according to an exclusive in InvestorDaily today.

During

a panel discussion at The REAL Future of Advice Conference in Vietnam

this week, former Macquarie head of sales and distribution for

mortgages, Tim Brown, noted the recent Federal Court decision ruling in

the favour of Westpac.

ASIC

had taken Westpac to court over allegations it breached lending laws

between 2011 and 2015 by using the household expenditure measure to

estimate potential borrowers’ living expenses.

ASIC had argued the benchmark was too frugal and that customers’ expenses were higher.

Mr

Brown, who is currently the chief executive of Ezifin Financial

Services, called the current lending landscape a “minefield” where

lenders “can’t get clarification from ASIC” over standards for

evaluating consumers’ eligibility for mortgages.

“I

think the problem with this whole expense discussion, as I was pointed

out earlier on is that a lot of the assessors put their own personal

assessment on what someone else spends money on, which is where the

problem lies,” Mr Brown said.

“It needs to be much more factual.

“I

think it is going to be a problem for at least another six months until

some of the banks get together with ASIC and say look we need to get

some clear guidelines around this. Because they’re basically saying HEM

isn’t acceptable anymore.”

Mr

Brown noted when he first started lending, brokers would sit with

clients, go through their expenses and make sure they had enough

capacity to meet any future increases and interest rates, by using HEM

and allowing up to two and a half per cent above the current rate.

Reflecting on his expenses when buying his first house, said he did not think he would have passed current standards.

“But

within the first six months of buying a home, and we know this

factually and we’ve recently seen ASIC having these discussions, that

most people will reduce their discretionary spending by 20 per cent.

“Now,

most assessors in the past could make that decision without any

concern. But in the current environment, they are afraid to make those

decisions now because there’s a way around it and ASIC might review

that. And this comes back to this personal assessment of someone else’s

opinion on what someone should have a discretionary not a discretion.

“Because

ASIC just goes ‘well you know best endeavors, you know, whatever you

think is reasonable.’ And then they’ll charge you if they don’t think

it’s reasonable.”

‘We want some direction’

Talking

about missing clarity from ASIC, Mr Brown said: “The banks are sick of

this game that they’re playing with ASIC at the moment and eventually

the four of them will get together and say look, you need to give us

some clear guidelines.”

“At

the moment, I think the industry bodies are trying to come together

with something they can take to ASIC both from a vendor’s perspective

and also from a MFAA (Mortgage and Finance Association of Australia) and

FBAA (Finance Brokers Association of Australia).”

Mr Brown noted every time he had been on a panel, he had been asked about the Westpac decision.

“There’s obviously a real concern among the number of people at the moment,” he said.

Fitch Ratings says residential mortgage loans in Scandinavia, the Netherlands and Switzerland have seen exceptionally strong performance despite high loan-to-value (LTV) ratios and significant household debt. This reflects generous social security systems and large household wealth, which are a common denominator of these ‘AAA’ rated jurisdictions with strong public finances.

The growth of housing

debt in Scandinavia, the Netherlands and Switzerland can be explained

by a combination of tax deductibility, low interest rates, and unique

features of each respective mortgage market. These include long

contractual tenors and interest-only periods. Limited repayment has made

borrowers more sensitive to house price decreases. However,

macro-prudential requirements in each country are helping to address the

risk that high household debt could jeopardise financial stability.

Macro-prudential

measures were originally focused on maximum LTV and stressed

affordability at origination, but lower mortgage rates continued to

stimulate mortgage growth. Banking authorities therefore imposed minimum

mortgage loan amortisation as well as maximum loan-to-income (LTI) or

debt-to-income ratios. Such restrictions have contributed to the recent

adjustment in Norwegian and Swedish house prices and limited lending

growth in Denmark. Swiss regulators have tightened capital requirements

for banks and promoted self-regulation, which established minimum

amortisation for mortgages above 66% LTV. Gradual changes to tax

incentives and underwriting standards were introduced by the Dutch

authorities, especially since 2013, which have made the mortgage market

more resilient.

The latest discussion with Chris Bates, mortgage broker and financial planner, as we dissect the latest trends. Property prices higher, maybe in some places, but there are other more critical trends in play, and prospective buyers need to be careful!

Chris can be found at www.wealthful.com.au & www.theelephantintheroom.com.au plus via LinkedIn: https://www.linkedin.com/in/christopherbates

Australia’s customer owned

banking sector welcomes reports that the Australian Competition and Consumer

Commission (ACCC) is requesting to conduct an inquiry into the banking

industry’s competitiveness.

Customer Owned Banking Association CEO Michael Lawrence

says the request from the ACCC and the comments from Tim Wilson MP were

encouraging for credit unions, building societies and mutual banks who have

been leading the charge for a more competitive retail banking market.

“The enduring solution to concerns about the banking

market is action to promote competition.

“We don’t have sustainable banking competition at

the moment. A lack of competition can contribute to inappropriate conduct

by firms, and insufficient choice, limited access and poor-quality products for

consumers.

“We strongly support the ACCC’s calls for an

inquiry to examine the banking industry’s competitiveness. It’s encouraging to

see that the ACCC and Tim Wilson MP share our sector’s concerns about

competition and what an uncompetitive banking market means for consumers.

“Last year’s Productivity Commission’s report on

competition in banking sent strong messages to regulators and policymakers that

regulation is hurting competition and consumers are paying the price.

“The regulatory framework over time has

entrenched the dominant position of the largest banks.

“The PC report shone a light on a problem that is not

well enough recognised – that more and more regulation can be harmful to

consumers because it weakens competition.

“The Productivity Commission found that competition

drives innovation and overall value for customers.

“The Financial Services Royal Commission

looked into misconduct, now is the time to look into competition.”

ASIC says Australian financial services (AFS) licence holder ClearView Financial Advice Pty Ltd (ClearView) has completed a review and remediation program for over 200 clients who received poor life insurance advice.

Under this program, ClearView reviewed 4,269 advice files from 279 of

its advisers and remediated clients who had suffered loss. 215 clients

were offered $730,138 in financial compensation and 21 clients received

non-financial remediation through reissued advice documents and fee

disclosure.

ASIC first identified issues of non-compliant advice by ClearView’s

representatives during an industry-wide review of retail life insurance

in 2014 (14-263MR).

A sample review of ClearView’s advice files highlighted broad areas

of concern such as inadequate needs analysis for client, insufficient

explanation about the pros and cons of using superannuation to fund

insurance premiums, inadequate consideration of premium affordability

issues and poor disclosure about replacement products. ASIC raised these

issues as well as some concerns related to the conduct of Jason

Churchill, one of ClearView’s advisers at the time.

In 2016, ASIC accepted an enforceable undertaking (EU) from Mr

Churchill for failure to meet his obligations as a financial adviser (16-008MR).

Under the EU, Mr Churchill agreed to undergo additional training,

adhere to strict supervision requirements and have each piece of advice

audited by his authorising licensee before it was provided to clients.

Separately, ClearView undertook to review advice previously provided by

Mr Churchill and remediate clients who had received inappropriate

advice.

ClearView also began a review of the personal insurance advice

provided by its advisers to determine if there was a systemic issue

related to the broad areas of concern identified by ASIC and engaged

Deloitte to provide independent oversight. This review found that a

number of ClearView’s advisers did not undertake adequate ‘needs

analysis’ for clients.

The needs analysis is a critical part of the financial advice

process. It enables advisers to understand their clients’ financial

situation, needs and objectives, and provides the basis for the

financial advice.

To identify all instances of this issue and to remediate any

adversely affected clients, ClearView undertook a full review and

remediation program in accordance with Regulatory Guide 256: Client review and remediation conducted by advice licensees

(RG 256). Deloitte oversaw the review and remediation program to

ensure that it was conducted in accordance with the principles set out

in RG 256.

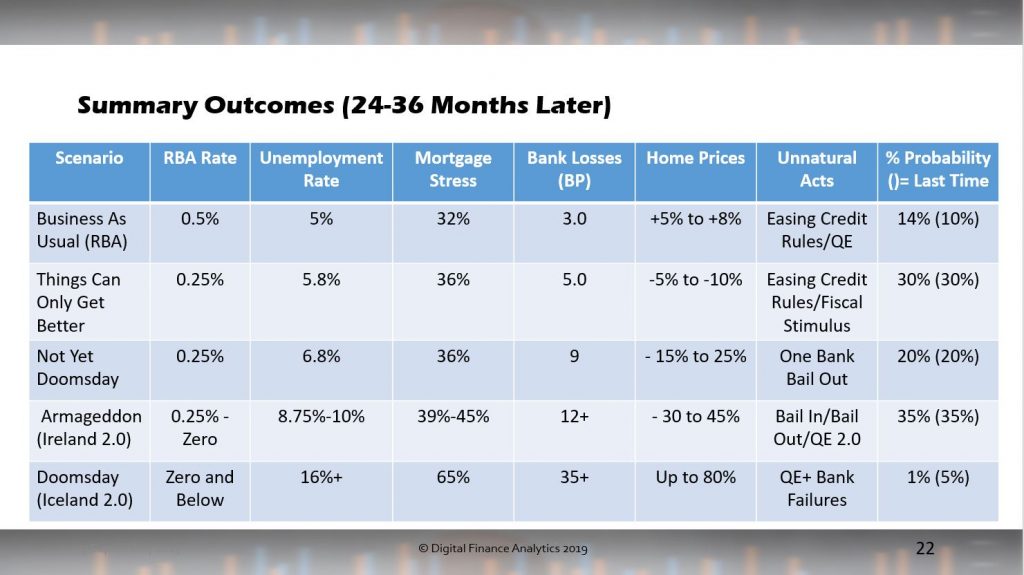

We ran our September 2019 live event last night with strong participation from our audience. During the show we discussed our updated scenarios (based on a starting point of August 2018) and answered a range of questions on property and finance.

The edited edition of the show is available to view in replay. This excludes the pre-show and live chat, but does include some behind the scene glimpses.

Our scenarios present a range of alternative outcomes, looking 2-3 years out. “Business As Usual” is based on the RBA’s view, with some tweaks – as we do not believe unemployment will fall to their target of 4.5%! Here there is a path to higher home prices, though with falls later as the current “recovery” reverses.

“Things Can Only Get Better” – is our view of the fading local economy without significant international economic disruption, with unemployment rising, as retail and construction slows, countered by additional Government intervention within their “surplus” limits. Here home prices fall once again.

“Not Yet Doomsday” is our scenario where international economic conditions deteriorate (China, US, Brexit Etc…) as global growth slows. This has a significant impact on the local economy and the spillover effects drive the Australian economy into recession. As liquidity pressures emerge one bank will need assistance.

“Armageddon” is where we get a GFC 2.0 type event, with global liquidity under pressure, and banks needing to be rescued by either bailing in or bailing out. The spillover impacts will be significant (as once again tax payers or households end up picking up the tab. More QE will follow.

Finally “Doomsday” would be the case where Central Banks and Governments allow banks to fail, with all the knock-on consequences.

As well as estimating the impact on unemployment and home prices we also weight the probability of each outcome. This is updated each month as new information arrives via our Core Market Model.

The original live stream recording is also available, with the show commencing at 30 mins in to allow for the live chat replay.

More on the Cash Restriction Bill with Robbie Barwick from the CEC.

The Liberal/Nationals joint party room agreed to support the bill, despite the 4,000 or so public submissions not posted by Treasury, and the details of the bill yet to be released. Democracy at work?

Use and share these links for finding MPs and Senators.

Click the link, and find the heading State/Territory in the box titled Refine Search on the right hand side of the page. Click on your state and call as many MPs and Senators as you can, on their Parliament House numbers, starting with 02-6.

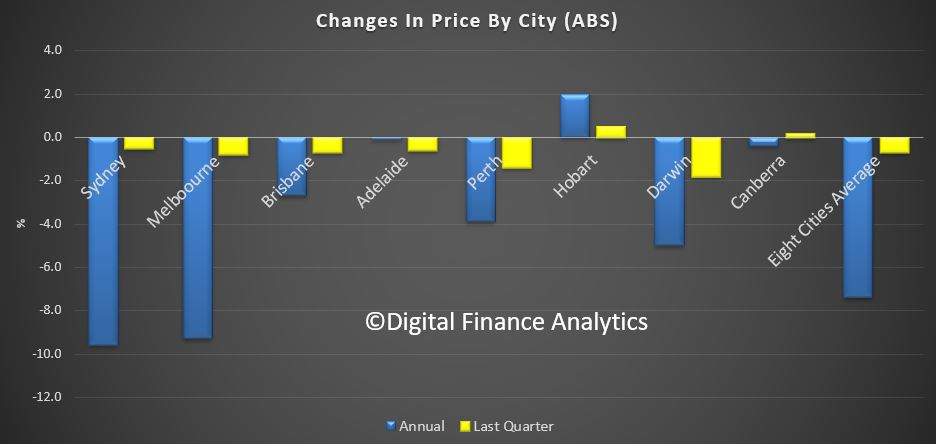

The ABS released their price data series to end June, so late as to be little more than a historical artifact, given the rate cuts, APRA changes and other events. Since June the kitchen sink has been thrown to try to force prices higher, though lead indicators are weakening again now. The total value of Australia’s 10.3 million residential dwellings fell by $17.6 billion to $6,610.6 billion in the June quarter 2019.

Residential property prices fell 0.7 per cent in the June quarter 2019, according to figures released today by the Australian Bureau of Statistics (ABS).

The falls in property prices were led by the Melbourne (-0.8 per cent) and Sydney (-0.5 per cent) property markets. All capital cities apart from Hobart (+0.5 per cent) and Canberra (+0.2 per cent) recorded falls in property prices in the June quarter 2019.

ABS Chief Economist Bruce Hockman said, “The falls in Melbourne were driven by detached dwellings, while attached dwellings drove the fall in Sydney”.

Through the year, residential property prices fell 7.4 per cent in the June quarter 2019. Prices fell 9.6 per cent in Sydney and 9.3 per cent in Melbourne. Hobart (+2.0 per cent) was the only capital city to record positive through the year growth.

“Sydney and Melbourne housing markets have seen residential property price falls moderate this quarter. A number of housing market indicators, such as auction volumes and clearance rates, have begun to show signs of improvement, though they remain below the levels seen one year earlier”, said Mr Hockman.

The total value of Australia’s 10.3 million residential dwellings fell by $17.6 billion to $6,610.6 billion in the June quarter 2019. The mean price of dwellings in Australia is now $638,900. The total value of residential dwellings has fallen for five consecutive quarters, down from $6,957.2 billion in the March quarter 2018.

The RBA released their minutes today. Clear talk of more cuts, against a weaker global scene. But holding on to households spending more as the housing sector wakens. Rates will be lower for longer as Central Banks globally cut to the max. Saved somewhat by Government spending and higher iron ore price, but small businesses not borrowing, and households not spending.

International Economic Conditions

Members commenced their discussion of the global economy by noting that business conditions in the

manufacturing sectors in many economies had remained subdued. They discussed the escalation of the

US–China trade and technology disputes, which had intensified the downside risks to the global

outlook. By contrast, conditions in more domestically focused sectors had generally continued to be

resilient, supported by ongoing strength in labour markets. Employment growth had remained robust in the

major advanced economies, although it had eased a little in some economies in recent months, and

unemployment rates had remained low. Although wages growth had picked up, year-ended inflation had

remained below target in the major advanced economies. Members noted that inflation in the United States

had increased in recent months.

The main development over the previous month had been the escalation of the US–China trade and

technology disputes. The United States had announced higher tariffs on most imports from China,

including consumer goods that had not previously been subject to the tariff increases, to take effect

over the remainder of 2019. Members noted that recent and prospective increases in tariffs could

increase consumer price inflation in the United States by between ¼ and ½ percentage

point over the following few years, based on a range of published estimates. In response to the US

announcements, China had suspended purchases of US agricultural products and had announced plans to

increase tariffs on around one-half of the value of US imports. In value terms, US exports to China

had contracted by around 20 per cent over the year to June, while US imports from China

had been around 3 per cent lower. Members also noted that some other east Asian economies were

benefiting from the diversion of US imports away from China.

More generally, global trade volumes had fallen over the previous year, reflecting both the escalation

of trade tensions and slower growth in Chinese domestic demand. Weak external demand had been reflected

in slowing growth in global industrial production and below-average conditions in the global

manufacturing sector. Recent indicators suggested trade-related activity would remain weak for some

time.

Members noted that weak external demand and heightened geopolitical uncertainty had contributed to

lower growth in business investment in many economies, including the United States, the euro area and

the United Kingdom. These economies had also recorded declines in investment intentions. By contrast, in

the United States the household sector had been resilient, but overall GDP growth had slowed in the June

quarter. GDP growth had also slowed in most euro area countries in the June quarter; Germany had

recorded a small contraction in GDP. By contrast, GDP growth in Japan had been moderate, supported by

consumption brought forward ahead of a scheduled increase in the consumption tax in October, as well as

ongoing growth in investment, bolstered by the need to address labour shortages.

Recent data suggested that growth in China had eased further. Most indicators of economic activity had

slowed in July, including in components being supported by recent policy measures, such as

infrastructure investment. The level of steel production had declined slightly. Retail sales growth had

resumed its downward trend, after having received a boost from strong growth in car sales in recent

months ahead of tighter emission standards coming into effect. In India, recent indicators had also

pointed to output growth slowing.

Weak global trade had continued to weigh on growth in east Asia. Trade within the region and with China

had contracted further in June. Growth in industrial production and survey measures of manufacturing

conditions had remained weak. Political unrest had weighed on economic conditions for businesses and

households in Hong Kong, while an ongoing dispute with Japan had disrupted South Korean production of

electronics. However, domestic demand elsewhere in the region had held up, supported by government

policies in some cases.

Iron ore prices had declined since the previous meeting, but were around 40 per cent higher

than a year earlier. Market reports had attributed these declines to a number of factors, including

concerns about the outlook for steel demand in China following the escalation of the disputes between

the United States and China in early August, lower steel prices and an easing in supply concerns. The

prices of coal and rural commodities had been somewhat lower over the prior month, while oil and base

metals prices had been little changed, except where there had been disruptions to the supply of specific

metals.

Domestic Economic Conditions

The main information on the domestic economy received since the previous meeting had been on the labour

market as well as partial indicators of output growth in the June quarter in the lead-up to the

publication of the national accounts. Quarterly GDP growth was expected to be around

½ per cent, supported by a strong recovery in resource exports from earlier supply

disruptions.

The ABS capital expenditure (Capex) survey suggested that mining investment had grown in the June

quarter, driven by an increase in machinery & equipment investment. The Capex survey suggested there

had also been an increase in machinery & equipment investment by the non-mining sector in the June

quarter, while non-residential construction was expected to have declined. Investment intentions for

2019/20 had been positive for the mining sector, but had been modestly

lower for the non-mining sector. Members noted that the outlook for the construction sector was

particularly weak.

Members recognised that, overall, Australian businesses had not appeared to have been affected by the

weak trade environment to the same extent as businesses in other advanced economies. This was partly

because Australia’s exports are more exposed to Chinese domestic demand and less integrated in

global supply chains.

Consumption growth was expected to have remained low in the June quarter. Retail sales volumes had been

weak in the June quarter and the value of retail sales had fallen in July. The low- and middle-income

tax offset (LMITO) was expected to boost household income, and thus support consumption growth, in

coming quarters. However, the Bank’s liaison with retailers suggested that this had yet to lift

spending noticeably. Members noted that even if the LMITO was used to pay off debts, this would still

bring forward the point at which households could increase their spending.

Established housing market conditions had steadied in recent months. Reported housing prices in Sydney

and Melbourne had risen noticeably in August and auction clearance rates had increased further, although

volumes had remained low. Housing market conditions had been subdued elsewhere, although there were

signs of housing prices stabilising in Brisbane. Housing turnover had remained low. Consequently,

spending on home furnishings and other housing-related items was not expected to contribute to

consumption growth in the near term. Indicators suggested that dwelling investment had declined further

in the June quarter and indicators of earlier stages of residential building activity had remained weak;

building approvals had declined further in June and other measures of early-stage activity and buyer

interest had remained at low levels.

Employment growth had remained strong in July, but the unemployment rate had remained at

5.2 per cent. Employment growth over preceding months had been broadly based across states and

had predominantly been in full-time work. Strong employment growth had been accompanied by a further

increase in the participation rate, which had recorded another all-time high. Members noted that the

increase in participation had been particularly notable for New South Wales. Forward-looking indicators

had continued to suggest that employment growth would moderate over the following six months.

Information from liaison suggested employment intentions had remained weak in the residential

construction sector but positive among services firms.

Wages growth had remained low and the upward trend in wages growth appeared to have stalled. The wage

price index had increased by 2.3 per cent over the year to the June quarter. Private sector

wages growth had been unchanged in the quarter, while public sector wages growth had been a little

higher. Most of this increase had been the result of a one-off adjustment to equalise the wages of

nurses and midwives in Victoria with those in New South Wales.

Financial Markets

Members commenced their discussion of financial markets by noting that government bond yields had

declined and were at record lows in many countries, including Australia. Volatility and risk premiums in

global financial markets had increased in August, following the escalation of the disputes between the

United States and China and disappointing economic data releases in Germany and China. The persistent

downside risks to the global economy, combined with subdued inflation, had led a number of central banks

to reduce interest rates in recent months and further monetary easing was widely expected.

In the United States, market pricing implied that the federal funds rate was expected to decline by

around 100 basis points over the following year. Market participants also expected the European

Central Bank to provide additional monetary stimulus in the near term, including renewed asset purchases

and a reduction in its policy rate further into negative territory. Central banks in a number of other

advanced economies had also eased policy, or signalled that they were prepared to do so, in response to

subdued inflation, moderating activity and downside risks to growth. For similar reasons, central banks

in emerging markets had also been easing policy over recent months and had signalled the possibility of

further easing.

Financial conditions for corporations remained accommodative globally. This reflected market

participants’ ongoing expectations that central banks were likely to deliver further monetary

easing to sustain the global economic expansion. Corporate bond spreads had increased a little in

August, but remained low. Equity prices had declined somewhat, reflecting concerns about the outlook for

growth, but remained substantially higher over the year to date. In Australia, equity prices were

5 per cent below the record high reached in late July. Australian listed companies’

profits had risen, driven by the resources sector. At the aggregate level, companies had increased their

dividends over the preceding year, although this reflected higher dividends in the resources sector in

particular.

In China, the authorities had intervened to support three small banks in preceding months, and the

People’s Bank of China had continued to maintain a high level of liquidity in the banking system.

While funding conditions for smaller banks had tightened this year, money market rates and corporate and

government bond yields in China had generally remained low and market participants were expecting

further easing in monetary policy in the period ahead.

In foreign exchange markets, the Chinese renminbi had depreciated against the US dollar in August

following the escalation of the US–China disputes, while the Japanese yen had appreciated over

the month. The Australian dollar had been little changed at around its lowest level in some years.

In Australia, borrowing rates for both businesses and households were at historically low levels, as

were banks’ funding costs. Variable mortgage rates had declined broadly in line with the reductions

in the cash rate in June and July. Fixed mortgage rates had also declined substantially over the

preceding six months. Financial market pricing continued to imply that the cash rate was expected to be

lowered by another 25 basis points by November 2019, with a further cut expected in the early part

of 2020.

Growth in housing credit had been little changed over the year to July, having declined steadily

through 2018. Credit to investors had declined slightly over previous months. Meanwhile, housing loan

approvals to both owner-occupiers and investors had increased for the second consecutive month in July.

This pick-up in loan approvals had followed a significant decline over the preceding two years and was

consistent with the signs of stabilisation in the established housing market. Borrowing by large

businesses had continued to grow at a relatively strong pace. In contrast, small businesses’ access

to finance remained difficult, and had become more difficult over the preceding year as banks had

tightened their lending practices. While new sources of non-traditional finance had been growing,

including equity funding from family offices and private equity funds, they remained a small share of

business funding.

Members had a detailed discussion of the ways in which financial conditions abroad affect Australia.

They discussed how shifts in world interest rates and global risk premiums flow through to domestic

financial conditions. While Australia’s floating exchange rate means that monetary policy can be

set largely according to domestic considerations, members discussed the large shifts in

savings/investment decisions globally, which were affecting the level of interest rates everywhere,

including in Australia. Members also noted the critical role that the exchange rate had played over many

years as a shock absorber for the Australian economy. One important factor here has been that Australian

entities raising offshore funding are able to do so in Australian dollars, either directly or via

hedging markets.

Considerations for Monetary Policy

Turning to the policy decision, members observed that the news on the international economy had

confirmed that the risks to the global growth outlook were to the downside. The trade disputes between

the United States and China had escalated and growth in China had continued to slow. There had been

further indications that these developments were affecting trade and investment decisions in overseas

economies, although businesses had continued hiring and labour market conditions had remained

tight.

Against this backdrop and with ongoing low inflation, a number of central banks had reduced interest

rates over recent months and further monetary easing was widely expected. Long-term government bond

yields had declined and were at record lows in many countries, including Australia. Borrowing rates for

both businesses and households were also at historically low levels, and the Australian dollar exchange

rate was at the lowest level that it had been in recent times.

Domestically, members considered a number of developments over preceding months that had a bearing on

the monetary policy decision. First, employment had continued to grow strongly and the participation

rate was at a record high. However, the unemployment rate had remained steady at around

5.2 per cent over recent months. At the same time, wages growth had remained low and there

were few indications that wage pressures were building. Members noted that a further gradual lift in

wages growth would be a welcome development. Taken together, recent outcomes suggested that spare

capacity remained in the labour market and that the Australian economy could sustain lower rates of

unemployment and underemployment.

Second, there had been further signs of a turnaround in established housing markets, especially in

Sydney and Melbourne, although housing turnover had remained low. Housing credit growth had remained

subdued, although mortgage rates were at record low levels and there was strong competition for

borrowers of high credit quality. Data on residential building approvals and information from the

Bank’s liaison program suggested that there was likely to be further weakness in dwelling

investment in the near term; members recognised that this could sow the seeds of an upswing in the

housing price cycle at some point, particularly given the lengthy stages in the construction of

higher-density residential housing. Demand for credit by investors continued to be subdued and credit

conditions, especially for small and medium-sized businesses, remained tight.

Finally, based on partial indicators, GDP growth in the June quarter was expected to have been around

½ per cent. The largest contributions to growth were expected to have been from exports

and public demand. Private final demand, which includes consumption, business investment and dwelling

investment, was expected to have been weak.

Looking forward, the outlook for output growth was being supported by the low level of interest rates,

recent tax cuts, signs of stabilisation in some established housing markets and a brighter outlook for

the resources sector. A key uncertainty continued to be the outlook for consumption growth, which was

expected to increase over time, supported by a gradual pick-up in growth in household disposable income

and improvements in conditions in the housing market. Inflation pressures remained subdued, but

inflation was expected to increase gradually to be a little above 2 per cent over 2021 as

output growth picked up and the labour market tightened.

Based on the information available, members judged that it was reasonable to expect that an extended

period of low interest rates would be required in Australia to make sustained progress towards full

employment and achieve more assured progress towards the inflation target. Members would assess

developments in both the international and domestic economies, including labour market conditions, and

would ease monetary policy further if needed to support sustainable growth in the economy and the

achievement of the inflation target over time.

The Decision

The Board decided to leave the cash rate unchanged at 1.00 per cent.