The opaque, discretionary pricing of residential mortgages by banks makes it difficult and time consuming for borrowers to shop around and stifles price competition, a report by the ACCC has found.

The ACCC’s Residential Mortgage Price Inquiry monitored the prices

charged by the five banks affected by the government’s Major Bank Levy

between 9 May 2017 and 30 June 2018.

The ACCC’s final report

found the unnecessarily high search costs or effort required by

borrowers to find better prices reduces their willingness to shop

around, but that many borrowers who negotiate with their bank can get a

much better price.

“Pricing for mortgages is opaque and the big four banks have a lot of

discretion. The banks profit from this and it is against their

interests to make pricing transparent,” ACCC Chair Rod Sims said.

“Borrowers may not be aware they can negotiate with their lender on

price, both before and, particularly, after they have established their

mortgage.”

As at 30 June 2018, an existing borrower with an average-sized

mortgage could initially save up to $850 a year in interest if they

negotiated to pay the same interest rate as the average new borrower at

the five banks under review. For many borrowers the gain will be much

larger.

It appears that media attention on banks from the Banking Royal

Commission, the Productivity Commission’s Inquiry into competition in

the Australian financial system and the ACCC’s inquiry prompted some

borrowers to approach their lender for a better rate.

The ACCC reports that about 11 per cent of borrowers with variable

rate mortgages had the price of their current residential mortgage

reduced by one of the five banks under review in the year to 30 June

2018.

“I encourage more people to ask their lender whether they are getting

the lowest possible interest rates for their residential mortgage and,

as they do so, be ready to threaten to switch to another lender,” Mr

Sims said.

“I am afraid that the threat of switching banks will often be necessary to achieve a competitive mortgage rate.”

When directing the ACCC to conduct this inquiry, the Treasurer

requested the ACCC to report whether it found any evidence of the five

banks passing on the costs associated with the Major Bank Levy to

residential mortgage borrowers.

“The ACCC found no evidence that the five banks changed prices

specifically to recover the cost of the Major Bank Levy, whether in part

or in full, during the price monitoring period,” Mr Sims said.

The ACCC did find that measures announced by APRA in March 2017 to

limit new interest-only residential mortgage lending created an

opportunity for banks to synchronise increases to headline variable

interest rates for interest-only mortgages.

“We were not surprised banks seized the opportunity to increase

prices for interest-only loans. These price rises were enabled by the

oligopoly market structure in which the big four banks collectively have

a market share of about 80 per cent,” Mr Sims said.

ANZ was the first bank to announce increases to these interest-only

rates in June 2017. It did so safe in the knowledge that its move would

put the other banks at risk of breaching the APRA limits.

The other four banks, therefore, announced similar changes in the

same month. Together, the big four banks estimated revenue gains of over

$1.1 billion for their 2018 financial year, primarily as a result of

these rate increases.

“We consider that ANZ increased its rates, clear in its belief that,

given the APRA limits, the other big four banks would follow its lead,

and this expectation proved correct,” Mr Sims said.

The ACCC calculated that the rate increases by the five banks would

have added, in the first year, about $1300 in interest charged to the

average-sized owner-occupier interest-only standard variable mortgage.

“Such is the oligopolistic nature of banking that the banks all took

the opportunity to increase rates on both new and existing interest-only

mortgages, despite APRA’s measures only applying to new lending,” Mr

Sims said.

The ACCC also compared the approach to pricing of a sample of seven

banks that were not subject to the Inquiry. Three of these banks were

particularly focussed on competing on price, and therefore have lower

rates. Some of the banks in our sample rely heavily on brokers and

aggregators to gain market share. The ACCC notes that these banks, and

other lenders in a similar position, are likely to be more vulnerable to

future regulatory changes that affect the use of brokers as a

distribution channel.

In this report the ACCC notes that the new Consumer Data Right will,

among other things make it much easier for consumers to compare

available interest rates.

“The ACCC looks, in particular, to the Consumer Data Right to empower consumers in their dealings with banks,” Mr Sims said.

On 9 May 2017 the Treasurer, the Hon. Scott Morrison MP, issued a

direction to the ACCC to inquire into prices charged or proposed to be

charged by Authorised Deposit-taking Institutions affected by the Major

Bank Levy in relation to the provision of residential mortgage products

in the banking industry in Australia. The Major Bank Levy came into

effect from 1 July 2017.

The five banks affected by the levy are Australia and New Zealand

Banking Group Limited (ANZ), Commonwealth Bank of Australia, Macquarie

Bank Limited, National Australia Bank Limited, and Westpac Banking

Corporation.

The ACCC used its compulsory information gathering powers to obtain

documents and data from the five banks on their pricing of residential

mortgage products. The ACCC supplemented its analysis of the documents

and data supplied by the five banks with data from the Reserve Bank of

Australia (RBA), Australian Prudential Regulation Authority (APRA) and

the Australian Bureau of Statistics (ABS).

This Inquiry was the first task of the ACCC’s Financial Services Unit

(FSU), which was formed as a permanent unit during 2017 following a

commitment of continuing funding by the Australian Government in the

2017-18 Budget. Alongside the ACCC’s role in promoting competition in

financial services through its enforcement, infrastructure regulation,

open banking, and mergers and adjudication work, the FSU will monitor

and promote competition in Australia’s financial services sector by

assessing competition issues, undertaking market studies, and reporting

regularly on emerging issues and trends in the sector.

The FSU is currently examining the pricing of foreign currency

conversion services in Australia to evaluate whether there are

impediments to effective price competition in the sector. An inquiry

report is to be delivered to the Treasurer by 31 May 2019.

Nearly 170 years before the invention of Bitcoin, the journalist

Charles Mackay noted the way whole communities could “fix their minds

upon one object and go mad in its pursuit”. Millions of people, he

wrote, “become simultaneously impressed with one delusion, and run after

it, till their attention is caught by some new folly more captivating

than the first”.

His book Extraordinary Popular Delusions and the Madness of Crowds,

published in 1841, identifies a series of speculative bubbles – where

people bought and sold objects for increasingly steep prices until

suddenly they didn’t. The best-known example he cites is the tulip mania

that gripped the Netherlands in the early 17th century. Tulip bulbs

soared in value to sell for up to 25,000 florins each (close to A$45,000

in today’s money) before their price collapsed.

The Bitcoin bubble surpasses this and all

other cases identified by Mackay. It is perhaps the most extreme bubble

since the late 19th century. In four years its price surged almost

2,800%, reaching a peak of US$19,783 in December 2017. It has since

fallen by 80%. A month ago it was trading at more than US$6,000; it is

now down to US$3,500.

That’s still a fantastic gain for anyone who bought Bitcoin before

May 2017, when it was worth less than US$2,000, or before May 2016, when

it was worth less than $500.

But will it simply keep dropping? What makes Bitcoin worth anything?

To begin to answer this question, we need to understand what creates

the values that drive speculative price bubbles, and then what causes

prices to plunge.

The above chart shows the magnitude of the Bitcoin bubble compared

with the price movement of Japanese property and dot-com bubble from

four years prior to their peak until four years after.

When asset values diverge

We typically think about bubbles in financial assets such as stocks

or bonds, but they can also occur with physical assets (such as

property) or commodities (like tulip bulbs).

A bubble begins when the price people are willing to pay for something deviates significantly from its “intrinsic value”.

The intrinsic value of an asset is theoretical, based its

“fundamental” value. Fundamental value includes: the ability to generate

cash flow (e.g. interest or rental income); scarcity or rarity value

(e.g. gold or diamonds); and potential use (e.g. silver and platinum are

used in both jewellery and industrial operations).

A house may have fundamental value owing to the scarcity of land, its

use as a home, or its ability to generate rental income. A tulip (or

Bitcoin) has none of those things; even the presumed scarcity does not

exist when you consider all of the alternative flowers (or

cryptocurrencies) available.

A bubble tends to occur after a sustained period of economic growth,

when investors’ get used to the price an asset always increasing and

credit is easily accessible.

To these conditions something more must be added for a bubble to

form. That is typically a major disruption or innovation, such as the

development of a new technology. Think of railways in the 19th century,

electricity in the early 20th century, and the internet at the end of

the 20th century.

Initially most investors tend to be cautious and “rational” about a

new technology. For instance, early investment in railways took

advantage of limited competition and focusing on profitable routes only.

It was gradual and commercially successful.

This creates higher growth and profitability, leading to positive

feedbacks (from greater investment, higher dividend payouts, and

increased consumer spending), which raises confidence further.

If conditions allow, this develops into a period the economic historian Charles Kindleberger described as “euphoric”: investors become fixated on the ability to make a profit by selling the asset to a “greater fool” at an even higher price.

South Cryptocurrency values are

displayed in the Seoul shopfront of Bithumb, South Korea’s leading

cryptocurrency exchange, in January 2018.

Jeon Heon-Kyun/EPA

That is, they are attracted not by “fundamental” motives – the

benefits from potential cash-flows such as dividend or rental income –

but by “speculative” motives – the pursuit of short-term capital gains.

Higher prices attract a greater number of speculators, pushing prices

higher still. Uncertainty around the significance of the new technology

allows extreme valuations to be rationalised, although the

justifications seem weaker as prices rise further.

The virtuous cycle of ever-rising prices continues, often fuelled by

credit, until there is an event that leads to a pause in price rises.

Kindleberger suggests this can be a change in government policy or an

unexplained failure of a firm.

When asset prices stop rising, investors who have borrowed to finance

their purchases realise the cost of interest payments on their debt

will not be offset by the capital gain to be made by holding onto the

asset. So they cut their losses and start to sell the asset. Once the

price starts falling, more investors decide to sell.

Bitcoin’s bubble

The possible triggers for a pause in Bitcoin price rises included

concerns about increased government regulation of crypto-assets and the

possibile introduction of central bank digital currencies, as well as

the large theft of assets and collapse of exchanges that have dogged Bitcoin’s short history.

Going down

In liquid markets such as stocks (where it is inexpensive to buy and

sell assets in large values) the price decline can be steep. In illiquid

markets, where assets cannot easily be sold for cash, the fall can be

brutal. Examples include the mortgage-backed securities (MBS) and

collateralised debt obligations (CDOs) that led to the Global Financial

Crisis.

Bitcoin is particularly illiquid. This is due to a large number of different Bitcoin exchanges competing; often substantial transaction costs, and constraints on the capacity of the Blockchain to record transactions.

A Bitcoin ‘mine’ in China. Miners

are rewarded with new currency for solving the complex math problems

required to validate and record Bitcoin transactions. It requires a

massive amount of computer-processing power.

Liu Xingzhe/Chinafile/EPA

The aftermath

The aftermath of a bursting bubble can be brutal. The stock market

crash of 1929 was a prelude to the Great Depression of the 1930s. The

collapse in Japanese asset values after 1989 heralded a decade of low

growth and deflation. The dot-com crash of 2000-01 destroyed US$8

trillion of wealth.

The effect of a crash depends the size, ownership and importance of

the asset involved. The effect of the tulip crash was limited because

tulip speculations involved a relatively small number of people. But

sharp declines in property values during 2007 led to the worst financial

crisis since the Great Depression.

Bitcoin is more like tulips. The entire market valuation was about

US$300 billion at the peak. To put this into context, the US stock and

housing markets are currently valued more than US$30 trillion each (the

equivalent Australian markets are valued at A$2 trillion and A$6.9

trillion respectively). Relatively few investors own the majority – it

is estimated that 97% of all Bitcoin are owned by just 4% of users. This suggests the effects on the wider economy of the Bitcoin crash should be contained.

Estimating Bitcoin’s intrinsic value

Obtaining a realistic estimate of Bitcoin’s intrinsic value is tricky

because it is not an asset that generates a periodic cash flow, such as

interest or rental income.

This does not provide a positive story for Bitcoin. Though the total

number of Bitcoins is limited, there are many competing, virtually

indistinguishable cryptocurrencies (such as Ehtereum and Ripple).

Bitcoin also fails to meet the criteria of a currency.

Its the price movements are too volatile to be a unit of account. The

transaction capacity of the Blockchain is too limited for it to be a

medium of exchange. Nor does it appear to be a good store of value.

For such an asset, value ultimately depends on what others are willing to pay for it. This often relates to scarcity.

Since it produces no income, has limited scarcity value, and few

people are willing to use Bitcoin as currency, it is even possible that

Bitcoin has no intrinsic value.

Author: Lee Smale, Associate Professor, Finance, University of Western Australia

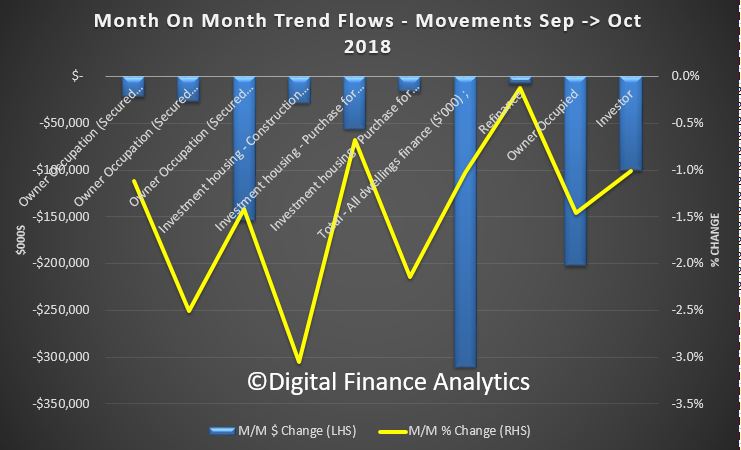

The ABS released their Housing Lending data to end of October 2018. The media will fixate on the 2.6% rise in seasonally adjusted terms and some will claim this marks the “turn around” in mortgage lending. However, it is worth saying the seasonally adjusted series moved around significantly, and it does not take account of the much longer processing and settlement time we are now seeing as banks continue to tighten their underwriting criteria. Average loan settlement times have blown out considerably.

So, we will continue to look at the trend series, which seeks to iron out the humps and bumps, and tends to be more reliable in terms of overall trajectory.

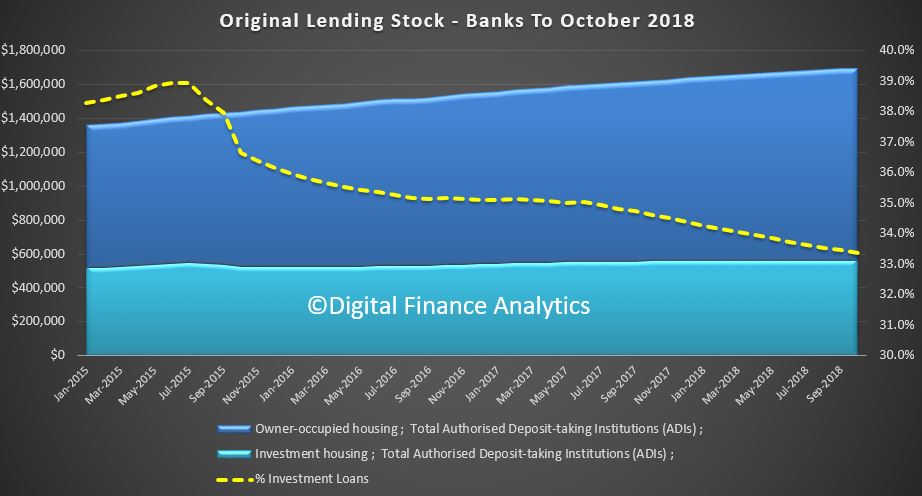

But before we go there, lets look at the original data series. So first to the stock of home loans held by the banks. Owner occupied loans held rose 0.4% in the month, or $4.8 billion to stand at $1.129 trillion. Investment loans were flat in the month, standing at $565.5 billion. So total home lending grew 0.3% to $1.695 trillion. Investor loans comprised 33.4% of all loans outstanding, compared with 39% in May 2015.

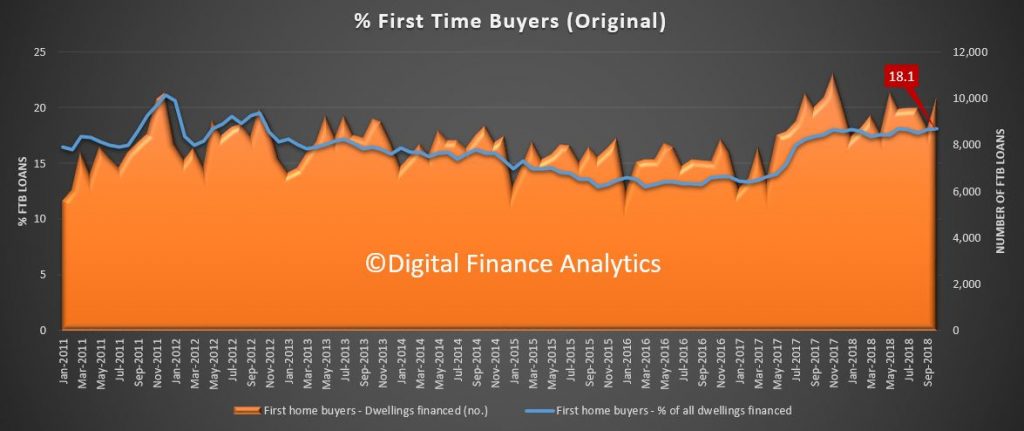

The original first time buyer data showed there was a rise of 15.7% compared with the previous month, to 10,137 loans approved, which offset the significant fall last month, and was caused by the longer loan processing times, and the incentives which still remain in the system to try and encourage first time buyers into the market. That meant that 18.1% of all loans were for First Time Buyers, still well below the 21% we saw in December 2011, or the 30.6% seen in 2009!

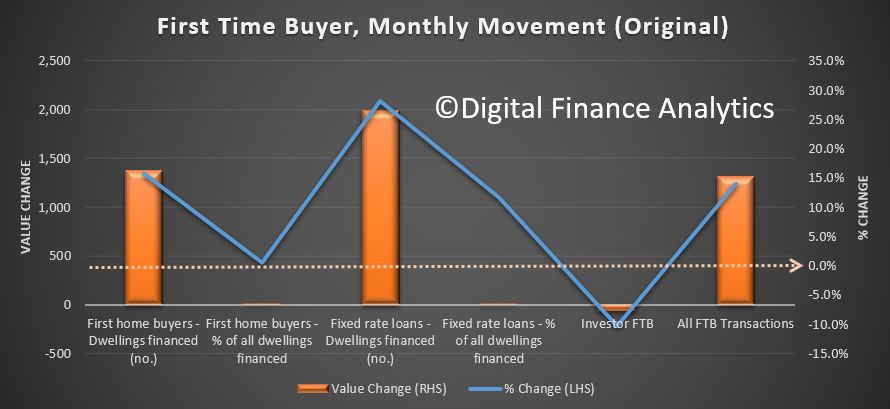

More loans were fixed rate this month, a reflection of the cheap refinance details on offer.

And the DFA tracker, which included first time buyers going direct to the investment market continues to fall.

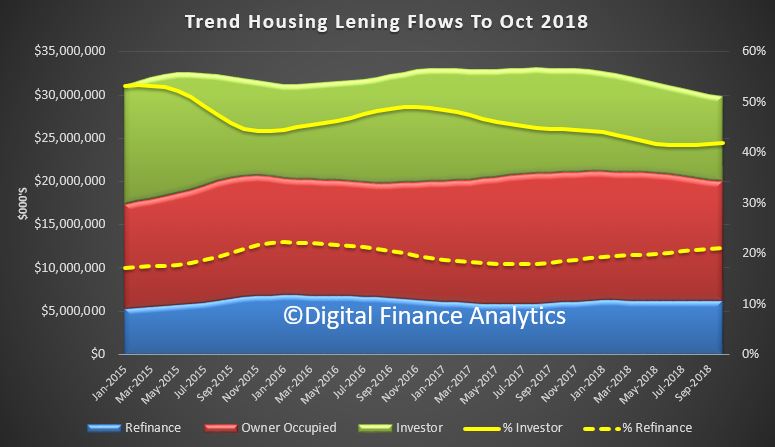

So now to the trend flow series. Total flows were down 1% to 29.85 billion, and within that refinances fell 0.1% to $6.3 billion, owner occupied loans fell 1.5% to $13.69 billion and investment loans fell 1% to 9.84 billion. Investor flows comprised 41.82% of new flows (excluding refinances) and refinances made up 21.1% of flows, the highest since June 2016.

Looking at the moving parts, lending flows for owner occupied secured construction fell 1.1% to $1.8 billion, purchase of new dwellings was down 2.5% to $1.04 billion, and purchase for owner occupation of established buildings fell 1.4% to $10.77 billion. Refinance flows fell just 0.1% to $6.31 billion while investment related construction fell 3.1% to $0.9 billion, purchase for individual investors fell 0.7% to $8.19 trillion and investment purchases by other entities (for example super funds) was down 0.21% to $0.74 billion.

So to conclude, there is nothing here to indicate a recovery in home lending, and in some categories the volumes continue to shrink. In fact we will really not get a good read until the February data is in, as the next couple of months are always wobbly thanks to the summer holidays. And what we do know is that auction clearance rates are languishing, and more property remains on sale for longer. So we think loan volumes will continue to weaken.

In a statement this morning, Bank of Queensland said the BOQ and Freedom had mutually agreed to terminate the St Andrews Insurance sale and purchase agreement.

“Following the termination of the agreement with Freedom, BOQ will continue to assess its strategic options in relation to St Andrew’s. In the meantime, St Andrew’s continues to be a strongly capitalised business that remains focused on delivering for its customers and corporate partners,” BOQ said.

The troubled Freedom Insurance Group last week completed its

strategic review, which was prompted by ASIC’s recommendations about the

life insurance industry.

As part of the review, which was conducted in collaboration with

Deloitte, the Freedom board identified that the company may face a

liquidity shortfall during calendar year 2019 arising from the timing of

payments of commission clawbacks in the absence of receipts of

commissions from new business sales.

Freedom had been pursuing equity funding for the purposes of the St Andrews acquisition, the process of which has included the provision of confidential due diligence to prospective third-party investors and negotiation of related transaction documentation.

it became clear that the conditions of the transaction would not be satisfied within the time limits contained in the sale agreement they said..

“In this regard, the company is considering alternate options to address the potential shortfall,” the group said in a trading update”.

“In addition, Freedom is implementing initiatives to improve operational efficiency and reduce costs.”

Freedom expects to make a provision for net remediation costs in its

financial accounts for the period ending 31 December 2018 of between

approximately $3 million and $4 million.

He concludes that “Global developments undoubtedly influence Australian financial conditions. In particular, developments abroad can influence the value of the Australian dollar and affect global risk premia. But changes in monetary policy settings elsewhere need not, and do not, mechanically feed through to the funding costs of Australian banks, and hence their borrowers are insulated from such changes”.

But the higher bank funding rate spreads which see here are perhaps more of a reflection of the risks the markets are pricing in, than anything else. Yet this was not discussed. Too low rates here for several years are the root cause (and guess where the buck for that stops?). This led to overheated lending, and home prices, which are now reversing, with obvious pressures on the banks. This leaves the economy open to higher rates, from overseas ahead.

This is the speech:

Australia is a small open economy that is influenced by developments in the rest of the world.

Financial conditions here can be affected by changes in monetary policy settings elsewhere, most

particularly in the United States given its importance for global capital markets. However,

Australia retains a substantial degree of monetary policy autonomy by virtue of its floating

exchange rate. In other words, a change in policy rates elsewhere need not mechanically feed

through to Australian interest rates. While Australian banks raise significant amounts of

funding in offshore markets, they are able to insulate themselves – and by extension

Australian borrowers – from changes in interest rates in other jurisdictions.

Just before delving into the details, some context is in order. First, Australian banks have long

borrowed in wholesale markets, including those offshore. However, they do so much less than used

to be the case (Graph 1).[1]

For a number of reasons, domestically sourced deposits have become an increasingly large share of

overall funding for banks.[2]

Graph 1

Second, to the extent that Australian banks have continued to tap offshore wholesale markets, it

is worth reflecting on some of the characteristics of this borrowing. For instance, some

banking sectors around the world borrow in US dollars in order to fund their portfolios of US

dollar assets.[3] This

can leave them vulnerable to intermittent spikes in US interest rates. However, this is

generally not the case for Australian banks. Rather, a good deal of the borrowing by Australian

banks in US dollars reflects the choice of the banks to diversify their funding base in what are

deep, liquid capital markets. By implication, if the costs in the offshore US dollar funding

market increased noticeably relative to the home market, then Australian banks can pursue other

options. They might opt to issue a little less in the US market for a time, switching to other

markets or even issuing less offshore. They are not ‘forced’ to acquire US dollars

at any price, as some other banks may be. Another important feature of this offshore funding, as

I will address in detail in a moment, is that the banks are not exposed to exchange rate risks

as they hedge their borrowings denominated in foreign currencies.

Independence – It’s an Australian Dollar Thing

As you are well aware, the US Federal Reserve has been raising its policy rate in recent years,

and interest rates in the United States are now higher than in Australia. These developments

reflect differences in spare capacity and inflation: unemployment in the United States is at

very low levels, inflation is at the Fed’s target and inflationary pressures appear to be

building. Since August 2016 – the last time the Reserve Bank changed its cash rate

target – the Federal Reserve has raised its policy rate seven times, by 175 basis points

in total (Graph 2). Yet while Australian banks raise around 15 per cent of their

funding in US dollars, interest rates paid by Australian borrowers since then have been little

changed.

Graph 2

How is it that interest rates for Australian borrowers have been so stable, despite Australian

banks having borrowed some US$500 billion in the US capital markets, in US dollars, paying US

dollar interest rates? The answer lies in the hedging practices of the Australian financial

sector. As I’ll demonstrate, Australian banks use hedging markets to convert their US

interest rate obligations into Australian ones.

The Australian banks fund their Australian dollar assets via a number of different sources. Some

of their funds are obtained in US dollars from US wholesale markets. In order to extend these

USD funds to Australian residents, they convert the US dollars they have borrowed into

Australian dollars soon after the securities are issued in the US. On the surface it would

appear that such transactions could give rise to substantial foreign exchange and interest rate

risks for Australian banks given that:

the banks must repay the principal amount of the security at maturity in US dollars. So an

appreciation of the US dollar increases the cost of repaying the loan in Australian dollar

terms; and

the banks must meet their periodic coupon (interest) payments in US dollars, which are tied to

US interest rates (either immediately if the security has a floating interest rate, or when

the security matures and is re-financed). So a rise in US interest rates (or an appreciation

of the US dollar) would increase interest costs for Australian banks that extend loans to

Australian borrowers.

However, it is standard practice for Australian banks to eliminate, or at least substantially

reduce, these risks. They can do this using a derivative instrument known as a cross-currency

basis swap. Such instruments are – when used appropriately – a relatively

cost effective way of transferring risks to parties with the appetite and capacity to bear them.

Simply put, cross-currency basis swaps allow parties to ‘swap’ interest rate streams

in one currency for another. They consist of three components (Figure 1):

first, the Australian bank raises US dollars in the US wholesale markets. Next, the

Australian bank and its swap counterparty exchange principal amounts at current spot

exchange rates; that is, the Australian bank ‘swaps’ the US dollars it has just

borrowed and receives Australian dollars in return. It can then extend Australian dollar

loans to Australian borrowers;

over the life of the swap, the Australian bank and its swap counterparty exchange a stream

of interest payments in one currency for a stream of interest receipts in the other. In this

case, the Australian bank pays an Australian dollar interest rate to the swap counterparty

and receives a US dollar interest rate in return. The Australian bank can use the interest

payments from Australian borrowers to meet the interest payments to the swap counterparty,

and it can pass the interest received from the swap counterparty onto its bondholders;

At maturity of the swap, the Australian bank and its swap counterparty re-exchange principal

amounts at the original exchange rate. The Australian bank can then repay its bond

holders.[4]

In effect, the Australian bank has converted its US dollar, US interest rate obligations into

Australian dollar, Australian interest rate obligations.

Figure 1

An analogy related to housing can help to further the intuition here. Imagine a

Bloomberg employee who owns an apartment in New York but has accepted a temporary job in Sydney.

She fully expects to return to New York and wishes to keep her property, and she does not wish

to purchase a property in Sydney. The obvious solution here is for her to receive rent on her

New York property and use it to pay her US dollar mortgage. Meanwhile, she can rent an apartment

in Sydney using her Australian dollar income. In other words, our relocating worker can

temporarily swap one asset for another. As a result, she can reduce the risks associated with

servicing a US mortgage with an Australian dollar income.

As I mentioned earlier, it is common practice for Australian banks to hedge their foreign

currency borrowings with derivatives to insulate themselves and their Australian borrowers from

fluctuations in foreign exchange rates and interest rates. The most recent survey of hedging

practices showed that around 85 per cent of banks’ foreign currency liabilities

were hedged (Graph 3). Also, the maturities of the derivatives used were well matched to

the maturities of the underlying debt securities.[5]

This means that banks were not exposed to foreign currency or foreign interest rate risk for the

life of their underlying exposures. By matching maturities, banks also avoided the risk that they

might not be able to obtain replacement derivatives at some point in the future (so called

roll-over risk).

Graph 3

For the very small share of liabilities that are not hedged with derivatives, there is almost

always an offsetting high quality liquid asset denominated in the same foreign currency of a

similar maturity, such as US Treasury Securities or deposits at the US Federal Reserve. Taken

together, these derivative hedges and natural hedges mean than Australian banks have only a very

small net foreign currency and foreign interest rate exposure overall (Graph 4).

Graph 4

So who is bearing the risk?

Despite Australia’s external net debt position,

in net terms Australian residents have passed on – for a cost, as we shall see – key

risks associated with their foreign currency liabilities to foreign residents. Australian

residents have found enough non-residents willing to lend them Australian dollars and to receive

an Australian interest rate to extinguish their foreign currency liabilities. As a result,

Australians are net owners of foreign currency assets, not borrowers.[6] Collectively,

Australians have used hedging markets and natural hedges to (more than) eliminate their

exchange-rate exposures associated with raising funds in offshore markets.

Australians’ ability to find non-residents willing to assume Australian dollar and Australian

interest rate risks is a reflection of the willingness of non-residents to invest in Australian

dollar assets. This in turn reflects Australia’s status as a country that has long had strong

and credible institutions, a high credit rating and mature and liquid capital markets. The

willingness of these non-resident counterparties to assume these risks via a direct exposure to

Australia’s banking system – sometimes for as long as thirty years – reflects the fact that

Australia’s banks are well-capitalised and maintain high credit ratings. In short, Australians

have found a source of finance unavailable domestically (at as reasonable a price), and

non-residents have found an asset that suits their portfolio needs.

Since there are no free lunches in financial markets, there is the question of the cost for

Australian banks to cover these arrangements. One part of this cost is known as the basis.

An imperfect world

Some swap counterparties have an inherent reason to enter into

swap transactions with Australian banks. In other words, such exposures actually help them to

manage their own risks. Non-residents that issue Australian dollar debt – in the so called

Kangaroo bond market – are a case in point. These issuers raise Australian dollars to fund

foreign currency assets they hold outside of Australia. This makes them natural counterparts to

Australian banks wanting to hedge their foreign currency exposures. Similarly, Australian

residents invest in offshore assets. To the extent that they want to hedge the associated

exchange rate exposures, they too would be natural counterparties for the Australian banks.

However, it turns out that these natural counterparties do not have sufficient hedging needs to

meet all of the Australian dollar demands of the Australian banks. So in order to induce a

sufficient supply of Australian dollars into the foreign exchange swap market, Australian banks

pay an additional premium to their swap counterparts on top of the Australian dollar interest

rate. This premium, or hedging cost, is known as the basis. Simply put, the basis is the price

that induces sufficient supply to clear the foreign exchange swap market.[7]

Since the start of the decade, the basis has oscillated around 20 basis points per annum (Graph 5).

Typically, though not always, the longer a bank wishes to borrow Australian dollars, the higher

the premium it must pay over the Australian dollar interest rate.

Graph 5

You may be wondering why Australian banks are willing to pay this premium; why don’t they

instead only borrow Australian dollars in the Australian capital markets to meet their financing

needs? In addition to the prudent desire to have a diversified funding base as I mentioned

earlier, the short answer is that it may not be cost-effective to raise all their funding at

home. What tends to happen is that banks – to the extent possible – seek to equalise

the marginal cost of each unit of funding from different sources. If they were to obtain all of

their funding at home, that would be likely to increase the cost of those funds relative to

funds sourced from offshore. So the all-in-cost of the marginal Australian dollar from domestic

sources will tend to be about the same as the marginal dollar obtained from offshore.

Astute students of finance will also wonder why the basis is not arbitraged away.[8]

The answer is that structural changes in financial markets have widened the scope for market

prices to deviate from values that might prevail in a world of no ‘frictions’. This

is consistent with the concept of ‘limits to arbitrage’ (which the academic

community only started to re-engage with in the past couple of decades). Arbitrage typically

requires the arbitrageur to enlarge their balance sheet and incur credit, mark-to-market and/or

liquidity risk. As Claudio Borio of the BIS has noted: balance sheet space is rented, not free.

And the cost of that rent has gone up.[9]

What about financial conditions more generally?

None of this is to suggest that

monetary policy settings in the United States (and elsewhere for that matter) have no impact on

financial conditions here in Australia. But the link is neither direct nor mechanical.

The primary channel through which foreign interest rates influence Australian conditions is

through the exchange rate. An increase is policy rates elsewhere will, all else equal, tend to

put downward pressure on the Australian dollar, because capital is likely to be attracted to the

higher rates of return available abroad. A depreciation of the Australian dollar in turn will

tend to enhance the competitiveness of our exporters, including those services priced in

Australian dollars like tourism and education. Through various channels, exchange rate

depreciation can also loosen financial conditions in Australia, which is not always the case in

other countries, particularly those for which inflation expectations are not well anchored and

where there are substantial foreign currency borrowings that are unhedged.[10]

Foreign monetary policy settings, particularly those in the United States, can also affect global

risk premia. We are now approaching a period when US monetary policy is moving to a neutral

stance. This follows a lengthy period of very easy monetary conditions, which may have

encouraged investors to ‘search for yield’ to maintain nominal portfolio returns in

an environment of low interest rates. The expectation of low and stable policy rates and

inflation outcomes in turn compressed risk premia across a range of asset classes. In the period

ahead, it seems plausible that term and credit risk premia will rise, which will increase costs

for all borrowers, Australian banks included.

The board of IOOF Holdings has today announced that IOOF managing director, Christopher Kelaher and chairman, George Venardos, have agreed to step aside from their respective positions effective immediately, pending resolution of proceedings brought by the Australian Prudential Regulation Authority (APRA) and announced last Friday, 7 December.

Mr Renato Mota, currently group general manager – wealth management,

has been appointed acting chief executive officer and Mr Allan

Griffiths, a current non-executive director of IFL, is acting chairman.

Both Mr Kelaher and Mr Venardos will be on leave while they focus on

defending the actions brought against them by APRA.

Chief financial officer David Coulter, company secretary Paul Vine

and general counsel Gary Riordan will remain in their positions, however

will have no responsibilities in relation to the management of the IOOF

trustee companies and will have no engagement at all with APRA during

this period, including in relation to the matters the subject of APRA’s

announcement of Friday 7 December.

“We maintain our position that the allegations made by APRA are

misconceived, and will be vigorously defended. The Board believes that,

in the interests of good governance, it is appropriate that Chris and

George step aside from their positions. The Board will also commence a

search for an additional non-executive Director,” Acting chairman, Allan

Griffiths said

“We acknowledge the seriousness of these allegations. We have a

responsibility to our superannuation members, shareholders, advisers,

employees and the wider community, to take decisive action.

“We are entirely focused on addressing the governance issues in the

interests of all stakeholders and will do so in an orderly manner.

“I will personally lead our review of the situation and, alongside

acting CEO Renato Mota, will work cooperatively with APRA to continue to

implement previously agreed initiatives. Many of these actions are

already complete.”

IOOF posted an underlying net profit after tax result in financial

year 2018 of $191.4 million, up 13 per cent on the financial year 2017

result.

“These results have been delivered by our unwavering commitment to

our clients, driven by our talented people and a recognition of the

importance of advice. We remain committed to the ANZ transaction and we

are working cooperatively with ANZ as they consider their position,” Mr

Griffiths said.

The prudential regulator is seeking to impose additional licence

conditions and issue directions to APRA-regulated entities in the IOOF

group.

The proceedings in the Federal Court seek to disqualify five

individuals that were responsible persons at IOOF Investment Management

Limited (IIML) and Questor Financial Services.

The proceedings are also seeking a court declaration that IIML and Questor breached the SIS Act.

The announcement drove ANZ to rethink the sale of its wealth business

to IOOF. ANZ released an update on its sale following APRA’s move to

disqualify IOOF individuals and its move to apply licence restrictions

on the group.

ANZs deputy chief executive Alexis George said ANZ would reassess the

sale of its OnePath Pensions and Investments business to IOOF.

“Given the significance of APRA’s action, we will assess the various

options available to us while we seek urgent information from both IOOF

and APRA.

“The work to separate Pensions and Investments from our Life

Insurance business continues. There is a framework available to complete

the Zurich transaction that does not involve IOOF,” he said.

Interesting perspective from property bulls in the West, arguing that population growth will drive property returns higher ahead and prices are down ~15% on average from the peak several years ago. Our data suggests net returns are significantly lower! This via Australian Broker:

Positive population growth and a decline in vacancy rates, as well as

the low interest rates, are making an attractive time to invest in

property in Western Australia.

After a 60,000 drop in 2015, West Australian annual population growth is rising again, with repeated climbs in recent years.

CBRE figures show Western Australia enjoyed a 21,000-person net increase alone in the past twelve months.

Population of the Perth and Peel region in 2010 was approximately

1.65 million. That is expected to exceed 2.2 million residents by 2031.

The change has prompted Gemmill Homes Managing Director, Craig Gemmill, to predict good times for the market.

He said, “This is the first step in the recovery of Western Australia.

“It’s really exciting, as there’s two real positives that come out of the population growth.

“Existing housing stock get soaked up. That affects supply and people

then go to the next level of pricing or they build. It will really

stimulate the market.”

Vacancy rates have seen a considerable drop after topping out at 7.3% in July last year.

Stabilisation has been followed by four consecutive quarterly falls

and Real Estate Institute WA figures show the vacancy rate has dipped to

3.9%, a level last seen in 2015.

Gemmill added, “It has happened so quickly. Yesterday we were all

saying it was all doom and gloom, but vacancy rates have dropped

considerably in just a year.

“When people were leaving the state it became a tenant’s market, due to the number of properties that were available.

“Now, we’re seeing things going back more in favour of the landlord, so it is a great time for investors.

“Investors need at least 5% return. The average now is around 5.5%.

When you claim 2% depreciation, that leaves a seven percent return.

That’s before investors have even claimed back their borrowing costs.

“So, in this market where interest rates are low, you can get a great return of investment.

“We’re going into an upswing in the cycle and it’s a great time to invest in the market.”

Michael Valetta, CBRE director of residential valuations agreed with

the positivity, saying recent data shows clear growth for WA.

He said, “An increase in population growth and decrease in vacancy rates present real opportunities for the real estate market.

“I see great potential in Western Australia and after some lean

years, signs point towards the fact we are turning things around.”

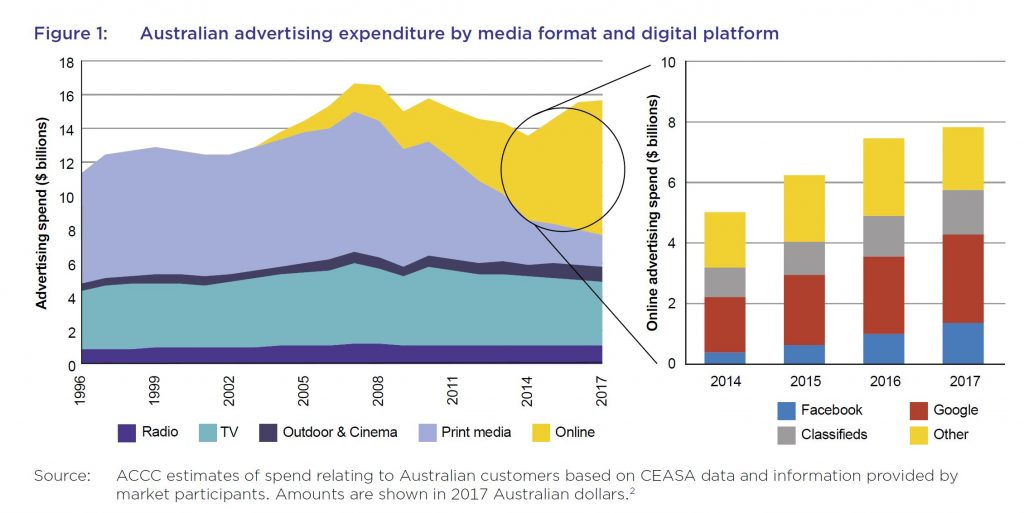

The issues raised are significant and far reaching, and questions the substantial market power players such as Google and Facebook have, the data they capture and monitise and their impact on the media. 94 per cent of online searches in Australia currently performed through Google.

Facebook and Instagram together obtain approximately 46 per cent of Australian display advertising revenue. No other website or application has a market share of more than five per cent.

They say there is a lack of transparency in the operation of Google and Facebook’s key algorithms, and the other factors influencing the display of results on Google’s search engine results page, and the surfacing of content on Facebook’s News feed.

Anti-competitive discrimination by digital platforms in favour of a related business has been found to exist in overseas cases. For example, in the European Commission’s 2017 decision, Google was found to have systematically given prominent placement to its own comparison shopping service (Google Shopping) and to have demoted rival comparison shopping services in its search results.

Monopoly or near monopoly businesses are often subject to specific regulation due to the risks of competitive harm. The risk of competitive harm increases when the monopoly business is vertically integrated. The ACCC considers that Google and Facebook each have substantial market power and each have activities across the digital advertising supply chain. Google in particular occupies a near monopoly position in online search and online search advertising, and has multiple related businesses offering advertising services.

This is their executive summary:

On 4 December 2017, the then Treasurer, the Hon Scott Morrison MP, directed the Australian Competition and Consumer Commission (the ACCC) to hold an inquiry into the impact of online search engines, social media and digital content aggregators (digital platforms) on competition in the media and advertising services markets. The ACCC was directed to look at the implications of these impacts for media content creators, advertisers and consumers and, in particular, to consider the impact on news and journalistic content.

Digital platforms offer innovative and popular services to consumers that have, in many cases, revolutionised the way consumers communicate with each other, access news and information and interact with business. Many of the services offered by digital platforms provide significant benefits to both consumers and business; as demonstrated by their widespread and frequent use by many Australians and many Australian businesses.

The ACCC considers, however, that we are at a critical point in considering the impact of digital platforms on society. While the ACCC recognises their significant benefits to consumers and businesses, there are important questions to be asked about the role the global digital platforms play in the supply of news and journalism in Australia, what responsibility they should hold as gateways to information and business, and the extent to which they should be accountable for their influence. In particular, this report identifies concerns with the ability and incentive of key digital platforms to favour their own business interests, through their market power and presence across multiple markets, the digital platforms’ impact on the ability of content creators to monetise their content, and the lack of transparency in digital platforms’ operations for advertisers, media businesses and consumers.

Consumers’ awareness and understanding of the extensive amount of information about them collected by digital platforms, and their concerns regarding the privacy of their data, are also critical issues. There are also issues with the role of digital platforms in determining what news and information is accessed by Australians, how this information is provided, and its range and reliability.

Digital platforms are having a profound impact on Australian news media and advertising. The impact of digital platforms on the supply of news and journalism is particularly significant. News and journalism generate broad benefits for society through the production and dissemination of knowledge, the exposure of corruption, and holding governments and other decision makers to account.

It is important that governments and the public are aware of, and understand, the implications of the operation of these digital platforms, their business models and their market power.

The ACCC’s research and analysis to date has provided a valuable understanding of the markets that are the subject of this Inquiry, including information that has not previously been available, and has identified a number of issues that could, or should, be addressed. Many of these issues are complex.

The ACCC has decided that the best way to address these issues in the final report, due 3 June 2019, is to identify preliminary recommendations and areas for further analysis, and to engage with stakeholders on these potential proposals. Such engagement may result in considerable change from the ACCC’s current views, as expressed in this report.

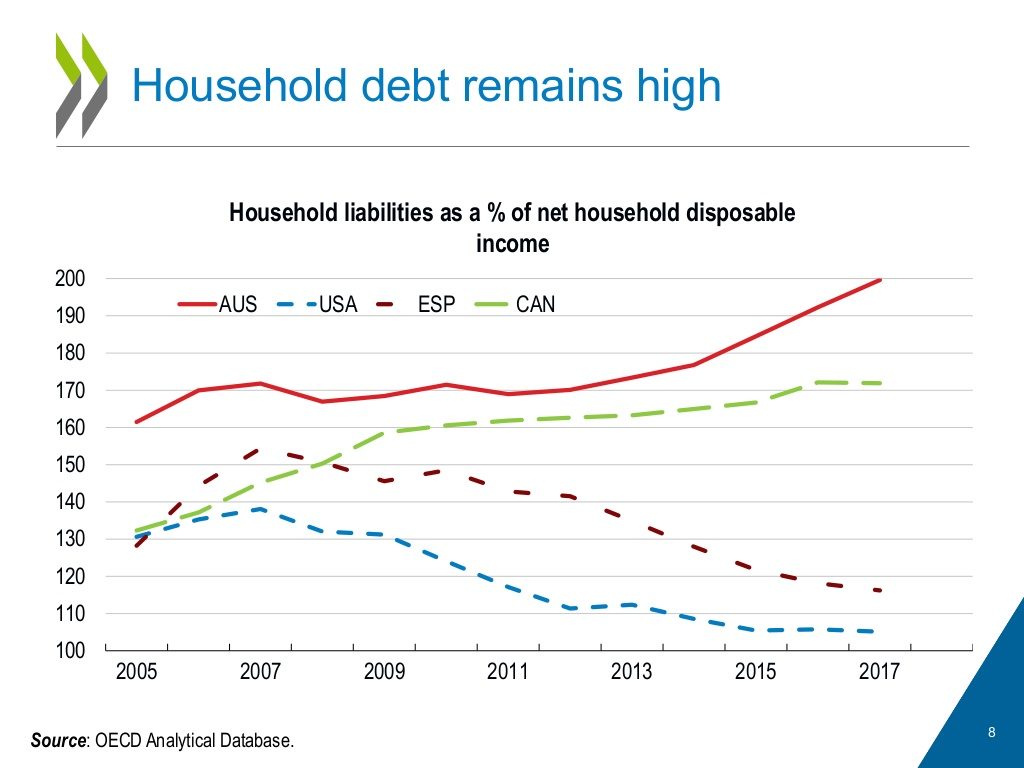

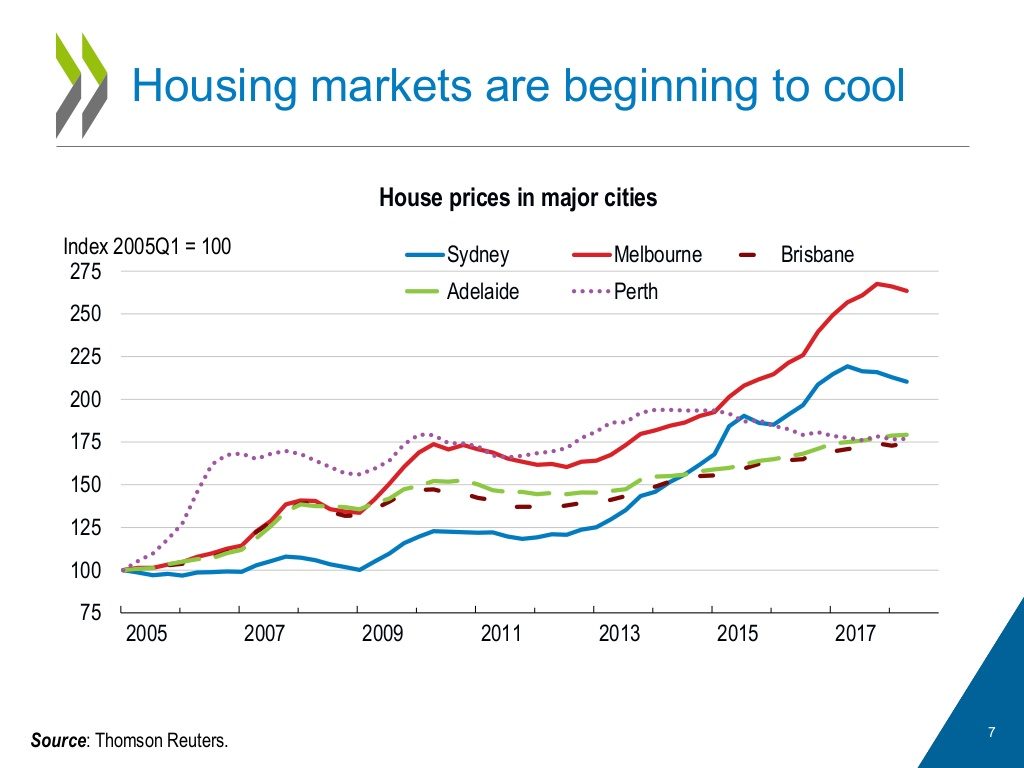

The OECD says Australia’s housing market is a source of vulnerability. Prices have more than doubled in real terms since the early 2000s and household debt has surged. The market has started to cool over the last year, with prices falling most notably in Melbourne and Sydney. So far, data point to a soft landing without substantial consequence for the overall economy. Nevertheless, risk of a hard landing remains.

To date the decrease in house prices has been gradual. Prudential

measures taken by the Australian authorities restricting certain types

of housing credit have played a role. So too has a pick-up in new

housing supply and construction activity remains elevated. Furthermore,

some evidence suggests that Australia’s house prices have not been

hugely overvalued; the IMF has estimated that as of Q3 2017 prices were

above equilibrium by only between 5 and 15% (Heilbling andLi, 2018).

Several features of Australian financing limit the risk of financial

fall-out from a house-price correction. Banks are well capitalised and

their liquidity position is sound. Indebtedness is concentrated in

middle- and high-income households, and data indicate declining

financial stress in recent years, despite rising mortgage debt.

Moreover,many mortgage holders have accumulated substantial buffers of

advance payments(“mortgage prepayments”).

Nevertheless, risk of a macroeconomic downturn from the cooling

housing market remains. Not withstanding the estimates that Australia’s

market is not greatly overvalued, house prices could fall more

substantially. Should this happen, household consumption could weaken.

Households would cut their spending due to lower housing wealth and due

to increased economic uncertainty generated by downturn. Households

would also reduce expenditures related to the purchase, sale and

maintenance of housing (such as spending on renovation and interior

decoration). Sustained decreases in house prices would also weaken

construction activity. Weakened aggregate demand could in turn lead to

losses on loans to businesses, putting stress on the financial sector.

The OECD’s 2018 Economic Survey of Australia

recommends authorities prepare contingency plans for a severe collapse

in the housing market. These should include the possibility of a crisis

situation in one or more financial institutions.

I discuss the latest developments in the New Zealand property market with Joe Wilkes. We look at the latest from the Reserve Bank, Deposit Bail-In and Bank Scorecards. Also highly relevant to other markets.

Please share this post to help to spread the word about the state of things….

Caveat Emptor! Note: this is NOT financial or property advice!!

{kind=link}