Digital Finance Analytics has released the latest edition of our flagship channel preferences report – “The Quiet Revolution” Volume 3, now available free on request, using the form below.

This report contains the latest results from our household surveys with a focus on their use of banking channels, preferred devices and social media trends.

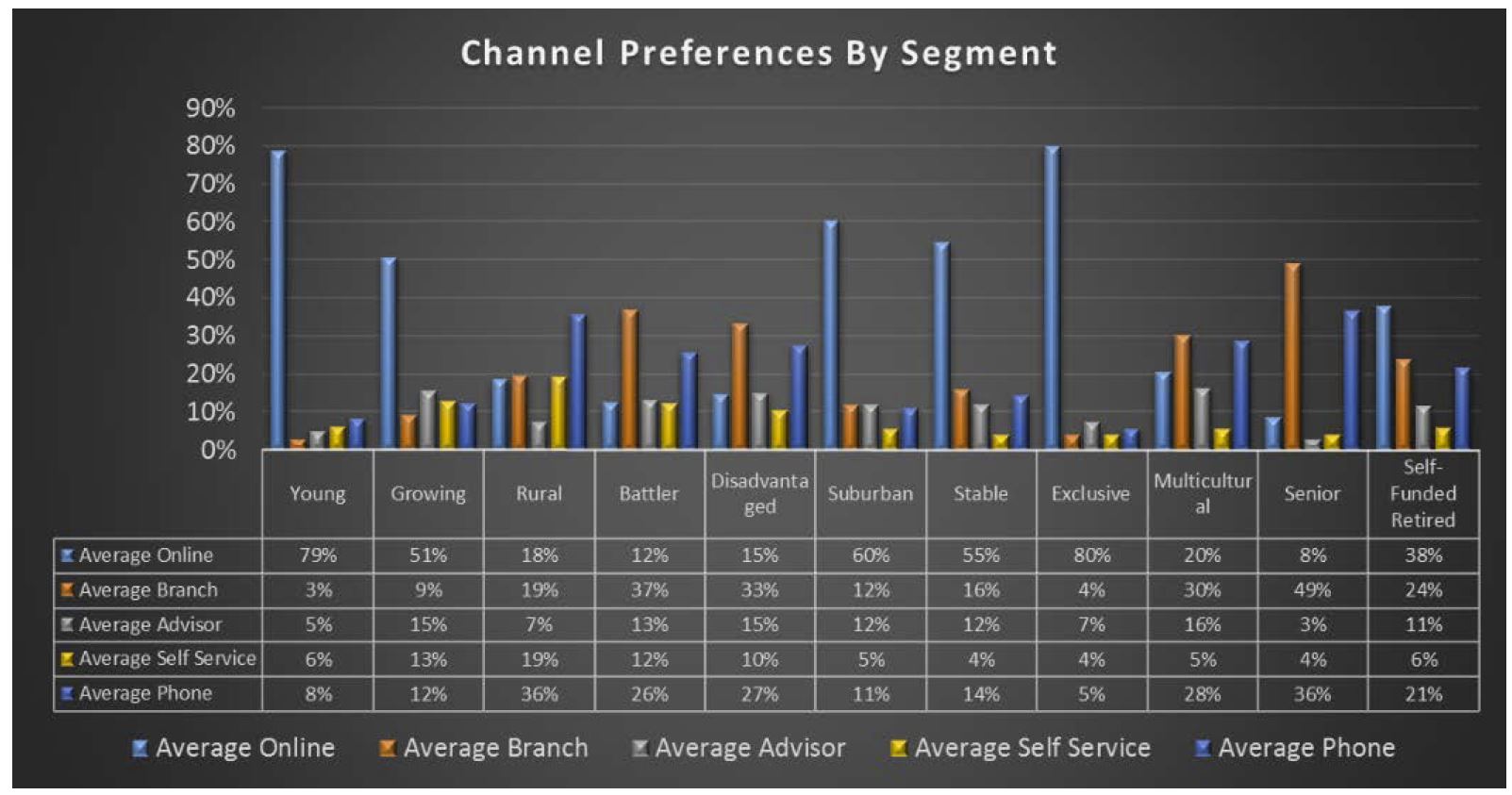

Our research shows that consumers have largely migrated into the digital world and have a strong expectation that existing banking services will be delivered via mobile devices and new enhanced services will be extended to them. Even “Digital Luddites”, the least willing to migrate are nevertheless finally moving into the digital domain. Now the gap between expectation and reality is larger than ever.

Our research shows that consumers have largely migrated into the digital world and have a strong expectation that existing banking services will be delivered via mobile devices and new enhanced services will be extended to them. Even “Digital Luddites”, the least willing to migrate are nevertheless finally moving into the digital domain. Now the gap between expectation and reality is larger than ever.

Looking across the transaction life cycle, from search, apply, transact and service; universally the desire by households to engage digitally is now so compelling that banks have no choice but to respond more completely.

We also identified a number of compelling new services which consumers indicated they were expecting to see, and players need to develop plans to move into these next generation banking offerings. Many centre around bots, smart agents and “Siri-Like” capabilities.

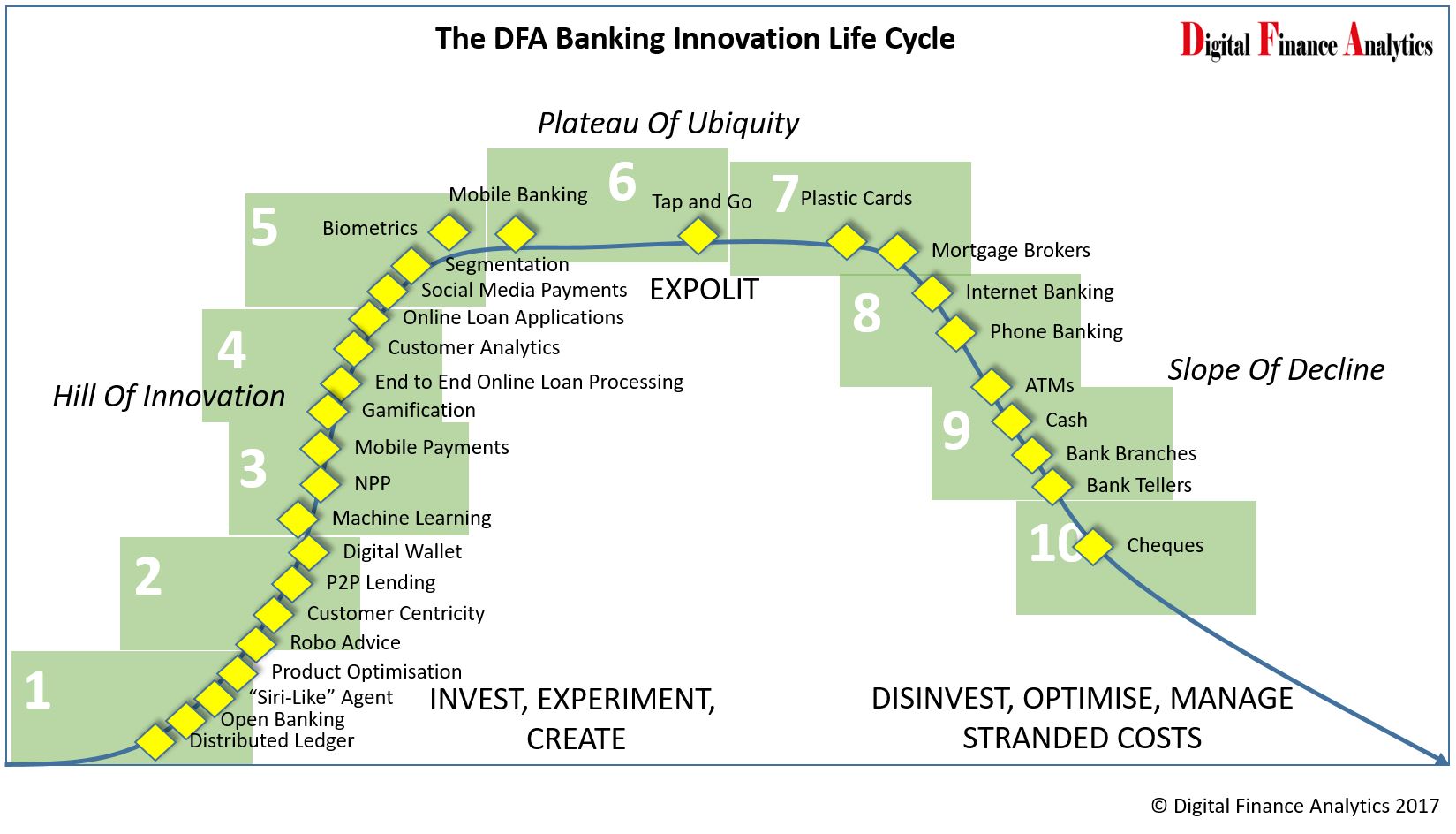

We have developed a mud-map to illustrate the journey of investment and disinvestment in banking. The DFA Banking Innovation Life Cycle, which is informed by our research, highlights the number of current assets and functions which are in the slope of decline, and those climbing the hill of innovation. A number of current “fixtures” in the banking landscape will decline in importance, and in relatively short order.

We are now at a critical inflection point in the development of banking as digital now takes the lead. Players must move from omni-channel towards digital first strategies, where the deployment of existing services via mobile is just the first stage in the development of new services, designed from the customers point of view and offering real value added capabilities. These must be delivered via mobile devices, and leverage the capabilities of social media, big data and advanced analytics.

We are now at a critical inflection point in the development of banking as digital now takes the lead. Players must move from omni-channel towards digital first strategies, where the deployment of existing services via mobile is just the first stage in the development of new services, designed from the customers point of view and offering real value added capabilities. These must be delivered via mobile devices, and leverage the capabilities of social media, big data and advanced analytics.

This is certainly not a cost reduction exercise, although the reduction in branch footprint, which we already see as 10% of outlets have closed in the past 2 years, does offer the opportunity to reduce the running costs of the physical infrastructure. Significant investment will need to be made in new core capabilities, as well as the reengineering of existing back-end systems and processes. At the same time banks must deal with their “stranded costs”.

The biggest challenges in this migration are cultural and managerial. But the evidence is clear that customers are already way ahead of where most banks are in Australia today. This means there is early mover advantage, for those who handle the transition swiftly. It is time to get off the fence, and on the digital transformation fast track. Now, banking has to be rebuilt from the bottom up. Digitally.

Request the report [44 pages] using the form below. You should get confirmation your message was sent immediately and you will receive an email with the report attached after a short delay.

Note this will NOT automatically send you our research updates, for that register here. You can find details of our other research programmes here.

[contact-form to=’mnorth@digitalfinanceanalytics.com’ subject=’Request The Quiet Revolution Report 3 – 2018′][contact-field label=’Name’ type=’name’ required=’1’/][contact-field label=’Email’ type=’email’ required=’1’/][contact-field label=’Email Me The Report’ type=’radio’ required=’1′ options=’Yes Please’/][contact-field label=’Comment if You Like’ type=’textarea’/][/contact-form]

The first edition is still available, in which we discuss the digital branding of incumbents and challengers, using our thought experiment.

Volume 2 from 2016 is also available.