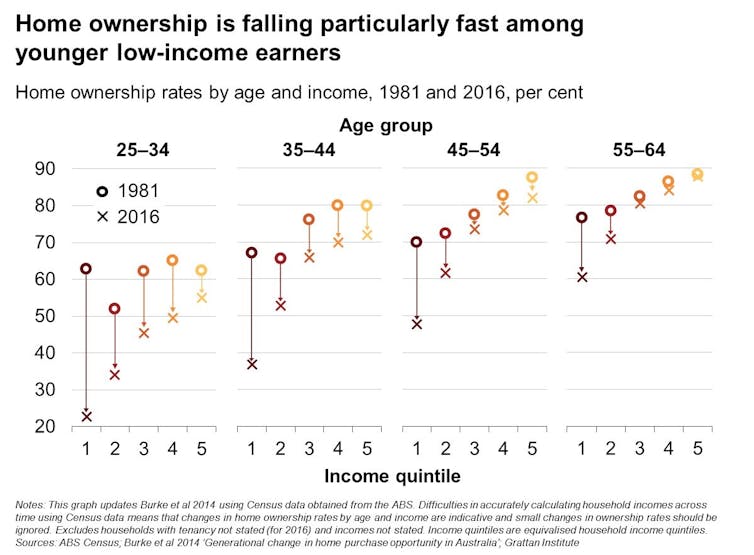

Rising housing costs are hurting low-income Australians the most. Those at the bottom end of the income spectrum are much less likely to own their own home than in the past, are often spending more of their income on rent, and are more likely to be living a long way from where most jobs are being created.

Low-income households have always had lower home ownership rates than wealthier households, but the gap has widened in the past decade. The dream of owning a home is fast slipping away for most younger, poorer Australians.

As you can see in the following chart, in 1981 home ownership rates were pretty similar among 25-34 year olds no matter what their income. Since then, home ownership rates for the poorest 20% have fallen from 63% to 23%.

Home ownership rates also declined more for poorer households among older age groups. Home ownership now depends on income much more than in the past.

Lower home ownership rates mean more low-income households are renting, and for longer. But renting is relatively unattractive for many families. It is generally much less secure and many tenants are restrained from making their house into a home.

For poorer Australians who do manage to purchase a home, many will buy on the edges of the major cities where housing is cheaper. But because jobs are becoming more concentrated in our city centres, people living on the fringe have access to fewer jobs and face longer commutes, damaging their family and social life.

Prices for low-cost housing have increased the fastest

The next chart shows that the price for cheaper homes has grown much faster than for more expensive homes over the past decade. This has made it much harder for low-income earners to buy a home.

If we group the housing market into ten categories (deciles), we can see the price of a home in the lowest (first and second) deciles more than doubled between 2003-04 and 2015-16. By contrast, the price of a home in the fifth, sixth and seventh deciles only increased by about 70%.

Tax incentives for investors may explain why the price of low-value homes increased faster. Negative gearing remains a popular investment strategy; about 1.3 million landlords reported collective losses of A$11 billion in 2014-15.

Many investors prefer low-value properties because they pay less land tax as a proportion of the investment. For example, an investor who buys a Sydney property on land worth A$550,000 pays no land tax, whereas the same investor would pay about A$9,000 each year on a property on land worth A$1.1 million.

Rising housing costs also hurt low-income renters

As this last chart shows, more low-income households (the bottom 40% of income earners) are spending more than 30% of their income on rent (often referred to as “rental stress”), particularly in our capital cities. In comparison, only about 20% of middle-income households who rent are spending more than 30% of their income on rent.

Why are more low-income renters under rental stress?

Secondly, rents for cheaper dwellings have grown slightly faster than rents for more expensive dwellings. Finally, the stock of social housing – currently around 400,000 dwellings – has barely grown in 20 years, while the population has increased by 33%.

As a result, many low-income earners who would once have been in social housing are now in the private rental market.

What can be done about it?

Increasing the social housing stock would improve affordability for low-income earners. But the public subsidies required to make a real difference would be very large – roughly A$12 billion a year – to return the affordable housing stock to its historical share of all housing.

In addition, the existing social housing stock is not well managed. Homes are often not allocated to people who most need them, and quality of housing is often poor. Increased financial assistance by boosting Commonwealth Rent Assistance may be a better way to help low-income renters meet their housing costs

Boosting Rent Assistance for aged pensioners by A$500 a year, and A$500 a year for working-age welfare recipients would cost A$250 million and A$450 million a year respectively.

Commonwealth and state governments should also act to improve housing affordability more generally. This will require policies affecting both demand and supply.

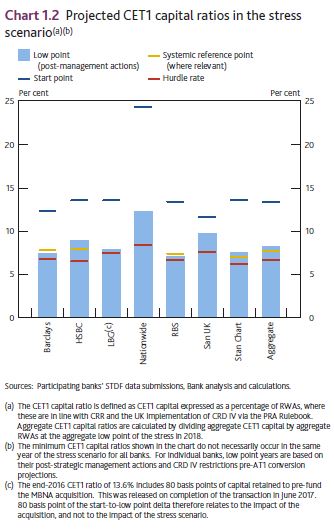

The Bank of England release their Financial Stability Report today, which includes the results of recent stress tests. Though the stress tests show that UK Banks could handle the potential losses in the extreme scenarios, the FPC is raising the UK counter cyclical buffer rate from 0.5% to 1% with binding effect from 28 November 2018. In addition buffers for individual banks will be reviewed in January 2018, to take account of the probability of a disorderly Brexit, and other risk factors hitting at the same time.

They highlighted risks from higher LTI mortgage and consumer lending, and the potential impact of rising interest rates. They still have their 15% limit on higher LTI income mortgages (above 4.5 times). They are concerned about property investors in particular – defaults are estimated at 4 times owner occupied borrowers under stressed conditions! Impairment losses are estimated at 1.5% of portfolio.

Beyond this, they discussed the impact of Brexit, and potential impact of a disorderly exit.

Finally, from a longer term strategic perspective, they identified potential pressures on the banks (relevant also we think to banks in other locations). There were three identified , first competitive pressures enabled by FinTech may cause a greater and faster disruption to banks’ business models than they currently expect; next the cost of maintaining and acquiring customers in a more competitive environment could reduce the scope for cost reductions or result in greater loss of market share and third the future costs of equity for banks could be higher than the 8% level that banks expect either because of higher economic uncertainty or greater perceived downside risks.

Here is the speech and press conference.

The FPC’s job is to ensure that UK households and businesses can rely on their financial system through thick and thin. To that end, today’s FSR and accompanying stress tests address a wide range of risks to UK financial stability. And they will catalyse action to keep the system well‐prepared for potential vulnerabilities in the short, medium and long terms.

In particular, this year’s cyclical stress test incorporates risks that could arise from global debt vulnerabilities and elevated asset prices; from the UK’s large current account deficit; and from the rapid build‐up of consumer credit. Despite the severity of the test, for the first time since the Bank began stress testing in 2014 no bank needs to strengthen its capital position as a result.

Informed by the stress test and our risk analysis, the FPC also judges that the banking system can continue to support the real economy even in the unlikely event of a disorderly Brexit. At the same time, the FPC has identified a series of actions that public authorities and private financial institutions need to take to mitigate some major cross cutting financial risks associated with leaving the EU.

The Bank’s first exploratory scenario assesses major UK banks’ strategic responses to longer term risks to banks from an extended low growth, low interest rate environment and increasing competitive pressures enabled by new financial technologies. The results suggest that banks may need to give more thought to such strategic challenges.

The Annual Cyclical Stress Test

Today’s stress test results show that the banking system would be well placed to provide credit to households and businesses even during simultaneous deep recessions in the UK and global economies, large falls in asset prices, and a very large stressed misconduct costs. The economic scenario in the 2017 stress test is more severe than the deep recession that followed the global financial crisis. Vulnerabilities in the global economy trigger a 2.4% fall in world GDP and a 4.7% fall in UK GDP falls.

In the stress scenario, there is a sudden reduction in investor appetite for UK assets and sterling falls sharply, as vulnerabilities associated with the UK’s large current account deficit crystallise. Bank Rate rises sharply to 4.0% and unemployment more than doubles to 9.5%. UK residential and commercial real estate prices fall by 33% and 40%, respectively. In line with the Bank’s concerns over consumer credit, the stress test incorporated a severe consumer credit impairment rate of 20% over the three years across the banking system as a whole. The resulting sector‐wide loss of £30bn is £10bn higher than implied by the 2016 stress test.

The stress leads to total losses for banks of around £50 billion during the first two years ‐ losses that would have wiped out the entire equity capital base of the banking system ten years ago. Today, such losses can be fully absorbed within the capital buffers that banks must carry on top of their minimum capital requirements. This means that even after a severe stress, major UK banks would still have a Tier 1 capital base of over £275 billion or more than 10% of risk weighted assets to support lending to the real economy.

This resilience reflects the fact that major UK banks have tripled their aggregate Tier 1 capital ratio over the past decade to 16.7%.

Countercyclical Capital Buffer

Informed by the stress test results for losses on UK exposures, the FPC’s judgement that the domestic risk environment—apart from Brexit—is standard; and consistent with the FPC’s guidance in June; the FPC is raising the UK countercyclical buffer rate from 0.5% to 1% with binding effect from 28 November 2018. In addition, as previously announced, capital buffers for individual banks will be reviewed by the PRC in January. These will reflect the firm‐specific results of the stress test, including the judgement made by the FPC and PRC in September. These buffers can be drawn on as necessary during a downturn to allow banks to support the real economy.

Brexit

There are a range of possible outcomes for the future UK‐EU relationship. Consistent with its remit, the FPC is focused on scenarios that, even if the least likely to occur, could have the greatest impact on UK financial stability. These include scenarios in which there is no agreement or transition period in place at exit. The 2017 stress test scenario encompasses the many possible combinations of macroeconomic risks and associated losses to banks that could arise in this event. As a consequence, the FPC judges that, given their current levels of resilience, UK banks could continue to support the real economy even in the event of a disorderly exit from the EU.

That said, in the extreme event in which the UK faced a disorderly Brexit combined with a severe global recession and stressed misconduct costs, losses to the banking system would likely be more severe than in this year’s annual stress test. In this case where a series of highly unfortunate events happen simultaneously, capital buffers would be drawn down substantially more than in the stress test and, as a result, banks would be more likely to restrict lending to the real economy, worsening macroeconomic outcomes. The FPC will therefore reconsider the adequacy of a 1% UK countercyclical capital buffer rate during the first half of 2018, in light of the evolution of the overall risk environment. Of course, Brexit could affect the financial system more broadly. Consistent with the Bank’s statutory responsibilities, the FPC is publishing a checklist of steps that would promote financial stability in the UK in a no deal outcome.

It has four important elements:

– First, ensuring that a UK legal and regulatory framework for financial services is in place at the point of leaving the EU. The Government plans to achieve this through the EU Withdrawal Bill and related secondary legislation.

– Second, recognising that it will be difficult, ahead of March 2019, for all financial institutions to have completed all the necessary steps to avoid disruption in some financial services. Timely agreement on an implementation period would significantly reduce such risks, which could materially disrupt the provision of financial services in Europe and the UK.

– Third, preserving the continuity of existing cross‐border insurance and derivatives contracts. Domestic legislation will be required to achieve this in both cases, and for derivatives, corresponding EU legislation will also be necessary. Otherwise, six million UK insurance policy holders with £20 billion of insurance coverage, and thirty million EU policy holders with £40 billion in insurance coverage, could be left without effective cover; and around £26 trillion of derivatives contracts could be affected. HM Treasury is considering all options for mitigating these risks.

– Fourth, deciding on the authorisations of EEA banks that currently operate in the UK as branches. Conditions for authorisation, particularly for systemic firms, will depend on the degree of cooperation between regulatory authorities. As previously indicated, the PRA plans to set out its approach before the end of the year. Irrespective of the particular form of the United Kingdom’s future relationship with the EU, and consistent with its statutory responsibility, the FPC will remain committed to the implementation of robust prudential standards. This will require maintaining a level of resilience that is at least as great as that currently planned, which itself exceeds that required by international baseline standards.

Biennial Exploratory Scenario

Over the longer term, the resilience of UK banks could also be tested by gradual but significant changes to business fundamentals. For the first time, the FPC and PRC have examined the strategic responses of major UK banks to an extended low growth, low interest rate environment combined with increasing competitive pressures in retail banking from increased use of new financial technologies. FinTech is creating opportunities for consumers and businesses, and has the potential to increase the resilience and competitiveness of the UK financial system as a whole. In the process, however, it could also have profound consequences for the business models of incumbent banks. This exploratory exercise is designed to encourage banks to consider such strategic challenges. It will influence future work by banks and regulators about longer‐term issues rather than informing the FPC and PRC about the immediate capital adequacy of participants.

Major UK banks believe they could, by reducing costs, adapt to such an environment without major changes to strategy change or by taking more risk. The Bank of England has identified clear risks to these projections:

– Competitive pressures enabled by FinTech may cause a greater and faster disruption to banks’ business models than they currently expect.

– The cost of maintaining and acquiring customers in a more competitive environment could reduce the scope for cost reductions or result in greater loss of market share.

– The future costs of equity for banks could be higher than the 8% level that banks expected in this scenario either because of higher economic uncertainty or greater perceived downside risks.

Conclusion

The FPC is taking action to address the major risks to UK financial stability. Given the tripling of their capital base and marked improvement in their funding profiles over the past decade, the UK banking system is resilient to the potential risks associated with a disorderly Brexit.

In addition, the FPC has identified the key actions to mitigate the impact of the other major cross cutting issues associated with a disorderly Brexit that could create risks elsewhere in the financial sector.

And on top of its existing measures to guard against a significant build‐up of debt, the FPC has taken action to ensure banks are capitalised against pockets of risk that have been building elsewhere in the economy, such as in consumer credit.

As a consequence, the people of the United Kingdom can remain confident they can access the financial services they need to seize the opportunities ahead.

CBA has today revealed a raft of changes including LVR caps and restrictions to rental income for serviceability that will impact mortgage brokers and their clients from next week.

On Saturday (2 December) CBA will introducing a new Home Loan Written Assessment document called the Credit Assessment Summary (CAS) for all owner occupied and investment home loan and line of credit applications solely involving personal borrowers.

“These changes further strengthen our responsible lending commitments related to the capture and documentation of customer information,” the bank said.

“The CAS will present a summary of the information you provided on behalf of your borrower(s) and / or that the Bank has verified (where relevant) and used to complete its credit assessment.”

It will include a summary of loan requirements and objectives, personal details and financial information, total monthly living expenses at a household level and information about the credit applied for.

CBA said the CAS will form part of the loan offer document packs for all owner occupied and investment home loan and line of credit applications.

“The CAS will not be issued for Short Form Top Up applications or applications involving non-person applicants (i.e. Trust or Company). The Document Checklist, which is on the last page of the Covering Letter to Borrower (Full Pack), will indicate when a CAS has been issued,” the group said.

“An application exception will be raised if the CAS is not returned or not signed by all personal borrowers. The application will not progress to funding until the exception is resolved.”

LVR and postcode restrictions

Meanwhile, CBA confirmed that it will introduce credit policy changes for certain property types in selected postcodes from Monday 4 December.

The changes include reducing the maximum LVR without LMI from 80 per cent to 70 per cent, reducing the amount of rental income and negative gearing eligible for servicing and changing eligibility for LMI waivers including all Professional Packages and LMI offers for customers financing security types in some postcodes.

“We continue to lend in all postcodes across Australia,” CBA said.

However, on Monday the bank will also introduce what it has called the Postcode Lookup Tool, which will be available under the Tools and Calculators section on CommBroker.

“This tool will provide you with detail on policies that may apply in certain areas. You should use this tool during your customer discussions to understand policies that may apply to postcodes in which they have expressed a home lending need. If policies apply, you should discuss these with your customers,” the bank said.

Long criticised as a laggard in digital technology, 2017 marks the year the super industry got serious says Willis Towers Watson.

Since 2013, we’ve surveyed superannuation funds on their use of digital. Four short years ago, the rate of uptake was slow and funds didn’t allocate significant budget to invest in technologies aimed at member education or engagement.

In 2017, our study showed 94 per cent of funds are increasing their use of digital – and their budgets – with a focus on developing new technologies and refining existing ones.

Nonetheless, the increased investment is still being stretched across a wide range of tools.

The big jump in this survey was in the use of social media – 88 per cent of funds in 2017, up from 47 per cent in 2015 and 35 per cent in 2013.

The reason? Members are driving the platforms that funds are using, rather than the other way around.

Social media is proving valuable to funds to leverage sponsored content and build brand awareness and trust – even if they aren’t talking about superannuation specifically.

It’s a big step forward to making super more approachable and relevant to the widest possible demographic.

But social media is not new – Facebook was founded 13 years ago, while Twitter launched in 2006. How funds embrace innovations that leverage social media platforms is something they need to address on a biannual basis at a minimum. This is a dynamic medium where a set-and-forget strategy will not work.

Innovation means different things to different funds. Compared to previous surveys, fewer funds consider themselves to be laggards. Early adopters of digital technology grew from 24 per cent to 31 per cent in 2017.

No-one is denying the clearly visible benefits of digital in creating personalised and targeted communication. But funds are questioning what needs to come next.

Regulation and compliance have always been issues with super funds in adopting technology and while some funds have started to use chat bots and are actively exploring AI, how exactly this may be used is still something for the future.

Problem solving a member’s simple queries using a chat bot seems like an effective use of technology but the industry remains convinced there will always be a need for human interaction.

Other financial services industries have embraced aspects of AI. StartUpCover, a joint venture between Willis Towers Watson and insurer CGU, launched a world-first Facebook Messenger chat bot this year.

It provides 24/7 insurance information and indicative quote within five minutes of messaging.

Clearly the technology is there to be leveraged, and its application for the superannuation industry is being worked through.

The 2016 Global Mobile Messaging Report, published by US communications company Twilio, showed that 46 per cent of consumers would like to learn about new products through messaging, while 85 per cent of consumers would like to reply to a message from a business or engage in conversation, noting that messaging is not a one-way communication channel.

Further research from the Centre for Generational Kinetics shows 41 per cent of Millennials would describe themselves as ‘truly satisfied’ if they could use messaging or SMS to connect with companies where they do business.

So, are super funds ready to support two-way communication via messaging? It’s another important question to be addressed.

Is there a digital saturation point?

We hosted a roundtable with fund marketing officers, heads of member engagement and digital experts where they talked a lot about following digital trends more broadly and using this as a way to influence their own future direction.

This means funds need to utilise their internal resources to be watching, learning and trialling new technologies that become popular and to assess what sticks with members.

Following the broader digital trends can be beneficial. It allows funds not to need to invent their own technology but rather adapt technology that is already being utilised.

But technology can’t just be used for technology’s sake. Like the debate over the use of apps by super funds, it needs to contribute to a fund’s member experience and create positive outcomes for their retirement strategy to assist funds to justify their investment in a new technology.

Do members want to check their super like they check their bank account balance?

With so much development in the digital space over the past five years, it makes sense that funds are continuing to test a number of digital options to see what works best for their members.

It’s a challenge for funds, servicing a huge and diverse group of members with varying attitudes, habits and priorities.We know that superannuation isn’t like other services. You don’t need to check your super account daily or weekly like you do with a bank account.

With an ageing demographic, and more members in retirement spending their savings, we’ll see a change in this behaviour.

However, long-term engagement, trust and loyalty are all things funds crave. So finding the right balance of tools that provide this to members is critical. A social media strategy is particularly crucial here.

Personalising super communication will continue to grow to a point where it is the norm rather than the exception.

Will data analytics have a greater role to play?

Data analytics will feed funds’ knowledge to understand the best tools to use for their members and where to focus their budgets. The use of data analytics can only increase.

The more funds can learn about how the digital tools their members are using are driving member outcomes, the more they can target their communication to make it more personal and engaging. Data analytics can reveal what is working already and what can be improved.

It will also assist funds in managing resources and budgets.

Digital tools can also be used in a more targeted manner, as we have seen with social media, which tends to be used for brand awareness rather than as a member education tool.

Do we have to be everywhere for everyone?

Consolidation of digital tools will come – it has to. However, this will bring a greater focus on an omni-channel approach to ensure a more consistent and co-ordinated member experience.

In the short term, funds will continue to explore a range of digital tools, but longer term, given limited resources, only those that drive member engagement and contribute to a fund’s overall strategy will survive.

What will this look like? AI, chat-bots or something we haven’t thought of yet? Watch this space. What we do know is there will be more to come.

Rick Body is head of digital solutions Australasia and Asia for Willis Towers Watson.

Amazon is well on the way to its goal of conquering the modern commercial world. The e-commerce, logistics, media and food titan is now the second biggest company in the world and Morgan Stanley predicts it will overtake Apple by the end of next year to become the globe’s first USD1 trillion company. Australian institutions, particularly the banks, are yet to feel the full force of Jeff Bezos’ global colossus but with Amazon’s arrival in Australia, that is all about to change.

THREE LESSONS FROM JEFF BEZOS

1. CUSTOMER OBESESSION.

At the core of Jeff Bezos’s leadership philosophy is the primacy of the customer. “Everything we’ve done, all the success we have, is at its root primarily due to the fact that we have put customers first” he says.

Amazon customers believe this as reflected in various metrics including its Net Promoter Score (NPS is a globally used and respected measure of the loyalty of an organisation’s customer relationships) of 61.

Further, Amazon is the second most admired company in the world, just behind Apple.

Our bank leaders also talk about the importance of putting the customer first but the key difference is that bank customers don’t believe the rhetoric. The average Net Promoter Score for the big four banks is -10 with the best (CBA) at -3 and the poorest (Westpac) at -15.

And not one of the big four Australian banks appears in BRW/Hays Group top ten admired companies.

It says a lot when the Treasurer of an unpopular government can gain easy political points by berating bank CEOs with the put-down that “your customers don’t like you very much”. It seems bank CEOs are even less popular than politicians.

Banks seem to be obsessively focussed on each other – witness the recent move by CBA to remove ATM fees which was followed within 24 hours by the other three.

“If you’re competitor-focused, you have to wait until there is a competitor doing something. Being customer-focused allows you to be more pioneering” says Bezos.

Here are four examples of where the banks wait for competitors or regulators to do something before they act.

1. Loyal existing home loan customers who don’t shop around. According to a recent report by Fairfax Media, this is costing customers nearly $5b a year.

2. Customers who have funds on deposit but don’t get paid any interest.

3. Open data. Customers believe that data about their banking records belongs to them and they want banks to embrace not frustrate open data.

4. Unfair terms in standard form contracts. Banks have taken advantage of their dominant bargaining position to impose unreasonable restrictions on customers who have little bargaining power.

Globalisation and technology are re-weighting this power imbalance. According to Bezos “the balance of power is shifting toward consumers and away from companies..… The right way to respond is to put the vast majority of your energy, attention and dollars into building a great product or service and put a smaller amount into shouting about it, marketing it.”

2. GROW, GROW, GROW.

Amazon is obsessed with driving growth from new customers, products and markets. Last quarter it had revenue of USD43b and this quarter it is expected to exceed USD55b.

The Amazon approach to growing customers is a simple cycle – cut prices to attract customers, which increases sales and attracts more customers, which allows the company to benefit from economies of scale until, ultimately, the company can cut prices again.

As an example, as soon as Amazon spent USD13.7b to acquire Whole Foods it cut some prices by around 40 per cent. Whole Foods is now selling a range of Amazon products and services through its 431 stores.

In recent times banks have used strategies like increasing fees and cutting costs in order to maintain profits and dividends. Bezos says “there are two kinds of companies, those that work to try to charge more and those that work to charge less. We will be the second.”

Invention is another key plank of Bezos’s philosophy. Amazon uses the internet to get maximum leverage from its fixed assets, and once it achieves enough volume of sales, the sum total of profits from all those sales exceed its fixed cost base, and it turns a profit.

Amazon is the ultimate scalable business. Amazon Web Services is the biggest cloud computing company in the world. The internet enables Amazon to quickly and successfully expand around the globe. It is now in 13 countries and employs more than 300,000 people and 45,000 robots to ship 1.6m packages a day.

Amazon dominates US online retail sales with a market share of 45 per cent. Given that 90 per cent of US retail sales are still made via bricks and mortar stores, the upside is enormous. Amazon has invested heavily in infrastructure too and now 44 per cent of Americans live within 32 km of an Amazon warehouse or delivery station hence their ability to offer fast delivery times.

Half of the households in the US subscribe to Amazon Prime which for USD5.99/month gives them services including steaming, video, music, e-books, free shipping & other deals.

Meanwhile our banks are getting smaller. They have retreated from failed off-shore operations and they’re offloading peripheral businesses like wealth management and insurance. A former CEO NAB was fond of remarking “I have never seen an organisation shrink to greatness” but that appears to be exactly what the big four banks are now trying to achieve.

3. LONG TERM VISION WITH EXECUTIVE REMUNERATION ALIGNED

Of course, its easier call the shots when you are the Executive Chairman, the founder and major shareholder but Bezos’ priorities have always been upfront – “if we take care of customers, the stock will take care of itself in the long term.”

Amazon has never been about profits, its all about growth. “If you’re very clear to the outside world that you’re taking a long-term approach, then people can self-select in” he says.

Clearly analysts and investors are buying this story. Wall Street analysts are almost unanimous in their “strong buy” recommendations notwithstanding traditional metrics which show:

PE Ratio is 230 and based on 2019 forecast it is still 75

ROE is 9 per cent and average over last 5 years is 5.5 per cent

Yield is 0 per cent – Amazon doesn’t pay dividends

Last year Bezos was not Amazon’s highest-paid employee. He received USD1.681m in total compensation of which USD81k was salary. Yet because he still owns 17 per cent, he is now the richest man in the world with a net worth of USD93b. Bill Gates is worth USD89b and Warren Buffett USD74b.

That’s a pretty good alignment of interest. Contrast this to ANZ’s former CEO Mike Smith who was paid $88m over 8 years when the share price actually fell during that period and his major strategy of expanding into Asia was immediately undone by his successor.

Australian bank bosses are paid huge sums regardless of shareholder return and their focus is excessively skewed to the short term. None have ever stood up to the markets like Bezos has and remember Bezos has talked like this from the onset.

AMAZON HAS THE BANKS’ ATTENTION & WITH GOOD REASON!

It’s only a matter of time before Amazon takes on Australia’s banks. Any market structure in which a small number of firms has the large majority of market share is at risk of being disrupted.

The four big banks are a similar size, they are cumbersome and are weighed down by antiquated ways of doing business. Despite or perhaps because they have shared the spoils of the banking market for over 25 years, their offerings are indistinguishable.

Australian banks still generate very acceptable ROEs around 14 per cent. Meanwhile, globally the banking industry’s ROE remains around 8 per cent to 10 per cent. This makes Australia’s banks even more attractive and as Bezos says “your margin is our opportunity.”

But Amazon wont tackle the banks head on, it will take them on where they are most vulnerable and where it can leverage its strengths including customer relationships, technology and data.

We only have to look at Amazon’s US banking activities to see where this is likely to be. It has a small-business lending arm that has already lent more than USD3b to more than 20,000 of the merchants on its e-commerce platform.

And it has a Visa credit card which rewards customers with benefits including 2 per cent discounts at restaurants, gas stations and drugstores. Meanwhile, Australian banks are winding back rewards from credit cards.

The banks are friendless. The Government’s popularity continues to decline and a banking inquiry or a Royal Commission now seems inevitable. No-one is going in to bat for the banks and repeated advertising campaigns are unlikely to shift public opinion.

It is worth noting the pronouncement by Keith Noreika, Acting Comptroller of the Currency (the agency that oversees US national banks) that “if a commercial company can deliver banking services better than existing banks, we hurt consumers by making it hard for them to do so.

For the politicians and bureaucrats it is sinking in that the quickest and easiest way to increase competition in banking is not to try to get the banks to change but rather to make it easier for new entrants. And the big players like Amazon have a head start over the fintech start-ups because they have deep pockets, customers and data.

WHERE TO FROM HERE?

The Amazon lesson is that in this new age, customers are ultimately the ones who will make or break any business. If the overseas experience is anything to go by, Australian consumers will embrace Amazon and Australian businesses also have the opportunity to grow as Amazon grows.

But Amazon itself faces several risks including its reliance on Bezos. There is also the risk of competition from other goliaths like Alibaba, Apple, Alphabet, Microsoft and Facebook as well as the prospect of an entirely new player disrupting the disruptors.

If Amazon does end up conquering the modern commercial world, would that be a good thing? At what stage might the regulators form the view that Amazon has gained too much power? Will it be too late then to unwind this behemoth?

The banks know what they are up against and are already responding. They still have customers, strong balance sheets and track records and they employ lots of very smart people but they are going to have to move more adroitly than they have done in the past.

We can expect the banks to push for the unwinding of the Four Pillars Policy to enable them to merge thereby reducing costs to better compete with the likes of Amazon.

One thing is for sure Jeff Bezos and Amazon have shown us all just how quickly the world of commerce is changing and the banking market is no exception.

Heritage Bank has announced that it has cut interest rates by up to 0.50 per cent on a range of its home loan offerings, with owner-occupier rates as low as 3.89 per cent. The cuts came into effect on Monday, 27 November.

Interest rates for Home Advantage variable owner-occupier loans with an LVR of less than 80 per cent have been cut by 0.10 per cent, with rates for $150,000 to $250, 000 loans now at 3.99 per cent, $250,000 to $700,000 loans at 3.94 per cent, and loans over 700,00 now at 3.89 per cent.

Investment Discount Variable Principal & Internist loans over $150,000 and with an LVR of less than 80 per cent have been cut by 0.30 per cent to 4.19 per cent.

First and second-year fixed rates for P&I investment loans have been cut by 0.20 per cent to 4.29 per cent.

Fixed rates for interest-only loans have also been cut, with rates for the first and second year cut by 0.40 per cent to 4.49 per cent.

Three-year and five-year fixed rates have also been reduced by 0.50 per cent to 4.49 per cent and 4.89 per cent, respectively.

CEO of Heritage Bank Peter Lock hopes that the decision will attract new customers to the regional lender.

“We’ve cut our rates to ensure we remain right in the sweet spot for competitiveness in the home loan market and to encourage even more people to enjoy the benefits of our people-first approach,” Mr Lock said.

“We do want to build and keep attracting new customers to the bank as part of a nationwide growth strategy.

“We’re a national player in the mortgage market via our broker partners, and our reduced rates, along with our overall service proposition, make us a great alternative for anyone in the market for a home loan.”

Heritage recently became the 22nd member of Aussie Home Loans’ lender panel, which Mr Lock believes will grant the bank access to more than 1,000 brokers across Australia and help the lender achieve its “national growth aspirations”.

Australian consumer lending fintech, MoneyMe, has finalised an AU$120 million asset-backed wholesale securitization facility led by $100 million from global investment manager, Fortress Investment Group, and joined with $20 million of bonds issued by corporate advisory, Evans & Partners.

We discussed MoneyMe a few weeks back, as a good example of the innovative new players pressing in on existing lenders with digitally sassy offerings to target market segments. We expect more disruption in the months ahead.

The funding places the fintech in an ideal position to continue capturing an even greater share of the digitally-savvy millennial consumer market over the next 3 to 5 years through an expanded product range, and additional delivery channels.

“A capital investment of this magnitude is recognition of the strength and depth of our value proposition, and an indication of the strong potential for Australian fintechs to capture serious wholesale market funding,” said Clayton Howes, CEO and Co-Founder of MoneyMe.

“A securitization warehouse structure and our institutional-grade treasury function akin to the major banks – combined with advanced automation and personalization capabilities, data-driven product integrity, cutting-edge technology for scalability, and a relatable brand personality – is a sure-fire way for Australian fintechs to attract the interest of global investors.

“This type of validation by a global investment management company, Fortress Investment Group, affirms a funding path that will now allow us to capitalise on growth and market share opportunities where bank branch models are not a natural fit in this digital age.

“As we further increase our independence and position as a mainstay in the improved distribution of consumer finance, we see this validation as a win for Australian fintech as a whole,” continued Clayton Howes.

Evans & Partners, the corporate advisory firm that led the bond issuance, has raised over $1.5 billion since 2008. The bond issued in this transaction is a publicly-tradable security, which investors are attracted to for the stability, yield, and track record of performance in this emerging sector.

The substantial capital injection will be used to fund continued loan book growth and facilitate both the expansion of MoneyMe’s distribution channels, and the launch of a series of niche loan products targeting the lucrative millennial market.

“As the millennial generation ages and gains even greater consumer power with their increasing incomes, their credit needs will also change and mature with them,” continued Clayton Howes.

“Our aim is to be there throughout their credit lifecycle journey, seamlessly delivering real-time finance solutions in the locations and format that allow focus to remain on the consumption experience and not the transaction itself,” concluded Clayton Howes.

Prime Minister Malcolm Turnbull and Treasurer Scott Morrison appear to have become hostages to rebel Nationals determined at all costs to secure a commission of inquiry into the banks.

On Monday a second federal National, Llew O’Brien, from Queensland flagged he is likely to cross the floor in the House of Representatives to support the private member’s bill sponsored by Queensland Nationals senator Barry O’Sullivan to set up a commission of inquiry that would investigate a broad range of financial institutions.

O’Brien, who has inserted an extra term of reference to protect people with mental health issues from discrimination, said “I like what I see” in the proposed bill. But he added that he would respect his party’s process. The bill is due to go to the Nationals party room on Monday.

The bill, which has the numbers to get through the Senate, is supported in the House by Queensland Nationals George Christensen, who after Saturday’s Queensland election apologised to One Nation voters for “we in the LNP” letting them down.

Backed by Christensen and O’Brien, together with Labor and crossbenchers, the bill would have the required 76 votes to enable its consideration by the House – although when it can get to be debated there is not clear.

In a discussion last week – later leaked – cabinet considered whether the government should adopt a pragmatic position and give in to calls for a royal commission. But Turnbull and Morrison have refused to do so.

Now the cabinet looks like it will have to decide whether to own the process of an inquiry or have it forced on it.

If Monday’s Nationals party meeting endorsed the bill, that would escalate the situation dangerously for the government, unless it had softened its opposition to an inquiry. It would amount to the minor Coalition partner formally rejecting a government position.

Cabinet would have to back down, or find some other way through.

As the crisis over the banking probe deepens for the government, there is currently no one with the authority or availability within the Nationals to manage the situation.

Barnaby Joyce remains leader but he’s absorbed in Saturday’s New England byelection, which is his path back into parliament. Senator Nigel Scullion is parliamentary leader but has little clout to curb the determined rebels.

With the commission push gaining momentum there is also less desire from some senior Nationals to fight it. Joyce is said to be relaxed about having a banking inquiry, which would be popular among voters and could be chalked up as a win for the Nationals.

The election loss in Queensland has strengthened the federal Nationals’ determination to pursue brand differentiation.

O’Sullivan has repeatedly referenced the example of Liberal Dean Smith’s use of a private member’s bill to pursue the cause of same-sex marriage, arguing he is following Smith’s pathway.

But there are still divided opinions within the parliamentary party about the bank probe. Resources Minister Matt Canavan, a member of cabinet, on Monday reaffirmed his opposition to a royal commission.

Joyce is likely to attend Monday’s party meeting although he will not be formally back in parliament by then.

Nationals are not clear whether they will elect their new deputy on Monday to replace Fiona Nash, who was ruled ineligible by the High Court because she had been a dual British citizen when she nominated. There is some speculation that this might be delayed to give aspirants time to lobby.

If there is no deputy leader chosen on Monday, it would mean that the minor party would be literally leaderless on the government front bench in the House of Representatives. Infrastructure Minister Darren Chester would be the most senior National sitting behind the Prime Minister in question time.

Christensen on Monday launched a website with a petition seeking signatures for a banking inquiry.

“Misconduct is not in the ‘past’”, he says on the site. “It is not being fixed by the industry to a standard acceptable to the community. Although positive steps are being made by government reforms, gaps still exist.

“Enough is enough…. unless the government acts to establish a Royal Commission, I will be acting before the end of this year to vote for a Commission of Inquiry into the banks.” The site also invites people “bitten by the banks” to ‘“tell your story”.

A commission of inquiry differs from a royal commission in being set up by and reporting to parliament, rather than being established by and reporting to the executive.

Author: Michelle Grattan, Professorial Fellow, University of Canberra

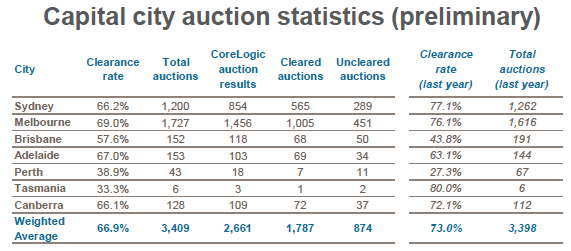

The current state of the property market in Sydney is still unclear following on from another weekend of auction results,” John Cunningham, president of the REINSW, told SCHWARTZWILLIAMS.

Cunningham said that 40 per cent of results have not been reported, and if those results represent a no sale, then the clearance rate for Sydney could be a lot lower than the 66.2 per cent being reported by CoreLogic.

Source: CoreLogic.

“With an initial clearance rate again in the mid 60 per cent range, the lack of clear data from the 40 per cent of unreported results fails to provide us with the real picture of the market,” he said.

“How many were withdrawn, how many were passed in, how many had no bids, needs to be known to get a clear picture,” said Cunningham.

“If we consider the worst case scenario that this missing 40 per cent did not sell, then the true clearance rate is 65 per cent of 60 per cent being 40 per cent,” said Cunningham.

“The reality from the word in the street is more like over 50 per cent of properties listed for auction at present are either selling at or before auction,” clarified Cunningham.

With so much uncertainty about auction clearance rates, Cunningham said the days on market “becomes the true test of what is really happening”. In the past year, days on market has risen from 33 days to 49 days, he said.

“It is sometimes taking longer to get vendors and buyers aligned on price,” said Cunningham.

Agent Nigel Mukhi from McGrath Lower North Shore Neutral Bay told SCHWARTZWILLIAMS he agrees with Cunningham’s assessment.

Though Mukhi said that the trend doesn’t apply to his office, when his competitors withdraw a property from auction or if they don’t sell, they don’t report the result.

Mukhi said that his office is achieving a clearance rate of 82 per cent, and that Sydney has to be analysed area by area.

Higher volumes weighing on Melbourne’s clearance rate

REIV President Richard Simpson told SCHWARTZWILLIAMS that the latest REIV data shows that 1,305 homes went to auction last weekend, recording a preliminary clearance rate of 69 per cent.

“Victoria’s weekly clearance rate has dipped below 70 per cent for the first time since June last year, as high auction volumes start to meet buyer demand.”

High auction volumes are set to continue, said Simpson, with around 1,300 auctions scheduled this coming weekend and a further 1,450 the following week.

“The city’s strong auction market is set to continue well into December with more than 3,600 auctions scheduled throughout the month,” said Simpson.

Regional areas experiencing strong clearance rates, said Simpson, especially Greater Geelong which achieved a clearance rate of 82 per cent.

Soft Northern Territory clearance rate

The Northern Territory recorded soft auction clearance rates last week, according to Karl Secondis of One Real Estate.

“Overall our market had a soft clearance rate of just 27 per cent,” he wrote in his report ‘The Auctioneer’.

“A large number of new listings have just hit the market this week which has strengthened auctions numbers in the final weeks leading into Christmas with a bumper week of over 30 auctions set to take place in week 49,” he wrote.

Five properties will go to auction in Gove on Wednesday night

Award-winning aggregator eChoice confirmed that Geoffrey Reidy and Andrew Barnden of Rodgers Reidy have been appointed as voluntary administrators of eChoice Limited and 13 subsidiary companies, pursuant to Section 436C of the Corporations Act.

The appointment was made by the secured creditor, Welas Pty Ltd, which has supported eChoice for many years but reached the view that it could no longer continue to support the aggregator in its current form.

Welas took the step to appoint the voluntary administrators to enable eChoice to assess its options on how to secure and sustain the future viability of the business.

“The voluntary administrators have not been appointed over any group companies with existing contracts with brokers or lenders,” the company said in a statement.

“Accordingly, the administration will not affect ongoing third-party stakeholder contractual obligations, such as trail payments by lenders to these companies and payments of trail by these companies to brokers.”

eChoice has confirmed earlier today that broker commissions, including trail payments made by lenders, will not be impacted by the appointment of voluntary administrators.

The eChoice aggregation business has experienced significant growth over the last financial year, with broker numbers up by 38 per cent over the 12 months to 30 June. Settlements also increased more than 25 per cent over the year to 30 September.

The Adviser understands that the administrators are seeking to sell off a number of underperforming entities within the eChoice Group, namely the aggregator’s lead generation and digital development arms. It is believed that the administrators are already aware of one major financial institution interested in the businesses.

“In the meantime, it is business as usual as far as possible,” the group said. “The focus of the business will be to ensure that employees, suppliers, lenders and brokers are able to deliver for customers as they always have.”