The latest data from the ABS shows home lending finance in June 2017 remained robust. In fact, overlaid with the latest home price data, and auction clearance rates, it looks like the property market has further to run, at least in the main markets of Sydney, Melbourne and Canberra. Loans for construction were up.

Or in other words, household debts will continue to climb, despite the “risk trimming” measures imposed by APRA.

Whilst the trend estimate for the total value of dwelling finance commitments excluding alterations and additions was flat, owner occupied housing commitments rose 0.5% while investment housing commitments fell 0.9%. However, in seasonally adjusted terms, the total value of dwelling finance commitments excluding alterations and additions rose 0.8%.

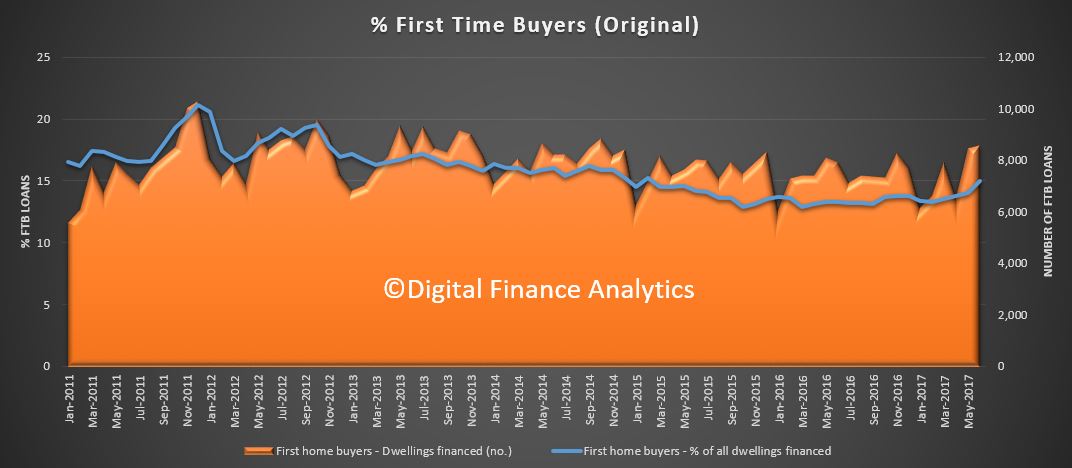

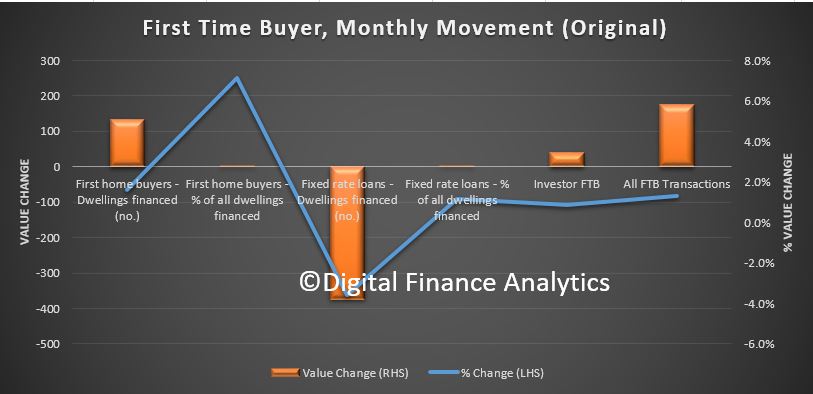

In original terms, the number of first home buyer commitments as a percentage of total owner occupied housing finance commitments rose to 15.0% in June 2017 from 14.0% in May 2017.

More first time buyers are entering the market now, reacting to the attractive rates selectively on offer.

More first time buyers are entering the market now, reacting to the attractive rates selectively on offer.

Overlaying the first time buyer investors, which was also quite strong, we see momentum building.

Overlaying the first time buyer investors, which was also quite strong, we see momentum building.

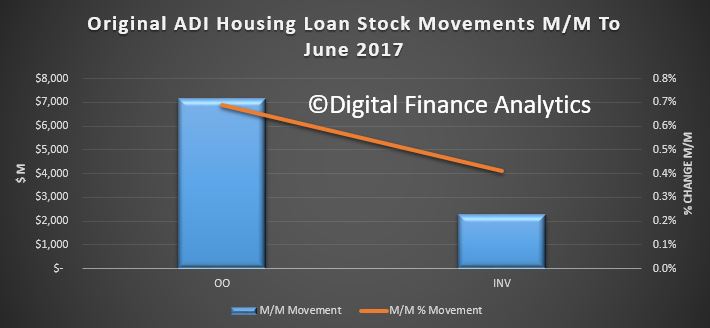

![]() In original terms, in the past month, owner occupied lending flows grew by $7 billion, whilst investment loans grew $2.1 billion.

In original terms, in the past month, owner occupied lending flows grew by $7 billion, whilst investment loans grew $2.1 billion.

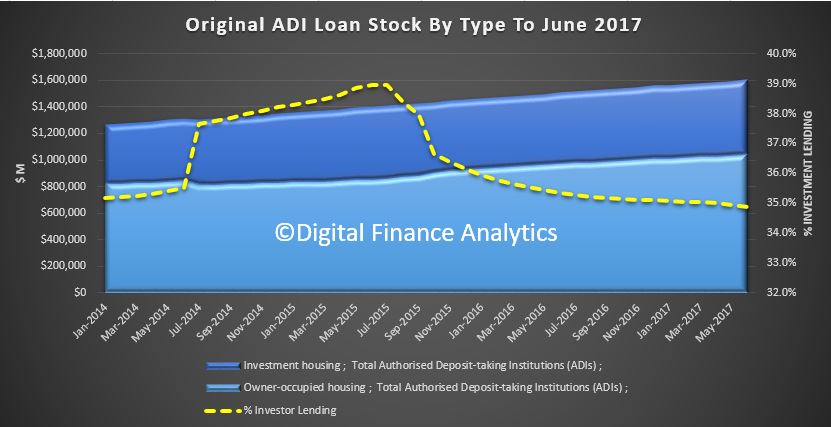

Looking at the trend adjusted stock, the mix of loans remained about the same at 35.9%, and overall loans pools grew.

Looking at the trend adjusted stock, the mix of loans remained about the same at 35.9%, and overall loans pools grew.

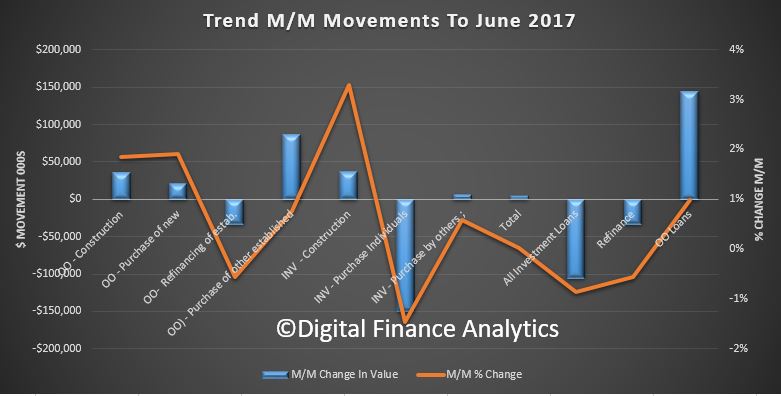

We see a rise in borrowing for both owner occupied and investment construction.

We see a rise in borrowing for both owner occupied and investment construction.

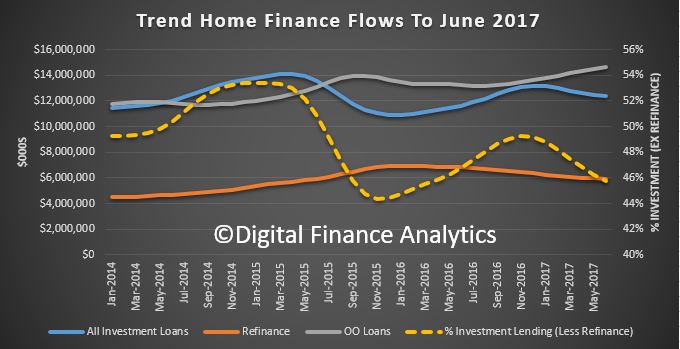

So here are the trend adjusted flows, with owner occupied loans on the rise, investment loans down a little, and refinanced loans also down.

So here are the trend adjusted flows, with owner occupied loans on the rise, investment loans down a little, and refinanced loans also down.

Worth noting that if you remove refinancing though, investment loans are still 46% of new loan flows. This is hardly indicative of a cooling of the property market.

Finally, the ABS says that in trend terms, the number of commitments for owner occupied housing finance fell 0.2% in June 2017.

Finally, the ABS says that in trend terms, the number of commitments for owner occupied housing finance fell 0.2% in June 2017.

In trend terms, the number of commitments for the construction of dwellings rose 1.9% and the number of commitments for the purchase of new dwellings rose 1.3%, while the number of commitments for the purchase of established dwellings fell 0.5%.

Finance for new dwellings appear to be getting a second wind with all eight state and territories showing growth in owner occupier loans for new dwellings during the month.