We discuss the latest ABS data.

Blog")

/

RSS Feed

Digital Finance Analytics (DFA) Blog

"Intelligent Insight"

We discuss the latest ABS data.

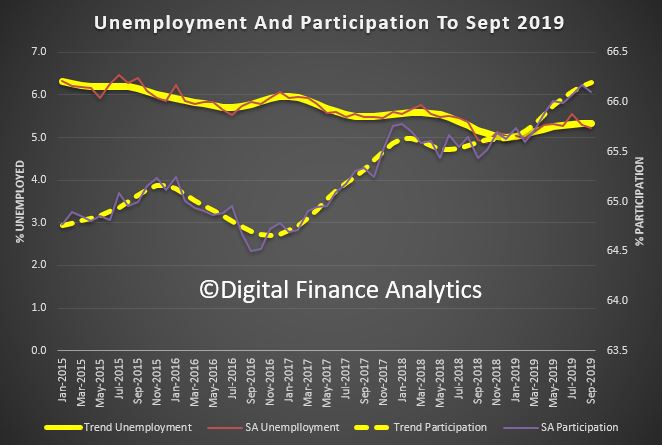

Australia’s trend unemployment rate remained steady at 5.3 per cent in September 2019, according to the latest information released by the Australian Bureau of Statistics (ABS).

“All of Australia’s key trend measures remained steady in September 2019, with the unemployment rate at 5.3 per cent and the participation rate at 66.2 per cent.” said ABS Chief Economist Bruce Hockman.

Employment and hours

In September 2019, trend monthly employment increased by around 20,200 people. Full-time employment increased by about 9,000 people and part-time employment increased by about 11,300 people.

Over the past year, trend employment increased by about 300,000 people (2.4 per cent), which continued to be above the average annual growth over the past 20 years (2.0 per cent). Full-time employment increased by 2.1 per cent and part-time employment increased by 2.9 per cent over the past year.

The trend monthly hours worked increased by 0.1 per cent in September 2019 and by 1.8 per cent over the past year. This was slightly above the 20 year average year-on-year growth of 1.7 per cent.

Annual Employment Change Over 20 Years (%)

Underemployment and underutilisation

The trend monthly underemployment rate remained steady at 8.4 per cent in September 2019, an increase of 0.1 percentage points over the past year. The trend monthly underutilisation rate remained steady at 13.7 per cent, an increase of 0.2 percentage points over the past year.

States and territories trend unemployment rate

The monthly trend unemployment rate remained steady in half of the states and territories in September 2019. Unemployment rate changes occurred in the Northern Territory (up 0.2 percentage points), Queensland and South Australia (up 0.1 percentage points) and Western Australia (down 0.1 percentage points).

Over the year, unemployment rates fell in Western Australia and the Australian Capital Territory, and increased in Victoria, Queensland, South Australia, Tasmania and the Northern Territory.

Seasonally adjusted data

The seasonally adjusted unemployment rate decreased by less than 0.1 percentage points to 5.2 per cent in September 2019, while the underemployment rate decreased by 0.2 percentage points to 8.3 per cent. The seasonally adjusted participation rate decreased by less than 0.1 percentage points to 66.1 per cent, and the number of people employed increased by an estimated 14,700.

The net movement of employed in both trend and seasonally adjusted terms is underpinned by around 300,000 people entering and leaving employment in the month.

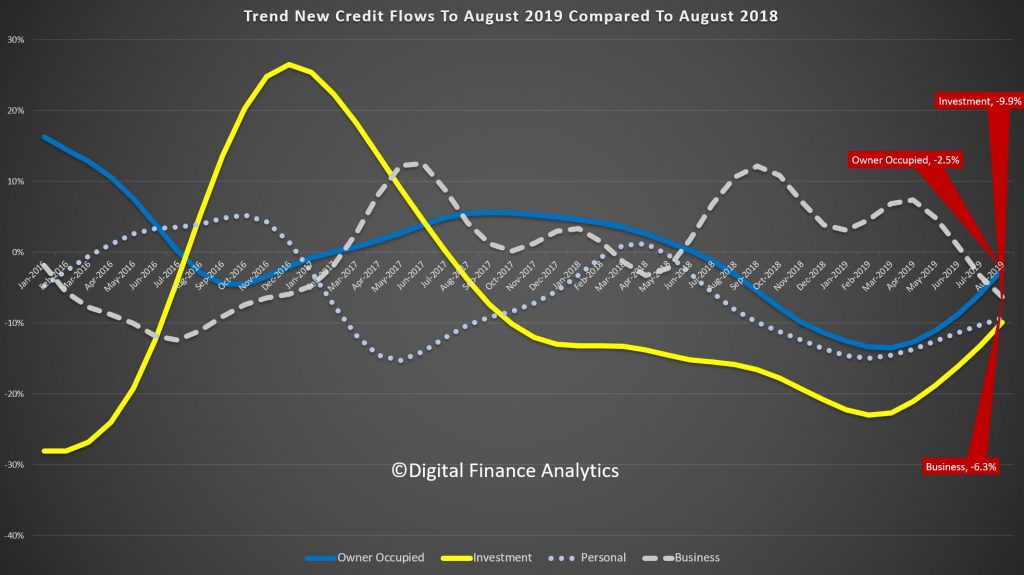

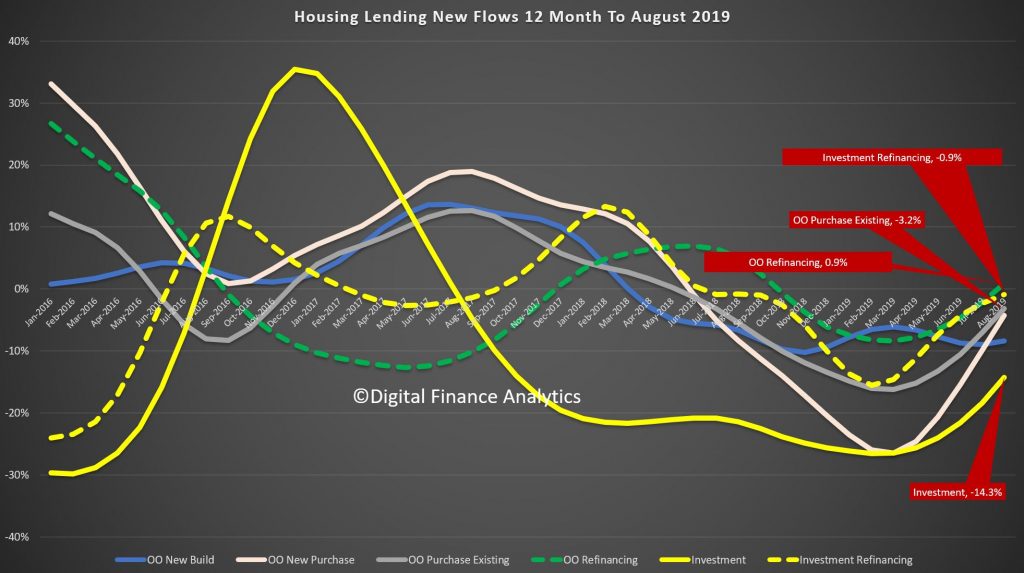

We review the latest from the ABS. 5601.0 – Lending to households and businesses, Australia, Aug 2019

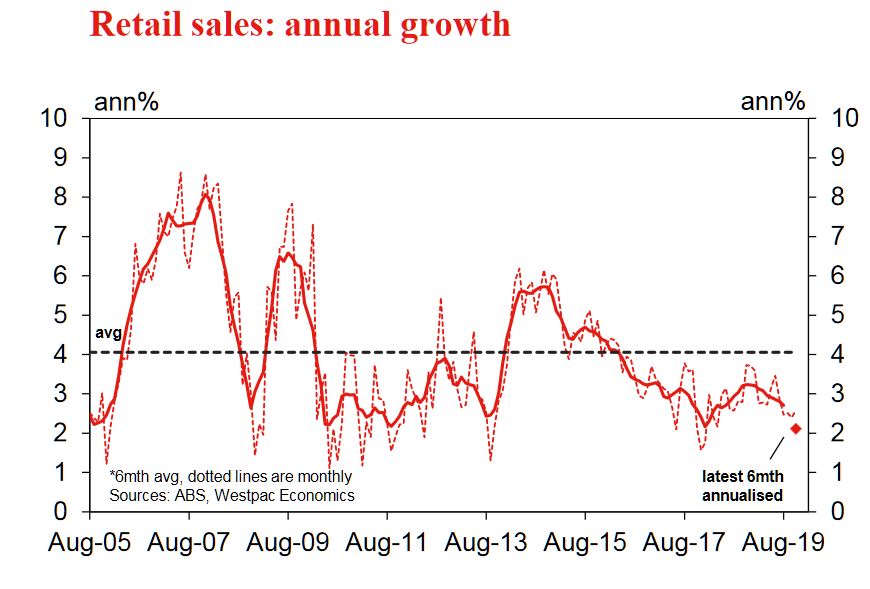

The ABS released their August 2019 retail figures today, and the data confirms the slowing economy, and that despite 2 rate cuts and tax refunds, households are unwilling or unable to spend. This is consistent with our surveys data which shows any free cash is going towards paying down debt, a sign of reduced levels of confidence and rising levels of financial stress.

Online retail turnover contributed 6.2 per cent to total retail turnover in original terms in August 2019. In August 2018, online retail turnover contributed 5.6 per cent to total retail.

The ABS released their latest trade figures today, and we look at the results.

We look at the latest from the ABS, on the day the RBA cut rates again.

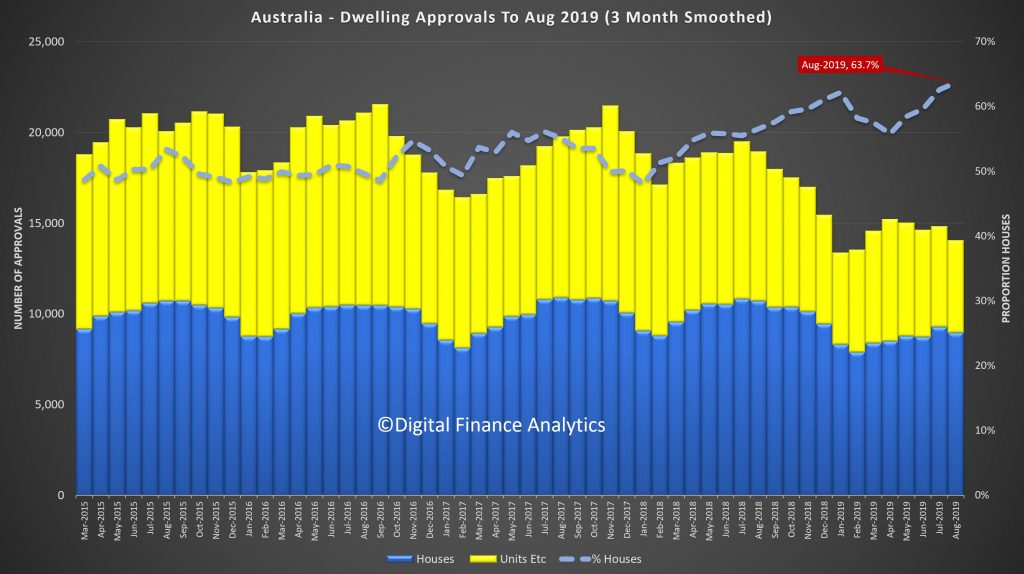

The ABS reported that the number of dwellings approved fell 3.9 per cent in August 2019, in trend terms, and has fallen for 21 months.

“The fall continues to be driven by private dwellings excluding houses, which decreased by 9.2 per cent in August,” said Daniel Rossi, Director of Construction Statistics at the ABS. “Private sector houses also fell, by 1.0 per cent.”

Across the states and territories, dwelling approvals decreased in August in the Australian Capital Territory (27.7 per cent), Northern Territory (8.7 per cent), New South Wales (5.4 per cent), Victoria (4.0 per cent), Queensland (2.3 per cent), South Australia (0.9 per cent), Tasmania (0.4 per cent) and Western Australia (0.2 per cent), in trend terms.

In trend terms, approvals for private sector houses fell in Western Australia (4.3 per cent), Queensland (1.7 per cent), South Australia (1.6 per cent) and Victoria (1.0 per cent), but rose in New South Wales (0.9 per cent).

The seasonally adjusted estimate for total dwellings approved fell 1.1 per cent in August, driven by a 2.4 per cent decrease in private houses. Private dwellings excluding houses rose 3.1 per cent in seasonally adjusted terms.

The value of total building approved rose 1.1 per cent in August, in trend terms, and has risen for eight months. The value of residential building fell 2.9 per cent, while non-residential building rose 5.7 per cent in trend terms.

“The value of non-residential building approved has risen for 12 months, to a record high of $4.8 billion. The rise in August was driven by approvals for health buildings in New South Wales,” said Mr Rossi.

According to the ABS Australian National Accounts, in seasonally adjusted terms, Australia became a net lender to overseas this quarter. This is the first time since June quarter 1975 that Australia has been a net lender as opposed to a net borrower. The ratio of net lending to overseas to GDP was 1.1% this quarter.

Graph 1. National net lending (net borrowing), relative to GDP, seasonally adjusted

At a sector level, net borrowing by general government declined to its

lowest level since September 2008, driven by sustained increases in

saving. Non-financial corporations’ net borrowing has also continued to

decline in line with slowing investment in non-residential buildings and

structures. Households recorded a small increase in net borrowing this

quarter, however the level remains lower than it was a year ago, driven

by weaker investment in dwellings.

Graph 2. Net lending (net borrowing), by sector, seasonally adjusted

National capital investment continues to fall

Household investment as a proportion of GDP has now declined for four

consecutive quarters. This decline continues to be driven by weakness in

dwelling investment in line with soft housing market conditions.

Capital investment by non-financial corporations as a proportion of GDP

was broadly unchanged this quarter. Machinery and equipment rose

strongly on the back of continued investment in autonomous machinery by

large mining companies. However, this was offset by softness in

non-residential building investment with the completion of projects

outstripping commencements this quarter. New engineering construction

was also weak, continuing to be impacted by liquified natural gas

projects transitioning from construction into the production phase.

General government investment as a proportion of GDP fell slightly to

3.6% this quarter. from 3.8% in March 2019. Despite the fall this

quarter, the ratio has been trending up since mid-2015, reflecting

increased public infrastructure investment by state and local general

governments to support population growth and growing demand for public

services.

Graph 3. Gross fixed capital formation, by sector, relative to GDP, seasonally adjusted

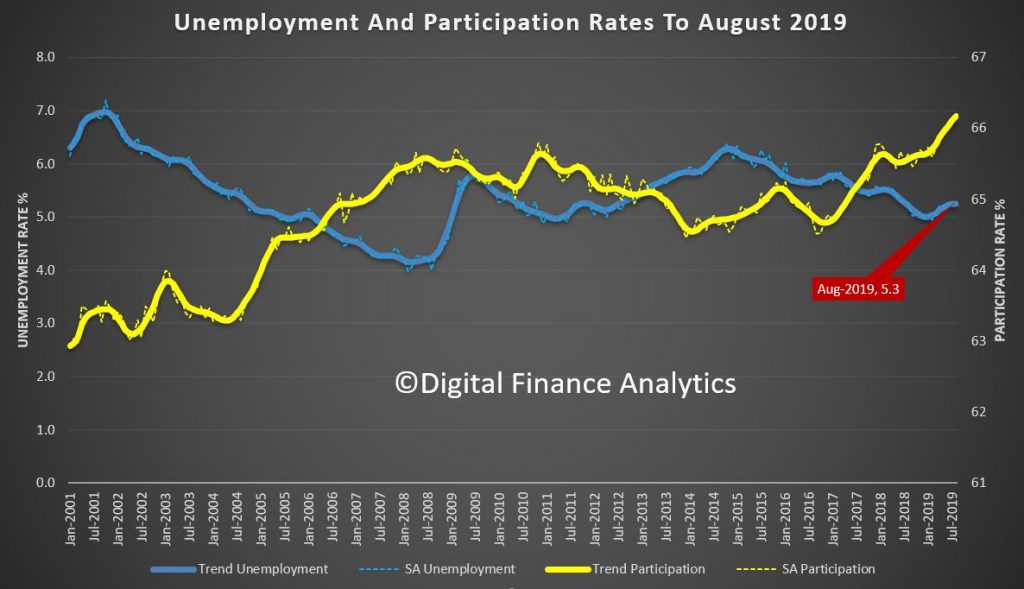

Australia’s trend unemployment rate increased in August 2019 to 5.3 per cent, from a revised July 2019 figure, according to the latest information released by the Australian Bureau of Statistics (ABS).

ABS Chief Economist Bruce Hockman said: “Australia’s trend unemployment rate increased to 5.3 per cent in August 2019. The trend participation rate increased further to 66.2 per cent, while employment continued to grow above the 20 year annual average.”

Employment and hours

In August 2019, trend monthly employment increased by around 22,000 people. Full-time employment increased by just over 7,000 people and part-time employment increased by an estimated 15,000 people.

Over the past year, trend employment increased by 0.3 million people (2.5 per cent) which was above the average annual growth over the past 20 years (2.0 per cent). Full-time employment increased by 2.4 per cent and part-time employment increased by 2.8 per cent over the past year.

The trend monthly hours worked increased by 0.1 per cent in August 2019 and by 1.7 per cent over the past year. This is in line with the 20 year average year-on-year growth of 1.7 per cent.

Underemployment and underutilisation

The trend monthly underemployment rate remained steady at 8.5 per cent in August, an increase of 0.1 percentage points over the past year. The trend underutilisation rate increased by 0.2 percentage points over the past year.

States and territories trend unemployment rate

The trend unemployment rate remained steady in most states and territories, except for South Australia (up 0.2 percentage points), Queensland and the Northern Territory (up 0.1 percentage points) and Western Australia (down 0.1 percentage points).

Over the year, unemployment rates fell in New South Wales, Western Australia and the Australian Capital Territory, and increased in Victoria, Queensland, South Australia, Tasmania and the Northern Territory.

Seasonally adjusted data

The seasonally adjusted unemployment rate increased by less than 0.1 percentage points to 5.3 per cent in August 2019, while the underemployment rate increased by 0.1 percentage points to 8.6 per cent. The seasonally adjusted participation rate increased by 0.1 percentage points to 66.2 per cent, and the number of people employed increased by an estimated 35,000.

The net movement of employed in both trend and seasonally adjusted terms is underpinned by around 350,000 people entering and leaving employment in the month.

Note that in original terms, the incoming rotation group in August 2019 had a higher employment to population ratio than the group it replaced (62.4% in August 2019, compared to 61.9% in July 2019), and higher than the sample as a whole (62.3%). The incoming rotation group had a lower full-time employment to population ratio than the group it replaced (41.2% in August 2019, compared to 42.3% in July 2019), and was lower than the sample as a whole (42.4%).

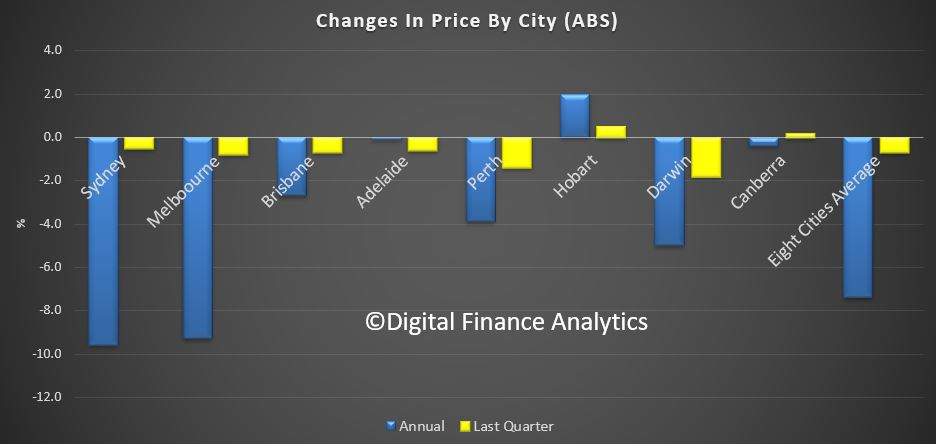

The ABS released their price data series to end June, so late as to be little more than a historical artifact, given the rate cuts, APRA changes and other events. Since June the kitchen sink has been thrown to try to force prices higher, though lead indicators are weakening again now. The total value of Australia’s 10.3 million residential dwellings fell by $17.6 billion to $6,610.6 billion in the June quarter 2019.

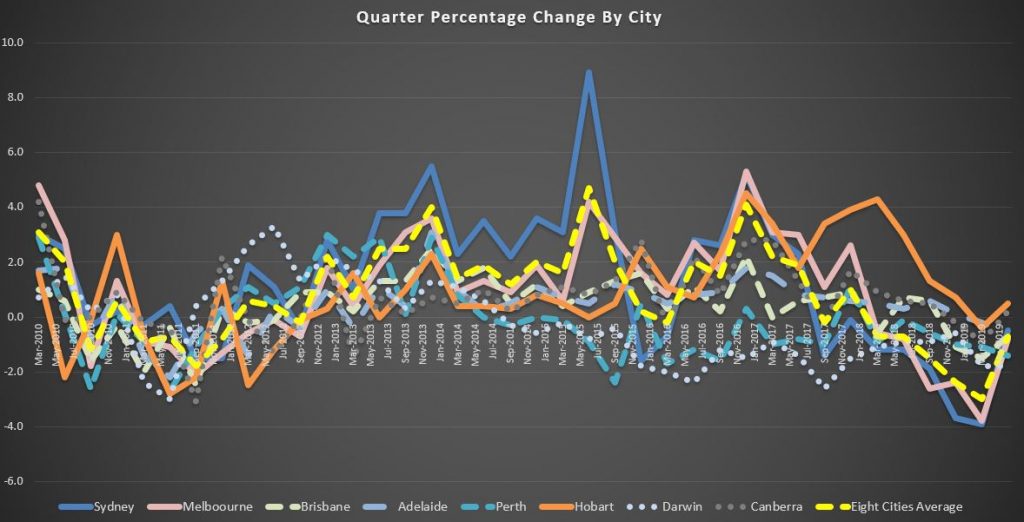

Residential property prices fell 0.7 per cent in the June quarter 2019, according to figures released today by the Australian Bureau of Statistics (ABS).

The falls in property prices were led by the Melbourne (-0.8 per cent) and Sydney (-0.5 per cent) property markets. All capital cities apart from Hobart (+0.5 per cent) and Canberra (+0.2 per cent) recorded falls in property prices in the June quarter 2019.

ABS Chief Economist Bruce Hockman said, “The falls in Melbourne were driven by detached dwellings, while attached dwellings drove the fall in Sydney”.

Through the year, residential property prices fell 7.4 per cent in the June quarter 2019. Prices fell 9.6 per cent in Sydney and 9.3 per cent in Melbourne. Hobart (+2.0 per cent) was the only capital city to record positive through the year growth.

“Sydney and Melbourne housing markets have seen residential property price falls moderate this quarter. A number of housing market indicators, such as auction volumes and clearance rates, have begun to show signs of improvement, though they remain below the levels seen one year earlier”, said Mr Hockman.

The total value of Australia’s 10.3 million residential dwellings fell by $17.6 billion to $6,610.6 billion in the June quarter 2019. The mean price of dwellings in Australia is now $638,900. The total value of residential dwellings has fallen for five consecutive quarters, down from $6,957.2 billion in the March quarter 2018.