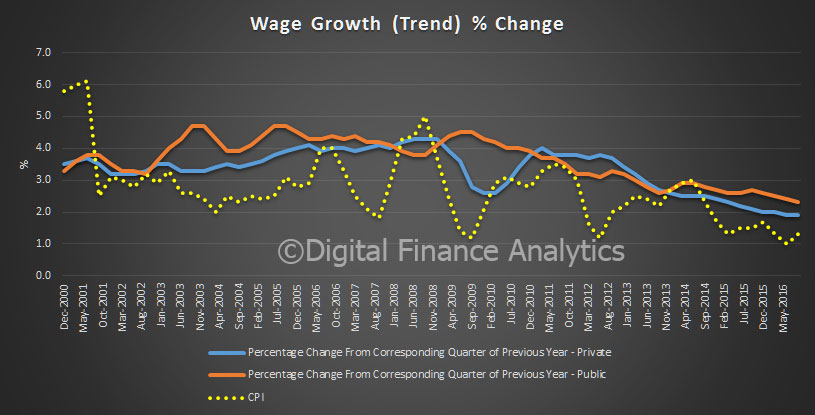

Through the year, All sectors rose 1.9%, a new low for the series. The Private sector through the year rise to the September quarter 2016 of 1.9% was lower than the Public sector rise of 2.3%.

Australia/Sector (original)

Australia/Sector (original)

September quarter wages growth was mainly influenced by increases to the national minimum wage and modern awards; regularly scheduled enterprise agreement increases; and salary reviews timed to coincide with the financial year. Of note, the 2015-16 Fair Work Commission decision increased the minimum wage and modern awards by 2.4%.

In the September quarter 2016, wages grew 0.7% for All sectors. Wages grew 0.8% in the Private sector and 0.9% in the Public sector.

The All sectors through the year rise was 2.0%. The Private sector rose 1.9% for the second quarter in a row, continuing the lowest through the year rise since the beginning of the series in September 1998. The Public sector rose 2.3%.

State/Territory (original)

In the September quarter 2016, the largest quarterly rise of 1.1% was recorded by Tasmania and the Northern Territory. The lowest quarterly rise of 0.5% was recorded by the Australian Capital Territory.

Rises through the year ranged from 1.7% for Western Australia to 2.3% for South Australia.

In the Private sector, the quarterly rise of 1.2% for Tasmania was the highest quarterly rise of all states and territories. The lowest quarterly rises of 0.4% was recorded by Western Australia.

Rises through the year in the Private sector ranged from 1.5% for Western Australia and the Northern Territory to 2.4% for Tasmania. Western Australia has recorded through the year growth of less than 2.0% since March quarter 2015.

In the Public sector, the Northern Territory recorded the highest quarterly rise (2.0%) of all states and territories. This was the largest rise for the Northern Territory since the December quarter 2009. Queensland and the Australian Capital Territory recorded 0.2%, the lowest of all states and territories. Changes in the timing of pay increases awarded under enterprise agreements can influence quarterly wages growth.

The Northern Territory recorded the highest through the year Public sector rise of all states and territories (3.6%) and Australian Capital Territory recorded the lowest (1.8%).

In the Private sector, Accommodation and food services recorded the highest quarterly rise of 1.7% and Mining the lowest growth over the quarter (0.1%). Rises through the year in the Private sector ranged from 1.0% for Mining to 2.5% for Electricity, gas, water and waste services.

Two Private sector industries recorded the lowest through the year growth since the start of the WPI: Mining; and Administrative and Support Services. Other resource related industries such as Construction and Professional, scientific and technical services recorded low through the year growth 1.7% and 1.6%, respectively, in the current quarter.

In the Public sector, Public administration and safety recorded the highest quarterly rise of 1.1%. Electricity, gas, water and waste services, Professional, scientific and technical services and Education and training recorded the lowest wages growth of 0.6%. Rises through the year in the Public sector ranged from 1.2% for Professional, scientific and technical services to 2.4% for Education and training.