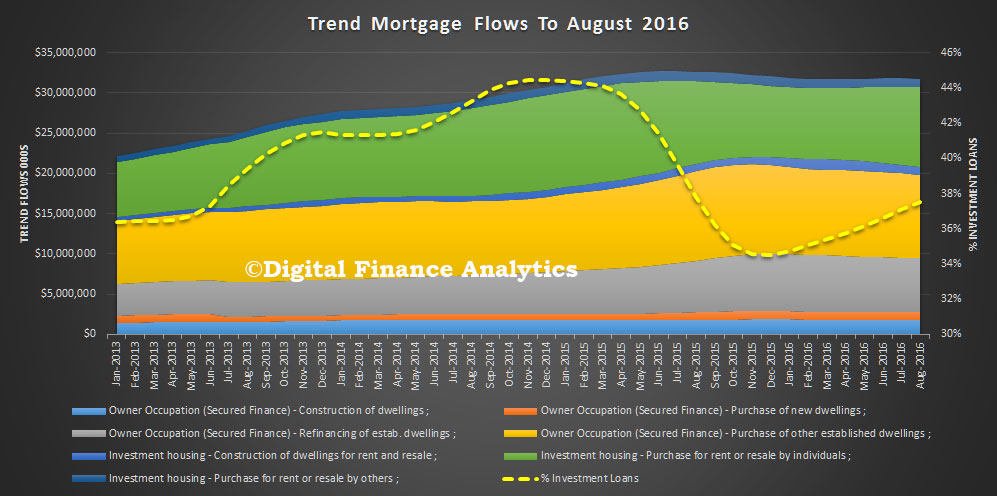

The latest data from the ABS on all lending flows shows the continued rise in investment housing, offset by a fall in owner occupied lending, and a small rise – housing apart – in commercial finance. Growth, other than for investment housing is insipid. We are walking a tightrope.

Overall lending flows, in trend terms, rose 0.1%, to $66.9 bn. Owner occupied housing commitments excluding alterations and additions fell 0.5% in trend terms. Total personal finance commitments fell 1.5% (within which revolving credit commitments fell 3.7%, and fixed lending commitments fell 0.1%). Total commercial finance commitments rose 0.6% with fixed lending commitments up 1.0%, while revolving credit commitments fell 0.6%. The value of total lease finance commitments rose 1.0%.

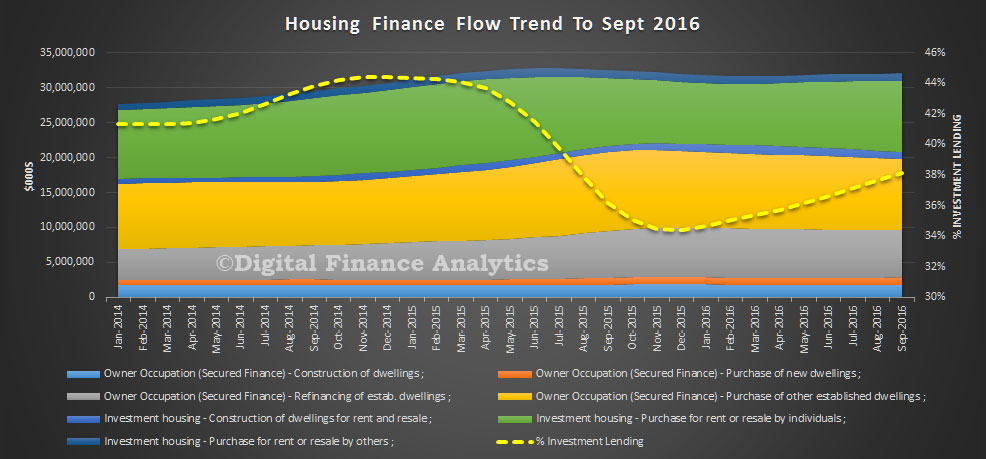

But looking at commercial lending (which includes both lending to investment property purchasers, and lending for other commercial purposes) we see lending for housing investment rose a massive 1.3% to $12.2bn, whilst lending for other commercial purposes rose 0.7% to $19.1bn. So the strongest growth was in investment housing.

As a result, the key ratios show a rise in investment lending as a proportion of the total, to 18.3%, a fall in owner occupied lending at 30.2% and non housing commercial up a little at 28.6%. Clearly without the surge in investment lending, total lending would have fallen.

As a result, the key ratios show a rise in investment lending as a proportion of the total, to 18.3%, a fall in owner occupied lending at 30.2% and non housing commercial up a little at 28.6%. Clearly without the surge in investment lending, total lending would have fallen.

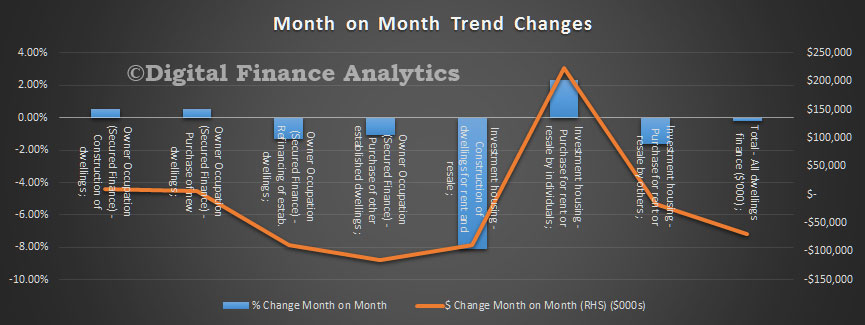

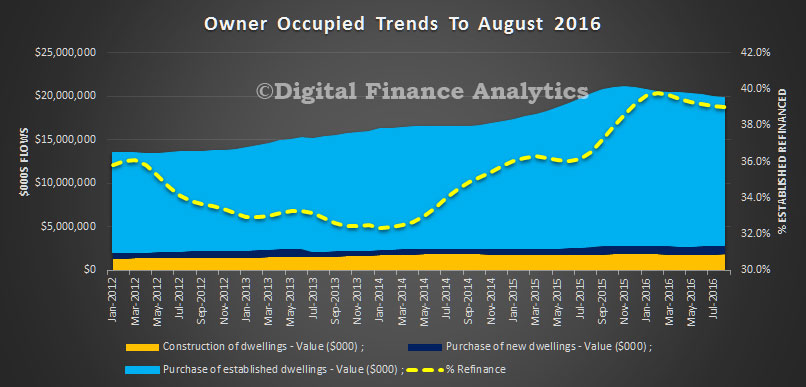

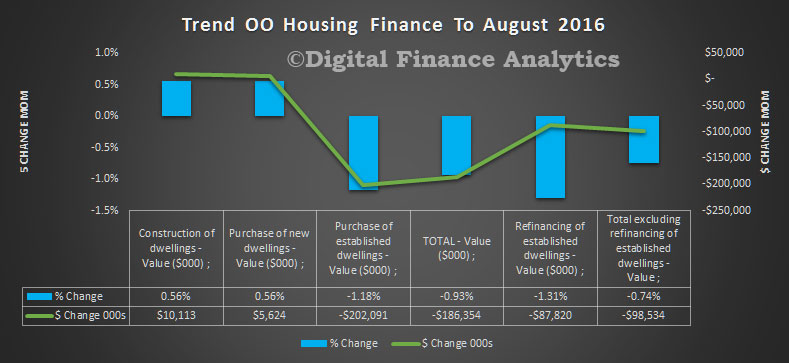

The same story is told looking at the more detailed housing series. Investment lending rose from 37.2% to 37.6% of flows ($12.2 bn), whilst refinance fell slightly to 20.8% ($6.7 bn). Funding for new buildings for owner occupied, and construction rose 0.4% ($2.8 bn), whilst purchase of established dwellings fell 0.8% and refinance ($6.7 bn) fell 0.5%.

The same story is told looking at the more detailed housing series. Investment lending rose from 37.2% to 37.6% of flows ($12.2 bn), whilst refinance fell slightly to 20.8% ($6.7 bn). Funding for new buildings for owner occupied, and construction rose 0.4% ($2.8 bn), whilst purchase of established dwellings fell 0.8% and refinance ($6.7 bn) fell 0.5%.

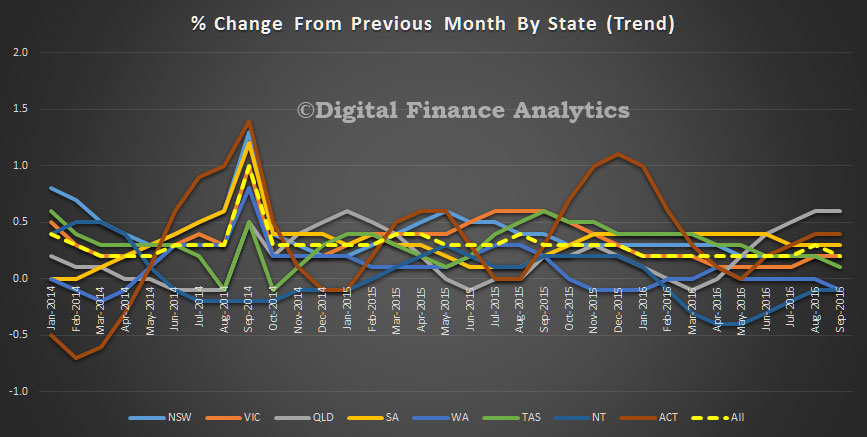

On the investment side, new construction fell 8.7% (0.9 bn) whilst purchase of existing housing stock rose 2.4% to $10.2 bn. The momentum was strongest in NSW and VIC.

This shows the dilemma for the RBA. The main growth engine in terms of credit is investment lending, yet this is the higher risk, and more concerning area of lending because if capital growth were to slow or reverse many investors would vote with their feet. We are on the edge of a precarious ridge, on one side is the slide into risky lending, on the other is the need for growth (at any cost). The pathway appears to becoming narrower, and the room more maneuver smaller. It is “the sharp edge” of policy.

We need to find a way to boost business lending, other than for investment housing. Current settings do not help. Cutting rates further will not either, and in all likelihood, the next turn in interest rates will be higher.