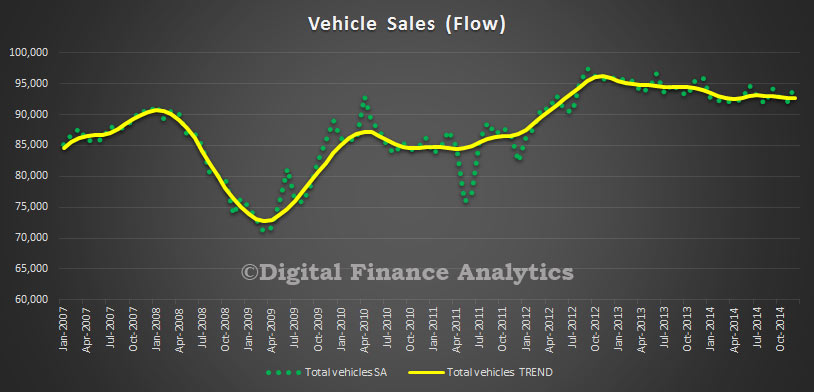

The ABS data for December, released today shows that the vehicle sales trend estimate of 92,618 decreased by 0.1% when compared with November 2014. The trend estimate has now decreased by 0.1% for five consecutive months, from a peak in 2012.

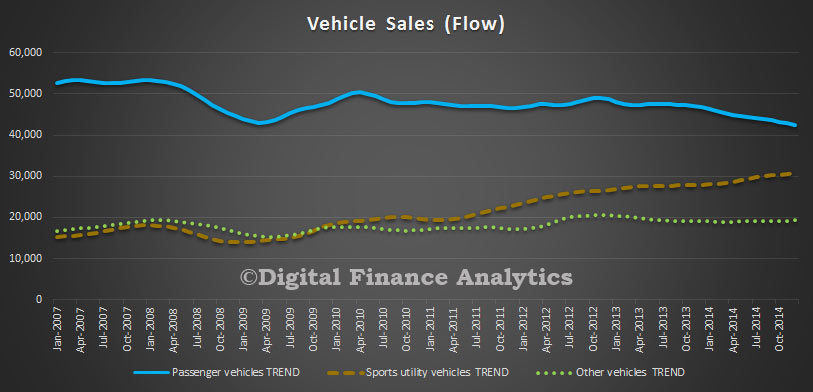

When comparing national trend estimates for December 2014 with November 2014, sales of Sports utility and Other vehicles both increased by 0.5% respectively. Over the same period, Passenger vehicles decreased by 0.8%. The rotation towards Sports utilities continues.

When comparing national trend estimates for December 2014 with November 2014, sales of Sports utility and Other vehicles both increased by 0.5% respectively. Over the same period, Passenger vehicles decreased by 0.8%. The rotation towards Sports utilities continues.

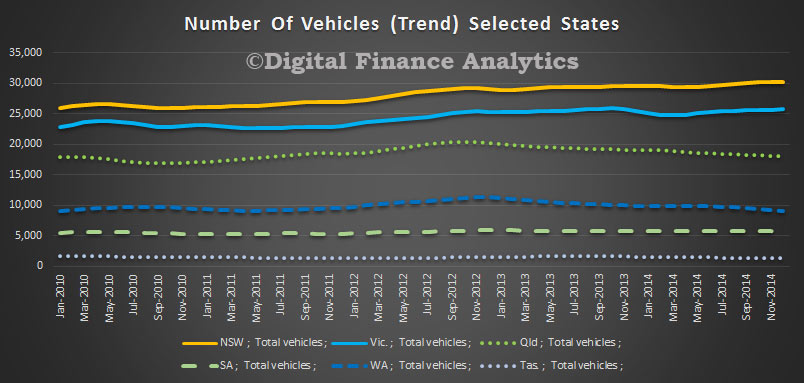

Five of the eight states and territories experienced a decrease in new motor vehicle sales when comparing December 2014 with November 2014. Western Australia recorded the largest percentage decrease (1.3%), followed by the Australian Capital Territory (1.2%) and South Australia (1.1%). Over the same period, both Victoria and the Northern Territory recorded the largest increase in sales of 0.3%. Queensland and WA have been showing the most consistent falls in recent months.

Five of the eight states and territories experienced a decrease in new motor vehicle sales when comparing December 2014 with November 2014. Western Australia recorded the largest percentage decrease (1.3%), followed by the Australian Capital Territory (1.2%) and South Australia (1.1%). Over the same period, both Victoria and the Northern Territory recorded the largest increase in sales of 0.3%. Queensland and WA have been showing the most consistent falls in recent months.