Supermarket operators will be able to coordinate immediately to ensure consumers have reliable and fair access to groceries during the COVID-19 pandemic following the ACCC’s granting of interim authorisation.

The interim authorisation will allow

supermarkets to coordinate with each other when working with

manufacturers, suppliers, and transport and logistics providers.

The purpose of this is to ensure the

supply and the fair and equitable distribution of fresh food, groceries,

and other household items to Australian consumers, including those who

are vulnerable or live in rural and remote areas.

The authorisation allows a range of

coordinated activities but does not allow supermarkets to agree on

retail prices for products.

“Australia’s supermarkets have experienced

unprecedented demand for groceries in recent weeks, both in store and

online, which has led to shortages of some products and disruption to

delivery services,” ACCC Chair Rod Sims said.

“This is essentially due to unnecessary

panic buying, and the logistics challenge this presents, rather than an

underlying supply problem.”

“We recognise and appreciate that

individual supermarket chains have already taken a number of important

steps to mitigate the many issues caused by panic buying. We believe

allowing these businesses to work together to discuss further solutions

is appropriate and necessary at this time,” Mr Sims said.

The ACCC granted interim authorisation on Monday afternoon after receiving the application last Friday.

“We have worked very swiftly to consider

this interim authorisation application, because of the urgency of the

situation, and its impact on Australian consumers,” Mr Sims said.

The Department of Home Affairs has

convened a Supermarket Taskforce, which meets regularly to resolve

issues impacting supermarkets. Representatives from government

departments, supermarkets, the grocery supply chain and the ACCC are on

the Taskforce. The interim authorisation applies to agreements made as a

result of Taskforce recommendations.

This authorisation applies to Coles,

Woolworths, Aldi and Metcash. It will also apply to any other grocery

retailer wishing to participate. Grocery retailers, suppliers,

manufacturers and transport groups can choose to opt out of any

arrangements.

The ACCC will now seek feedback on the application. Details on how to make a submission are available on the ACCC’s public register along with a Statement of Reasons.

The ACCC has provided urgent interim authorisation to allow the Australian Banking Association (ABA) and banks to work together to implement a small business relief package.

The package will allow for the deferral of

principal and interest repayments for loans to small businesses, in all

sectors, impacted by the COVID-19 pandemic.

The ACCC granted the interim authorisation this afternoon after the ABA’s application was lodged last night.

“The ACCC recognises the significant

financial hardship many Australian small businesses and their staff are

experiencing as a result of this unprecedented crisis,” ACCC Chair Rod

Sims said.

“We recognise the urgency of this issue.

We consider that this relief package will enable banks to quickly

provide relief to impacted businesses, and allow them to keep employing

their staff.”

“Importantly, interim authorisation does

not mean that individual banks can’t decide to offer more favourable and

tailored terms to their small business customers experiencing financial

hardship during these times.”

The interim authorisation applies to all

ABA member banks who agree to participate, which at this stage includes

AMP Bank, ANZ, Bank Australia, Bank of Queensland Limited, Bendigo and

Adelaide Bank Limited, Commonwealth Bank of Australia, HSBC, Macquarie

Bank, National Australia Bank, Suncorp Bank and Westpac.

The package includes a deferral of

principal and interest repayments for all term loans and retail loans

for 6 months, for small business customers with less than $3 million in

total debt owed to credit providers.

At the end of the deferral period

businesses will not be required to pay the deferred interest in a lump

sum. Either the term of the loan will be extended or the level of loan

repayments will be increased.

The ABA sought ACCC interim authorisation

on behalf of its members because the relief package involves

coordination by competing banks, actions that would otherwise raise

concerns under Australian competition laws.

Having granted interim authorisation for

the package, the ACCC will seek feedback on the ABA’s application for

authorisation. More information, including the ACCC’s statement of

reasons, is available at Australian Banking Association.

Background

ACCC authorisation provides statutory

protection from court action for conduct that might otherwise raise

concerns under the competition provisions of the Competition and

Consumer Act 2010. Broadly, the ACCC may grant an authorisation when it

is satisfied that the public benefit from the conduct outweighs any

public detriment.

We discuss the recent ACCC report on the Private Health sector, where the number of households covered is decreasing, premiums are rising faster than wages or inflation, more policies have exclusions and more households are being hit with a “gap” payment.

Plus there are concerns about data privacy especially relating to third party health and fitness apps. There is a lot which needs attention. Perhaps the industry should see a Doctor!

The ACCC just released their 21st report into the Private Health Insurance Sector, which analyses key competition and consumer developments and trends in the private health insurance industry to 30th June 2019 that may have affected consumers’ health cover and out-of-pocket expenses. This report also continues the ACCC’s focus on adequate private health insurer communications to their consumers, including on detrimental policy changes, as well as potential emerging issues in the use of consumer data.

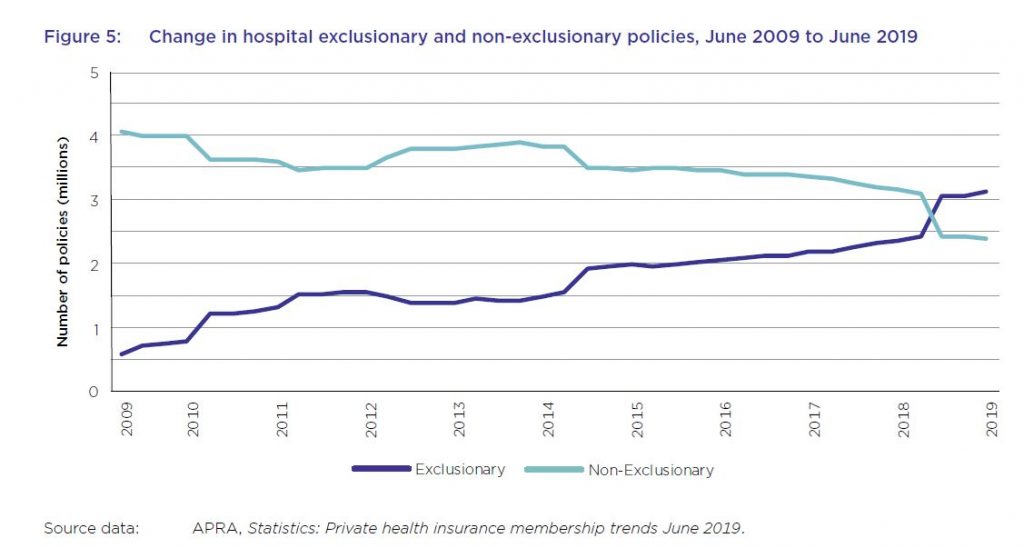

And in summary the system is unwell. Private health insurance premiums rise faster than income despite growing exclusions. For the first time, the majority of hospital treatment policies held by Australians now contain exclusions with more than 57 per cent of policies containing exclusions, up from about 44 per cent in the previous year. This chimes with our household surveys which shows more younger people are jettisoning their policies, or not signing up in the first place. This is a wicked problem, as more sick people as a total proportion are within the system, meaning that costs are becoming more concentrated.

Plus, the ACCC notes that consumer data collected by private health insurers and other businesses, for example through wellbeing apps and rewards schemes, can be used for a number of purposes such as targeted marketing, including from third parties.

Key industry data used and relied upon by the ACCC includes industry statistics and data collected by the Australian Prudential Regulation Authority (APRA) and private health insurance complaints data from the Private Health Insurance Ombudsman (PHIO).

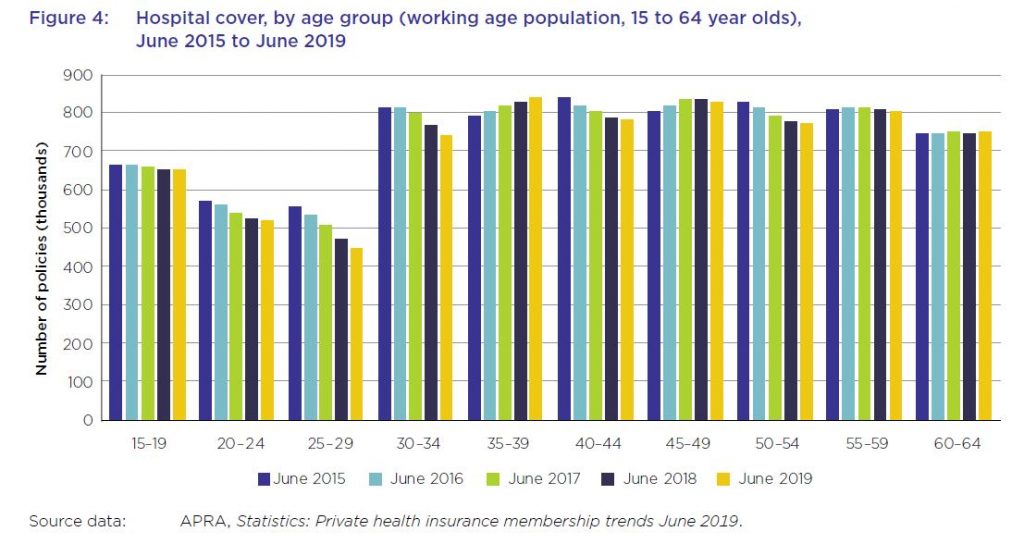

As at 30 June 2019, 13.6 million Australians, or 53.6 per cent of the population, had some form of private health insurance. This represents a membership reduction of 0.6 per cent from June 2018 (54.2 per cent). The Australian population grew by 396 722, or almost 1.6 per cent, during this period. The decline is sharpest among younger age groups.

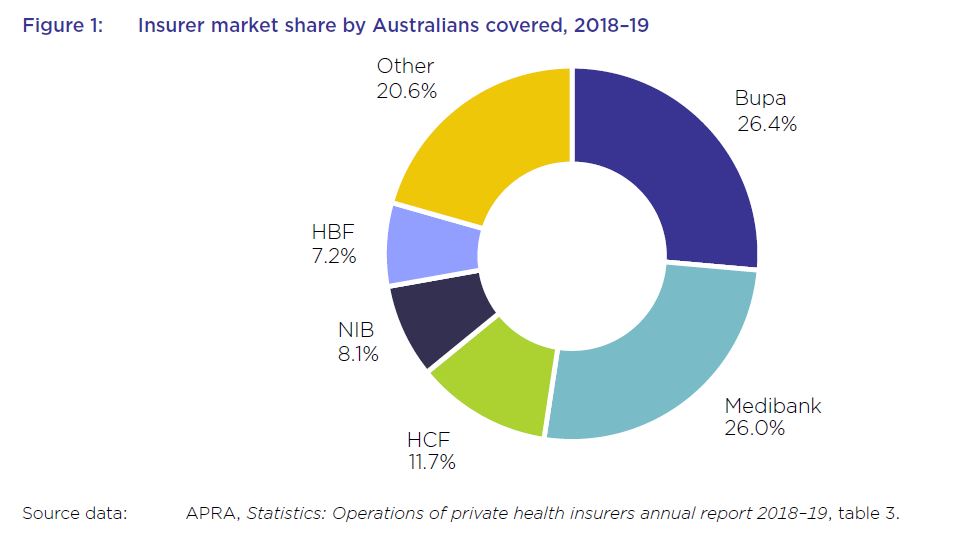

The five largest health insurers have a combined market share of almost 79.5 per cent and contributed to almost 77.5 per cent of total health fund benefits paid in 2018–1915, with Bupa and Medibank contributing 26.7 per cent and 25 per cent respectively.

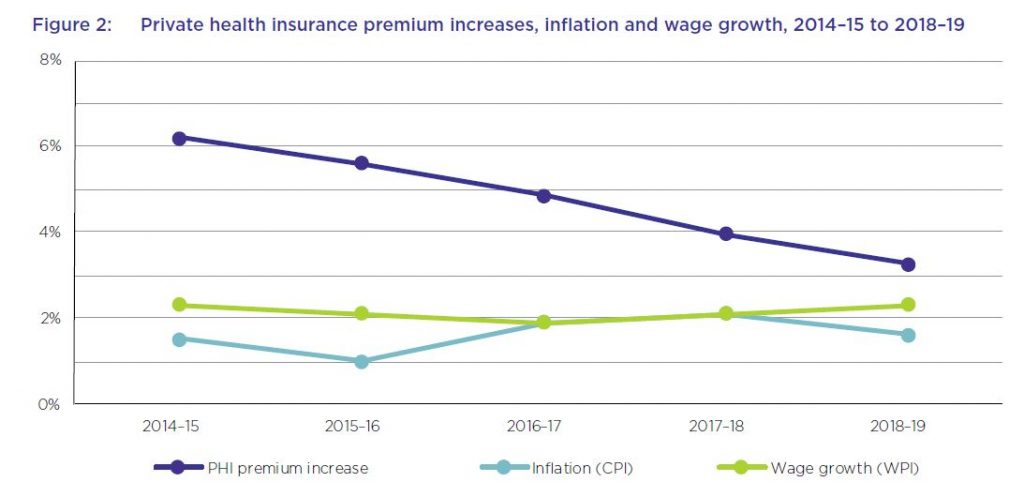

The average premium increase of 4.8 per cent per year over this period has been higher than the average annual growth in the wage price index (2.1 per cent) and the consumer price index (1.6 per cent) over the same period. While the rate of the average yearly premium increases has been decreasing each year over the past five years, and was 3.25 per cent in 2018–19, the average industry premium change for 2020, to take effect on 1 April 2020, will be 2.92 per cent – still well above wages growth.

From June 2018 to June 2019, the proportion of hospital policies held with exclusions increased by almost 14 per cent. For the first time, the majority of policies held now have exclusions.

The number of exclusionary policies held increased by over 650 000 from June 2018 to September 2018, with an equivalent reduction in non-exclusionary policies during the same period. APRA’s statistics did not indicate the reasons for this rise in the number of exclusionary policies during the reporting period. However, analysis by Silvester and others has suggested that less expensive exclusionary policies may appeal both to existing policyholders whose policies have become unaffordable, as well as to young people buying health insurance to avoid LHC loading and the Medicare levy surcharge.

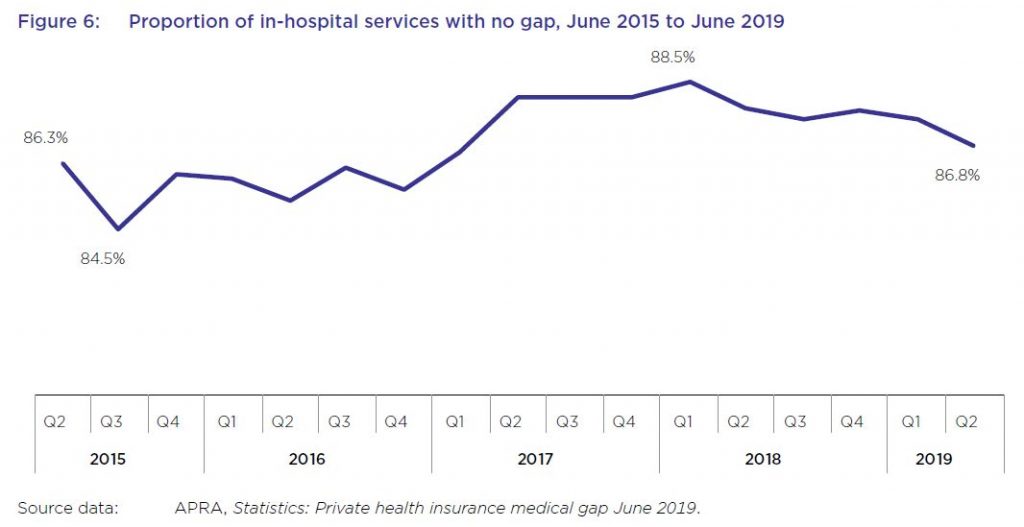

While most in-hospital services are delivered with no gap payments required from patients, this rate has varied in recent years, from a low of less than 85 per cent of services not requiring a gap payment in September 2015, to almost 89 per cent in March 2018, before falling again to under 87 per cent in June 2019.

From June 2018 to June 2019, the average gap expense incurred by a consumer for hospital treatment was $314.51, an increase of 1.9 per cent from the previous year, as shown in table 8. Average gap payments for extras treatment increased by almost 4 per cent to $49.20 over the same period.

A YouGov survey from late 2019 found that, after the cost of premiums and a perceived lack of value for money, out-of-pocket costs were a leading reason given by respondents for no longer holding private health insurance.

Several health insurers offer rewards schemes for their members, some of which involve the use of fitness tracking apps and devices to record activities such as steps and sleep. Some of these apps operate in conjunction with companies other than health insurers. For example, the health insurers MO Health and GMHBA are both partnered with the life insurer AIA Australia Limited, and use the AIA Vitality program issued by AIA.

HCF has also entered into a partnership with Flybuys where new HCF members can collect Flybuys points based on their annual health cover premiums. Qantas, which offers health insurance issued by NIB, also offers frequent flyer points for members who download the Qantas Wellbeing app and undertake certain activities. Its Qantas Wellbeing Program Terms and Conditions state that members must link a tracking device to record their physical activity, and that as members, they consent to Qantas: “collecting, using and disclosing any personal information including health and Wellbeing information submitted by the Member through joining or use of the Wellbeing Program or collected by Qantas through the Tracking Device or the Qantas Wellbeing App”.

Although Australians can receive benefits from rewards and discounts offered by health insurers and other organisations that collect consumer data, the ACCC is concerned that few consumers are fully informed of, fully understand, or can effectively control, the scope of data collected when they sign up for, or use, such services.

While the community rating system for private health insurance in Australia prohibits insurers from charging different private health insurance premiums to individual consumers based on health and other factors, the ACCC notes that the consumer data collected by wellbeing apps and rewards schemes could be used for a number of other purposes, including for targeted marketing (including from third parties), and potentially to create insights that could be shared with or sold to third parties.

The system will continue to be under pressure – and we think the model is frankly broken.

AFG and Connective are mortgage aggregators that act as intermediaries between lenders and their affiliated brokers.

“Combining AFG and Connective would create

the largest mortgage aggregator in Australia by a significant margin,

accounting for almost 40 per cent of all mortgage brokers operating in

Australia,” ACCC Chair Rod Sims said.

More than half of all home loans written

each year are initiated through the broker channel, and brokers play an

important role for consumers when seeking a home loan and for lenders in

reaching those consumers.

“AFG and Connective operate in an already

concentrated market, and not many other mortgage aggregators offer a

similar level or type of service. Additionally, potential entrants or

small players may be deterred from expanding by various barriers,

including compliance costs,” Mr Sims said.

“The ACCC is concerned there will be

limited similar alternatives for brokers to switch to. This may

negatively impact the services offered to brokers.”

The ACCC has published a statement of

issues and is seeking further information about the supply of mortgage

aggregation and distribution services, and the supply of home loans in

Australia. The ACCC invites further submissions from interested parties

in by 5 March 2020. The final decision will be announced on 7 May 2020.

AFG and Connective provide brokers with

access to a panel of lenders, and provide panel lenders access to

affiliated brokers to distribute loans. Generally, a broker will be

affiliated with one mortgage aggregator at a time, while lenders tend to

sit on a number of mortgage aggregator panels.

AFG and Connective also offer brokers

various support services to assist them to run their businesses. This

includes customer relationship management software that provides brokers

with the ability to compare products from the lender panel and assist

in the lodgement of loan applications.

AFG and Connective also offer white-label

or own-branded loan products under their respective brands. These

products are mostly funded by third party lenders, however, AFG also

offer loan products funded by its securitisation program.

I have warned before of the hidden algorithms which means that some comparison site results may not be providing what you expect. Not impartial, objective and transparent price comparisons. Hence the release from the ACCC should be of no surprise! Trivago misled consumers about hotel room rates.

The Federal Court has found Trivago breached the Australian Consumer Law when it made misleading representations about hotel room rates both on its website and television advertising.

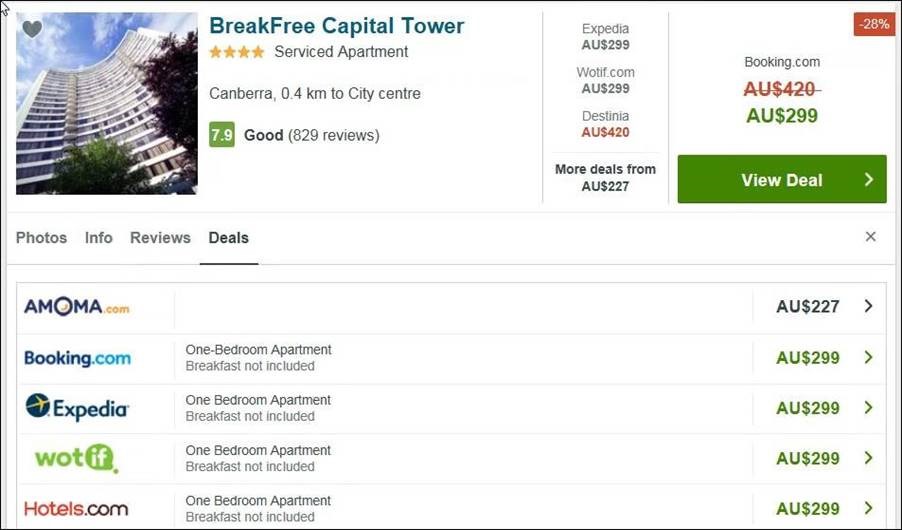

An example of Trivago’s online price display taken on 1 April, 2018. For example, the $299 deal is highlighted below, when a cheaper deal was available if a consumer clicked “More deals” (underneath the offers from other booking sites in the middle panel).

The Court ruled that from at least December 2016, Trivago misled consumers by representing its website would quickly and easily help users identify the cheapest rates available for a given hotel.

In fact, Trivago used an algorithm which placed significant weight on which online hotel booking site paid Trivago the highest cost-per-click fee in determining its website rankings and often did not highlight the cheapest rates for consumers.

“Trivago’s hotel room rate rankings were based primarily on which online hotel booking sites were willing to pay Trivago the most,” ACCC Chair Rod Sims said.

“By prominently displaying a hotel offer in ‘top position’ on its website, Trivago represented that the offer was either the cheapest available offer or had some other extra feature that made it the best offer when this was often not the case,” Mr Sims said.

The Court also found Trivago’s hotel room rate comparisons that used strike-through prices or text in different colours gave consumers a false impression of savings because they often compared an offer for a standard room with an offer for a luxury room at the same hotel.

“We brought this case because we consider that Trivago’s conduct was particularly egregious. Many consumers may have been tricked by these price displays into thinking they were getting great discounts. In fact, Trivago wasn’t comparing apples with apples when it came to room type for these room rate comparisons,” Mr Sims said.

The Court also found that, until at least 2 July 2018, Trivago misled consumers to believe that the Trivago website provided an impartial, objective and transparent price comparison for hotel room rates.

“This decision sends a strong message to comparison websites and search engines that if ranking or ordering of results is based or influenced by advertising, they should be upfront and clear with consumers about this so that consumers are not misled,” Mr Sims said.

A hearing on relief, including penalties, will be held at a later date.

Background

Trivago’s website aggregates deals offered by online hotel booking sites (like Expedia, Hotels.com and Booking.com) and hotel proprietors’ own websites for available rooms at a hotel and highlights one offer out of all online hotel booking sites (referred to as the ‘Top Position Offer’). However, Trivago’s own data showed that higher-priced room rates were selected as the Top Position Offer over alternative lower-priced offers in 66.8% of listings.

Trivago’s revenue was primarily obtained from cost-per-click (CPC) payments from online hotel booking sites, which significantly affected that booking site’s appearance and prominence in search results.

The ACCC has sought orders for penalties, declarations, injunctions and costs.

The ACCC has announced an update on the timeline for the implementation and launch of the Consumer Data Right (CDR) in the banking sector, deferring the launch of certain aspects from February to July 2020.

Consumers will be able to direct major

banks to share their credit and debit card, deposit account and

transaction account data with accredited service providers from 1 July

2020. Consumers’ mortgage and personal loan data will be able to be

shared after 1 November 2020.

The ACCC has formed the view that this

updated timeline for these aspects of the CDR reforms will allow

additional implementation work and testing to be completed and better

ensure necessary security and privacy protections operate effectively.

“The CDR is a complex but fundamental

competition and consumer reform and we are committed to delivering it

only after we are confident the system is resilient, user friendly and

properly tested,” ACCC Commissioner Sarah Court said.

“Robust privacy protection and information

security are core features of the CDR and establishing appropriate

regulatory settings and IT infrastructure cannot be rushed.”

The ACCC will make the CDR Rules in

January 2020 that reflect this adjustment to the timetable, and will

conduct further consultation regarding any consequential changes to

other phases of the CDR.

Background:

The Consumer Data Right will give

consumers the right to safely access data about them, held by

businesses, and direct this information be transferred to trusted third

parties of their choice.

Banking will be the first sector to which

the CDR applies. The CDR will subsequently be rolled out

sector-by-sector, with banking being followed by energy and

telecommunications.

Data portability increases competition,

particularly for more complex products and services, and allows

businesses to make more tailored offerings to consumers.

The ACCC has been working closely for

several months with the big 4 banks and the 9 entities selected to be

the initial data recipients to test and refine the CDR ecosystem.

The ACCC has authorised changes to the Australian Banking Association’s (ABA) Banking Code of Practice, after imposing several conditions aimed at improving the code’s benefits to low-income customers.

The ABA, on behalf of its 23 members, sought ACCC authorisation for

changes to update its Banking Code in response to recommendations of the

Royal Commission into Misconduct in the Banking, Superannuation and

Financial Services Industry (Hayne Royal Commission).

“The new Banking Code, with the ACCC’s conditions, will help ensure

that the harms to low income consumers so vividly identified by the

Hayne Royal Commission are addressed,” ACCC Deputy Chair Delia Rickard

said.

As authorised by the ACCC, the updated Banking Code now prohibits

informal overdrafts on low or no fee basic accounts held by eligible

customers, unless agreed to by the customer, and it prohibits overdrawn

fees and dishonour fees.

It also sets out the features of a basic bank account product,

including that it will have no minimum deposits; and will provide free

direct debit facilities, access to a debit card at no extra cost and

free unlimited domestic transactions for eligible customers.

In addition, the updated Banking Code will prevent default interest

and fees being charged on agricultural loans in areas affected by

drought and other natural disasters.

“The new Banking Code will address a significant source of harm to farmers experiencing drought,” Ms Rickard said.

“Our new conditions aim to address concerns that the ABA’s original

proposed Banking Code needed to be stronger,” Ms Rickard said.

“We had concerns that the original proposed code did not fully

reflect the spirit of the Hayne Royal Commission’s recommendations about

basic accounts. For example, low income customers could have been

charged interest rates of up to 20 per cent on overdrawn amounts despite

not having agreed to take on an overdraft facility.”

Under the conditions, ABA member banks must either not charge

interest, or refund any interest charged, on informal overdrafts on

basic accounts held by eligible low income customers if the customer has

not agreed to an overdraft facility. Banks must also proactively

identify customers who may be eligible for basic accounts.

The ABA must report to the ACCC on several matters; including any

changes to the number of banks offering basic bank accounts, how often

informal overdrafts are occurring without the customer’s agreement, and

the steps that banks have taken to contact existing customers who might

be eligible for a basic account. These reports will be made publicly

available.

“The ACCC wants to see improved outcomes for low-income customers and

farmers, and we also want the new Banking Code to deliver public

benefits and address the Hayne Royal Commission’s recommendations,” Ms

Rickard said.

Takeovers

of smaller rivals by digital platforms, including their data sets, may

pose a threat to consumers’ choice and privacy, said ACCC Chair Rod

Sims.

“Few consumers are fully informed of, nor can they effectively control, how their data is going to be used and shared. There are further concerns when the service they sign up to is taken over by another business,” said Mr Sims.

Mr Sims raised these issues in relation to Google’s recently announced proposed acquisition of Fitbit.

“The change in data collection policies, when a company like Fitbit

transfers its data to Google, creates a very uncertain world for

consumers who shared very personal information about their health to

Fitbit under a certain set of privacy terms,” said Mr Sims.

At the time of Google’s acquisition of DoubleClick, DoubleClick

reportedly denied that the data it collects through its system for

serving ads would be combined with Google’s search data. Eight years

later, Google updated its privacy policy and removed a commitment not to

combine Doubleclick data with personally identifiable data held by

Google.

When Facebook acquired WhatsApp, Facebook claimed it was unable to

establish reliable matching between Facebook users and WhatsApp users’

accounts. Two years later, WhatsApp updated its terms of service and

privacy policy, indicating it could link WhatsApp users’ phone numbers

with Facebook users’ identities.

“Given the history of digital platforms making statements as to what

they intend to do with data and what they actually do down the track, it

is a stretch to believe any commitment Google makes in relation Fitbit

users’ data will still be in place five years from now.”

“Clearly, personal health data is an increasingly valuable commodity

so it is important when consumers sign up to a particular health

platform their original privacy choices are respected and their personal

data is protected even if that company is sold.”

Research from the ACCC inquiry showed around 80 per cent of users

considered digital platforms tracking their online behaviour to create

profiles, and also the sharing their personal information with an

unknown third party, is a misuse of their information.

Facebook’s recent announcement of its planned offering of a

cryptocurrency Libra is also a potential cause for concern, said Mr

Sims.

“Here we have an organisation, whose lifeblood is to monetise data, getting into the financial services industry,” said Mr Sims.

“A lack of clear information about how their data will be handled

reduces consumers’ ability to make informed choices based on that data.”

“During our DPI we found a lack of consumer protection and effective

deterrence of poor data practises have undermined consumer’s ability to

choose products.”

“Vague, long and complex data policies contribute to this substantial

disconnect between how consumers think their data should be treated and

how it is actually treated,” said Mr Sims.

“Transparency and inadequate disclosure issues involving digital

platforms and consumer data were a major focus of our Inquiry, and

remain one of the ACCC’s top priorities.”

Yesterday, the government announced the ACCC will be conducting an inquiry into home loan pricing, investigating how lenders set their rates, why they often fail to pass through RBA rate cuts to borrowers in full, and the barriers that may be preventing consumers from switching to cheaper options on the market. Via AustralianBroker.

Over the course of the day, key industry players publicly responded

to the news, some welcoming the development, while the major banks

seemed to imply the key concerns listed were a matter of

miscommunication rather than misbehaviour.

FBAA

The Finance Brokers Association of Australia (FBAA) welcomed the announcement of an inquiry, with managing director Peter White dubbing the examination of the banking sector “appropriate.”

“I’ve been calling on the banks for a long time to pass on interest rate cuts in full,” White said.

“The banks have been playing some sort of seesaw game where they will

pass on a little bit this time and then a bit more – or a bit less –

the next time.

“There’s a pattern of behaviour here that Australians are clearly not happy with.”

White rejected the banks’ claims the partial rate pass throughs have been due to increasing costs.

“The banks are being hit with penalties for breaches uncovered through the royal commission, and through investigations by the Banking Executive Accountability Regime (BEAR).

“Trying to balance the books by passing on these penalties is not something that should be borne by borrowers.

“This inquiry provides an opportunity for banks to be transparent

around their decision making and how they balance the needs of the

community.”

COBA

The Customer Owned Banking Association (COBA) also welcomed news of

the inquiry, particularly singling out the investigation into what

prevents more consumers from switching banks when they may find a better

deal elsewhere.

Further, the association expressed optimism the inquiry with generate “creative new ways to unleash consumer power.”

“Empowering consumers to switch their banking and to shop around is

an unambiguously good thing,” said COBA director of strategy Sally

Mackenzie.

“A more competitive market will make all players care more about

their customers, and the market will function more effectively if there

is more intense competition for borrowers.

According to Mackenzie, it’s up to the policymakers to enable consumers to drive this market-wide competition.

ANZ

In its response, ANZ asserted the issues raised in the ACCC inquiry

launch stem from a shared misperception held among consumers.

“Despite intense competition, there is cynicism in the broader

community about interest rates for home loans,” said ANZ CEO Shayne

Elliott.

“We know we have not done a good job in explaining our position and

we will be working hard to ensure this process delivers results.

“The inquiry is a good opportunity to provide facts in what is a

complex space and we hope it will provide the public with renewed

confidence in the way their home loans are priced.”

Westpac

Westpac took a similar stance to ANZ, but went yet further, directly

defending its prioritisation of protecting its margins and making a

reasonable profit.

“The inquiry is an important opportunity to put the facts on the

table around mortgage pricing,” said Westpac Group CEO Brian Hartzer.

“Pricing decisions require banks to take into account a number of

factors, particularly as the cash rate heads towards zero. In particular

we have to manage the net interest margin – that is the difference

between deposit and lending rates. As part of this process we take into

account the interest of borrowers, depositors and shareholders who

provide the equity that enables us to operate.

“Banks also need to make a reasonable level of return. This not only

supports shareholder investment it also underpins prudential stability,

and our debt rating. The level of profit also needs to be considered in

relation to the size of our balance sheet which is $850bn. In fact our

profitability in terms of ROE has more than halved over the last 15

years.

“Westpac must also retain its double AA rating. This rating allows

the bank to import funding at more reasonable cost from international

investors. To lose it would increase the cost of our wholesale funding

which would inevitably lead to higher interest rates for our borrowers.”

NAB

NAB acknowledged the launch, but did so in a noncommittal manner.

Chief customer officer for consumer banking, Mike Baird said, “This

is an important opportunity to discuss the challenges of an increasingly

low interest rate environment and engage in a broader discussion about

how we support all our customers – both depositors and borrowers.”

The commentary did not extend further, aside from a list of “fast

facts” tagged onto the end, including that NAB currently has the lowest

Standard Variable Rate of the majors, has gotten rid of over 100 fees

from its products and services, and offers a special fixed rate of 2.88%

for two years for first home owners – seeming to imply the bank has

already done a great deal in making itself more hospitable for

customers.

Blog")