From Business Insider Australia.

ANZ Bank analysts have increased their forecasts for property price growth in Australia.

“Given Melbourne’s recent resilience, we have nudged our 2017 price forecasts higher, and now expect nationwide prices will finish the year 5.8% higher,” write economists Daniel Gradwell and Joanne Masters.

However, they see further evidence that the housing market is cooling.

“Weaker auction results point toward slow price growth through the rest of 2017, while tighter borrowing conditions and higher interest rates for investors are also likely to weigh on price growth in 2018,” they say.

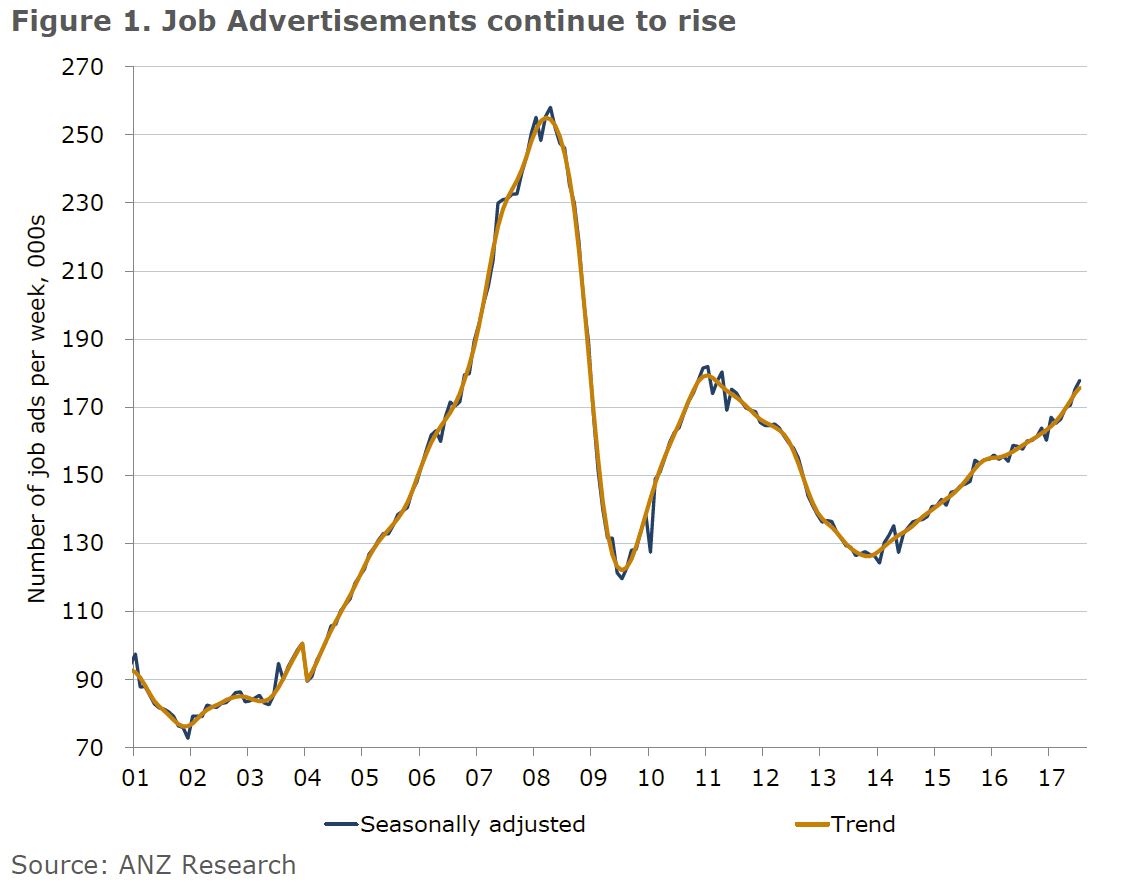

At the national level, dwelling price growth has slowed over the past three months.

Prices are now 9.7% higher than a year ago, down from the peak of 11.4% in May.

Here are the ANZ’s forecasts:

Source: ANZ Bank

Source: ANZ Bank“Much of this slowdown appears to be caused by a retreating investor presence in the market, in line with recent regulatory changes,” they say.

APRA’s further crackdown aimed at investor borrowing, particularly those with interest-only loans, has seen the investor share of total borrowing steadily decline.

“In turn, price growth has slowed across most capital cities and regional areas and across detached houses and the unit/apartment market,” say Gradwell and Masters.

“Having said that, the Melbourne market has recently been more resilient than the Sydney market, perhaps reflecting an element of catch-up after Sydney outperformed in previous years.”

The economists note there is no suggestion that prices will fall outright only that price growth will slow.

“Melbourne and Sydney will continue to be the main drivers of this growth, in line with their expanding populations,” they write.

“Strong additions to supply are expected to keep a lid on Brisbane’s prices, while Perth and Darwin are likely to have another year of weakness, as their mining boom adjustment winds up.”