The Australian Prudential Regulation Authority (APRA) has released for consultation a discussion paper on its proposals to revise the prudential framework for securitisation for authorised deposit-taking institutions (ADIs). APRA is also releasing a draft Prudential Standard APS 120 Securitisation (APS 120).

APRA’s objective in revising the prudential requirements for securitisation is to establish a simplified framework, taking into account global reform initiatives and the lessons learned from the global financial crisis. One of these lessons was that securitisation structures had become excessively complex and opaque, and that prudential regulation of securitisation had become similarly complex.

APRA first consulted on initiatives to simplify its prudential framework for securitisation in April 2014. Following consideration of the issues raised in submissions, APRA has amended its proposals in some areas. APRA’s amended proposals include:

- dispensing with a credit risk retention or ‘skin-in-the-game’ requirement;

- allowing for more flexibility in funding-only securitisation; and

- removing explicit references to warehouse arrangements in the prudential framework.

These amended proposals are expected to assist ADIs to further strengthen their funding profile and provide clarity for ADIs that undertake securitisation for capital benefits.

In December 2014, the Basel Committee on Banking Supervision (Basel Committee) released its updated securitisation framework (Basel III securitisation framework). The changes aim to enhance the Basel Committee’s existing securitisation framework and to strengthen regulatory capital standards.

APRA’s latest proposals incorporate the new Basel III securitisation framework, with appropriate adjustments to reflect the Australian context and APRA’s objectives, and will be applicable equally to all ADIs. Subject to consultation on this discussion paper and draft prudential standard, APRA proposes to implement these changes in line with the Basel Committee’s effective date of 1 January 2018.

In proposing revisions to its securitisation framework, APRA has sought to find an appropriate balance between the objectives of financial safety and efficiency, competition, contestability and competitive neutrality. APRA considers its proposals will deliver improved prudential outcomes and provide efficiency benefits to ADIs, particularly through the explicit recognition of funding-only securitisation within the prudential framework.

APRA invites written submissions on the proposals in this discussion paper by 1 March 2016. APRA also intends to release a draft prudential practice guide (PPG) and reporting standards and reporting forms, for consultation in the first half of 2016. APRA expects that the final prudential standard, PPG, reporting standards and reporting forms, will be released in the second half of 2016.

Background

Q: What is securitisation and is it important in Australia?

A: Securitisation is a form of funding where a ‘pool’ of assets, often residential housing loans, is separated from the originating ADI into a special purpose vehicle (‘SPV’). Cash flows from the pool of assets are used to make payments to investors in debt securities issued by the SPV. These payments are effectively secured by the pool of assets, hence the name “securitisation”.

The debt securities issued to investors will typically have a different order of priority claim over the assets in the pool. The senior class will have first claim, while more junior (or subordinated) class(es) will be utilised to absorb losses in the event of non-performance by some or all of the assets. The senior class of debt securities is therefore normally considered to be of lower risk than that of the underlying pool of assets, and this allows ADIs to source funding on attractive terms.

Sometimes an ADI will arrange for only the senior class to be sold to investors. Alternatively, where an ADI arranges to sell the junior class(es) to investors, they have transferred substantially all the credit risk of the pool to external investors. In these circumstances an ADI may also obtain regulatory capital benefits as APRA will, subject to meeting the specific requirements of APS 120, no longer require the ADI to hold capital against the credit risk of the pool.

Having a robust securitisation market therefore allows ADIs to strengthen their funding profile, and can offer capital management benefits as well. For smaller ADIs that may not have efficient access to unsecured wholesale debt markets, securitisation can be a valuable source of funding and, potentially, capital efficiency. As such, securitisation can support competition in the banking industry.

Q: How has APRA simplified the prudential framework?

A: APRA’s main proposals relating to the simplification of the prudential framework for securitisation are:

- the explicit recognition of funding-only securitisation. A simple structure facilitates a strong funding-only regime, where the originating ADI retains the junior securities and obtains funding from third parties through the sale of the senior securities. The explicit recognition of funding-only securitisation will assist ADIs to further strengthen their funding profiles;

- well defined thresholds for capital relief securitisation, which better articulate the requirements to be met for regulatory capital relief; and

- streamlining the approaches to determining regulatory capital requirements for ADIs’ securitisation exposures, and harmonising them for ADIs using standardised or internally-modelled risk weights.

Q: How will APRA’s proposals assist in facilitating a larger funding-only securitisation market?

A: The explicit recognition of funding-only securitisation, including the flexibility for bullet maturity structures that include a date-based call option, are likely to increase the potential size of the term securitisation market by attracting a broader investor base. These structures have not been permitted within the prudential framework previously.

Q: Why is APRA proposing not to include a ‘skin-in-the-game’ requirement in the prudential framework?

A: Skin-in the-game requirements are intended to address the misalignment of incentives whereby lenders may lack motivation to originate higher quality loans, since they may not have exposure to the loans once they are in a securitisation. A variety of skin-in-the-game requirements have emerged internationally and introducing an additional Australian requirement would run contrary to APRA’s objective of creating a simplified framework. In addition, Australian ADIs already have linkages to their securitisation — such as servicing of the underlying loans and entitlement to residual income — that reinforce incentives to maintain the quality of lending standards.

Q: How is APRA proposing to treat warehouse arrangements?

A: Warehouse arrangements allow ADIs to aggregate assets into pools before securities are issued to third parties. This can enable some ADIs to improve access to wholesale funding markets and raise funds at more competitive rates. The current regulatory requirements for warehouse arrangements have, however, created a gap in the prudential framework, such that less capital is held in the banking system relative to the risk retained in the system.

APRA is seeking submissions on viable approaches that maintain the benefits of warehouse arrangements but also address the gap in the prudential framework. In the absence of any such submissions APRA has indicated it will take a principles-based, rather than rules-based approach and will remove explicit reference to warehouse arrangements in APS 120. In these circumstances warehouse arrangements can still be entered into, but would need to meet the relevant requirements in APS 120 to be considered a securitisation.

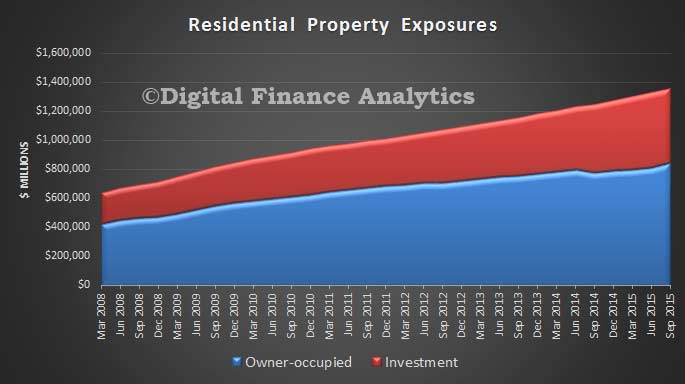

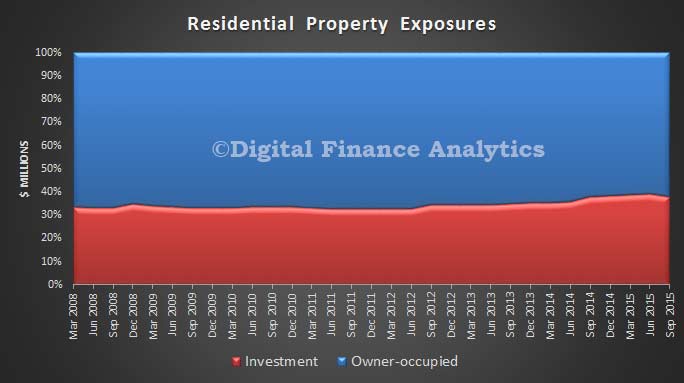

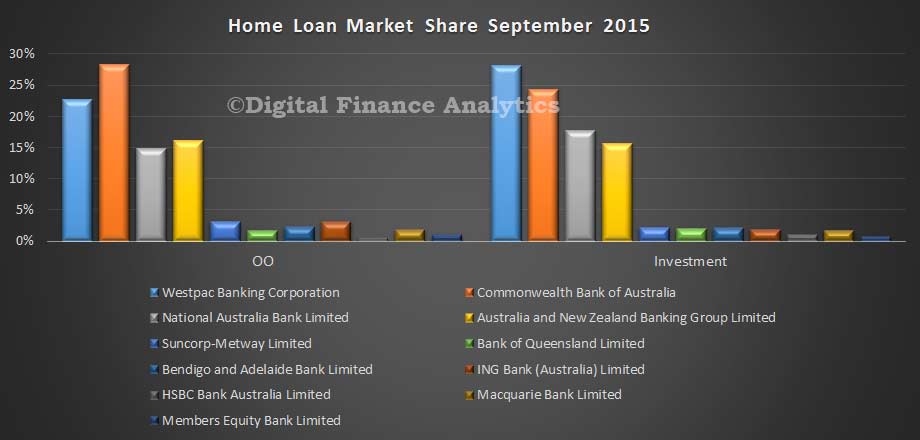

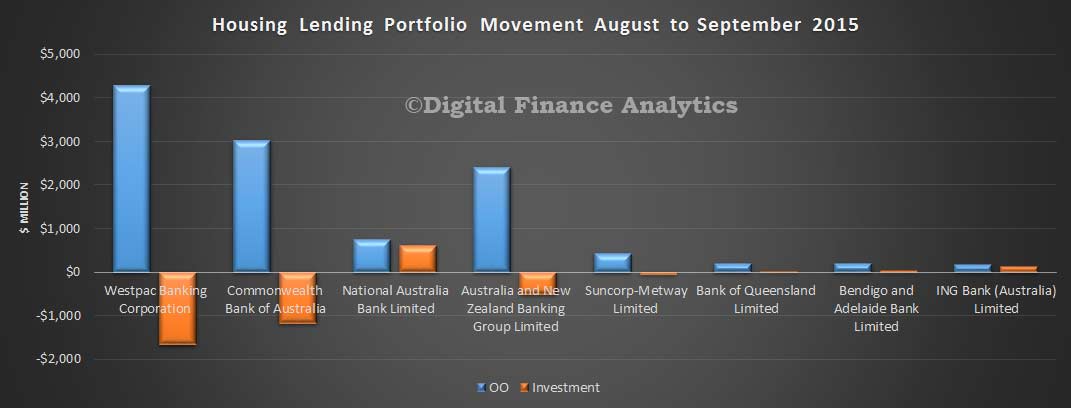

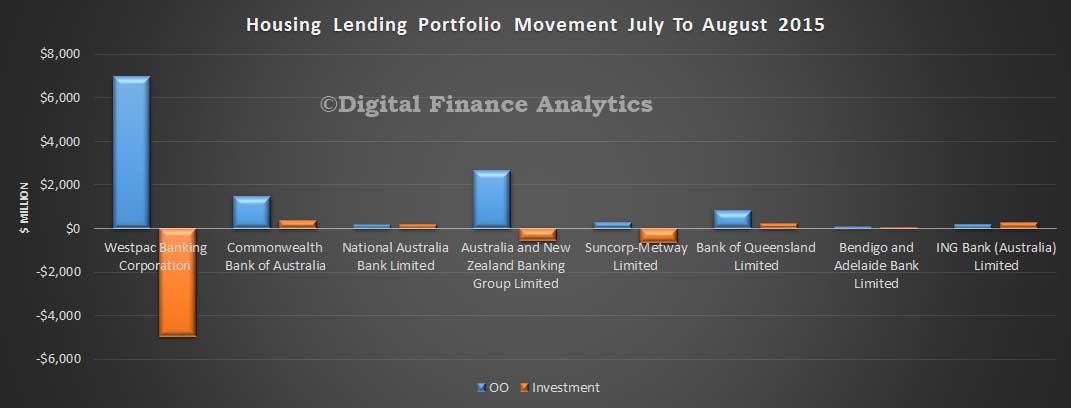

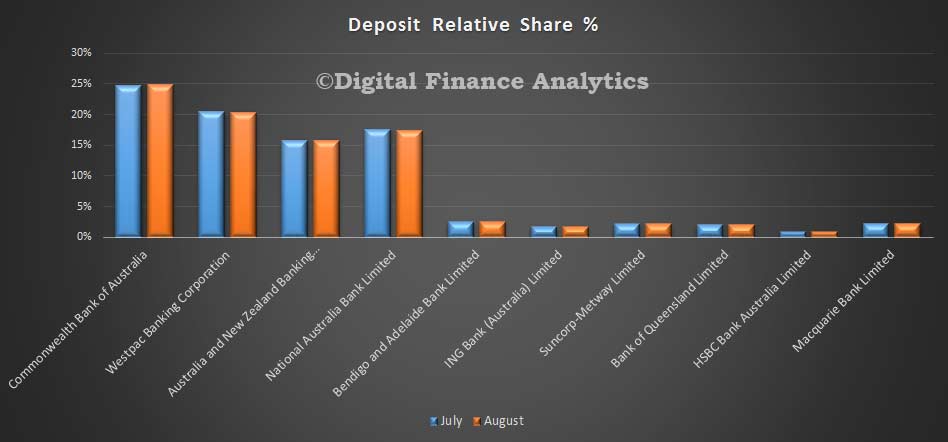

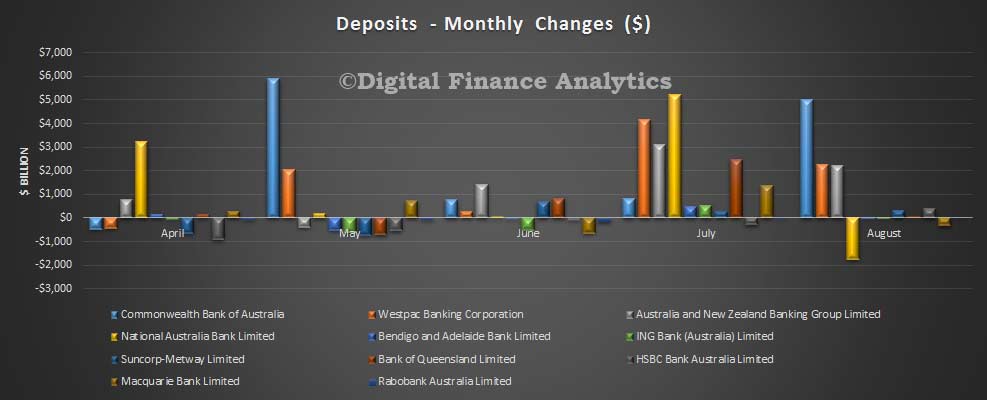

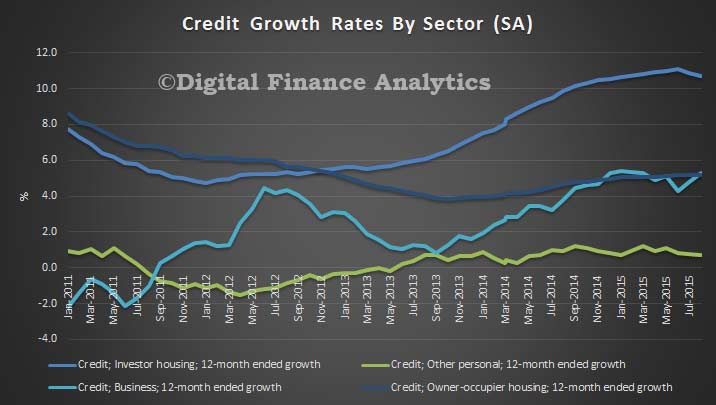

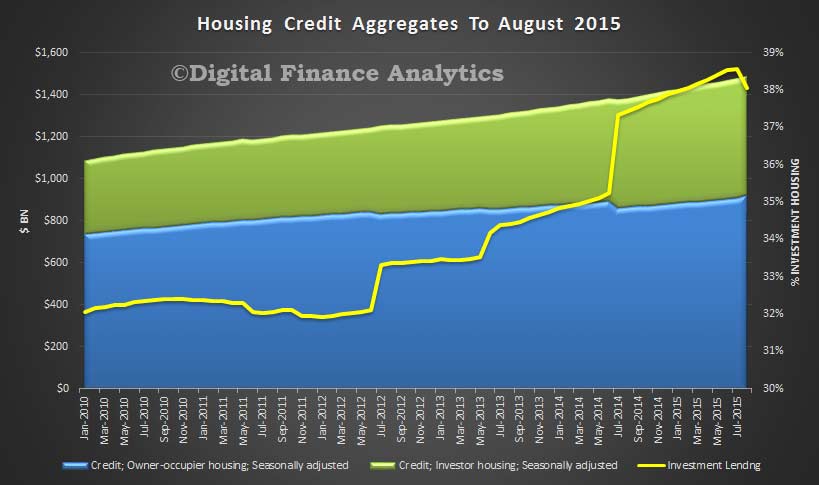

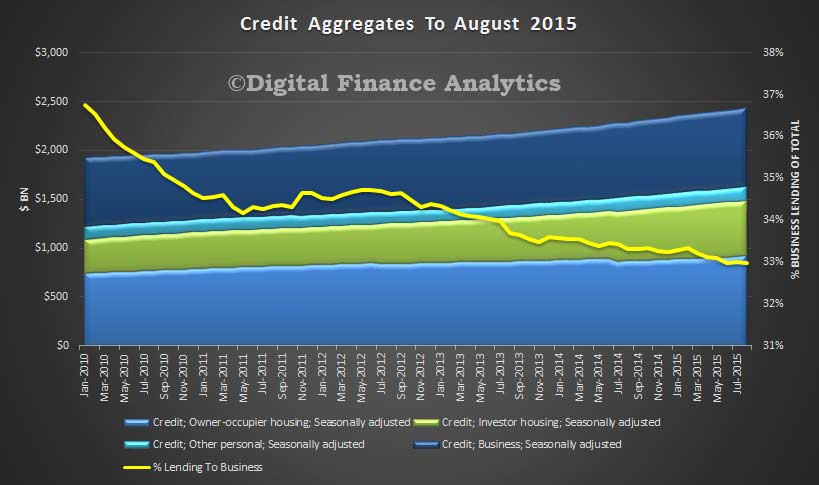

The monthly banking stats do not contain these adjustments, so cannot be directly reconciled. However, some interesting points are worth noting nevertheless. First is that total lending for housing rose by 7.5 bn to 1.4 trillion in the month. The RBA lending figure for the whole market (including the non-banks) was 1.5 trillion. This is another record. Investment lending sits at 37% on these numbers. Net movements for OO loans was up 2.73%, whilst investment loans fell 2.95%.

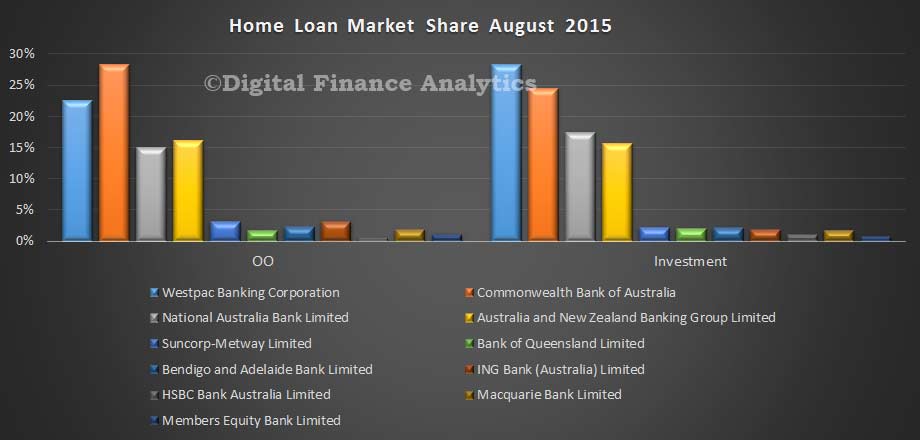

The monthly banking stats do not contain these adjustments, so cannot be directly reconciled. However, some interesting points are worth noting nevertheless. First is that total lending for housing rose by 7.5 bn to 1.4 trillion in the month. The RBA lending figure for the whole market (including the non-banks) was 1.5 trillion. This is another record. Investment lending sits at 37% on these numbers. Net movements for OO loans was up 2.73%, whilst investment loans fell 2.95%. So the current market shares are revised to:

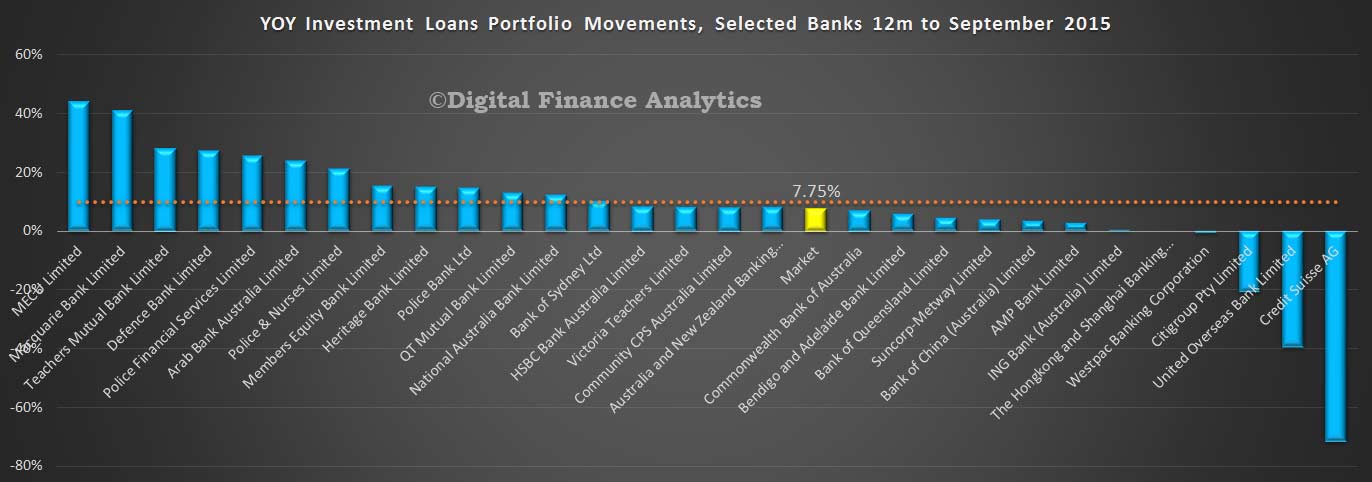

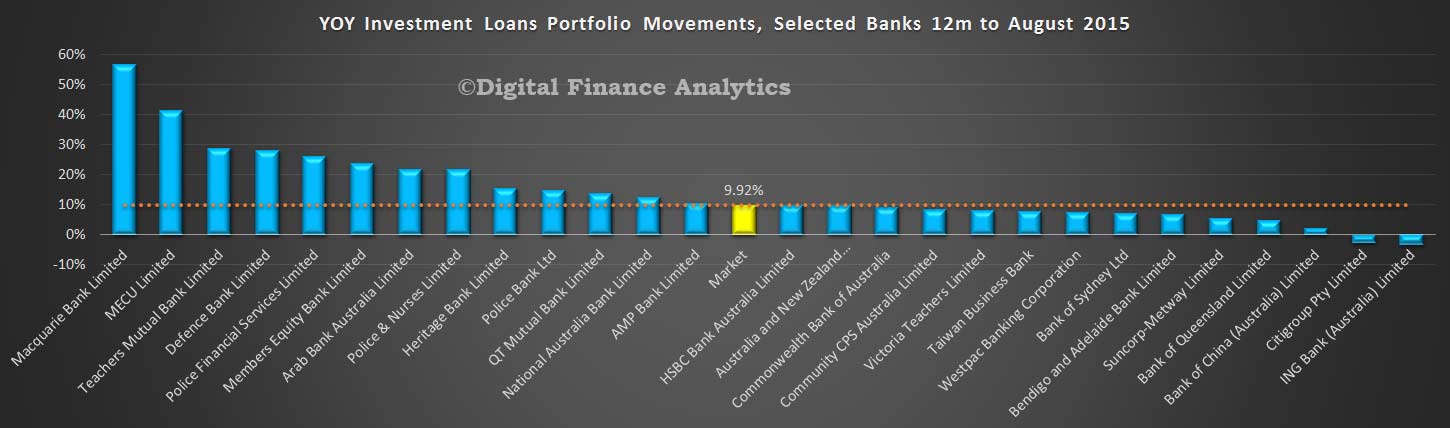

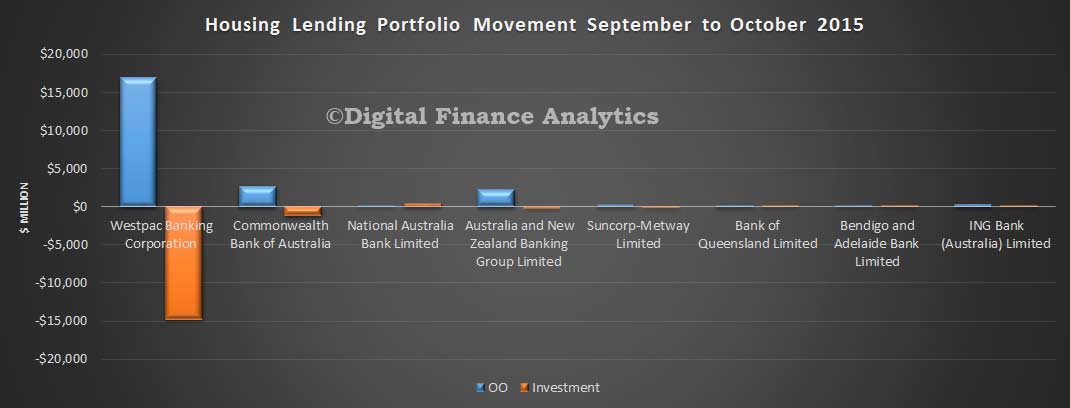

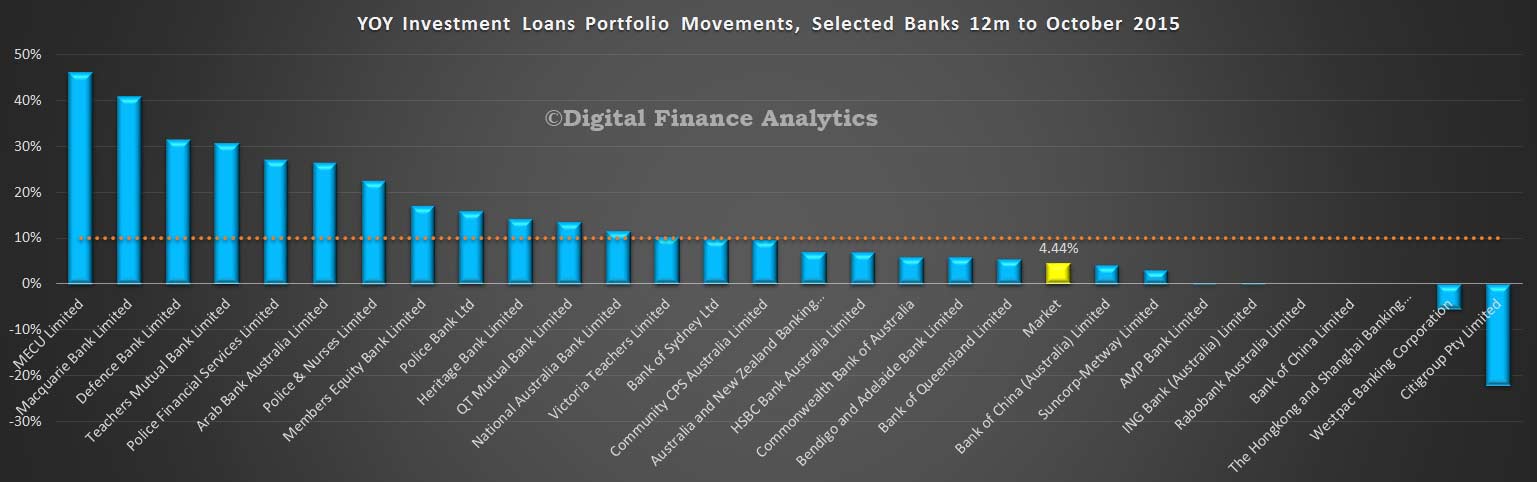

So the current market shares are revised to: In our modelling of the monthly movements, based on the APRA data, where we sum the monthly movements for the past year (and include adjustments where we can), it appears Westpac is now in negative territory for investment loans, and that the growth rates for the other majors is slowing. The imputed annual market movement is 4.4% against the RBA data above of just under 10%.

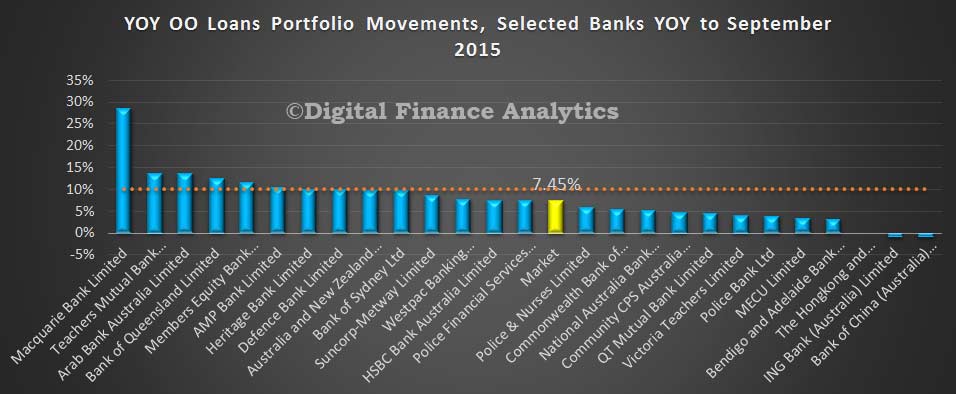

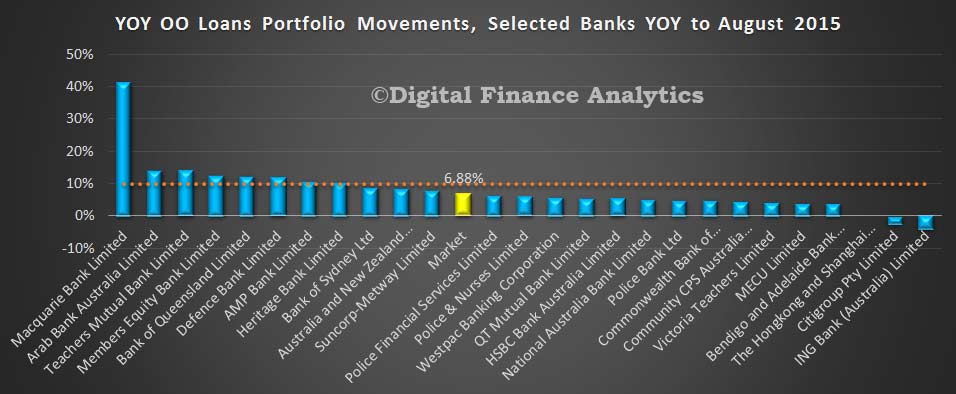

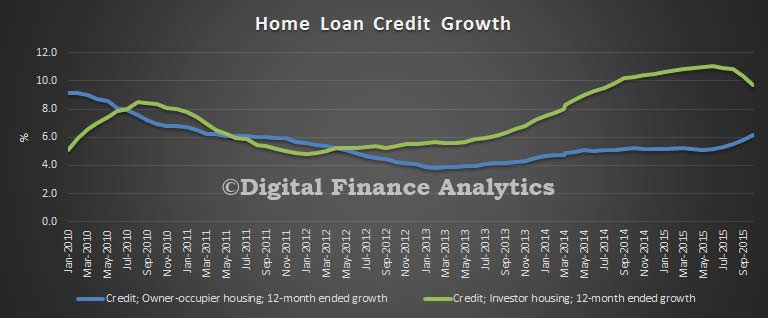

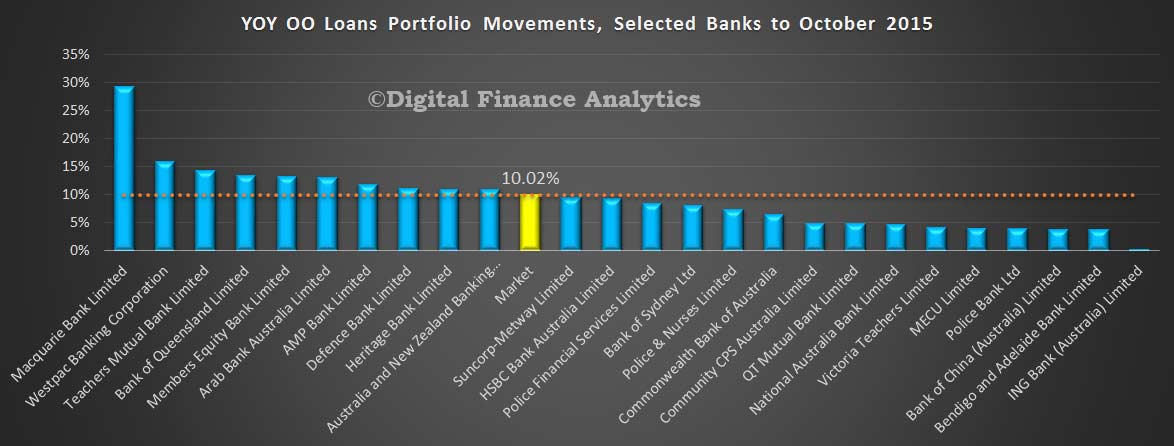

In our modelling of the monthly movements, based on the APRA data, where we sum the monthly movements for the past year (and include adjustments where we can), it appears Westpac is now in negative territory for investment loans, and that the growth rates for the other majors is slowing. The imputed annual market movement is 4.4% against the RBA data above of just under 10%. For completeness we also show the owner occupied movements. These too are impacted by reclassifications, and the imputed growth rate is 10%, compared with 6% from the RBA.

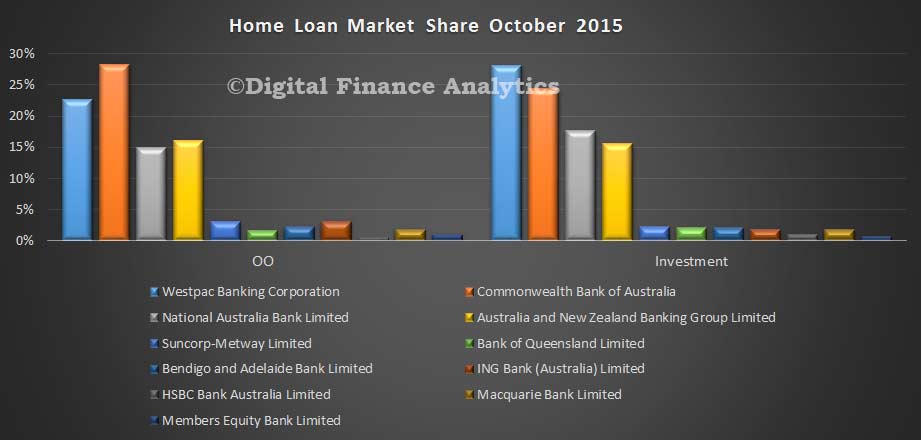

For completeness we also show the owner occupied movements. These too are impacted by reclassifications, and the imputed growth rate is 10%, compared with 6% from the RBA. The net effect of all this is that there is no true information about what individual banks are doing in their loan portfolios. Having tried to talk to a couple of them to clarify the story, I discover they are not willing to share additional data and refer back to the [flawed] APRA data.

The net effect of all this is that there is no true information about what individual banks are doing in their loan portfolios. Having tried to talk to a couple of them to clarify the story, I discover they are not willing to share additional data and refer back to the [flawed] APRA data.