Westpac will decrease its floor rate from 5.75% to 5.35%, effective 30 September.

The same change will go into effect at its subsidiaries: St. George, BankSA and Bank of Melbourne.

After the initial round of floor reductions across lenders of all sizes, Westpac matched CBA with the higher floor rate of the big four banks at 5.75%, while ANZ and NAB each amended theirs to 5.50%.

Smaller lenders followed suit, the majority also updating their rates to either the 5.50% or 5.75% figure.

While some went even lower, ME Bank amending its rate down to 5.25% and Macquarie to 5.30%, Westpac has taken a step away from the other majors with its newest update.

With July marking the strongest demand for new mortgages in five years and further RBA rate cuts expected in the near future, the floor reduction seems well timed to capitalise on the strong market activity forecasted to continue into the coming

This is a race to the bottom, and is bad news for financial stability. When will APRA wake up? It will also jack some home prices higher, in selected areas and types.

The Australian Prudential Regulation Authority (APRA) notes the judgment today in its court action against IOOF entities, directors and executives.

APRA initiated the action last December due to its view that IOOF entities, directors and executives had failed to act in the best interests of their superannuation members. Before taking the court action, APRA had sought to resolve concerns with IOOF over several years but considered that it was necessary to take stronger action – through use of directions, conditions and court action – after concluding the company was not making adequate progress, or likely to do so in an acceptable period of time.

The court has dismissed APRA’s application for a finding that IOOF entities, directors and executives had contravened their obligations under the Superannuation Industry Supervision Act 1993 (SIS Act). Accordingly, the case cannot proceed to a hearing on penalties, including disqualification.

APRA is examining the lengthy judgment in detail and will then make a decision on whether to pursue an appeal.

Although disappointed by the decision, APRA Deputy Chair Helen Rowell said: “This case examined a range of legal questions relating to superannuation law and regulation that had not previously been tested in court, relating to the management of conflicts of interest, the appropriate use of super funds’ general reserves and the need to put members’ interests above any competing priorities.

“Litigation outcomes are inherently unpredictable, however APRA remains prepared to launch court action – where appropriate – when entities breach the law or fail to act in an open and cooperative manner. APRA still believes this was an important case to pursue given the nature, seriousness and number of potential contraventions APRA had identified with IOOF,” Mrs Rowell said.

Additional licence conditions that APRA imposed on IOOF in December are unaffected by today’s judgment and remain in force.

Despite today’s decision, Mrs Rowell said APRA’s tougher approach to enforcement had led to IOOF being better placed to deliver sound, value-for-money outcomes for its members.

“APRA has seen significant improvement in the level of cooperation from IOOF since this case was launched. Additionally, the new licence conditions have enhanced IOOF’s organisational structure and governance, including the role and independence of the trustee board within the IOOF group. This will better support effective identification and management of future conflicts of interest,” she said.

The current low interest rate environment could impact the ability of smaller banks to compete against the major institutions, APRA chair Wayne Byres has cautioned, via InvestorDaily.

In an address to the European Australian Business Council in Melbourne, Mr Byres spoke on financial stability and the challenges ahead for the banking system.

The return on equity (RoE) of the Australian major banks has certainly declined but has not fallen below 10 per cent, even during the GFC, and is now in the order of 12 per cent; for large global European banks, RoE was negative at the height of the crisis, and has struggled to get much above 5 per cent since then.

Reflecting this, the price-to-book (PTB) ratio of the Australian majors averages around 1.5x, and capital is readily available; for large European banks, PTB has typically been in the order of 0.5x and new capital is therefore expensive.

In 2018, a decade after the crisis, the four Australian majors were ranked in the top 35 banks in the world by market capitalisation. Europe, despite a much larger banking system and population, only had four banks in the top 35.

All four Australian major banks enjoy AA credit ratings, and ready access to funding; very few European banks (without explicit government support) enjoy similar ratings.

He compared the experience of the Australian

market to Europe, noting local banks are having to get used to low

interest rates, as opposed to their weathered overseas counterparts.

In

Europe, where the continent’s GDP fell more than 5 per cent at the

height of the global financial crisis and didn’t make it back to 2008

levels for another five years as well as unemployment rising to 11 per

cent and only just recovering, he noted the environment has been tough.

“For

European banks, of course, it is nothing new – Europe has operated with

its interest rate on the ECB’s main refinancing operations at 1 per

cent or below since late 2011, and zero since early 2016,” Mr Byres

said.

“In

that regard, the European experience illustrates some of the challenges

potentially ahead for Australian banks. A very low interest rate

environment will see margins squeezed, adding to the headwinds from slow

lending growth.

“Profitability, and therefore capital generation,

will come under more pressure. And given their different funding

profiles, these trends may well impact smaller banks more forcefully

than larger ones, reducing the ability of the former to apply

competitive pressure to the latter. But to be clear, neither group will

welcome further rate reductions.”

He reflected on the market

around 2014-15, when APRA was concerned the banks were not responding

prudently to the environment of high house prices, high household debt,

low rates and subdued income growth.

“Speculative activity was increasingly prominent,” Mr Byres said.

“Such

an environment would, one might think, see prudent bankers trimming

their sails and battening down the hatches. Instead, intense competitive

pressures across the industry saw a tendency for standards go by the

wayside – for lenders, it was full steam ahead.”

APRA and ASIC worked to drive standards to more prudent levels, while ASIC focused on responsible lending.

“However,

it is worth remembering that the original risks we were concerned about

in 2014 – high prices, high debt, low interest rates and subdued income

growth – have not gone away, and in some cases increased,” Mr Byres

said.

“When it comes to the supply of credit, it would therefore

be unwise for lending standards to be allowed to erode again as a means

of generating lending growth. And on the demand side, it would be

unhelpful if recent (and prospective) interest rate reductions led to a

resurgence in speculative activity.”

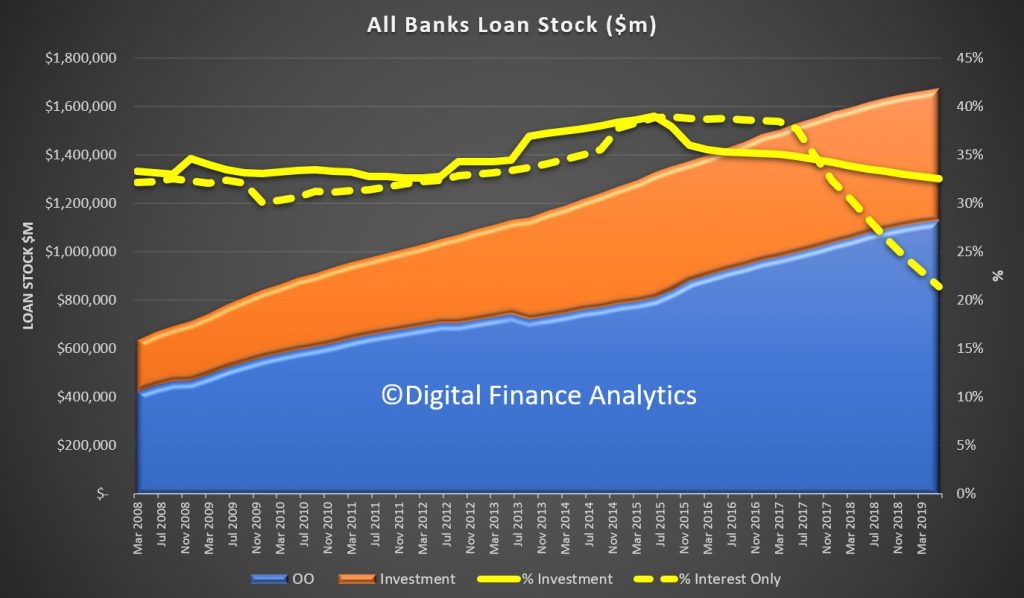

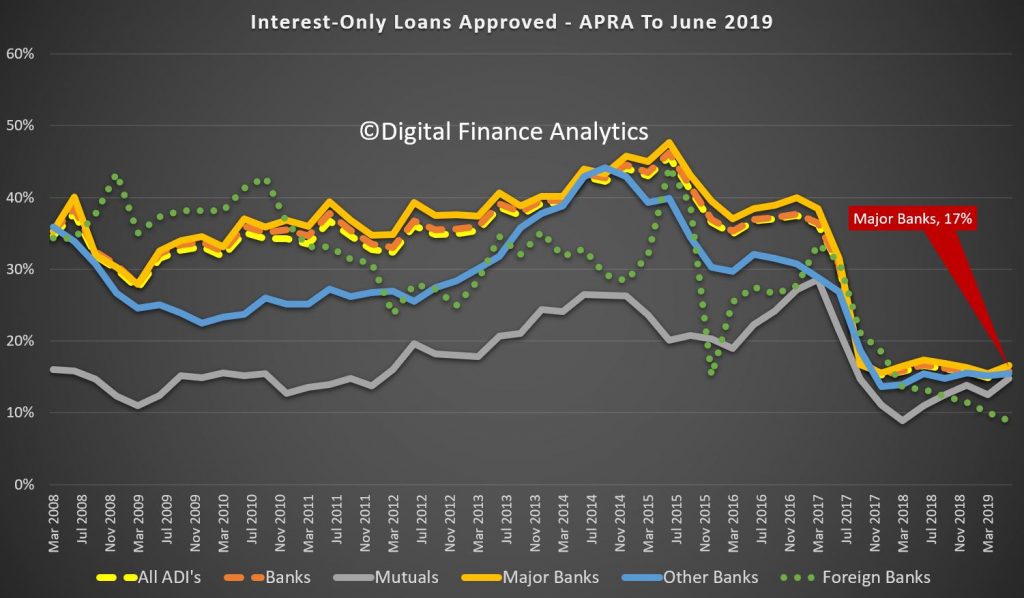

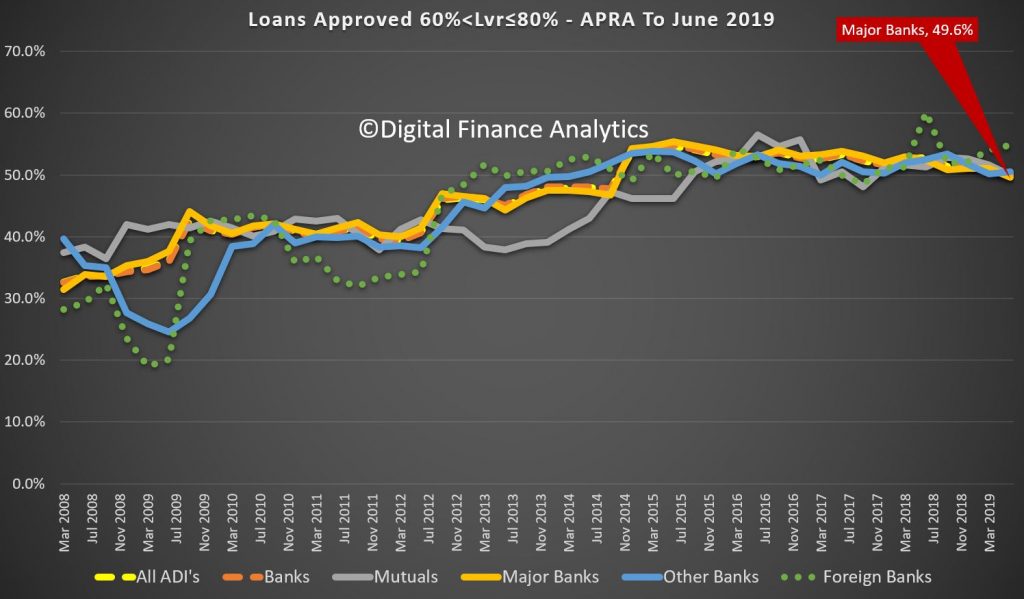

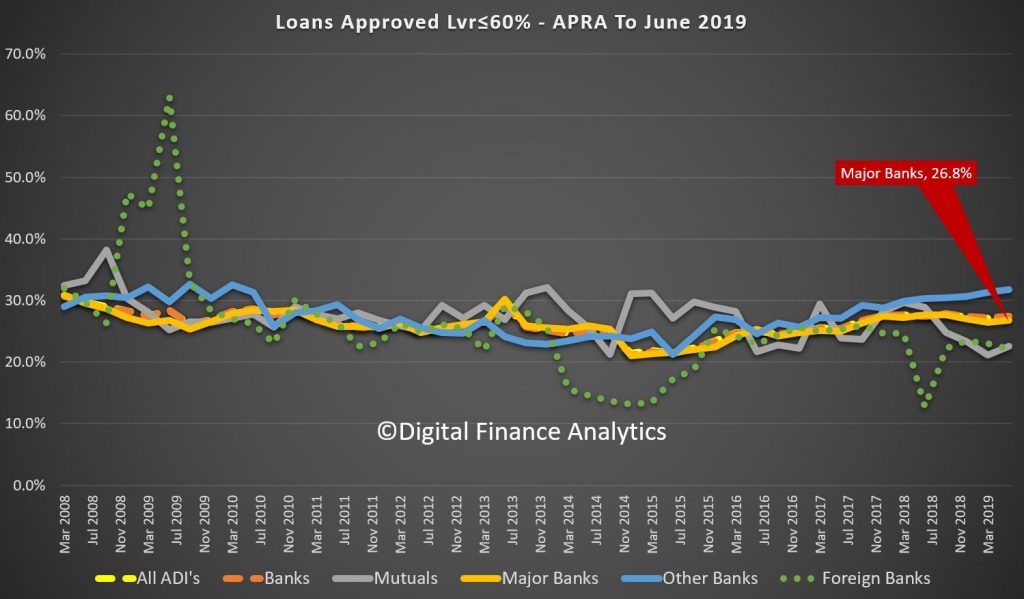

APRA released their quarterly property exposures data to Jun 2019 today. We can see some of the moving parts in the Industry, though only at an aggregated levels.

At the top level we can see the impact of APRA first imposing restrictions on investment lending in 2015, and later in 2017 on interest only loans. The subsequent loosening of standards which APRA introduced has yet to hit the statistics.

We can see that mortgage lending growth did slow thanks to their measures, with total ADI mortgages at $1.67 trillion, comprising $547 billion of investor loans and $359 billion of interest only loans. This translates to 32.6% of loans being for investment purposes (still too high) and 21.4% of all mortgages being interest only. Not disclosed is the distribution of interest only loans between owner occupied and investment loans, but we can assume most are investment related.

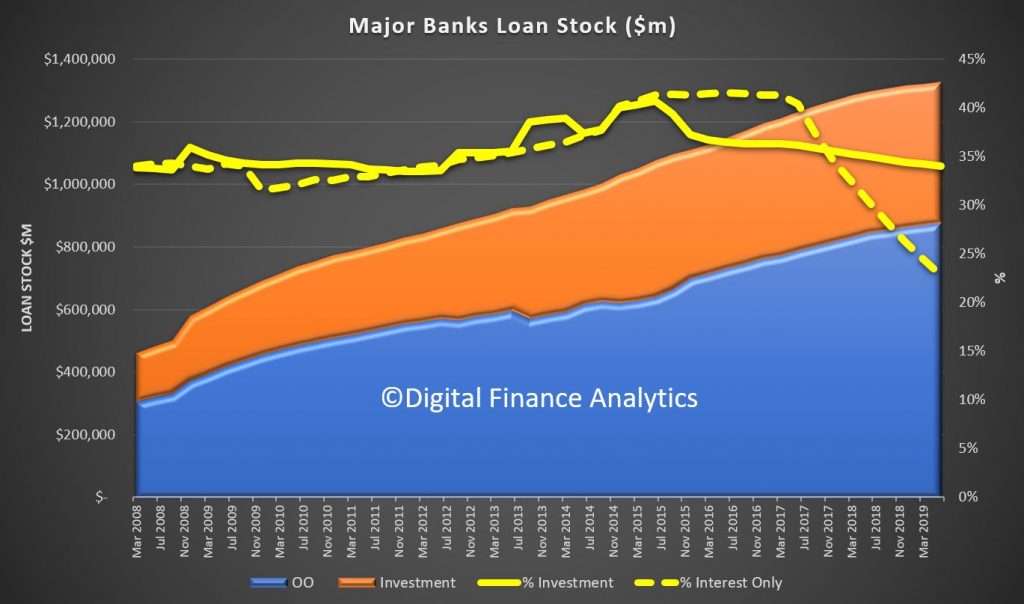

We can pull out the same data for the four major banks. Here total loans are $1.33 trillion, with $452 billion being investment loans and $303 billion being interest only, giving a 34% share of investment loans and 22.8% of interest only loans, so they still have a larger share of investment loans and IO loans relative to the market. No bank level data is disclosed, though we know Westpac has a larger share of investment loans, and we assume interest only loans too.

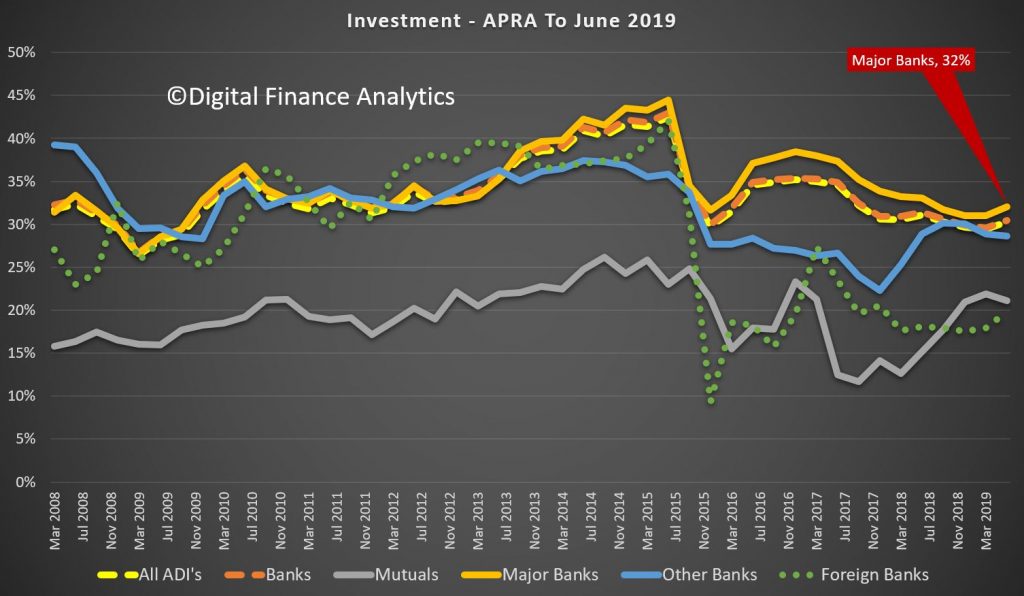

We can then look at the new lending flows across the various lender types. The flow of new investment loans is running at 32% to June, and is rising (we expect it will be even higher next time as the APRA loosening is executed). As a result mutuals are writing a lower share of investment loans now.

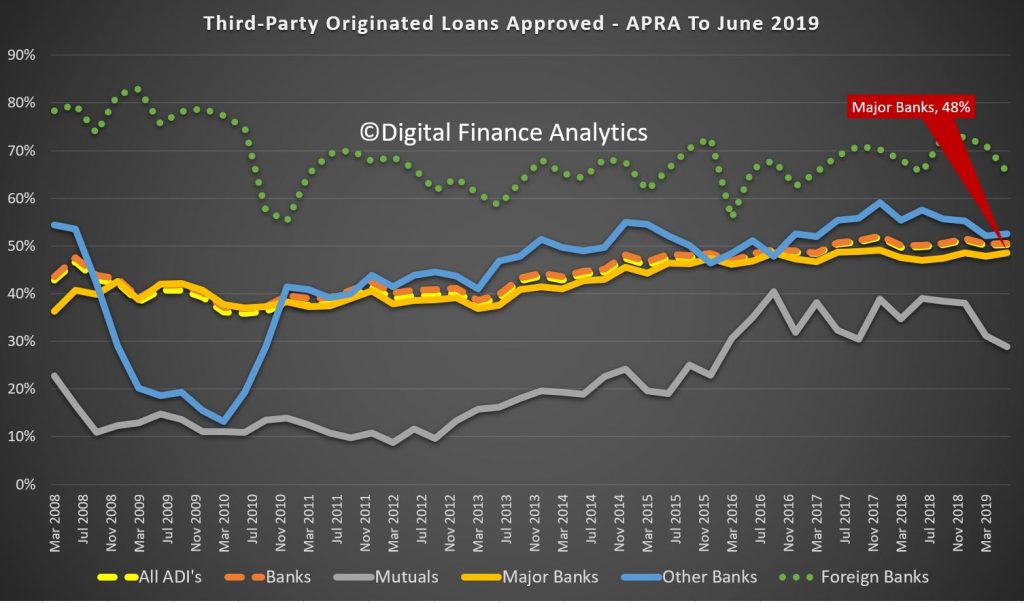

The proportion of new loans via Brokers varies by lender category, with foreign banks sitting around 65%, compared with the 48% of major banks. Mutuals are seeing a fall, as competition from majors increases.

The proportion of new interest only loans is at around 17% for most lender types, with foreign banks writing less. Mutuals are writing more IO loans now.

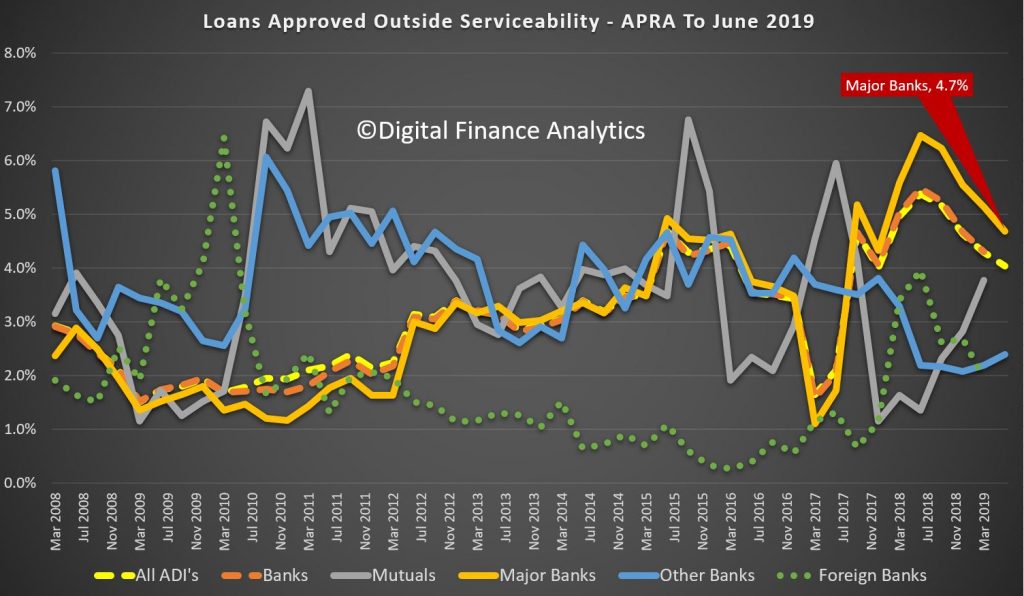

Loans written outside serviceability has fallen across the industry, though major banks are still at 4.7%, and above the other lender types. Mutuals are writing more, as they attempt to gain share in the increasingly competitive market. There are higher risks in these loans.

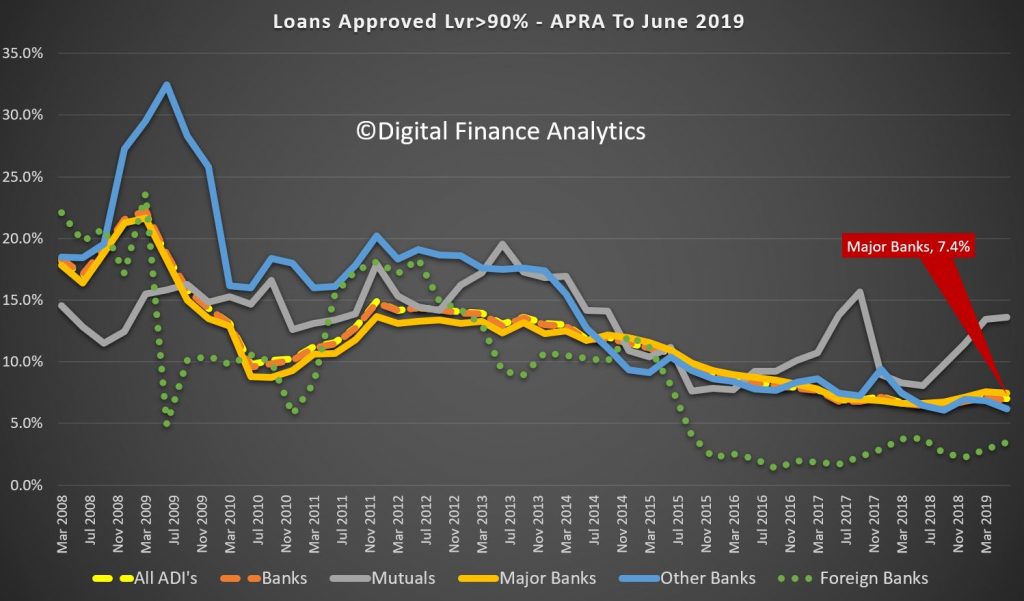

Finally, we can look across the loan to value bands, at time of origination.

Major banks are writing around 7.4% of loans above 90%, compared to mutuals at 13% – once again showing mutuals having to break their rules more often to win business.

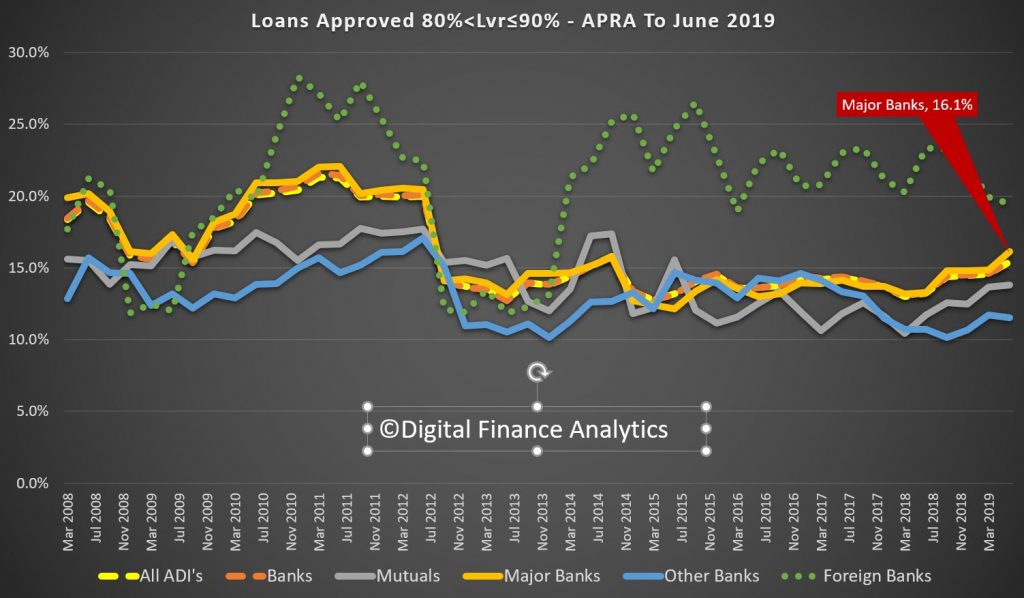

In the 80-90 bands, majors are at 16.1% and rising.

Nearly half of all loans written are around 50% of loan to value ratio – here the best deals are on offer, so refinancing is quite strong. There is little variation across the lender segments.

The lower LVR bands are around 26%, with other banks (including regionals) a little higher.

So this data suggests that mutuals are under pressure, the effect of the APRA tightening is obvious, the question now will be how this changes in the new “you set the risk” environment. It appears from our data lenders are more willing now, so we will be watching the serviceability and LVR metrics. But loan volumes remain constrained, which will limit potential excesses, at least for a time.

But, the Reserve Bank of Australia has pointed to Australia’s high debt levels as a factor in its decision making for the cash rate, fearing that it will make the economy more vulnerable to shocks.

Just remember this in the context of APRA reducing the lending standards recently! And in APRA’s Corporate plan Australia’s banking watchdog will stress test the country’s banks every year, instead of the current three-year cycle, ramping up oversight of a sector that has been marred by misconduct.

In the most recent series of stress tests in 2017, all 13 of the country’s largest banks passed the “severe but plausible” scenarios applied by the regulator, despite projected losses of about A$40 billion in home loans alone.

The RBA published its four-year corporate plan on Friday, pointing to the banks’ exposure to housing loans and cyber security in financial institutions as the largest risks to the country’s financial stability.

In Australia, wages growth is low, reflecting spare capacity in the labour market as well as some structural factors.

The

central bank expects the unemployment rate will remain around 5.25 per

cent for a time, before declining to around 5 per cent in 2021, with

wages growth expected to remain stable and then increase modestly from

2020.

Consumer price inflation is forecast to increase to be a

little under 2 per cent over 2020 and a little above 2 per cent over

2021.

The

RBA noted over the next four years, “movements in asset values and

leverage may be more important for economic developments than in the

past given the already high levels of debt on household balance sheets.

“Especially

in the context of weak growth in household income, high debt levels

could complicate future monetary policy decisions by making the economy

less resilient to shocks,” the RBA said.

The central bank noted

policymakers in the US and other countries employing quantitative easing

as a result of intensifying trade and technology disputes.

Globally,

the RBA reported, labour market conditions remain tight in major

advanced economies, although unemployment rates are at multidecade lows.

“Global

interest rates and measures of financial market volatility both remain

low compared with historical experience,” the RBA said in its corporate

plan.

“The future path of global monetary policy and financial

conditions more generally remain subject to substantial uncertainty.

These global factors significantly influence the environment in which

monetary policy in Australia is conducted,” the RBA said.

Last

week, RBA governor Philip Lowe reflected on the RBA’s decision on the

cash rate during an address to Jackson Hole Symposium in Wyoming.

“So

the question the Reserve Bank Board often asks itself in making its

interest rate decision is how our decision can best contribute to the

welfare of the Australian people,” Mr Lowe said.

“Keeping

inflation close to target is part of the answer, but it is not the full

answer. Given the uncertainties we face, it is appropriate that we have a

degree of flexibility, but when we use this flexibility we need to

explain why we are doing so and how our decisions are consistent with

our mandate.”

He said a challenge the central bank is facing is elevated expectations that monetary policy can deliver economic prosperity.

“The

reality is more complicated than this, not least because weak growth in

output and incomes is largely reflecting structural factors,” Mr Lowe

commented.

“Another element of the reality we face is that

monetary policy is just one of the levers that are potentially available

for managing the economy. And, arguably, given the challenges we face

at the moment, it is not the best lever.”

The RBA is due to deliver its cash rate decision tomorrow.

Blog")