The corporate regulator has told the Hayne royal commission that it is at a loss over how to successfully prevent misconduct in financial services, via InvestorDaily.

The Australian Securities and Investments Commission has expressed in its submission that work had to be done to stop misconduct in the industry but there was not enough evidence as to how.

“There is unfortunately currently a dearth of knowledge and research as to what effectively deters misconduct across the range of corporate sectors and, in particular, the financial sector itself,” it reads.

ASIC recognised that it had a duty to force significant cultural change in the industry and said it would begin onsite supervision in major financial institutions.

However, ASIC rejected the interim reports idea that it did not go to court or issue civil penalties.

The Hayne Interim Report made claims that ASIC rarely went to court, seldom brought civil penalty proceedings and allowed entity’s to pay infringement notices with no admission.

ASIC said it was willing to change its enforcement practices but said it regularly undertook litigation against the financial sector.

“ASIC has litigated matters (through civil and criminal proceedings) twice as much as it has accepted enforceable undertakings,” ASIC’s report read.

ASIC also rejected the emphasis the interim report placed on its track record in the past decade against the major banks.

The interim report noted how ASIC had only issued commenced 10 civil proceedings against the major banks but 45 infringement notices to the major banks and accepted 13 enforceable undertakings.

ASIC said that the figures expressed in the report do not support the proposition that ASIC presently avoids compulsory enforcement action, nor do they reflect the full variety of enforcement tools made available to ASIC.

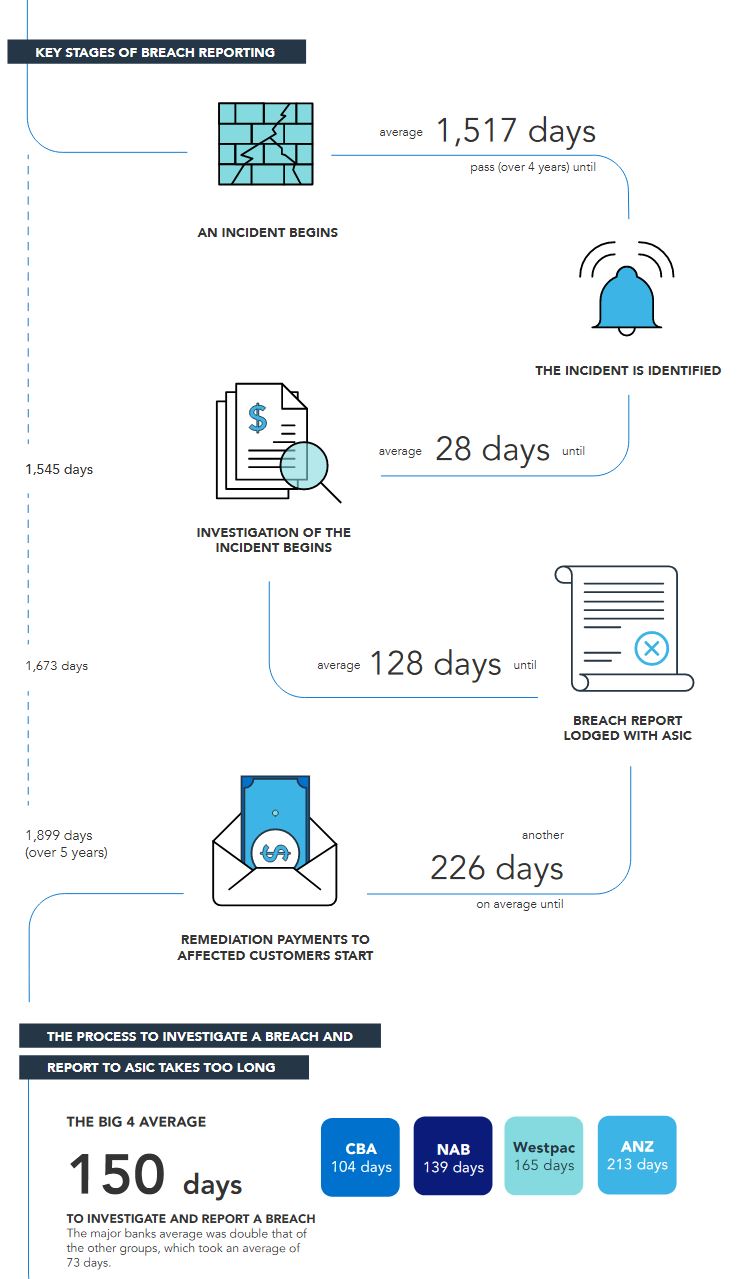

ASIC provided no comment on the interim reports findings that the commission had never brought proceedings against a licensee who failed to report a data breach.

“As at April 2018, ASIC had never brought, or sought to have the Commonwealth Director of Public Prosecutions (CDPP) bring, proceedings against a licensee for failing to comply with the 10 day time limit for breach reporting under Section 912D of the Corporations Act 2001 (Cth) (the Corporations Act), 21 despite affirming that it believed that entities frequently fail to comply with the section,” the report read.

The commission also provided no comment to the reports findings that it had never commenced proceedings against an entity for fees for no service.

“At 30 May 2018, ASIC had never commenced, or sought to have CDPP commence, proceedings under Section 12DI of the Australian Securities and Investments Commission Act 2001 (Cth) (the ASIC Act). This prohibits accepting payment for financial services when the payee does not intend to, or there are reasonable grounds to believe it cannot, supply the service,” it read.