Macquarie Securities (Australia) Limited (‘Macquarie’) has paid a penalty totalling $300,000 to comply with an infringement notice given by the Markets Disciplinary Panel (‘the MDP’).

The MDP had reasonable grounds to believe that Macquarie contravened

the market integrity rules that deal with the provision of regulatory

data to ASX and Chi-X.

Over a four-year period from July 2014 to July 2018, Macquarie

transmitted approximately 42 million orders to ASX and Chi-X that

included incorrect regulatory data or omitted required regulatory data.

Over the same period, Macquarie also submitted approximately

377,000 trade reports to ASX and Chi-X with the same deficiencies.

The kinds of regulatory data that was incorrect or missing was information about:

‘capacity’: a notation to identify whether Macquarie was acting as principal or agent;

‘origin’: a notation to identify the person on whose instructions Macquarie was acting; and

‘intermediary’: the AFSL number of an intermediary using Macquarie’s automated order processing system.

The MDP emphasised that the provision of accurate regulatory data

enhances market transparency and ensures an orderly market. The

provision of incorrect or missing regulatory data to market operators

impedes informed regulatory decision-making by market operators and by

ASIC.

The MDP found that while Macquarie intended to comply with the market integrity rules, there were weaknesses in the configuration and integration of Macquarie’s systems, its processes for on-boarding new clients and its control framework.

The MDP considers Macquarie’s conduct to be negligent, having regard

to Macquarie’s poor design and implementation of updates to key systems,

the high number of orders and trade reports containing incorrect or

missing data, the multiple categories of incorrect or missing data and

the length of time the problems persisted without detection by

Macquarie.

Given Macquarie’s scale, market share and high market flows, the MDP

considers that market participants such as Macquarie have greater

potential and capacity to undermine market integrity. A market

participant such as this should carry a greater responsibility to

properly manage the risks that flow from their conduct. If that risk is

poorly managed, the financial consequences to the market participant

should be commensurately greater.

The MDP noted that, once Macquarie became aware of the scale of the

issues, which it reported to ASIC, it undertook a comprehensive review

to identify the causes, and promptly implemented remedial measures.

Brokers should be applying new credit card assessment rules to their loan applications, the solicitor director of The Fold Legal has suggested. Via The Adviser.

The Australian Securities and Investments Commission (ASIC) last year announced

new assessment criteria that is to be used by banks and credit

providers when assessing new credit card contracts or credit limit

increase for consumers.

Under

the changes, credit licensees are required to assess whether a credit

card contract or credit limit increase is “unsuitable” for a consumer

based on whether the consumer could repay the full amount of the credit

limit within the period prescribed by ASIC.

ASIC outlined last year that,

as part of the new measures, credit licensees undertaking responsible

lending assessments for “other credit products”, including mortgages,

should ensure that the consumer “continues to have the capacity to repay

their full financial obligations” under an existing credit card

contract, within a “reasonable period”.

Speaking

of the new rules, Jaime Lumsden Kelly, solicitor director of The Fold

Legal, has suggested that, while it is not mandatory for brokers, both

lenders and brokers should apply the same rules to their loan

applications.

Writing in a

blog post for The Fold Legal, Ms Lumsden Kelly elaborated: “In the past,

credit card contracts were assessed as unsuitable if the applicant

couldn’t repay the minimum monthly repayment for that limit. Under the

new rules, credit card providers must make their assessment based on

whether the applicant can repay the entire credit card limit within

three years.

“If a credit

card applicant cannot repay the full credit limit in three years, it’s

assumed that they will be in substantial hardship. This is because a

consumer who cannot afford to repay the limit within three years will

probably pay a staggering amount of interest that will take an

extraordinarily long time to repay.

“If

the applicant is in substantial hardship, the credit card provider must

decline the application as being unsuitable,” she said.

While

the rule doesn’t “technically” apply to other lenders or brokers, the

lawyer added that “all lenders and brokers have an obligation to reject a

credit contract if it would place the consumer into substantial

hardship”.

“If the

inability to repay a credit card within three years is considered to be a

substantial hardship when assessing a credit card application, how can

it also not be substantial hardship, if a consumer will no longer be

able to repay their credit card within three years because they’re

meeting new repayment obligations on a car or home loan?” she said.

Ms Lumsden Kelly gave the following scenarios as an example to illustrate the point.

In

the first scenario, an applicant with a $500,000 mortgage applies for a

$15,000 credit card. When assessing the credit card, the provider

determines that the applicant is “unsuitable” because they won’t have

enough income to repay their credit card limit in full within three

years. So the credit card provider declines the application.

However,

if the same applicant already has a $15,000 credit card and then

applies for a $500,000 mortgage (on identical terms as in the first

scenario). The licensee is only required to consider whether the

applicant can make the minimum monthly repayment on their credit card

when determining if they will suffer substantial hardship. On this

basis, the licensee approves the mortgage.

“The

end result for the applicant is the same in both scenarios,” she said.

“They have a $500,000 mortgage and a $15,000 credit card limit. So how

can we say that they are in substantial hardship in one scenario but not

in the other?

“It’s an

absurd outcome that the same person could be approved or declined for a

credit product just because they applied for them in a particular

order.”

The Fold Legal

solicitor concluded: “Over time, the courts and AFCA may seek to align

the obligations of all credit providers and brokers. In the meantime,

ASIC has said it expects all credit licensees to apply the rule to

existing credit cards by 1 July 2019.

“This

means credit providers and brokers should consider the implications of

this situation when determining how they will assess a credit card

holder’s capacity to pay and substantial hardship for other loan

applications.”

She urged any brokers unsure of how the rules affect their business or credit obligations to contact a lawyer.

Following an ASIC investigation, Citigroup will refund over $3 million to 114 retail customers for losses arising out of structured product investments offered by Citigroup between 2013 and 2017. Citigroup will also write to over 1000 customers remaining in the products to provide them an opportunity to exit early without cost.

ASIC investigated Citigroup’s sale and provision of general advice to

customers for fixed coupon structured products, which are complex,

capital at risk products tied to the performance of reference shares.

ASIC was concerned that while Citigroup considered its financial

advisers to be providing general advice, elements of its practice may

have led some customers to believe that Citigroup was providing personal

advice.

Citigroup’s practices included its advisers asking customers about

their personal circumstances, such as their tolerance for risk, and

providing financial education about benefits and risks to customers who

had no previous experience of investing in structured products.

Financial advisers have higher obligations and disclosure requirements

when providing personal advice.

From 1 January 2018, as a result of ASIC’s investigation, Citigroup

ceased selling structured products to retails clients under a general

advice model.

Citigroup will shortly start contacting affected customers. The

remediation will be completed by 10 September 2019, will be

independently assured and Citigroup will report to ASIC once the process

is complete.

ASIC has warned Australian financial services licensees that offer over-the-counter derivatives to retail investors located overseas could be breaking laws abroad, with Chinese authorities having alerted the watchdog that some online platforms have engaged in illegal activity, via InvestorDaily.

Regulators

in jurisdictions including Europe, Japan, North America and China have

restricted or prohibited the provision of certain OTC derivatives, such

as binary options, margin foreign exchange and other contracts for

difference (CFDs) to mitigate harm to retail investors.

ASIC has

expressed concern that some OTC derivative issuers that hold AFSLs may

be marketing or soliciting overseas clients to open accounts with

Australia-based licensees on the basis of avoiding overseas intervention

measures.

The regulator said is it considering whether breaching

overseas laws is consistent with obligations under Australian law to

provide services ‘efficiently, honestly and fairly’.

ASIC is also

considering whether it will see AFSL holders could be making misleading

or deceptive statements about the scope or effect of their license.

“AFS licensees who break the law in overseas

jurisdictions, or who mislead retail investors about their services

undermine the integrity of the Australian licensing regime,”

commissioner Cathie Armour said.

“ASIC will not tolerate that conduct.”

Chinese

authorities have already informed ASIC that “some online platforms are

illegally engaged in forex margin trading activities”.

Under Chinese law, no institution or agency has approval to carry out margin foreign exchange trading.

Temporary

product intervention measures have also been extended in Europe by the

European Securities and Markets Authority, with authorities in the UK

and Germany introducing permanent measures including anti-avoidance

provisions.

“AFS licensees offering OTC derivatives to overseas

retail clients should, as a matter of priority, seek advice on the

legality of their offerings to these clients,” commissioner Armour said.

“Any non-compliant activities should cease immediately and be notified to ASIC and the relevant overseas authorities.”

ASIC has released KordaMentha Forensic’s final report on CBA’s advice compensation program under its additional licence conditions.

CBA has offered approximately $9.3 million to customers whose advice has been reviewed as a result of the licence conditions imposed by ASIC in August 2014.

ASIC had imposed additional conditions on the Australian financial

services (AFS) licences of CBA’s Commonwealth Financial Planning Ltd and

Financial Wisdom Ltd with the consent of the licensees in August 2014,

and appointed KordaMentha Forensic as the independent expert to monitor

the licensees’ compliance with the additional licence conditions.

ASIC took this action because the licensees did not apply review and

remediation processes consistently to customers of 15 financial

advisers, disadvantaging some customers. The additional licence

conditions required that CBA offer compensation for inappropriate advice

that caused financial loss (where applicable) and offer affected

customers up to $5,000 to get independent advice from an accountant,

financial adviser or lawyer.

KordaMentha Forensic has produced five reports since the licence conditions took effect. In the first report, the Comparison Report, KordaMentha

Forensic identified inconsistencies in treatment of clients and

required the licensees to correct the inconsistencies for approximately

2,740 customers.

In the second report, the Identification Report,

KordaMentha Forensic found that the licensees had taken reasonable

steps in 2012 to identify which clients of the 15 advisers had to be

included in the compensation program.

KordaMentha Forensic also found that the licensees had taken

reasonable steps to identify other potentially high-risk advisers, but

that the licensees had not adequately reviewed advice given by 17 of

those advisers. To address this, KordaMentha Forensic prescribed the

scope of the additional reviews (of the 17 advisers) that the licensees

had to undertake.

KordaMentha then produced three additional reports describing the

licensees’ compliance with the conditions, the additional steps that the

licensees were required to take, and the compensation outcomes. Compliance Report Parts 1 & 2 assessed

the steps taken by the licensees to communicate with and compensate

(where applicable) customers of 15 former advisers for advice provided

between 2003 and 2012.

Compliance Report Part 3 described

the licensees’ review of the 17 potentially high-risk advisers and

KordaMentha Forensic’s conclusion that the licensees should apply the

compensation program to customers of five of those advisers.

In the final report, Compliance Report Part 4,

published today, KordaMentha Forensic covers the last of CBA’s advice

compensation program under the licence conditions. The report states

that CBA has offered a further $2.3 million to 232 clients of the five

advisers. This is in addition to:

$4.95 million (including interest) offered to customers of different

advisers under the licence conditions (reported in KordaMentha

Forensic’s Compliance Report Parts 1 & 2);

$1.9 million (including interest) offered to additional customers as

a result of CBA’s review outside the licence conditions. The need for

these reviews was identified during the licence conditions process.

This means that CBA has offered approximately $9.3 million to

customers whose advice has been reviewed as a result of the licence

conditions imposed by ASIC in August 2014.

ASIC has welcomed the passage of key financial services reforms contained in the Treasury Laws Amendment (Design and Distribution Obligations and Product Intervention Powers) legislation introducing:

a design and distribution obligations regime for financial services firms; and

a product intervention power for ASIC

The design and distribution obligations will bring accountability for

issuers and distributors to design, market and distribute financial and

credit products that meet consumer needs. Phased in over two years,

this will require issuers to identify in advance the consumers for whom

their products are appropriate, and direct distribution to that target

market.

The product intervention power will strengthen ASIC’s consumer

protection toolkit by equipping it with the power to intervene where

there is a risk of significant consumer detriment. To take effect

immediately, this will better enable ASIC to prevent or mitigate

significant harms to consumers.

These reforms were recommended by the Financial System Inquiry in

2014 and represent a fundamental shift away from relying predominantly

on disclosure to drive good consumer outcomes.

ASIC Chair James Shipton said the reforms were a critical factor in

the development of a financial services industry in which consumers

could feel confident placing their trust.

‘These new powers will enable ASIC to take broader, more proactive

action to improve standards and achieve fairer consumer outcomes in the

financial services sector. This will be a significant boost for ASIC in

achieving its vision of a fair, strong and efficient financial system

for all Australians,’ he said.

‘This will also provide invaluable assistance to ASIC as we all seek

to rebuild the community’s trust in our banking and broader wealth

management industries. And we note the overwhelming level of support

this attracted from across the Parliament.’

Mr Shipton also welcomed the amendments to the original legislation,

which extended the reach of these reforms, providing a comprehensive

framework of protection for most consumer financial products. It will

also empower ASIC to intervene in relation to a wider range of products

where ASIC identifies a risk of significant detriment to consumers.

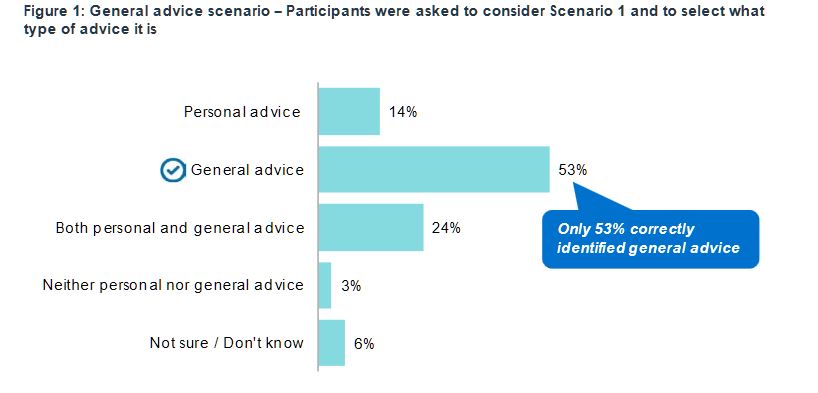

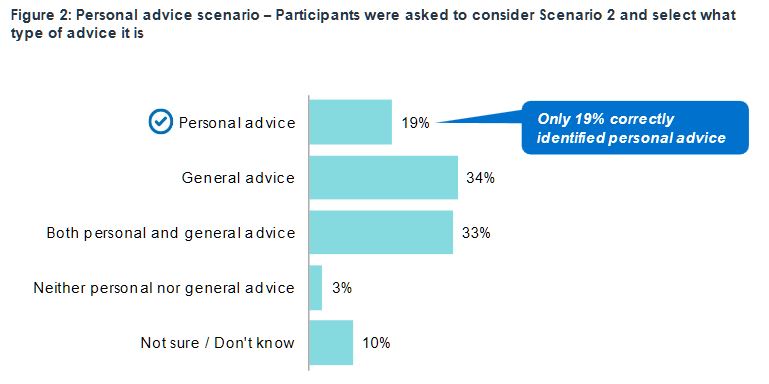

ASIC has released new research revealing many consumers confuse ‘general’ and ‘personal’ advice exposing them to greater risk of poor financial decisions.

The ASIC report, Financial advice: Mind the gap (REP

614), presents new independent research on consumer awareness and

understanding of general and personal financial advice, identifying

substantial gaps in consumer comprehension.

“This disturbing gap in understanding whether the advice they are

getting is personal or not means many consumers are under the false

premise their interests are being prioritised, when no such protection

exists,” said ASIC Deputy Chair, Karen Chester.

Millions of Australians will likely seek financial advice at some

stage in their lives. When they do, it is critical they understand

whether that advice is personal, whether it is tailored to their

circumstances and does the adviser have a legal obligation to act in

their interest.

“The survey not only revealed consumers are not familiar with the concepts of general and personal advice, but only 53 per cent of those surveyed correctly identified ‘general’ advice. And even when provided the general advice warning, nearly 40 per cent of those surveyed wrongly believed the adviser had an obligation to take their personal circumstances into account,” Ms Chester said.

The report highlights the importance of consumer awareness and

understanding of the distinction between personal and general advice

with the Future of Financial Advice (FOFA) protections only applying

when personal advice is provided. These include obligations for advisers

to act in their client’s best interests, to provide advice that is

appropriate to their client’s personal circumstances and to prioritise

their client’s interests. These obligations do not apply when general

advice is provided.

“The survey also revealed that the responsibilities of financial

advisers, when providing general advice, is not well understood. Nearly

40 per cent of those surveyed were unaware that advisers were not required by law to act in their clients’ best interests,” Ms Chester said.

ASIC anticipates the need for financial advice to grow, reflecting an

ageing population and many financial products, especially retirement

products, becoming more complex. ASIC reports that much of the advice is

likely to be general advice, and while appropriate in some

circumstances, it is inevitably of limited use.

“ASIC is seeing increased sales of complex financial products under

general advice models – so not tailored to personal circumstances –

leaving many consumers, especially retirees, exposed to the potential

risk of financial loss. And whilst the Financial Services Royal

Commission, and the Government’s response, dealt with the most egregious

risks of hawking of complex financial products, consumer confusion

about what is personal and general advice needs to be addressed,” Ms

Chester said.

The report’s findings reinforce those of the Murray Financial System

Inquiry and the Productivity Commission reports on the financial and

superannuation systems. Those reports made recommendations about the use

of the term ‘general advice’, which is likely to lead to false consumer

expectations as to the value of and protections afforded advice

received.

Ms Chester said, “This consumer research is timely. It comes as the

Government is considering policy recommendations on financial advice

from the Productivity Commission’s twin reports on Australia’s financial

and superannuation systems. And at a time when the financial system

itself undergoes much change, following the intense scrutiny of the

Financial Services Royal Commission, including considering new financial

advice and distribution business models”.

The report includes quantitative and qualitative research

commissioned by ASIC and undertaken by independent market research

agency, Whereto Research. The research used hypothetical advice

scenarios to test consumer recognition of when general and personal

advice was being provided, and awareness of adviser responsibilities

when being given each type of advice.

Report 614 Financial advice: Mind the gap is the first stage

in ASIC’s broader research project into consumer experiences with and

perceptions of the financial advice sector. Additional research by ASIC

will get underway in 2019 to identify a more appropriate label for

general advice and consumer-test the effectiveness of different versions

of the general advice warning.

ASIC today released an update on the fees for no service (FFNS) further review programs undertaken by six of Australia’s major banking and financial services institutions.

ASIC’s ongoing supervision of the review programs undertaken by AMP,

ANZ, CBA, Macquarie, NAB and Westpac (the institutions) has shown that

most of the institutions are yet to complete further reviews – i.e. reviews to identify systemic FFNS failures beyond those already identified and reported to ASIC since 2013.

ASIC Commissioner Danielle Press said the institutions had taken too

long to conduct these reviews, and welcomed the Government’s commitment

to give ASIC new directions powers that could speed up remediation

programs in the future.

‘These reviews have been unreasonably delayed. ASIC acknowledges that they are large scale reviews – they relate to systemic failures over long periods with reviews going back six to 10 years and cover 36 licensees from the six institutions that currently authorise more than 7,000 advisers]. However, we believe the institutions have failed to sufficiently prioritise and resource their reviews, particularly as ASIC advised them to commence the reviews in mid-2015 or early 2016.

‘We are pleased the Government has agreed to adopt recommendations from the 2017 ASIC Enforcement Review Taskforce Report,

which includes a directions power. This would allow ASIC to direct AFS

licensees to establish suitable customer review and compensation

programs,’ she said.

The main reasons for delays by the institutions are:

poor record-keeping and systems within the institutions, which mean

that in many cases they have been unable to access customer files for

review;

failure by some institutions to propose reasonable customer-centric

methodologies to identify and compensate customers despite ASIC’s clear

articulation of expectations. (For example, ASIC rejected a few of the

methodologies such as a requirement for customers to ‘opt-in’ to the

review and remediation program, and a proposal to assess if there had

been a ‘fair exchange of value’ with customers instead of assessing

whether customers received the specific services they paid for); and

some institutions have taken a legalistic approach to determination

of the services they were required to provide. (For example, ASIC’s view

is that if the agreement requires an annual review, the mere offer of

an annual review is not sufficient.)

Overview of ASIC’s FFNS work

ASIC’s large-scale FFNS supervisory work includes overseeing:

the institutions’ programs to compensate customers impacted by the

reported failures to provide advice services paid for by customers (compensation programs); and

the institutions’ reviews to determine whether there were further

systemic FFNS failures beyond those already identified and reported to

ASIC (further reviews).

Under the compensation programs, AMP, ANZ, CBA, NAB and Westpac have

collectively paid or offered approximately $350 million in compensation

to customers who were charged financial advice fees for no service at

the end of January 2019. Additionally, the institutions have provisioned

more than $800 million towards potential compensation for further

systemic FFNS failures. However, these reviews are incomplete.

Along with supervision of the compensation programs and further reviews undertaken by the institutions, ASIC

is also conducting a number of FFNS investigations and plans to take

enforcement action against licensees that have engaged in misconduct.

ASIC said the royal commission’s recommendations reinforce and will inform the implementation of steps ASIC has been taking as part of a strategic program of change that commenced in 2018 to strengthen its governance and culture and to realign its enforcement and regulatory priorities; via InvestorDaily.

“There are 12 recommendations that are directed at ASIC, or where the

Government’s response requires action now by ASIC, without the need for

legislative change. ASIC is committed to fully implementing each of

these,” ASIC said in a statement.

“Many of the recommendations made by the Royal Commission involve

reforms ASIC advocated for in its earlier submissions to the Royal

Commission and, in some cases, in earlier reviews and inquiries.”

These include:

• an expanded role for ASIC to become the primary conduct regulator in superannuation;

• the extension of Banking Executive Accountability Regime (BEAR)-

like accountability obligations to firms regulated by ASIC, with their

focus being on conduct;

• the end of grandfathering of Future of Financial Advice (FOFA) commissions;

• the extension of the proposed product intervention powers and

design and distribution obligations to a broader range of financial

products and services;

• the extension of ASIC’s role to cover insurance claims handling and

the application of unfair contract terms laws to insurance;

• reforms to breach reporting; and

• ASIC being provided with a directions power

Recommendation 1.8 – Amending the Banking Code

ASIC confirmed it will commence work immediately with the banking

industry on appropriate amendments to the banking code in relation to

each of these recommendations.

Recommendation 4.9 — Enforceable code provisions

ASIC will work with industry in anticipation of the parliament

legislating reforms in relation to codes and ASIC’s powers to provide

for ‘enforceable code provisions’.

“This work will include a focus on which code provisions need to be

made ‘enforceable code provisions’ on the basis they govern the terms of

the contract made or to be made between the financial services provider

and the consumer,” the regulator said.

“ASIC will also continue to work within the existing law to improve the quality of codes and code compliance.”

Recommendation 2.4 — Grandfathered commissions

The royal commission recommended that grandfathering provisions for

conflicted remuneration should be repealed as soon as is reasonably

practicable.

The government has agreed to end grandfathering of conflicted remuneration effective from 1 January 2021.

Consistent with the government’s response to this recommendation,

ASIC said it will monitor and report on the extent to which product

issuers are acting to end the grandfathering of conflicted remuneration

for the period 1 July 2019 to 1 January 2021.

“This will include consideration of the passing through of benefits

to clients, whether through direct rebates or otherwise,” ASIC said.

Recommendation 2.5 — Life risk insurance commissions

The royal commission recommended that when ASIC conducts its review

of conflicted remuneration relating to life risk insurance products and

the operation of the ASIC Corporations (Life Insurance Commissions)

Instrument 2017/510, it should consider further reducing the cap on

commissions in respect of life risk insurance products.

The final report recommended that unless there is a clear

justification for retaining those commissions, the cap should ultimately

be reduced to zero.

ASIC today confirmed it will implement this recommendation.

“ASIC will consider this recommendation and factors identified by the

Royal Commission in undertaking its post implementation review of the

impact of the ASIC Corporations Life Insurance Commissions Instrument

2017/510, which set commission caps and clawback amounts, and which

commenced on 1 January 2018,” the regulator said.

As noted by the royal commission, and consistent with the government’s timetable, ASIC’s review will take place in 2021.

Recommendation 6.2 — ASIC’s approach to enforcement

The regulator said actions are already underway to adopt an approach

of enforcement that considers whether a court should determine the

consequences of a contravention.

In particular, ASIC has adopted a ‘Why not litigate?’ enforcement stance and initiated an internal enforcement review (IER).

“ASIC’s Commission has determined to create a separate Office of

Enforcement within ASIC and this will be implemented in 2019,” the

regulator said.

“ASIC will take the IER report and the Royal Commission’s comments on

it into account, as it makes its final changes to its enforcement

policies, procedures and decision-making structures to deliver on its

‘Why not litigate? enforcement stance.”

Recommendation 6.10 — Co-operation memorandum

Together with APRA, ASIC has agreed to implement this recommendation,

including in relation to any statutory obligation to cooperate, share

information and notify APRA of breaches or suspected breaches, that the

Government puts in place as part of its response to Recommendation 6.9.

Recommendation 6.12 — Application of the BEAR to regulators

The royal commission recommended that both APRA and ASIC internally

formulate and apply a management accountability regime similar to those

established by BEAR.

ASIC agrees to implement this recommendation. In anticipation of the

Government’s establishment of the external oversight body, ASIC will

commence work on developing accountability maps consistent with the

BEAR.

ASIC will consider the approach of the Financial Conduct Authority in

implementing this recommendation. ASIC will develop and publish

accountability statements before the end of 2019.

ASIC is appealing last year’s landmark Federal Court decision, determinedto prove two Westpac subsidiaries provided personal financial advice despite not being licensed to do so, via Financial Standard.

In

December 2018, Justice Jacqueline Gleeson determined Westpac Securities

Administration Limited (WSAL) and BT Funds Management (BTFM) had

breached the Corporations Act in 2014, during two telephone campaigns in

which staff recommended the rollover of superannuation accounts to

Westpac/BT super products.

However,

the judge said ASIC failed to prove the phone calls constituted

personal financial advice. Under their respective AFSLs, WSAL and BTFM

are only licensed to provide general advice.

ASIC has now filed an

appeal of the decision, seeking greater clarity and certainty as to the

difference between general and personal advice for consumers and

financial services providers.

“The

dividing line between personal and general advice is one of the most

important provisions within the financial services laws. It directly

impacts the standard of advice received by consumers,” ASIC deputy chair

Daniel Crennan said.

“This is why ASIC brought this test case and

ASIC believes further consideration by the full court of the Federal

Court is necessary to better inform consumers and industry.”

The

case concerned 15 phone calls which the judge determined to be general

advice “because the callers did not consider one or more of the

objectives, financial situation and needs of the customers to whom the

advice was given.”

However, in 14 of the 15 calls, the law was

breached by the implication that the rollover of super funds into a BT

account was recommended. While not dishonest, the product advice was not

provided efficiently, honestly and fairly, the judge deemed.