We look at the latest stats from APRA on branch and ATM networks, both of which are shrinking fast.

https://www.apra.gov.au/authorised-deposit-taking-institutions-points-of-presence-statistics

Digital Finance Analytics (DFA) Blog

"Intelligent Insight"

We look at the latest stats from APRA on branch and ATM networks, both of which are shrinking fast.

https://www.apra.gov.au/authorised-deposit-taking-institutions-points-of-presence-statistics

I discussed the future of ATMs with Neil Mitchell on 3AW following the banks’ removal of withdrawal fees last year. Now many banks are removing these devices as usage falls, but should they have a social obligation (in the light of the Royal Commission)?

The ACCC says ATM provider Cardtronics has admitted that its subsidiary, DC Payments, offered contract terms with small business that may be unfair under the Australian Consumer Law.

Cardtronics has given a court-enforceable undertaking to the ACCC to change terms that may be unfair for businesses under existing contracts.

“Business contracts need to balance the rights of each party to ensure they aren’t unfair, as smaller firms may not always be in a strong negotiating position,” ACCC Deputy Chair Dr Michael Schaper said.

“We considered Cardtronics’ contract had several unfair terms, including automatic renewal for six years, unilateral increase of fees, and first right of refusal should businesses seek to change providers at the contract’s conclusion.”

Cardtronic has co-operated with the ACCC’s investigation, and undertaken not to enforce unfair terms for all existing merchants, some of whom entered contracts six years ago.

“This undertaking is a great outcome for Cardtronics’ customers, as the unfair contracts protections for small business only became effective in November 2016,” Dr Schaper said.

While Cardtronics contracts will continue to be automatically renewed, the minimum notice to cancel will be reduced from six months to three months and Cardtronics will provide written notice to customers five months before the end of the contract.

Previously, merchants had to keep track of automatic rollover dates more than five years after entering contracts.

Cardtronics must also provide written notice of any fee increase to customers and allow them to terminate the contract without penalty under a new contract term.

The undertaking is available at Cardtronics Australasia Pty Ltd

Background

This outcome is part of a wider ACCC review of small business contracts in a range of industries. As part of this review, the ACCC has been engaging with a range of businesses to encourage compliance with the new unfair contract term provisions.

For more information, see Businesses remove unfair contract terms before new law.

The Australian Consumer Law allows a court to determine that a term of a standard form contract is unfair and therefore void, meaning that the contract is treated as if the term never existed.

If the term is declared void, the remainder of the contract continues to bind the parties to the extent that it can operate without the unfair term.

From 12 November 2016 the unfair contract terms provisions of the Australian Consumer Law were extended to cover standard form contracts involving small businesses.

The recently published RBA Bulletin included an article “Recent Developments in the ATM Industry”. The article shows that the number of ATMs in Australia is very high relative to population, thanks to significant growth in third party fee for service machines. Now that the banks have announced they will not charge for foreign withdrawals, the RBA says third party players – like owners of petrol stations and convenience stores may see a decline in income, and that overall declines in transaction volumes are likely to reduce the number of machines available, especially in regional areas. That said, many independently owned ATMs are in convenience locations not serviced by bank ATMs (such as pubs and clubs) and so they may be shielded somewhat from this competitive pressure. But many consumers will end up paying even higher fees to use these machines, which may be the only options for some.

The ATM industry in Australia is undergoing a number of changes. Use of ATMs has been declining as people use cash less often for their transactions, though the number of ATMs remains at a high level. The total amount spent on ATM fees has fallen, and is likely to decline further as a result of recent decisions by a number of banks to remove their ATM direct charges. This article discusses the implications of these changes for the competitive landscape and the future size and structure of the industry.

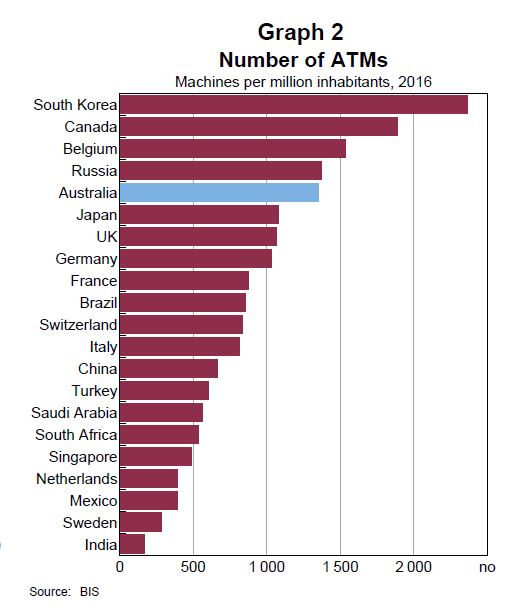

By international standards, we have a large number of ATMs per capita (though not corrected for geographic size).

As at September 2017, there were 32 275 ATMs, only slightly below the peak of nearly 32 900 in December 2016. This represents over 1 300 ATMs per million inhabitant.

The share of the national ATM fleet owned by independent deployers has been rising over the past decade. Independent deployers operate standalone ATM networks that are not affiliated with any financial institution and which are often focused on convenience locations like petrol stations and licensed venues. They rely on the revenue generated by charging fees on all transactions, irrespective of the cardholder’s financial institution, to support their networks.

As at June 2017, 57 per cent of ATMs in Australia were independently owned, up from 55 per cent in mid 2015 and 49 per cent in 2010. The remaining 43 per cent were owned by financial institutions. The increase in the independent deployers’ share reflects strong growth in their ATMs, while the number of bank-owned ATMs has declined over the past few years.

A small number of ATMs that carry financial institutions’ branding but are owned and operated by an independent deployer are recorded in data for independent deployers; other similar arrangements may be recorded under financial institutions. (b) In late 2016, DC Payments acquired First Data’s Cashcard ATM business. (c) NAB, Cuscal and Bank of Queensland, along with a number of other smaller financial institutions, are part of the rediATM network, which allows customers of member institutions to access about 3 000 ATMs (as at June 2017) within that network on a fee-free basis. From August 2017, Suncorp also joined the rediATM network. (d) In November 2017, Stargroup was placed in administration after it was unable to complete a restructure of its debt.

There has been significant consolidation in the independent deployer market over recent years. Cardtronics, an independent deployer, had the largest fleet in Australia in June at nearly 10 500 ATMs, which is around one-third of all ATMs. Cardtronics is part of a US-based group that is also the largest deployer of ATMs globally. It entered the Australian market around the start of 2017 when it acquired DC Payments, which was the largest domestic independent deployer at the time. DC Payments had itself acquired a number of smaller independent networks over earlier years, including First Data’s Cashcard ATM business in late 2016. Other large independent deployers, such as Banktech and Next Payments, have also expanded their ATM fleets since 2015, partly through acquisitions.

Despite the increase in the share of independently owned ATMs, most Australian cardholders have had access to large networks of fee-free ATMs provided by their financial institutions. As at June 2017, three of the four major banks each had fleets of at least several thousand ATMs; NAB had the smallest fleet among the majors, but it is also part of the rediATM network, which means its customers had access to about 3 000 ATMs in that network on a fee-free basis.

A number of the banks, including all the majors, have recently removed the ATM withdrawal fees they used to charge non-customers. This means Australian cardholders can now generally access cash free of charge at around 11 000 financial institution ATMs across the country, which is a significant increase in access to fee-free ATM services.

However, following the removal of withdrawal fees by various banks, the distribution has changed significantly: there is now no charge for foreign withdrawals at around one-third of ATMs, whereas most of these ATMs had previously charged $2.00. But Independent deployer ATMs have the greatest variation in ATM fees; as at June this year, their withdrawal fees ranged from zero to $8.00, though most were around $2.50 to $3.00.

With the removal of withdrawal fees providing a much larger network of fee-free ATMs, it will now be even easier for cardholders to avoid paying fees. As a result, those ATM deployers that continue to charge withdrawal fees – particularly independent deployers, who typically charge the highest average fees – may face additional competitive pressure, especially where they have ATMs in close proximity to fee-free bank ATMs. That said, many independently owned ATMs are in convenience locations not serviced by bank ATMs (such as pubs and clubs) and so they may be shielded somewhat from this competitive pressure.

For those banks that eliminated their withdrawal fees, the direct reduction in their revenue will be relatively small, especially given the decline in ATM use over recent years. In particular, based on the Bank’s survey, it is estimated that withdrawal fees paid at ATMs owned by the major banks in 2016/17 totalled around $50 million. As noted earlier, the bulk of ATM fees has been paid at independent deployer ATMs rather than bank-owned ATMs.

Given that cardholders can now effectively use most bank ATMs on a fee-free basis, it is likely that having a large ATM fleet will be viewed as less of a source of competitive advantage to banks than it was in the past. With ATM use declining rapidly and the costs of ATM deployment continuing to rise, the removal of ATM fees may strengthen the case for deployers to reduce the size of their ATM fleets. Having multiple bank ATMs side-by-side or in close proximity (as can often be seen in shopping centres, for example) will make less economic sense now that all or most of those ATMs are fee-free.

Fleet rationalisation could occur in a number of ways. Some banks (and possibly independent deployers) might look to better optimise their own fleets by removing ATMs in low-density or low-use areas. Banks may look to pool part or all of their fleets with other banks under generically branded, shared service or ‘utility’ ATM models as a way to improve efficiency, while still maintaining adequate access for cardholders.

A pooled network may enable the participants to remove ATMs that are co-located or in close proximity, which would reduce costs and help them sustain, and possibly grow, their joint network coverage. Indeed, before the recent announcements on direct charges, some banks had been in discussions about pooling their ATM fleets into a shared utility.

Facing similar downward trends in cash and ATM use, a number of other countries, particularly in northern Europe, have successfully implemented or are considering shared ATM models. For example, bank ATMs in Finland were outsourced to a single operator in the mid 1990s, while Sweden’s five largest banks adopted a utility model earlier this decade. The large Dutch banks are currently looking to set up a joint ATM network to help ensure the continued wide availability of ATMs in the Netherlands even as cash use is decreasing.

While it is too early to assess the full impact of the recent announcements by the major banks, it is likely that they will focus attention on the growing disparity between the number of ATMs in Australia and the demand for ATM services.

Some consolidation seems likely, and may even be desirable for the efficiency and sustainability of the ATM network, though it will be important that adequate access to ATM services is maintained, particularly for people in remote or regional locations, where access to alternative banking services is often limited.

The ACCC has issued a draft determination proposing to grant re-authorisation to parties to provide fee free ATM services in very remote Indigenous communities for 10 years.

Under the arrangement, participating banks and ATM deployers provide fee-free ATM withdrawals and balance enquiries at up to 85 selected ATMs for customers of those banks. The ACCC previously authorised the arrangement in 2012 for five years, which expires in December.

“The arrangement co-ordinated by the Australian Bankers’ Association has resulted in significant public benefits over the past five years, which are likely to continue for the next ten years,” ACCC Commissioner Roger Featherston said.

People living in very remote Indigenous communities can often pay high levels of total ATM fees, due to frequent ATM usage and a lack of access to alternatives.

“High ATM usage and fees intensifies the financial and social disadvantage found in very remote communities. Enabling Indigenous people in these communities to have the same access to fee-free ATMs that other Australians enjoy in less remote parts of the country lessens this disadvantage,” Mr Featherston said.

The proposed conduct allows for additional banks and ATM deployers to be added to the arrangement.

The communities to benefit from this project are located across the Northern Territory, Queensland, South Australia and Western Australia. The full lists of ATM locations and participating banks are attached to the draft determination, available on the public register.

The ACCC is now seeking submissions on the draft determination by 16 November 2017 and expects to release its final determination in December 2017.

The CBA led move last weekend to abolish foreign ATM fees, which was quickly followed by the other majors and Suncorp is a benefit to those using other banks ATMs to withdraw cash, and will be especially welcome in regional and rural areas, where travel times to own branch machines tends to be extended.

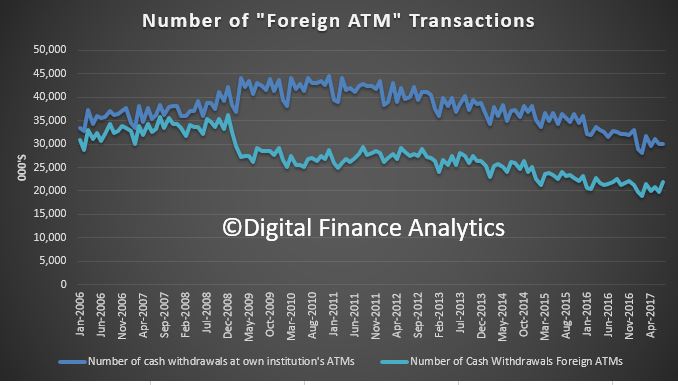

We showed that the volume of cash withdrawals is decreasing.

ATMs are now a legacy banking artifact, to be managed not for strategic advantage (replacing more expensive branches) but to reduce costs, as it is being replaced by electronic payments, pay waive and mobile devices.

ATMs are now a legacy banking artifact, to be managed not for strategic advantage (replacing more expensive branches) but to reduce costs, as it is being replaced by electronic payments, pay waive and mobile devices.

The timing, I suggest, rather than being a deliberate attempt to distract from the BEAR proposals which were released by the Government a couple of days before; is more an outworking of recent discussions, centered on driving more cost savings from the ATM system. The fact is ATMs are expensive animals to service, not so much from the technology point of view, but because the cash cartridges need to be physically replenished, which requires a small army of security guards, vans, and a supply of fresh notes. Remote ATMs are especially costly to service. Many are outsourced.

We examined the Point of Presence Data from APRA which includes counts of ATMs, listed by bank, and other provider. This annual report is helpful when exploring distribution strategy, though the format will be changed this coming edition. We have data to 2016.

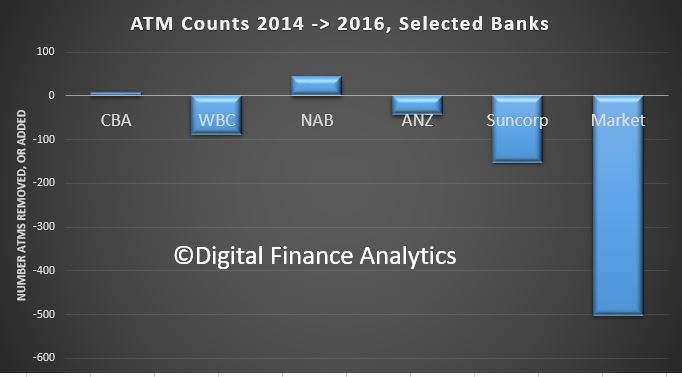

It shows that between 2014 and 2016 there was a 3.5% fall in the number of ATMs operating, with a total count of 14,293. We lost net, net around 500 machines in 2 years.

We then looked at the major banks, and Suncorp. Suncorp was responsible for a net 152 reduction, followed by Westpac 88 and ANZ 43. NAB grew their fleet by 45 and CBA by 7.

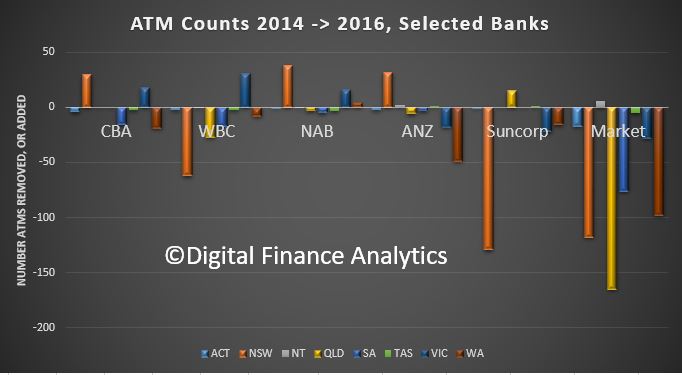

The state by state data shows that Queensland lost the most machines, down 165, then NSW 118, WA 98 and SA 76. By bank, CBA, NAB and ANZ grew their footprint in NSW, while WBC and Suncorp cut machines significantly there.

The state by state data shows that Queensland lost the most machines, down 165, then NSW 118, WA 98 and SA 76. By bank, CBA, NAB and ANZ grew their footprint in NSW, while WBC and Suncorp cut machines significantly there.

Now, the point of all of this is that given falling transaction volumes, we expect the number of ATMs to continue to fall. The removal of “foreign” ATMS fees allows consumers to use any ATM within reach. As a result, banks can with some justification say that therefore multiple ATMs in a location are no longer required. As a result I expect a rush of closures, with the aim of not being the “last man standing” effectively holding the community service obligation in a given area.

Now, the point of all of this is that given falling transaction volumes, we expect the number of ATMs to continue to fall. The removal of “foreign” ATMS fees allows consumers to use any ATM within reach. As a result, banks can with some justification say that therefore multiple ATMs in a location are no longer required. As a result I expect a rush of closures, with the aim of not being the “last man standing” effectively holding the community service obligation in a given area.

So, in my view the ATM fee story is more about managing down legacy systems and costs than providing customer benefit. Think of it as a utility service. The Banks should consider formalising this in my view!

You could argue, provided you can still get cash, you may not care, but of course if there is a single machine in town, it is also a point of single failure, especially over a long weekend!

As always, there is more behind the PR than first appears….

Suncorp will remove fees for all non-Suncorp customers so that no customer pays an ATM fee anywhere in Australia.

Suncorp Executive General Manager Deposits & Investments, Bruce Rush says the change will deliver greater value to all banking customers while increasing the availability of fee-free ATMs across the country.

“Suncorp supports fee-free ATMs and we will implement this change in early December to coincide with other positive changes, including updating technology and enhancing customer experience which is already planned for our ATM network,” Mr Rush said.

“It is great to see all Australians benefit and we are especially pleased for Suncorp customers who live in locations where there are limited options to withdraw cash.”

All the major banks have removed foreign ATM fees. The ABA welcomed the move.

Statement from Anna Bligh, Australian Bankers’ Association Chief Executive:

“The ABA welcomes the announcement from the major banks today to abolish ATM fees.

“It’s a boon for customers and makes banking more affordable for everyday Australians.

“This is the latest in a suite of initiatives by banks to create better products and services for customers and boost customer choice, including reducing interest rates on credit cards and offering fee-free transaction accounts.

“A competitive banking system is good for customers and good for the sector.”

NAB has today announced it will remove ATM withdrawal fees for everyone using any of its NAB ATMs around the country.

Already, NAB customers using NAB ATMs incur no cash withdrawal fee.

“We’re pleased to now extend this so that all Australians, regardless of whether they bank with NAB or not, can use any of our ATMs and not be charged a cash withdrawal fee,” NAB Chief Customer Officer of Consumer Banking and Wealth, Andrew Hagger, said.

“This is a good outcome for customers. We know it has been frustrating for them to be charged to withdraw their own money from an ATM, and the change we are announcing today will benefit millions of Australians.

“At NAB, we’re proud of our track record of making banking fairer over many years, and we will always look at how we can improve the experience and services we provide customers.”

Since 2009, NAB has led the industry by removing many of the fees and charges that annoy customers the most, and NAB remains the only major bank to have a transaction account with no monthly account service fee, saving customers around $5 every month.

“NAB’s commitment is to back our customers by continuing to listen to them, and respond to their concerns and needs so we can be a better bank,” Mr Hagger said.

ANZ today announced it would remove fees for all non-ANZ customers using its fleet of automatic teller machines anywhere in Australia. The change will impact non-ANZ customers who are currently charged a $2 fee when they use an ANZ ATM.

ANZ customers are not currently charged when they use one of ANZ’s more than 2,300 machines. ANZ Group Executive Fred Ohlsson said: “While we had been actively working on how we provide fee free ATMs for our customers, we have decided to remove these fees all together from October.

“We know ATM fees are one of the most unpopular and while our customers have benefitted from our network of ATMs across the country, this is another example of acting on customer feedback as well as genuine reform from the industry,” Mr Ohlsson said.

The change will be implemented in early October 2017.