CBA cut interest rates by as much as 0.30% across its savings accounts yesterday, exemplifying the tactics many banks are using to help recoup the costs incurred from reducing home loan rates by the full 0.25% March cash rate reduction. Via Australian Broker.

Two weeks before the major’s home loan

reductions come into effect, the ongoing bonus rates on its Goal Saver

account have been reduced by 0.25%, its pensioner security account by up

to 0.25% and its Youth Saver account by 0.30%; the NetBank Saver

account was unchanged, with an ongoing rate of just 0.10%

“CBA is one of six banks so far to cut

deposit rates since last week’s cash rate cut, with dozens more expected

to follow,” said RateCity.com.au research director Sally Tindall.

“It’ll be interesting to see how far

Westpac, NAB and ANZ shave their rates, seeing as they’ve already taken

the knife to some of their savings rates this year.

“In this low rate environment, finding a

savings rates above inflation can feel like finding a needle in a

haystack, but they are out there.”

The highest rate currently on offer is 2.25%, which can be found at neobanks 86 400 and Xinja Bank.

However, they’re “unlikely to stick around”, according to Tindall.

Last week, Xinja announced no new Stash

savings accounts will be able to be opened for an indefinite period, in

order to take care of existing customers.

For now, the neobank will maintain its

2.25% rate, with no strings attached and interest paid from the first

dollar up to $245,000, calculated daily and paid monthly.

“When faced with higher than expected deposit flows, and an RBA

rate cut, most banks would just drop deposit interest rates, hurting

existing customers while chasing new ones. That’s not what Xinja is

about,” said CEO and founder, Eric Wilson.

“Xinja offers a different way of banking, and that extends beyond technology to how we treat our customers.”

However, Wilson did reiterate the Stash account has a variable rate which may go up or down in the future.

“Right now, in what are turbulent times, we want to stand by the rate we have offered,” he said.

“But there are three things we have to

balance: the RBA rate cut makes it more expensive for Xinja to hold

deposits at the same rate before the launch of our lending program;

there has been an unprecedented uptake of Xinja Bank by Australians; and

now, how we – as a new bank – manage the costs of those deposits. “

Despite the recent influx of positive reporting on the trajectory of the housing market, there remains “a fundamental, structural problem” with the price of property in Australia, according to financial analyst Martin North. Via Australian Broker.

While the rising home values evidenced

from mid-2019 have been largely celebrated as an overtly positive trend,

North has his doubts.

“It’s not sensible to hope and assume

prices will continue to go ever higher. House prices are very high

relative to income. Actually, very high relative to any other measure

you can name, like GDP,” he said.

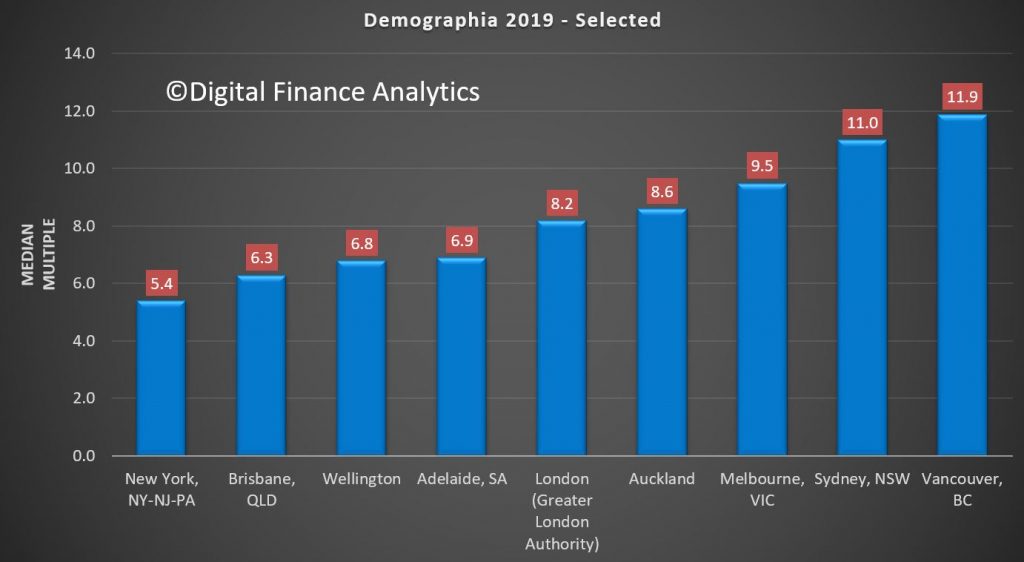

A recently-released Demographia survey

showed Australia has some of the most unaffordable property in the

world. While Hong King and Vancouver claimed the top two spots on the

list, Sydney and Melbourne came right after.

“Further, we’ve got too much debt in our

system, which is supported by debt that’s difficult to repay, even at

low interest rates,” said North.

“There is definitely a cap, in my view, on how much home price growth we should expect and will see.”

The affordability concerns which have

dominated Australia for years were again thrown into sharp relief by

recent figures around hopeful market entrants.

“The latest data shows the first home

buyer average loan is now $408,000 across Australia – the highest it’s

ever been,” said North.

“That’s massive for a first-time buyer

trying to get into the market. Think about the income multiples that

figure represents; that’s maybe eight, nine, 10 times what many people

make.

“It’s an unsustainable position to be in.

We can’t allow home prices to continue to run away. It will create a

bigger problem for us later.”

It’s important to focus on the hard data amidst the sea of vested parties doubling down on their own rhetoric, North said.

“The banks want property prices to go

higher because if they go lower, they have much more risk in their

system and on their books than they want to admit,” he explained.

“The Reserve Bank and Treasury both want

prices to rise to create the wealth effect. If people feel more wealthy,

which they generally do as prices rise, they go and spend more. Trying

to bring prices higher is really the only lever they’ve got.”

However, according to North, it’s “failed

policy” to bank the future of the economy on “ever-inflated house

prices” with nothing else to support it.

“I come back to the fundamental reality of the ratio between debt and income, the ratio between debt and GDP,” he said.

“We’re in an unsustainable position. We’re

betting the farm on the property sector and, in my view, it’s going to

fall over at some point; it’s just a question of how soon.”

The government has released the draft legislation implementing 22 recommendations and two additional commitments which arose from the Hayne Royal Commission, including recommendations 1.6 and 2.7 which establish a compulsory scheme for checking references for prospective financial advisors and mortgage brokers. Via Australian Broker.

Before the royal commission began, under

ASIC’s Regulatory Guide 104, both Australian financial services

licensees and Australian credit licensees were meant to undertake

appropriate background checks before appointing new representatives,

through referee reports, searches of ASIC’s register of banned and

disqualified persons or police checks.

However, despite this requirement’s existence, the royal commission found financial services licensees weren’t doing enough to communicate the backgrounds of prospective employees among themselves, highlighting that licensees “frequently fail to respond adequately to requests for references regarding their previous employees” and that they do not “always take the information they receive seriously enough”.

As such, financial advisers facing

disciplinary action from an employer were able to simply leave and find

another to employ them.

Recommendation 1.6 and 2.7 seek to address this systemic weakness.

The latter looks to promote better

information sharing about the performance history of financial advisers,

focusing on compliance, risk management and advice quality, while the

former made sure this change is extended to mortgage brokers as well.

According to the draft legislation, the

reporting obligation “targets misconduct by and serious compliance

concerns about individual mortgage brokers” and “recognises that in the

industry, other parties such as lenders and aggregators are often well

positioned to identify this misconduct”.

Obligation to undertake reference checking and information sharing

New law: Both Australian financial

services licensees and Australian credit licensees are subject to a

specific obligation to undertake reference checking and information

sharing regarding a former, current or prospective employee.

Current law: Australian financial services

licensees are subject to general obligations, including taking

reasonable steps to ensure its representatives comply with the financial

services laws and credit legislation.

Civil penalty for failure to undertake reference checking and information sharing

New law: Australian financial services

licensees and credit licensees who fail to undertake reference checking

and information sharing regarding a prospective employee are subject to a

civil penalty.

Current law: No equivalent.

The proposed legislation will be in

consultation until 28 February, with interested parties invited to make a

submission before the deadline.

Westpac has announced that for one year, it will cover the mortgage repayments of home loan customers who lost their principal place of residence due to the bushfires raging across the country, paying up to $1,200 per month per customer. Via Australian Broker.

Westpac’s Bushfire Recovery Support

Package also includes interest free home loans to cover the gap between

insurance payouts and construction costs for consumers who need to

rebuild, as well as $3m in funds allocated to bushfire emergency cash

grants, of which eligible retail customers can claim up to $2,000.

At the time of writing, the bushfires have

claimed the lives of 28 people across the country, with over 3,000

homes destroyed or damaged in New South Wales alone.

“These initiatives are designed to provide

practical, on the ground support for our customers, our people and for

those who are caring for affected communities,” said Peter King,

Westpac’s acting CEO.

The relief package also makes grants of up

to $15,000 available to assist small businesses with the cost of

refurbishing premises that have been damaged or destroyed during the

bushfires.

Westpac has committed to “fast tracked”

credit approvals to provide short-term assistance to businesses impacted

by the fires, as well as offering 2.83% three-year variable rate,

low-interest rebuilding loans.

Further, no foreclosures will be made for

three years on any farming businesses in the affected areas, and all

volunteer firefighters across the nation are able to access the Disaster

Relief Package.

FBAA managing director Peter White has

encouraged brokers to be aware that it’s not only clients who have lost

their properties that are unable to meet their mortgage repayments;

while that subsection may be the most likely to automatically speak to

their lenders and insurers, there are many others whose properties were

not touched by fire but have been impacted in other ways.

“There will be those who have had to

evacuate, or who may operate a small business that has seen a dramatic

drop in revenue because an area has been blocked off. There will be

others who have had to sacrifice their earnings to help friends, family

or their community,” White said.

“Lenders are currently allowing people to

momentarily stop their repayments, and while each situation is

different, they are listening and helping and working with all

borrowers.”

According to White, brokers are ideally positioned to have the most impact on and support damaged communities.

“Chances are the bank won’t come knocking

on our clients’ doors because they don’t know who is being impacted and

who isn’t, but we can knock on those doors,” he said.

“Finance brokers are part of local

communities and we know many of our clients and their families

personally, so this is a great opportunity for us to serve our clients

and repay the trust they have in us.”

The bushfires raging across Australia are likely to lead to elevated mortgage arrears in the coming months and, if weather-related “peril events” continue to become a more regular occurrence, they could reshape the standard arrears fluctuations expected throughout the year, according to a new report from S&P Global Ratings, via Australian Broker.

“Mortgage arrears typically increase

during the summer period, reflecting the pre- and post-Christmas

spending and extended holiday season, before declining during the second

quarter,” the report reads.

“If the longevity and intensity of

bushfire seasons become a more regular occurrence, arrears could remain

elevated for longer periods in drought-prone areas due to the flow-on

effect of bushfire devastation on local employment conditions.”

Local employment conditions such as

tourism and agriculture are expected to be impacted, causing

debt-serviceability pressures for affected borrowers.

This dynamic will be further compounded in

areas with drought conditions, or where agriculture forms a large part

of local employment, with arrears predicted to remain elevated for an

even longer period of time.

Lenders to borrowers in affected areas

will likely experience an increase in financial hardship claims, which

they are obliged to consider under consumer laws and banking codes.

Possible concessions can include a reduction in the interest rate or

payment, lengthening of loan maturity, or full or partial deferral of

interest for a temporary period.

Comprehensive credit reporting will soon leave unprepared finance providers with unprofitable business models while it spurs those ahead of the curve to further success, says credit and risk consultant Andrew Tierney, via AustralianBroker.

The news that most consumers can now

benefit from comprehensive credit reporting should come as a wake-up

call to finance providers who have yet to embrace the digital era.

All four major banks are now providing

credit bureaux with detailed customer transaction data relating to

credit card usage, personal loans, mortgages and other financial

commitments.

CCR is poised to reshape our industry.

‘Game changer’ may be an overused phrase – but in this case it’s

accurate. For this reason, it surprises me that there are a large number

of credit providers still stuck in the analogue era, who show no signs

of wanting to change. They aren’t benefiting from CCR and don’t seem to

want to.

For example, while talking to a subprime

lender just last week about what he was doing to meet this new

challenge, he said his company already treated all applicants as

subprime, with an interest rate that reflected the level of risk. He

didn’t need transaction data direct from the applicant’s current account

to help him make a decision, so why fix something that had been

generating profits for as long as he could remember?

I can’t imagine how those with this

mindset, determined to carry on as they have done, will still be in

business in 10, maybe even five years’ time.

While many don’t see it at first, there’s

eventually a light-bulb moment that arrives once you spell out how CCR

is going to impact their business.

For the lender I mentioned, all it took

was me pointing out that legislation requires lenders to use all the

tools available to understand the risk a loan presents to the client.

Without tapping into CCR, is he really doing this?

What defence will he have for not

utilising CCR when the regulator comes knocking on his door? Cost isn’t a

factor. There is no need for any major investment in back-office

infrastructure or IT when you can tap into CCR and open data at little

cost via platforms provided by tech companies.

Was he prepared for legal action that he could face, as a result of not fully checking affordability?

Further, there is the risk exposure that

comes from not knowing the size that your liability could be in the

future. As we all know, the regulator has been moving the due diligence

goalposts for us.

By the end of our talk, the time

investment he was willing to devote to this had grown exponentially.

Now, he is days away from taking full advantage of CCR.

However, CCR should not be viewed simply as a big stick when it poses many more business benefits.

As recently calculated by Kevin James at

Equifax, $20bn in extra loans could be granted to consumers over just

one year by giving lenders granular detail on customers’ debt and

repayment habits. The real-time transaction history at the point of

application gives lenders the data needed to allow loans that previously

would have been turned down.

Suddenly, a slice of business that

used consultantto be a ‘no’ could become a ‘maybe’, then a ‘yes’.

Because this decision will be largely automated, it will be possible to

use true risk-based pricing for the first time, with loan terms designed

specifically for a borrower.

Those that lag in this business are undoubtedly going to be left behind.

It won’t be long before they see a change

in demographic in their pipeline. The profile of hopeful borrowers they

are used to dealing with will change, as previous ‘nos’ find they can go

to more mainstream sources and become ‘yeses’. Why would borrowers be

willing to pay a higher rate of interest when they can get a lower one

that is specifically tailored to their situation?

Finance providers who stubbornly remain

behind the times may also find the likely ‘nos’ will begin to target

firms that do not use CCR or open data, because they know their

transaction data will not stand up to the same level of scrutiny and

they are more likely to sneak by to approval.

Those who do not embrace these changes are

going to have the rug pulled out from underneath them in the

not-too-distant future. Their business model that has always been

profitable could lose its edge overnight.

If doubt remains, remember that none of us

need to think very hard to come up with examples of analogue businesses

that have long been left behind.

The 2019 Consumer Pulse Report from financial comparison site Canstar surveyed over 2,000 Australians to get insight into current trends and how they’re likely to play out into the future. Via Australian Broker.

According to the data, less Australians

are worried about mortgage interest rate movements than in years

previous. Just 7% named it as their biggest financial concern for the

year ahead in 2019 as compared to 9% last year.

However, concern over debt as a whole has

risen, with 7% naming mounting debt levels as their leading concern for

the year ahead as compared to 5% in 2018.

Just over a quarter (26%) of Australians

reported they spend more than they earn, don’t save regularly and don’t

limit their debts. The average debt outside of property loans rests at

$48,809.

The respondents communicated credit cards

are their biggest downfall, giving way to “accidental debt” through

spending rather than the considered decision of taking out a loan and,

without the discipline of a fixed repayment plan, it tends to linger

longer.

Of those surveyed, 67% said their debt is

in the form of a credit card, 17% a car loan, 16% a personal loan, 10%

buy now pay later, and 20% other.

Nearly half (43%) of those with debt say they think about it on a daily basis.

Nearly a quarter (24%) doesn’t have any

savings at all – the same percentage as in 2018, showing a lack of

improvement in savings habits. Of those not saving, close to three

quarters (74%) indicated they live pay cheque to pay cheque.

Younger generations continue to live at

home longer while they save for their financial goals, be it a holiday, a

car or a home, with respondents saying adult children should move out

by the age of 34.

Home loan repayments as a percentage of

the average income are now at a similar level as they were before the

Global Financial Crisis (GFC); however, the RBA cash rate is

approximately one-tenth of the pre-GFC cash rate, meaning repayments

have been reduced.

Canstar expects worry to intensify when interest rates start to rise, and says now is the time to be getting a good deal.

AUSTRAC, Australia’s anti money-laundering and terrorism financing regulator, has taken Westpac to court, alleging the major bank violated anti-money laundering and terrorism regulation on over 23 million occasions. Via Australian Broker.

According to AUSTRAC CEO Nicole Rose, the decision to commence civil

penalty proceedings came on the back of a detailed investigation into

Westpac’s non-compliance.

The regulator has alleged Westpac’s oversight of its program intended

to identify, mitigate and manage money laundering and terrorism

financing risks was deficient.

AUSTRAC has found the failures led to “serious and systemic non-compliance” with the AML/CTF Act.

“These AML/CTF laws are in place to protect Australia’s financial

system, businesses and the community from criminal exploitation. Serious

and systemic non-compliance leaves our financial system open to being

exploited by criminals,” said Rose.

“The failure to pass on information about IFTIs to AUSTRAC undermines

the integrity of Australia’s financial system and hinders AUSTRAC’s

ability to track down the origins of financial transactions, when

required to support police investigations.”

Westpac allegedly failed to:

Appropriately assess and monitor the ongoing money laundering and

terrorism financing risks associated with the movement of money into and

out of Australia through correspondent banking relationships

Report over 19.5m International Funds Transfer Instructions to

AUSTRAC over nearly five years for transfers both into and out of

Australia

Pass on information about the source of funds to other banks in the

transfer chain, depriving them of information needed to manage their

own AML/CTF risks

Keep records relating to the origin of some of these international funds transfers

Carry out appropriate customer due diligence on transactions to the

Philippines and South East Asia that have known financial indicators

relating to potential child exploitation risks

AUSTRAC aims to build resilience in the financial system and ensure

the financial services sector understands, and is able to meet,

compliance and reporting obligations.

“We have been, and will continue to work with Westpac during these

proceedings to strengthen their AML/CTF processes and frameworks,” Rose

said.

“Westpac disclosed issues with its IFTI reporting, has cooperated

with AUSTRAC’s investigation and has commenced the process of uplifting

its AML/CTF controls.”

Westpac is a member of the Fintel Alliance, a private-public

partnership established by AUSTRAC to tackle serious financial crime,

including money laundering and terrorism financing.

Yesterday, the government announced the ACCC will be conducting an inquiry into home loan pricing, investigating how lenders set their rates, why they often fail to pass through RBA rate cuts to borrowers in full, and the barriers that may be preventing consumers from switching to cheaper options on the market. Via AustralianBroker.

Over the course of the day, key industry players publicly responded

to the news, some welcoming the development, while the major banks

seemed to imply the key concerns listed were a matter of

miscommunication rather than misbehaviour.

FBAA

The Finance Brokers Association of Australia (FBAA) welcomed the announcement of an inquiry, with managing director Peter White dubbing the examination of the banking sector “appropriate.”

“I’ve been calling on the banks for a long time to pass on interest rate cuts in full,” White said.

“The banks have been playing some sort of seesaw game where they will

pass on a little bit this time and then a bit more – or a bit less –

the next time.

“There’s a pattern of behaviour here that Australians are clearly not happy with.”

White rejected the banks’ claims the partial rate pass throughs have been due to increasing costs.

“The banks are being hit with penalties for breaches uncovered through the royal commission, and through investigations by the Banking Executive Accountability Regime (BEAR).

“Trying to balance the books by passing on these penalties is not something that should be borne by borrowers.

“This inquiry provides an opportunity for banks to be transparent

around their decision making and how they balance the needs of the

community.”

COBA

The Customer Owned Banking Association (COBA) also welcomed news of

the inquiry, particularly singling out the investigation into what

prevents more consumers from switching banks when they may find a better

deal elsewhere.

Further, the association expressed optimism the inquiry with generate “creative new ways to unleash consumer power.”

“Empowering consumers to switch their banking and to shop around is

an unambiguously good thing,” said COBA director of strategy Sally

Mackenzie.

“A more competitive market will make all players care more about

their customers, and the market will function more effectively if there

is more intense competition for borrowers.

According to Mackenzie, it’s up to the policymakers to enable consumers to drive this market-wide competition.

ANZ

In its response, ANZ asserted the issues raised in the ACCC inquiry

launch stem from a shared misperception held among consumers.

“Despite intense competition, there is cynicism in the broader

community about interest rates for home loans,” said ANZ CEO Shayne

Elliott.

“We know we have not done a good job in explaining our position and

we will be working hard to ensure this process delivers results.

“The inquiry is a good opportunity to provide facts in what is a

complex space and we hope it will provide the public with renewed

confidence in the way their home loans are priced.”

Westpac

Westpac took a similar stance to ANZ, but went yet further, directly

defending its prioritisation of protecting its margins and making a

reasonable profit.

“The inquiry is an important opportunity to put the facts on the

table around mortgage pricing,” said Westpac Group CEO Brian Hartzer.

“Pricing decisions require banks to take into account a number of

factors, particularly as the cash rate heads towards zero. In particular

we have to manage the net interest margin – that is the difference

between deposit and lending rates. As part of this process we take into

account the interest of borrowers, depositors and shareholders who

provide the equity that enables us to operate.

“Banks also need to make a reasonable level of return. This not only

supports shareholder investment it also underpins prudential stability,

and our debt rating. The level of profit also needs to be considered in

relation to the size of our balance sheet which is $850bn. In fact our

profitability in terms of ROE has more than halved over the last 15

years.

“Westpac must also retain its double AA rating. This rating allows

the bank to import funding at more reasonable cost from international

investors. To lose it would increase the cost of our wholesale funding

which would inevitably lead to higher interest rates for our borrowers.”

NAB

NAB acknowledged the launch, but did so in a noncommittal manner.

Chief customer officer for consumer banking, Mike Baird said, “This

is an important opportunity to discuss the challenges of an increasingly

low interest rate environment and engage in a broader discussion about

how we support all our customers – both depositors and borrowers.”

The commentary did not extend further, aside from a list of “fast

facts” tagged onto the end, including that NAB currently has the lowest

Standard Variable Rate of the majors, has gotten rid of over 100 fees

from its products and services, and offers a special fixed rate of 2.88%

for two years for first home owners – seeming to imply the bank has

already done a great deal in making itself more hospitable for

customers.

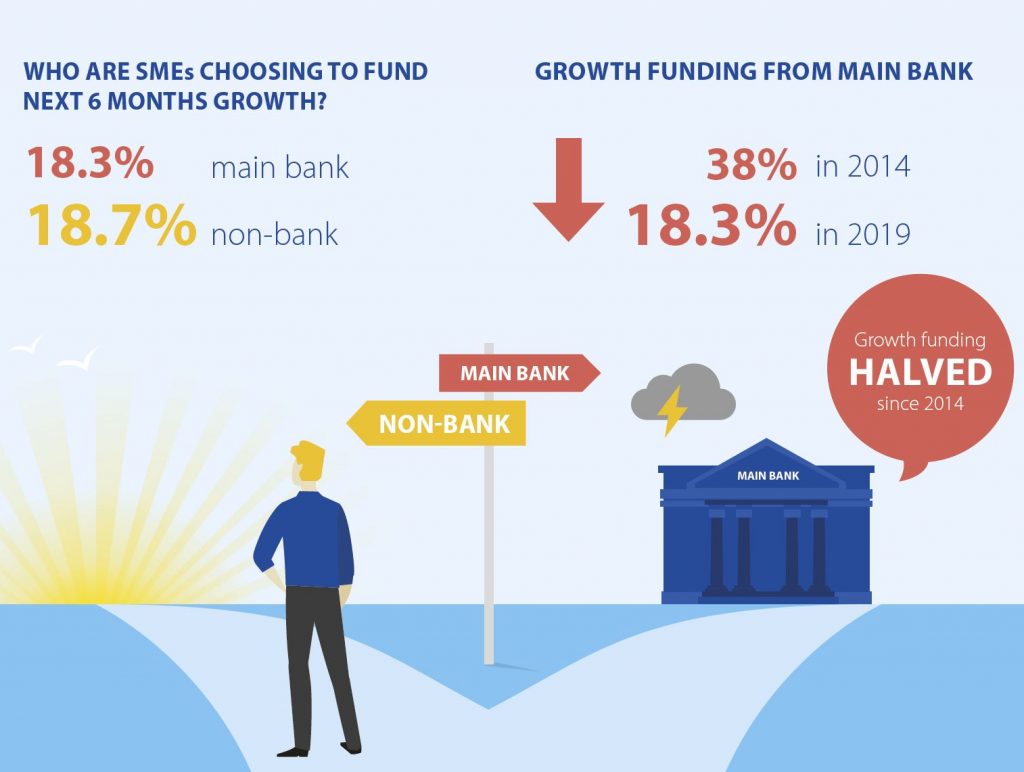

A new trend has emerged in the SME lending space, with Australian small businesses more likely to use a non-bank to fund growth rather than their main bank, according to a national survey, via Australian Broker.

Small business owners’ reliance on non-banks is the highest it’s ever been, with 18.7% of SMEs planning to fund revenue growth with such a lender, as charted in the September 2019 SME Growth Index commissioned by Scottish Pacific and drawing data from over 1,000 businesses.

Conversely, business owners planning to fund their growth via their

main bank has halved, dropping from 38% in the first year of reporting

in 2014 to 18.3% in the most recent data.

The main reason given for turning away from banks, cited by 21.3% of the SMEs, was avoiding having to use property as security against new or refinanced loans, up from 18.7% in September 2018.

Other considerations contributing to the gravitation towards

non-banks included reduced compliance paperwork (19.8%), short

application times (17.1%), royal commission disclosures (8.8%) and

banks’ credit appetite (6.9%).

Of the SME owners relying on non-bank funding, 77% utilise invoice

finance, 23% merchant cash advances, 10% peer to peer lending, 9%

crowdfunding and 5% other online lending.

Just 2.6% of those surveyed indicated they would not consider using a non-bank lender – down from 4.0% last year.

“[However], the SME sector still has a long way to go in taking

advantage of the alternatives available to them,” said Peter Langham,

Scottish Pacific CEO.

“Some business owners remain unaware of funding alternatives. [They]

are aware of non-bank funding, but don’t fully understand how it works.

“They are too busy to research it, so put this in the ‘too hard’

basket. When they can’t secure bank funding, they just tip their own

money in to fund growth.”

For growth SMEs, almost twice as many as in H1 2018 say their cash flow is worse or significantly worse (21.2%, up from 12.3%). At the same time, non-growth SMEs reporting worsening cash flow has increased to 17.6%, up from 10% in H1 2018.

According to the survey, 83% of business owners plan to stimulate revenue growth with their own funds.