Economist John Adams and I discuss the latest of the question on deposit account “Bail-In” and try to answer John’s question “Is Parliament “Too Stupid to be Stupid”?

Either way, the question of deposit bail-in remains unclear in our view.

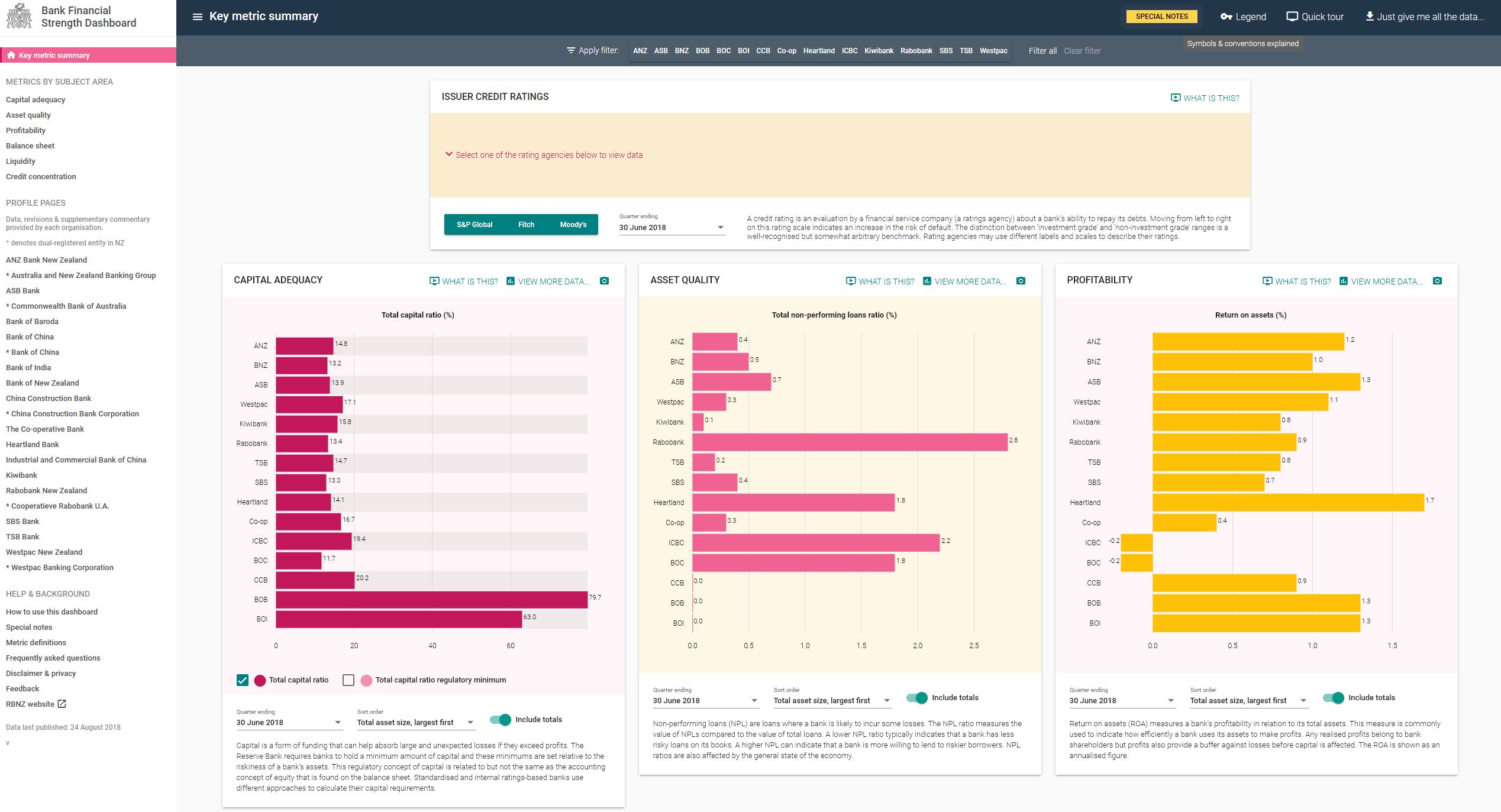

We also discuss the Reserve Bank of New Zealand Dashboard which is designed to assist Kiwi’s as they try to pick which bank to place their deposits with. In New Zealand it is QUITE CLEAR, bank deposits are available for “Bail-In”!

The IMF has published an excellent piece on their blog, which sharply defines the issues around bank bail-out and bail-in should a bank fail.

The trouble is the “bail-in” route which they define as targetting “Sophisticated Investors” such as super funds, effectively means a indirect risk to households who save via their superannuation, and of course there is the risk that even deposits could be grabbed as is explicitly stated in New Zealand.

The IMF argues that the risk of bail-in means prospective investors should see a premium to cover the risk, in the returns they get from their investments. But it seems to me in an attempt to deflect risks away from governments being forced to bail-out a bank, once again the end user of financial services products are effectively taking the risks, and creating a moral hazard, where banks and governments can pass the buck.

Watch my previous video:

During the global financial crisis, policymakers faced a steep trade-off in handling bank failures. Using public funds to rescue failing banks (bail-outs) could weaken market discipline and lead to excessive risk taking—the moral hazard effect.

Letting private investors absorb the losses (bail-ins) could destabilize the financial sector and the economy as a whole—the spillover effect. In most cases, banks were bailed out.

This created public resentment and prompted policymakers to introduce measures to shift the burden of bank resolution away from taxpayers to private investors.

Resolving a failing bank should rely on bail-ins: private stakeholders should bear the losses.

Our recent study, also featured in an Analytical Corner in the 2018 Spring Meetings, looks at the question of what to do when a bank fails.

We advocate a resolution framework that carefully balances the moral hazard and spillover effects and improves the trade-off. Such a framework would make bail-outs the exception rather than the rule.

Balancing moral hazard and spillover effects

Not all crises are alike. Some are isolated, with little or no spillover effect. In those cases, bail-outs would merely create moral hazard. Resolving a failing bank should rely on bail-ins: private stakeholders should bear the losses.

Other crises are systemic, and affect all corners of an economy or many countries at the same time.

The destabilizing spillovers associated with bank failures in such a situation would justify the use of public resources: moral hazard still exists but is bearable compared to the alternative of a severe crisis that hurts all, including those without a stake in the troubled bank.

So, the framework should commit to using bail-ins in most cases and allow use of public funds only when the risks to macro-financial stability from bail-ins are exceptionally severe.

Improving the trade-off

The best way to avoid such dilemmas is to reduce spillovers and the need for bail-outs in the first place. This can be achieved through two mutually re-enforcing mechanisms.

The first mechanism is reducing the likelihood of crises and minimizing costs should a crisis occur. This translates into having a more resilient banking system: less leverage and risk taking, and more capital and liquidity. Then the odds that a bank runs into trouble are smaller. And, if there is trouble, banks can absorb the losses without help from the government.

The second mechanism is making the bail-in option viable. The problem is that policymakers may make the promise to bail in a troubled bank but, in a crisis, they will be tempted to bail them out. So people will not believe that bail-ins will happen and continue to expect bail-outs.

This is the worst of both worlds, because it has spillover and moral hazard effects.

How do policymakers make a credible commitment that there really will be bail-ins?

First, ensure that banks have enough buffers to absorb losses and clarify upfront which investor claims (such as bonds and deposits) will in the event of failure be written down and in what order. Second, only allow sophisticated investors who can understand and absorb the losses to hold these bail-in-able claims. Third, improve systemic banks’ resolvability by periodic assessments, living wills that spell out how the bank will be resolved, and domestic and cross-border drills to assess the impact of a threat.

Turning to the other side of the trade-off, how do we limit moral hazard?

First, credibly commit to using bail-outs only in exceptional cases and on a temporary basis with a clear exit plan. Second, use public funds only after those that can absorb the losses have been bailed in. Third, recover these bail-out funds after the storm has passed and ensure that all is executed in a transparent, accountable manner.

The way forward

Reforms since the crisis have improved the trade-off by seeking to make bail-ins a credible option and to make bail-outs less likely.

New frameworks—such as those in the United States and the European Union—introduce comprehensive powers to resolve banks, including through bail-ins. These measures also seek to contain spillovers from bail-ins by ensuring that banks have adequate buffers to absorb losses, and aim to make them more resolvable via effective resolution planning.

We support the ongoing reform agenda and stress that resolution frameworks should minimize moral hazard. That said, we also emphasize the need to allow for sufficient, albeit constrained, flexibility to be able to use public resources in systemic crises—when spillovers are deemed likely to severely jeopardize macro-financial stability.

Proposed amendments to the EU Bank Recovery and Resolution Directive (BRRD) regarding minimum levels of bail-inable subordinated debt may make it harder to effect a bail-in resolution on mid-sized banks that run into trouble, Fitch Ratings says.

Minimum subordinated debt requirements may only apply to global systemically important banks (G-SIBs) and “top-tier” banks with assets above EUR100 billion, according to a draft paper to be discussed at a European Council meeting on Friday.

This EUR100 billion threshold to designate a top-tier bank would be at the top of the range previously proposed, and could make it more difficult to apply bail-in to mid-sized banks under the EU’s bail-in framework. This may be because of legal challenges from bondholders that are bailed in if equally ranking creditors (eg junior depositors) are not or because of financial stability risks of bailing in equally ranking retail bondholders and junior depositors alongside institutional bondholders.

The EUR100 billion cut-off is particularly relevant to markets with less concentrated banking systems, for example Italy and Spain, and to smaller EU countries. For banks below the threshold, it could be challenging and costly to issue large amounts of subordinated debt, particularly for smaller banks with a more limited footprint in the debt capital markets. Consequently, mid-sized bank senior creditors may miss out on the protection the subordinated buffers would have provided.

How widely minimum subordination requirements should apply has been a matter of contention. Some northern EU member states want a broader scope covering at least all of the “other systemically important institutions” (O-SIIs), to minimise contagion risk. Others, mainly southern EU member states, want to limit the application to avoid forcing any but the largest banks to build subordinated debt buffers. An amendment originally proposed by Belgian delegates provides resolution authorities with the option to request subordinated minimum required eligible liabilities and own funds (MREL) for banks deemed systemic – but this is not automatic, as it is for the top-tier banks and GSIBs.

The European Council’s draft BRRD paper also proposes capping for most banks the requirement for subordinated MREL at 8% of a bank’s total liabilities and own funds. This would limit the associated costs for banks, but would leave their senior creditors less well protected in the event of outsized losses.

Friday’s discussions will also seek to agree a timescale for banks to meet the new requirements. The draft proposes G-SIBs and top-tier banks will have until January 2022. Other banks subject to the requirements will be given until 1 January 2024, but some EU member states are seeking longer timescales as some banks may struggle to build buffers, particularly if they are deposit-funded and have not issued subordinated debt previously.

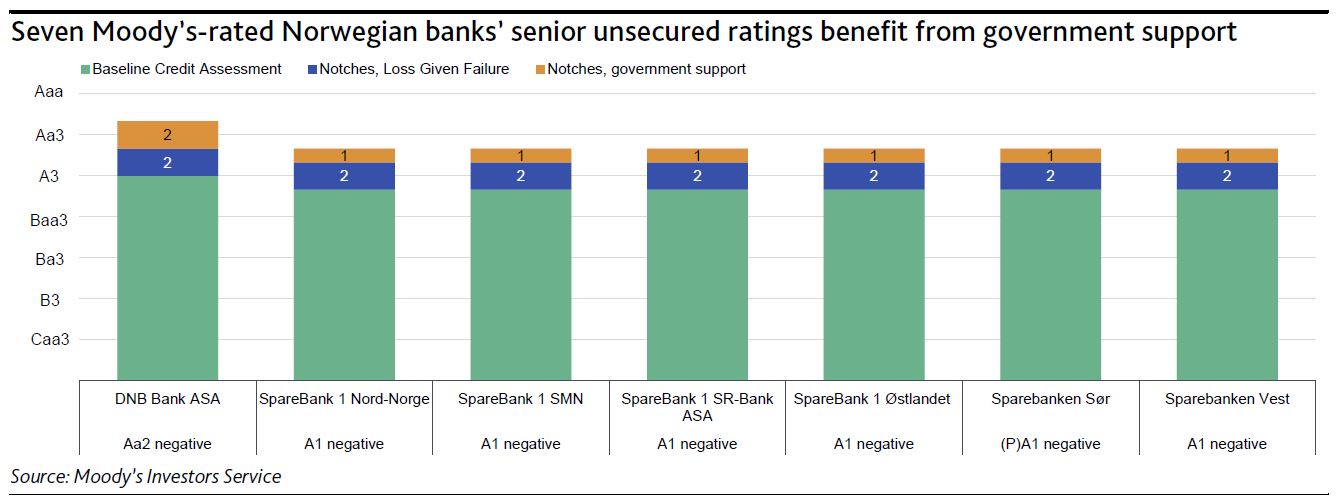

Last Tuesday, Norway’s parliament began debating proposed legislation to implement the Bank Recovery and Resolution Directive (BRRD) and an amended deposit guarantee scheme.

The intention of the BRRD law is to promote financial stability and ensure that losses are borne by a bank’s shareholders and creditors rather thantaxpayers. Although the first reading in parliament concluded with a unanimous vote in favour for the proposal, a second reading (at least three days after the initial reading) is required before the bill can be transposed into Norwegian law. The BRRD law’s enactment, which we expect within the next few weeks, would be credit negative for seven of the 17 Norwegian banks we rate because it would reduce the probability that they would receive government support in case of need.

In line with the European Union’s (EU) BRRD, the proposed legal framework features recovery and resolution plans for banks, early intervention measures and resolution tools including the bail-in of creditors. Additionally, the proposal includes small changes to the current deposit guarantee scheme to align it with that of the EU. However, in contrast to the EU’s deposit guarantee scheme limit of €100,000 per depositor per bank, the Norwegian Ministry of Finance has proposed maintaining its current coverage of NOK2 million (approximately €200,000) per depositor in each bank.

The bail-in tool is a central feature in the BRRD framework, intended to reduce the need for government intervention in failing banks. Consequently, government support is less likely for Norwegian banks since bail-in can be used to recapitalise financial institutions and absorb losses.

We assigned negative outlooks to those banks’ ratings following the submission of the legislative proposal in June 2017 in anticipation of the law’s passage, and the eventual moderation of our government support assumptions, which likely will lead us to remove the one-notch rating uplift incorporated into the banks’ ratings.

We expect Norway’s implementation of BRRD to be followed by a minimum requirement for own funds and liabilities (MREL) for each bank within the next 12 months. Nevertheless, no relevant details have been disclosed yet, although the BRRD proposal includes MREL requirements in line with the EU’s BRRD.

We expect Norwegian banks that will be subject to MREL requirements to gradually change their funding plans by raising non-preferred senior debt instruments in order to be compliant. This likely will provide senior unsecured creditors additional protection against potential losses, which eventually could counterbalance the negative rating effect on banks from revised government support assumptions.

Let’s talk about the bank bail-in conundrum. A couple of weeks back I discussed whether bank deposits in Australia would be safe in a crisis. The video received more than 1,400 views so far, and has prompted a number of important questions from viewers. So today I update the story, and addresses some of the questions raised. The bottom line though is I think we are being sold a pup, which by the way refers to a confidence trick originating in the Late Middle Ages!

Watch the video, or read the transcript.

First, a quick recap, for those who missed the first video. Officially, in Australia currently bank deposits are protected up to $250,000 per person by a Government Guarantee – The Financial Claims Scheme. For banks, building societies and credit unions incorporated in Australia, the FCS provides protection to depositors up to $250,000 per account-holder per ADI according to APRA. Only deposit products provided by ADIs supervised by APRA were eligible to be covered. Amounts between $250,000 and $1 million are not be covered under the Guarantee Scheme. Above $1m banks can elect to pay a fee to the Government for this for protection, but none do. However, as we will see there are even questions about the sub $250k. But note this, the FCS can only be activated by the Australian Government, whilst APRA is responsible for administering the Scheme.

The RBA says upon its activation, APRA aims to make payments to account-holders up to the level of the cap as quickly as possible – generally within seven days of the date on which the FCS is activated. The method of payout to depositors will depend on the circumstances of the failed ADI and APRA’s assessment of the cost-effectiveness of each option. Payment options include cheques drawn on the RBA, electronic transfer to a nominated account at another ADI, transfer of funds into a new account created by APRA at another ADI, and various modes of cash payments.

The amount paid out under the FCS, and expenses incurred by APRA in connection with the FCS, would then be recovered via a priority claim of the Government against the assets of the ADI in the liquidation process. If the amount realised is insufficient, the Government can recover the shortfall through a levy on the ADI industry. Ok, maybe in the case of a single failure

Now, since the Global Financial Crisis, regulators have been working on ways to avoid a tax payer based rescue in a crash, because for example, the UK’s Royal Bank of Scotland was nationalised in 2007. This cost tax payers dear, so regulators want measures put in place to try to manage a more orderly transition when a bank gets into difficulty.

The New Zealand the Open Bank Resolution (not to be confused with Open Banking) is the clearest example of a so called bail-in arrangement. Customer’s money, held as savings in a distressed bank can be grabbed to assist in a resolution in a time of crisis. The thinking behind it is simple. Banks need an exit strategy in case of a problem, and Government bail-outs should not be an option. So a manager can be appointed to manage through the crisis. They can use bank capital, other instruments, like hybrid bonds and deposits to create a bail-in. This approach to rescuing a financial institution on the brink of failure makes its creditors and depositors take a loss on their holdings. This is the opposite of a bail-out, which involves the rescue of a financial institution by external parties, typically governments using taxpayer’s money.

So what about Australia? Well, the Financial Sector Legislation Amendment (Crisis Resolution Powers and Other Measures) Bill 2017 is now law, having been through a Senate Inquiry. It all centers on the powers which were to be given to APRA to deal with a banking collapse.

In the bill, there is a phrase “any other instrument” in the list of bail-in items. Treasury said, “the use of the word ‘instrument’ is intended to be wide enough to capture any type of security or debt instrument that could be included within the capital framework in the future. It is not the intention that a bank deposit would be an ‘instrument’ for these purposes”. Yet, deposits were not expressly excluded.

In fact, when the Bill came back to Parliament it went through both houses with minimal discussion (and members on the floor, the chambers were all but empty). And despite a proposal being drafted and with Government Lawyers in parallel to exclude deposits, it was passed on 14th February without this change, leaving the door wide open under “any other instrument”. All the verbal assurances are meaningless.

So, the result appears to be APRA has wider powers now to handle a bank in crisis, and deposits are potentially accessible. They are not expressly excluded, and in a time of crisis, could be bailed-in.

But this is not the end of the story. Treasurer Morrison issued a letter to Liberal government members with some talking points to justify this actions, in response to a wave of protests. But in so doing, he raises more questions.

The first point is that the Deposit Guarantee scheme (the one up to $250k) is not currently active. The Government would need to activate it, and can only do so when an institution fails. This is important because it means that in theory at least, APRA could mount a deposit bail-in before the Government activates the deposit protection scheme. Consider what would happen if many banks all got into difficulty at the same time, as could be the case in a wider banking crisis – after all, they all have similar banking models.

The second point is that the Treasurer makes reference to the 1959 Banking Act, and says that depositors have a claim above other creditors in a bank failure. But in fact the 1959 Act says depositors do indeed rank ahead of other unsecured creditors, but that means the secured creditors come first. So would anything be left in case of a bank failure given the massive exposure to property?

Next, the letter says APRA has now enhanced powers to protect the interests of depositors – not deposits. And looking at the New Zealand situation the bail-in provisions there are framed to do just this, by utilising deposits to help keep the bank afloat, thus protecting depositors. The Reserve Bank of New Zealand says this is IN THE INTERESTS OF DEPOSITORS.

Oh, and finally, Morrison says the way the Bill went into Law was quite normal by being listed in the Senate Order of Business, meaning members had the opportunity to debate the bill if they had wanted to. In fact, only seven Senators were there despite really needing a quorum of 19, but there is a get out in that a quorum is only needed if a division was called, and in this case it was simply nodded through. Democracy in action.

So there you have it. No Deposit Protection currently exists. Its limited to $250k per person if activated by the Government, at their discretion, and the legalisation leaves the door wide open for a New Zealand style of Bail-In. Not a good look.

So what should Savers do? Well, this is not financial advice, but the New Zealand view is that savers should make a risk assessment of banks and select where to deposit funds accordingly. But I am not sure how you do that, given the current low level of disclosures. APRA releases mainly aggregate data and protects the confidentially of individual banks as they are required to do under the APRA act.

Next, do not assume deposits are risk free, they are not. This means lenders should be offering rates of return more reflective of the risks we are taking, currently they are not (in fact deposit rates are sliding, as banks seek to repair margins). You might consider spreading the risks across multiple institutions

Consider alternative savings options (which are limited). Clearly, property, stocks and shares and even crypto currencies are all risky – there are no safe harbours. I guess there is always the mattress.

One other point to make. Several people are calling a bill to bring a Glass-Steagall split between core banking operations and the speculative aspects of banking. Glass-Steagall was enacted in the US in 1933 after the great crash, separating commercial and investment banking and preventing securities firms and investment banks from taking deposits. But in 1999 the US Congress passed the Gramm–Leach–Bliley Act, also known as the Financial Services Modernization Act, to repeal them. Eight days later, President Bill Clinton signed it into law. Following the financial crisis of 2007-2008, legislators unsuccessfully tried to reinstate Glass–Steagall Sections 20 and 32 as part of the Dodd–Frank Wall Street Reform and Consumer Protection Act. Both in the United States and elsewhere, banking reforms have been proposed that refer to Glass–Steagall principles. These proposals include issues of “ring fencing” commercial banking operations and narrow banking proposals that would sharply reduce the permitted activities of commercial banks.

The point of the bill was to isolate the risky bank behaviour, relating to derivatives and trading from core banking activities. In the case of a banking crisis, triggered by a collapse in the financial markets such an arrangement would protect the operations of the core banking. We got a glimpse of that a month ago when US trading volatility shot through the roof.

But, in Australia, the bulk of the risks in the banking system comes not from the derivatives side of the business, but the massive exposure to household debt and the property sector, and the risky loans they have made. We discussed this on the ABC yesterday. More than 60% of all banking assets are aligned with home lending, plus more relating to commercial property. Thus I do not believe a Glass-Stegall type separation would help to mitigate risks to the banking sector here much at all.

Better to push for a definitive change to the APRA Bill and get deposits excluded from the risk of bail-in. Or place a levy on all banks to directly protect depositors as has been put in place in Germany, where a dedicated government entity has been created for just this purpose.

What I find remarkable is that following loose banking regulation for years, during which the banks have returned massive profits to shareholders, and ramped up their risks, depositors are being lined up by the Government to bail out a failing bank. This is simply wrong.