Please consider supporting our work via Patreon

Please share this post to help to spread the word about the state of things….

/

RSS Feed

Digital Finance Analytics (DFA) Blog

"Intelligent Insight"

We look at the Productivity Commission commentary on home loan rates and disclosure.

Please consider supporting our work via Patreon

Please share this post to help to spread the word about the state of things….

In ASIC’s post-draft submission to the Productivity Commission’s Inquiry into competition in the Australian financial system, the corporate regulator said it “support[ed] the Productivity Commission’s recognition of the importance of ASIC having a broad, proactive competition mandate”.

“An explicit and broad competition mandate for ASIC would ensure we have a clear basis to consider and promote competition in the financial system,” ASIC’s submission report said.

A broad mandate would allow competition to be factored into ASIC’s regulatory decision-making, as well as the capability to “address market failure as a driver of misconduct or poor consumer outcomes”.

ASIC also acknowledged previous instances of “uncertainty” regarding “if and how ASIC could consider competition factors”, but pushed back against the idea of actually regulating competition.

“Having a broad competition mandate – to ensure we can appropriately incorporate competition considerations into our existing role as a market conduct regulator – would not make ASIC a competition regulator,” the submission report said.

“We would not have a role in enforcing competition laws – for example, regulating corporate transactions from a competition perspective or monopolies, bringing abuse of market power cases, or regulating pricing and access regimes.”

The regulator added that it supported the co-operation of different regulators in tackling competition issues and the value of learning from each other.

However, ASIC pointed out that each regulator had its own specified area of expertise and “therefore best placed to assess how competition should be weighed and balanced within its area”.

“While we appreciate the Productivity Commission’s concern to ensure that all regulators give appropriate consideration to the competition impacts of their decisions, we are not sure that the role of the competition champion, as envisioned in the draft report, is necessarily the best option to achieve that goal,” the submission report said.

Furthermore, ASIC highlighted the “significant role” of the Australian Competition and Consumer Commission as a regulator of competition “for the entire economy”, as well as its role as a “competition advocate”.

“We acknowledge and support the ACCC’s establishment of its Financial Services Unit, and the role it plays in the financial sector,” the submission report said.

“ASIC maintains a strong working relationship with the ACCC, and welcomes the ACCC’s views and input, including in our work to encourage positive consumer outcomes through effective competition.”

Rod Sims, Chairman ACCC spoke at the AFR Banking and Wealth Summit “Synchronised swimming versus competition in banking”. His excellent speech is worth reading in full. Net, net, the tempo for reform just got stronger still….

He discussed the results of their recent investigation into mortgage pricing, and also discussed the broader issues of competition versus financial stability in banking. He warns that the industry should be aware of, and respond to, the fact that the drive for consumers to get a better deal out of banking is shared by many beyond the ACCC. Every household in Australia is watching.

He discussed the results of their recent investigation into mortgage pricing, and also discussed the broader issues of competition versus financial stability in banking. He warns that the industry should be aware of, and respond to, the fact that the drive for consumers to get a better deal out of banking is shared by many beyond the ACCC. Every household in Australia is watching.

He specifically called out a lack of vigorous mortgage price competition between the five big Banks, hence “synchronised swimming”. Indeed, he says discounting is not synonymous with vigorous price competition. They saw evidence of communications “referring to the need to avoid disrupting mutually beneficial pricing outcomes”.

He also said residential mortgages and personal banking more generally make one of the strongest cases for data portability and data access by customers to overcome the inertia of changing lenders.

Finally, on competition. he says if we continue to insulate our major banks from the consequences of their poor decisions, we risk stifling the cultural change many say is needed within our major banks to put the needs of their customers first. Vigorous competition is a powerful mechanism for driving improved efficiency, and also for driving improved price and service offerings to customers. It can in fact lead to better stability outcomes.

This puts the ACCC at odds with APRA who recent again stated their preference for financial stability over competition – yet in fact these two elements are not necessarily polar opposites!

As the economy-wide competition and consumer regulator, the ACCC has always had a role in the banking sector. It is fair to say, however, that our role has been reactive to date, focusing on pursuing breaches of the Competition and Consumer Act 2010.

For example, following an ACCC investigation the Federal Court, 16 months ago, imposed a penalty of $9 million against ANZ and $6 million against Macquarie for attempted cartel conduct.

We’ve also always had a role in considering mergers in the banking sector.

But following the Treasurer’s 2017/18 Budget announcement, the ACCC now has a proactive role in the financial services sector. We have established a permanent team within the ACCC, the Financial Services Unit (FSU), to investigate competition in our banking and financial system.

The FSU was originally a recommendation of the Coleman Committee Review of the Four Major Banks in November 20161, which said:

… the Australian Competition and Consumer Commission… [should] establish a small team to make recommendations to the Treasurer every six months to improve competition in the banking sector.

If the relevant body does not have any recommendations in a given period, it should explain why it believes that no changes to current policy settings are required.

The FSU will undertake regular inquiries into specific financial service competition issues, and so facilitate greater competition in the sector.

The first task of the FSU is the current Residential Mortgage Price Inquiry; the interim report was released on 15 March.

In addition, the Government has recently announced that the ACCC will be the lead regulator for the consumer data right, with banking being the first sector covered.

Clearly our role in the financial sector will be more active than it has been in the past.

Today I will cover three topics.

- The findings from the interim report from our Residential Mortgage Price Inquiry

- Data as a competition driver, and

- Stability and competition; the topic we avoid but must talk about.

1. Residential mortgage price inquiry findings

Our interim report indicates quite clearly, based on evidence we have collected, that not only does competition in the banking sector need to improve, but that where there appears to be competition it may often be illusory.

A number of issues were raised in the interim report; today I will concentrate on three:

- The transparency of interest rates

- The treatment of loyal customers compared to new customers

- Why discounts do not indicate vigorous competition.

The transparency of rates: apples and oranges

It is the nature of competition that similar goods can be compared; you need to be able to compare apples with apples.

It is the nature of residential mortgage products, however, that no two apples are alike (See chart 1).

Chart 1: Total variable residential mortgage book by size of discounts – 30 June 2017

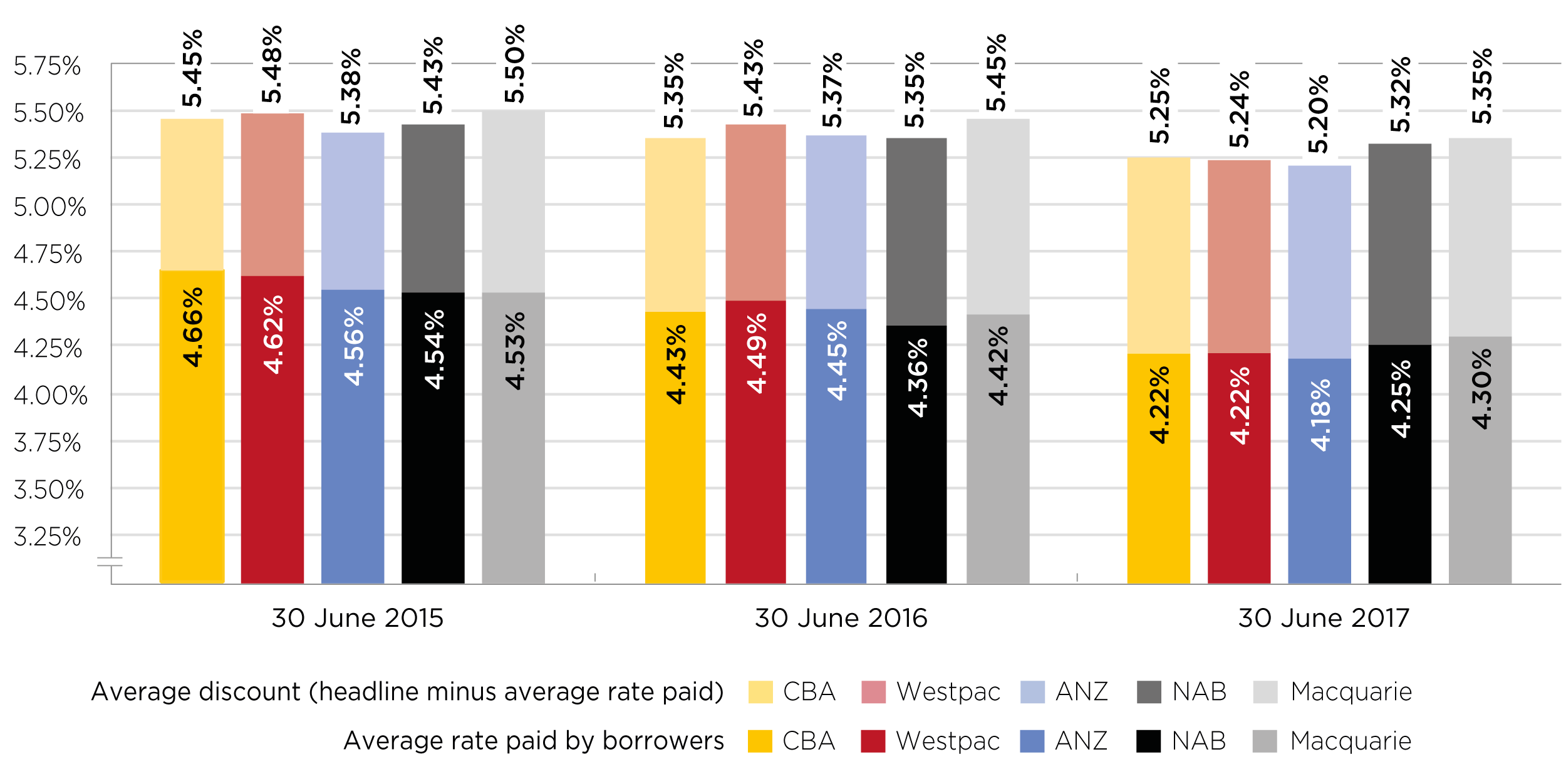

The headline price is a starting price which may then vary by as much as 78–139 basis points below the applicable headline interest rate.

Over the life of an average loan, and this is crucial, we are talking about discounts which amount to life-changing amounts of money for average income earners.

These discretionary discounts do give borrowers a better price, but easy comparison is almost impossible.

Lenders determine discretionary discounts against a range of criteria, some of which are opaque to the borrower.

Since the decision criteria for discretionary discounts vary across lenders, borrowers can find it difficult to determine in advance what, if any, discount they may be eligible for.

Further, discretionary discounts may only be applied and known deep in the application process, and borrowers may even be required to lodge a loan application to confirm the discretionary discount available to them.

And to compare one product with another, the whole process needs to be repeated each time.

Borrowers essentially need to go through the time-consuming process of lodging an application with multiple lenders in order to make an informed decision.

These requirements increase the time and effort associated with obtaining accurate interest rate offers, making it difficult for borrowers to determine the range of effective interest rates available to them (see chart 2).

Chart 2: Headline and average interest rates7 paid for standard8 variable interest rate residential mortgages —owner-occupier with principal and interest repayments9

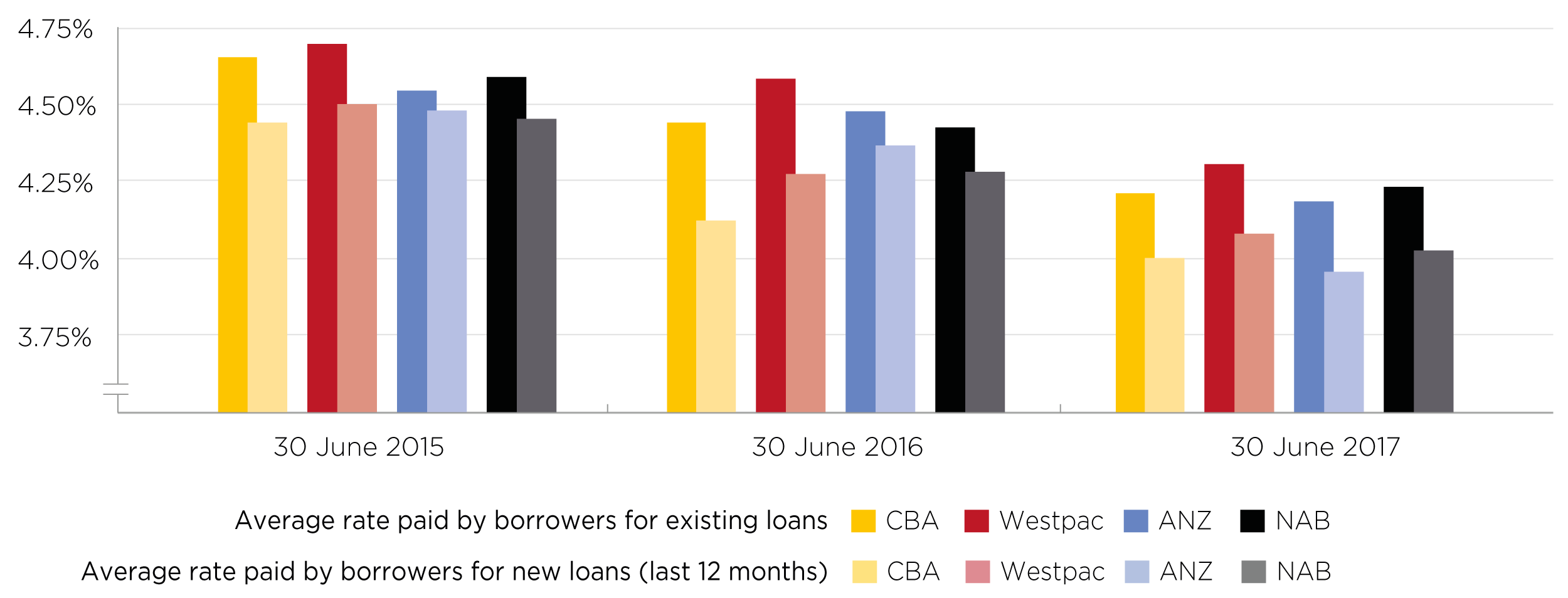

Offers for new customers versus rates available to existing customers

When it comes to residential mortgages, it pays to be a new customer as discounts are a key tool used by residential mortgage lenders to secure new borrowers.

Due to the difficulty of changing your existing loan, existing customers are assumed to be ‘locked in’. For good reason. In most cases, they are.

In recent years, residential mortgage lenders have been increasing the discounts offered to their new borrowers compared to the discounts offered to new borrowers in the past (see chart 3).

This practice has resulted in new residential mortgage borrowers often paying a lower interest rate than existing borrowers.

Based on data supplied by the big four banks for 30 June 2015, 30 June 2016 and 30 June 2017, existing borrowers on standard variable interest rate residential mortgages were paying interest rates up to 32 basis points higher (on average) than new borrowers.

Chart 3: Average interest rates paid on standard10 variable interest rate residential mortgages by new and existing borrowers—owner-occupier with principal and interest repayments

On a $375,000 mortgage, 32 basis points would save approximately $1200 in interest over the first year of a loan alone.

Banks are clearly saying to their customers: “if you want a lower interest rate you will need to keep switching lenders.”

Why discounts do not indicate vigorous competition

In response to the above, the banks and their representatives have said that, in effect, “discounts indicate vigorous competition”.

Discounting is not, however, synonymous with vigorous price competition.

For example, and at its most basic, if a monopolist or oligopolist offers a 10% discount on a price already inflated by market power, we wouldn’t say this is evidence of vigorous price competition.

In residential mortgage lending, “discounts” are a measure of a gap between the actual rate charged by the bank and a reference or headline rate that the bank decided for itself and that almost nobody ever pays.

This tells us very little about the vigour of price competition, particularly if the headline rate provides for a profit margin that is inflated well above what is needed to cover any notion of the risk-adjusted return on capital.

Moreover, the ability of the banks we investigated to selectively offer higher discounts to some types of customer, and maintain lower discounts to others, indicates an ability to refrain from vigorous price competition at least with respect to some types of customers.

Our observation that loyal customers pay higher mortgage interest rates, on average, than new borrowers indicates clearly that loyal customers are not seeing the benefits that vigorous price competition would be expected to provide.

The finding about a lack of vigorous price competition was the focus of most attention when we released our report last month.

Little wonder.

It goes to the heart of the problem in banking and confirms long-held consumer suspicions.

Internal documents reviewed by the ACCC reveal a lack of vigorous price competition between the five Inquiry Banks (ANZ, Commonwealth, NAB, Westpac and Macquarie), and the big four banks in particular. In fact, their behaviour more resembles synchronised swimming than it does vigorous competition.

What we found is that the pricing behaviour of the Inquiry Banks appears more consistent with ‘accommodating’ a shared interest in avoiding the disruption of mutually beneficial pricing outcomes, rather than vying for market share by offering the lowest interest rates.

This manifests in at least four ways:

- The big four banks largely focus on each other when they determine headline interest rates and discounts on variable rate residential mortgages. This means the actions and reactions of over 100 other residential mortgage lenders do not appear to have much bearing on interest rate decisions for the big four banks’ main brands. This is important as the big four represent approximately 80 per cent of all outstanding residential mortgages held by banks in Australia.

- The Inquiry Banks generally have not often sought to compete by offering the lowest headline variable interest rate to borrowers.

- The banks usually move their interest rates at the same time, and in response to RBA changes in the overnight cash rate.

- During late 2016 and early 2017, two of the big four banks (independently of each other) decided to take action to reduce discounting in the market. They each reduced their own discounts and sought to trigger reduced discounting by rivals, even though this was likely to be costly for them if other banks did not follow their lead. We observed that by early 2017 the two banks considered they had been successful in leading competitors to reduce discounts for a time.

These are the observed behaviours.

Then there are the internal communications.

In 2015, for example, we saw references to the need to avoid disrupting mutually beneficial pricing outcomes.

There were also references to “encouraging rational market conduct”, “maintaining orderly market conduct” and maintaining “industry conduct”.

There were also references to a desire to have interest rates that are “mid-ranking”, and to the need not to “lead the market down”.

Comments like these are at odds with banks’ assurances and the reasonable community expectations that competition in the sector is vigorous and effective.

2. Data as competition driver

From a competition perspective, it could be argued that ‘customer stickiness’ is an issue for the customer to resolve.

Fair point. Up to a point.

A study by one Inquiry Bank into customer refinancing requests found that where an existing borrower requests a discount, the Inquiry Bank only needs to come close to the discount requested in order to retain the borrower.

That Inquiry Bank observed in a presentation to its executives in the residential mortgage lending division in June 2015 that “where we allowed repricing to occur, customers are price inelastic when the discount offered is close to their requested discount”.

For this reason, residential mortgages and personal banking more generally make one of the strongest cases I have seen for data portability and data access by customers to overcome the inertia of changing lenders.

As an organisation, the ACCC is more than pleased with Treasury’s Report of the Review into Open Banking and its recommendations as it outlines a framework for a consumer data right.

As the Treasurer noted:

Granting third-party access to a customer’s data will allow rival providers to offer competitive deals, products that are tailored to individual needs, and enhanced services that simplify the choices customers face when accessing banking services.

It should simplify the process of switching between banks and help to overcome the ‘hassle factor’ that sees customers stay with their current bank even in the presence of more competitive deals elsewhere.12

At worst, the ‘hassle factor’ of comparing and switching should be a bug in the system; it shouldn’t be a feature which benefits an industry lacking in vigorous competition.

The Government has announced that the ACCC will be the lead regulator for the consumer data right, with strong support from the Office of the Australian Information Commissioner.

The consumer data right was, of course, the brain child of the Productivity Commission in a report to the Government last year.

The ACCC’s proposed roles include making rules to implement the specifics of the data right, and taking enforcement action to ensure that participants in the new framework meet their obligations.

We are undertaking preparatory work in anticipation of this new role, recognising that formal commencement will be determined once the government has finalised its response to the Open Banking report.

3. Stability versus competition

This is a topic we avoid, but it is one we must talk about.

In recent public statements, particularly in response to the recent Productivity Commission draft report on Competition in the Australian Financial System, senior bank representatives have suggested that prudential regulation and other supportive measures are vital to keep them strong.

They also argue, however, that they are commercial enterprises and as such, must be allowed to pursue an objective of maximising shareholder value.

I believe there is a tension in these two positions that needs to be examined further.

But beyond this tension, we must recognise that the poor performance and failures of banks worldwide, that have often prompted enhanced stability measures, were not caused by excessive competition. Quite the contrary.

Often they appear to have been caused by inappropriate behaviour and endemic short termism, possibly driven by a desire for huge bonuses.

The current Banking Royal Commission is also revealing further failures that cannot be blamed on strong competition.

On the contrary, if we continue to insulate our major banks from the consequences of their poor decisions, we risk stifling the cultural change many say is needed within our major banks to put the needs of their customers first.

There is a, perhaps old fashioned view, that facing strong competition forces firms to increase their focus on customer outcomes.

I think this holds for all sectors of economy, including the banking sector.

Vigorous competition is a powerful mechanism for driving improved efficiency, and also for driving improved price and service offerings to customers.

Culture change to deliver better outcomes for consumers will not occur because the community, regulators or perhaps even some bankers wish it to happen.

Competition is not, repeat not, welcomed by businesses. This is because it delivers better outcomes for consumers. This is exactly what seems to be needed in our banking system.

The ACCC is deeply involved in helping consumers find and achieve lower prices in areas of essential purchases, from electricity to petrol. But most consumers spend significantly more on various financial products, particularly servicing their home mortgage.

Financial stability will be helped by more competition. More importantly, so will consumers.

Conclusion

Ladies and gentlemen, the ACCC’s mandate is to promote competition and fair trading.

It is clear from our interim report into residential mortgage pricing that there are significant issues in the banking sector which raise concerns about competition in the sector as well as fair trading.

Soon after June 30 this year, the ACCC will be releasing its final report into residential mortgages. Our focus will then turn to how best to promote competition in the industry more generally and we will proactively identify issues to examine, particularly leveraging off the work of the Productivity Commission.

Australia’s most recognised regional banks have called on a major competition inquiry to level the playing field and put consumers and the economy first.

In a joint submission lodged with the Productivity Commission, AMP Bank, Bank of Queensland, Bendigo and Adelaide Bank, ME Bank and Suncorp highlighted five key areas that require policy reform to achieve sustainable competition and competitive neutrality:

- Further policy reform to reduce the artificial funding cost advantages enjoyed by the major banks. While the new Major Bank Levy has reduced this advantage, it only recoups a small proportion of the overall credit rating uplift enjoyed by the majors;

- Further reform of risk weights to address the significant gap that still exists between the capital requirements of the major banks and standardised banks. While there has been some risk weight narrowing following the FSI, the gap remains significant, and is particularly stark for loans with the lowest risk;

- A review of macro-prudential rules to better balance macro outcomes such as stability, without undermining banking competition. One option would be for APRA to give greater policy weight to minimum capital requirements. Macroprudential rules set by APRA have effectively ‘locked-in’ market share of loan books at current levels, thus leaving smaller banks with no room to challenge the already dominant position of major banks;

- Mortgage aggregators and brokers owned by major banks should publicly report on the proportion of loans they direct to their owners. While we do not suggest that major banks should be banned from owning broker networks, we do believe that where this occurs it should be managed in an open and transparent way to ensure customers are able to make fully informed decisions; and

- Before any new regulations are introduced, greater consideration should be given to the impacts on smaller banks. The unprecedented pace and volume of new regulation and compliance has a disproportionate impact on smaller banks which stifles sustainable competition.

The banks also support the ABA’s submission calling for more care and attention into the shadow banking sector, which continues to compete free of many regulations and APRA oversight.

The CEOs said while Australia had been well served by a strong and highly regulated banking sector, it was important that stability did not overshadow competition and good consumer outcomes.

Suncorp Banking & Wealth CEO David Carter said: “We believe there can be a balanced and fair framework allowing banks of all sizes to compete on a level playing field, while still meeting all sound, prudential principles. We would like to see more attention on macro-prudential rules to promote customer choice and competitive pricing, as opposed to maintaining the status quo – which is in effect similar to the ‘yellow flag’ being waved at the Grand Prix, where all drivers are then prohibited from overtaking one another.”

ME CEO Jamie McPhee said: “Regulatory imbalances have allowed a small group of banks to dominate the Australian market. Reform is needed if we want to create a fairer banking system so smaller banks can compete. A more competitive banking system is about improving customer choice and promoting economic growth.”

AMP Bank Group Executive Sally Bruce said: “Access to cheaper funding plus lower capital requirements for like-for-like loans gives the big banks a huge advantage over smaller players. Combined with the blanket approach to compliance and macro-prudential limits, we have a system of issues which impede competition and the best outcomes for customers. We are at risk of keeping big banks big and small banks small unless we address.”

The CEOs said improving competitive neutrality will deliver better customer outcomes and drive greater innovation in the sector.

“A strong banking system is good for all Australians and smaller banks bring vital competition and choice to the market,” they said.

“While the market is competitive today, it is vital this competition is fair, productive and sustainable.

“The bottom-line test must be: what is good for customers is good for the economy.”

The Business looked at the impact of S&P’s down grades on 23 smaller banks in Australia, and highlighted the impact on funding and competition, especially in the longer term. It will more than offset the bank levy the big banks will have to wear!

They also looked a funding costs and explained why mortgage rates may rise and the potential adverse impact on household debt.

The big four Australian banks are likely to continue to benefit from the ‘wealth effect’ created by strong asset values, with investor concerns about high residential mortgage exposures “overdone”, says Morningstar.

In an analyst note about Westpac, Morningstar said Australia’s “rational and highly profitable major bank oligopoly is alive and well”.

The dominant position of the major banks will be further fueled by the ‘wealth effect’ from strong asset values, the expected rise in household spending, ongoing contributions from exports, the east coast residential construction boom and continuing government investment in infrastructure, said the research house.

Westpac remains Morningstar’s preferred major Australian bank, with its home-loan growth strategy viewed as a core strength rather than a key weakness.

“Investor concerns, centred on [Westpac’s] large exposure to residential mortgages, are overdone … We see solid earnings upside potential, with international investors continuing to focus too much attention on negative short-term issues,” said Morningstar.

The pressure on the banks to raise capital in order to satisfy the prudential regulator is likely to ease in coming months, said the note.

“We expect APRA will allow the major banks to raise the expected higher minimum capital requirements organically over a three-to-four year period,” said Morningstar.

“Despite regulator and media noise, it is becoming increasingly clear the capital raising scenario has been delayed for Westpac and major Australian bank peers.

“This is a positive outcome and one we have been pushing for several months at least.”

The Customer Owned Banking Association (COBA) – the industry body for credit unions, building societies, mutual banks and friendly societies – has today called on the Turnbull Government to allocate funds in the May Budget to bring forward a planned Productivity Commission review of banking competition.

“There is an urgent need for well-considered measures to promote competition in banking,” COBA CEO Mark Degotardi said.

“In its response to the 2014 Financial System Inquiry (FSI), the Government agreed to implement periodic reviews of competition in the financial sector.

“COBA requests allocation of funding to enable the Productivity Commission to complete the first such review by the end of 2017. The Government’s current commitment is to commence, but not complete, such a review in 2017. Given the state of competition in the banking market, we can’t afford to wait.

“The case for an accelerated timetable for the Productivity Commission review is underlined by the House Economics Committee’s November 2016 report that was highly critical of the state of competition in the banking market.”

The House Economics Committee report found:

- Australia’s banking sector is an oligopoly

- Australia’s four major banks have significant pricing power, higher than average returns on equity and large market shares

A lack of competition in Australia’s banking sector has significant adverse consequences for the Australian economy and consumers. It:

o creates issues around banks being perceived as too-big-to-fail (TBTF) (such as moral hazard)

o reduces incentives for the major banks to innovate and invest in new infrastructure, and

o can allow banks to use their pricing power to extract excess profits from consumers.

“The enduring solution to concerns about the banking market is action to promote sustainable competition so that poor conduct is swiftly punished by loss of market share.

“An expert review to identify the barriers to a more competitive market and measures to overcome those barriers is sorely needed,” Degotardi said

“COBA’s recently commissioned Deloitte Access Economics (DAE) report on implementation of key FSI recommendations shows that significant work remains unfinished.

“We strongly endorse DAE’s suggestion that the Productivity Commission review should consider whether regulators’ rules and procedures are creating inappropriate barriers to competition and whether there is appropriate regard to other business models, including the customer owned model.”

The DAE report mentions two examples of regulator decision-making affecting competition:

- APRA’s approach to regulatory capital instruments for customer owned banking institutions, and

- APRA’s application of the cap on investor lending growth.

COBA’s pre-budget submission lodged with Treasury urges the Government to announce the following measures in the 2017-18 Budget:

1. Funding to bring forward a review by the Productivity Commission of competition in the banking market, to report by the end of 2017.

2. A company tax rate for customer-owned banking institutions that matches the effective tax rate of major banks of between 22% and 25%.

3. Expand GST RITC item 16 ‘credit union services’ to accommodate mutual building societies and mutual banks that are former mutual building societies.

“These measures, along with implementation of key FSI recommendations, will help deliver a more competitive banking market for the benefit of consumers and the wider economy.”

As reported in Fairfax outlets today, Coles has announced plans to offer personal loans by teaming up with GE Capital and will split the cost 50/50. The new service planned is planned for launch mid-2015. It will need regulatory approval, but Coles will not need a banking licence. 400,000 Coles MasterCard customer accounts form part of the venture which is targetting a lending book of $800 million in its first year. Coles already announced plans to launch its “mobile wallet” using a credit card chip embedded in a sticker that can be applied to the case of a smart phone. The sticker also contains a barcode linking purchases to flybuys rewards. A smartphone application will provide assess to transaction data and a flybuys statement.

The UK Prudential Regulation Authority (PRA) and Financial Conduct Authority (FCA) have today published a review of the changes introduced last year which were put in place to reduce the barriers to entry for new financial institutions. The purpose of the measures was to enable increased competition in the banking industry, to the benefit of customers. The changes focussed on two key areas: reforms to and a simplification of the authorisation process for new banks; and a major shift in the prudential regulation, such as capital requirements, for new entrants.

The two areas of focus were:

In the twelve months following the changes, the PRA authorised five new banks and there has been a substantial increase in the number of firms discussing the possibility of becoming a bank with the regulators. In the twelve months to 31 March 2014 the regulators held pre-application meetings with over 25 potential applicants. These firms have a range of different business models from retail and wholesale banking to FCA-regulated Payment Services firms who are looking to enter the banking market and offer deposits and lending to their current client base (including small SMEs) and others who are proposing to offer a mixture of SME or mortgage lending funded by retail and SME deposits.

The minimum amount of initial capital required by a new entrant bank is £1m compared to £5m under the previous regime. The on-ramp strategies have been helpful for applicant firms that may previously have faced challenges in raising capital or investing in expensive IT systems without the certainty of being authorised.

The PRA intends to publish statistics regarding banking authorisation annually.

In the Australian context, we know from recent client work that potential new entrants face a stiff climb to gain access to the local market. Consideration should be given to given to emulate the UK approach, because we need greater competitive tension in Australian banking.