There is currently no legal requirement for product providers to move legacy clients into cheaper products, but that could change in the wake of last week’s royal commission hearings, says NGM Consulting.

Product providers could be the next in line for an explicit ‘best interests’ obligation following the revelations at the royal commission hearings last week, says NGM Consulting.

In its latest ‘Trialogue’ article, NGM Consulting noted a distinct “adjustment” at last week’s hearings when it comes to product providers.

“It relates to the test that we should use when making ‘conflicted decisions’, where the interests of consumers are at odds with the commercial interests of the firm,” said NGM.

Counsels assisting the commissioner delved into examples where product providers had a range of products, said NGM – “the more contemporary of which are unambiguously known to be better and cheaper than the older, legacy products.”

“An adviser might be expected to shift the client into the better product, but as a product manufacturer many have declined the opportunity to carve up their own revenue line to ensure clients are shifted to the more contemporary product solution,” said NGM.

One example came about in evidence of AMP head of platform development John Keating, who failed to explain why clients had not been moved out of platforms AMP’s own benchmarking guide rated as ‘uncompetitive’ with the broader market.

It is unlikely product providers would fall into legal trouble for this kind of behaviour, said NGM – “until now”.

“There is a test of ‘community standard’ being applied to decisions made by for-profit institutions,” said the consulting firm.

“Regardless of where this all lands, it’s clear any attempt to walk-back the standard from the new high set by the commission will not help the industry’s reputation.”

Mr Wilkins will lead the company as Executive Chairman for an interim period while the process for selecting a Chairman, and appointment of an additional new non-executive director, is conducted. This will further strengthen governance and ensure stability while a measured process of board renewal is undertaken. Mr Wilkins will now lead the selection process for a new Chief Executive Officer, which is in progress.

AMP also announces that Group General Counsel and Company Secretary Brian Salter will leave the company. His outstanding deferred remuneration will be forfeited as a result of the Board exercising its discretion.

The Board has received advice from Philip Crutchfield QC, Tamieka Spencer Bruce of Counsel, and Tim Bednall of King & Wood Mallesons in relation to certain issues raised in the Royal Commission concerning the preparation of the Clayton Utz report on AMP’s fee for no service issue. The advice follows the establishment of the Board Committee chaired by Mr Wilkins to examine the issues relating to AMP’s advice business that have been raised in the Royal Commission.

Having considered and assessed the matters, the Board is satisfied that the former Chairman Catherine Brenner, former Chief Executive Officer Craig Meller and the other directors did not act inappropriately in relation to the preparation of the Clayton Utz report.

The Board, including the former Chairman, were unaware of and disappointed about the number of drafts and the extent of the Group General Counsel’s interaction with Clayton Utz during the preparation of the report. The Board commissioned and received the report. It was not a matter for the Board’s approval.

The Board announces the following further actions:

Recognising collective governance accountability for the issues raised in the Royal Commission and for their impact on the reputation of AMP, the Board is reducing fees for all AMP Limited Board Directors by 25 per cent for the remainder of the 2018 calendar year; and

The employment and remuneration consequences for the individuals within the business responsible for the fee for no service issue will be determined on finalisation of an ongoing external employment review, which is expected to complete shortly

Catherine Brenner said: “I am honoured to have been Chairman of AMP. I am deeply disappointed by the issues at hand and am particularly concerned for the impact they have had on our customers, employees, advisers and shareholders.

“As Chairman, I am accountable for governance. I have always sought to act in the best interests of the company and have been in discussions with the Board about the most appropriate course of action, including my resignation. The Board has now accepted my resignation as Chairman as a step towards restoring the trust and confidence in AMP.”

Mike Wilkins, Executive Chairman, AMP Limited said: “The Board acknowledges Catherine’s leadership and thanks her for her professionalism, integrity and dedication to the company over the past eight years. We will now begin a process of board renewal, including fast-tracking selection of a Chairman, and a new director. This process will help ensure stability and further strengthen governance.

“AMP respects the Royal Commission process. I can assure you that the evidence and submissions presented by Counsel Assisting are being treated extremely seriously by the Board. Appropriate steps are being taken to address the issues raised, and remediating our customers is being given utmost priority. On behalf of the Board, I reiterate our sincerest apology to our customers, and know we have significant work to do to rebuild their trust.”

AMP will be making a formal submission to the Royal Commission by Friday 4 May in response to the matters raised in closing submissions by Counsel Assisting the Royal Commission.

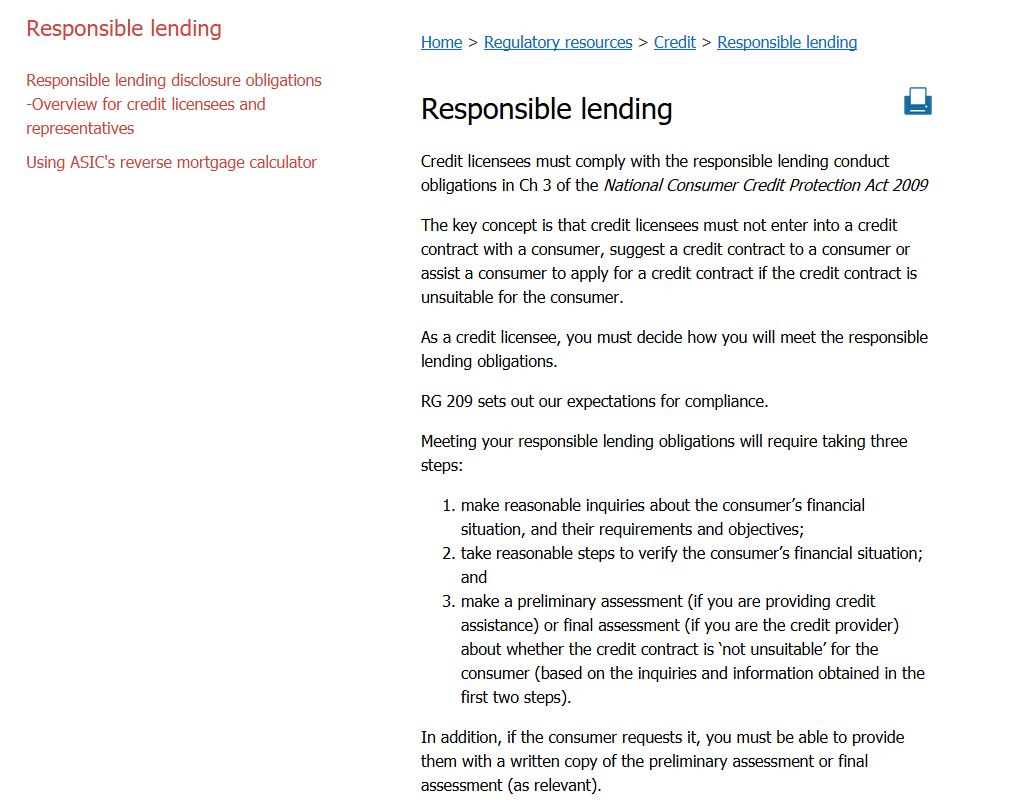

Under the National Consumer Credit Protection Act 2009, credit providers are required to lend responsibly.

This means that before lending, the credit provider must assess the suitability of a loan for a borrower, which involves an assessment of the borrower’s capacity to repay the loan as well as an assessment of the extent to which the loan will meet the objectives and requirements of the borrower.

A failure to undertake these assessments before lending will amount to a breach of the act, which should result in sanctions ranging from enforceable undertakings to the cancellation of a credit provider’s credit licence.

There is clearly a need for a robust and well-enforced responsible lending regime to curtail undesirable market practices and prevent increased financial stress on households in Australia.

The evidence that has come out of the Financial Services Royal Commission must lead to a serious re-assessment of the efficacy of the responsible lending regime, particularly in relation to its enforcement by ASIC. It also calls into question the efficacy of the prudential regulator, APRA.

It is now clear that the major banks have based many lending decisions on flawed information, leading to what have been labelled “liar loans”.

ANZ bank, in its submissions to the royal commission, acknowledged a lack of evidence that it had made genuine enquiries into customers’ living expenses.

William Rankin who was responsible for ANZ’s home loan portfolio stated that from October 2016 to September 2017 ANZ sold $67 billion in home loans and that 56 per cent of those ($38 billion) came from mortgage brokers.

Damningly, Mr Rankin confirmed that ANZ did not take steps to verify the information provided by brokers regarding customers’ expenses.

Gym owner among NAB ‘introducers’

In its submission to the inquiry, CBA acknowledged inaccuracies in calculations, insufficient documentation and verification, and deficiencies in controls around manual loan approval processing.

Daniel Huggins, who supervises the home buying division at CBA, gave evidence that while the bank had explicitly documented its recognition that volume based commissions to brokers (as opposed to flat fee payments) encouraged poor quality loans and poor customer outcomes, the bank had continued with volume based commissions and in fact “de-accredited” brokers who did not refer a sufficient volume of loans.

He also stated that CBA continued to rely on the customer information provided by mortgage brokers, notwithstanding an explicit acknowledgment by CBS that customer information provided by brokers could not be relied upon.

Anthony Waldron, the executive general manager for broker partnerships at NAB, gave evidence regarding NAB’s “introducer program”, which included a number of shocking admissions.

The program involved introducers who were not necessarily carrying on lending businesses (one introducer ran a gymnasium), who formed relationships with bankers employed by NAB.

Both bankers and introducers benefitted from the loan referrals (through bonuses and commissions), and introducers were required to meet minimum loan referral thresholds.

Mr Waldron acknowledged that the program led to unsuitable loans, false documentation, dishonest application of customers’ signatures on consent forms and misstatements of information in loan documentation.

He agreed that the bankers were more concerned with sales than keeping customers and the bank safe.

ASIC and APRA should be doing more

Westpac had acknowledged in its submission that it was the subject of ASIC enforcement action in relation to breach of the responsible lending obligations, for failure to properly assess whether borrowers could meet their repayment obligations before entering into home loan contracts.

Westpac had also acknowledged that in 2016 some of its authorised home lending bankers were not correctly verifying customer income and expenses.

There is now no doubt that the financial regulators, ASIC and APRA, should be doing more to ensure prudent lending standards by credit providers in Australia.

The prospective harm that could result to Australian households from elevated levels of indebtedness, and the adverse flow-on effects to the Australian economy, cannot be ignored.

The evidence at the royal commission has confirmed a current tendency of lenders to reduce lending standards to increase credit activity and profitability, but it will all come crashing down soon if it is allowed to continue.

For an increasing number of households, even small increases in the loan interest rates, a decline in real estate values, or a reduction in working hours or conditions may have grave consequences.

There are also more significant risks for borrowers which include unemployment, the removal of government benefits, rapid and significant increases in loan interest rates, a recession, a housing or equity market crash, or a financial crisis.

Therese Wilson is an associate professor at Griffith law School; Gill North is a professor at Deakin University Law School

Full Disclosure: Gill North is also a Principal at Digital Finance Analytics!

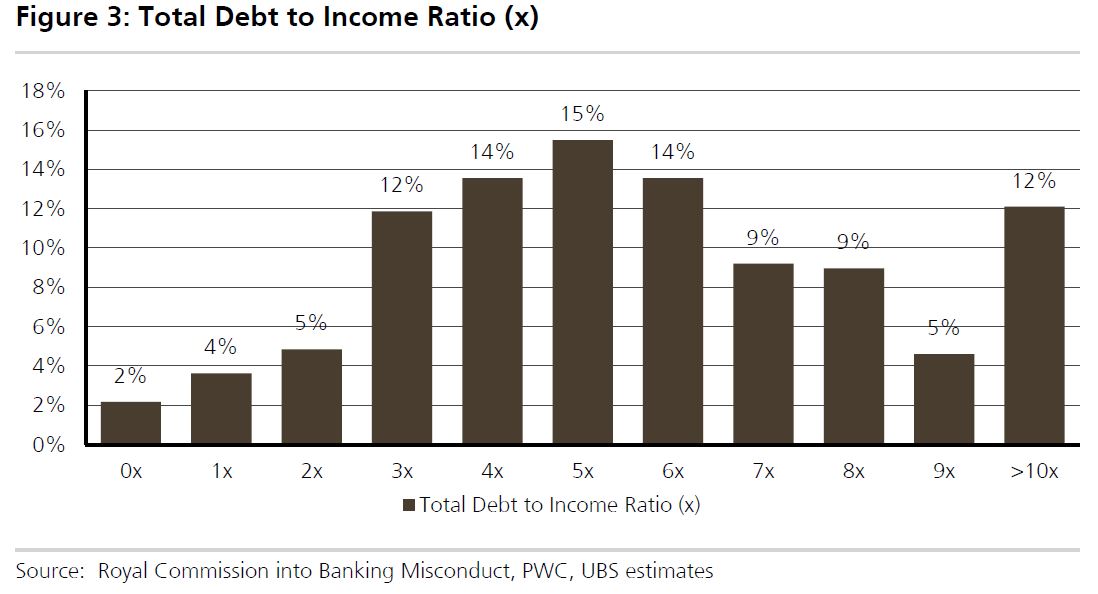

UBS continues their forensic dissection of the mortgage industry with the release of their analysis of data from Westpac, which the lender provided to the Royal Commission. This was representative data from the bank of 420 WBC mortgages analysed by PwC as part of APRA’s recent review. APRA Chairman Wayne Byres found WBC to be a “significant outlier”, with

PwC finding 8 of the 10 mortgage ‘control objectives’ were “ineffective”.

UBS says for the first time information on borrower’s Total Debt-to-Income ratios (not Loan-to-Income) has been made available. They found WBC’s median Debt-to-Income at 5.4x, with 35% of the sample having Debt-to-Income ratios of >7x. Further 46% of the mortgage applications had an assessed Net Income Surplus of <$250 per week.

This data raises questions regarding the quality of WBC’s $400bn mortgage book (70% of its loans). While WBC has undertaken significant work to improve its mortgage underwriting standards over the last 12 months, we expect it and the other majors to further sharpen underwriting standards given the Royal Commission’s concerns with Responsible Lending. This could potentially lead to a sharp reduction in credit availability.

This raises two questions. First how much tighter will credit availability now be. We continue to expect an absolute fall in loan volumes, and this will translate to lower home prices.

Second, is this endemic to the industry, or is Westpac really an outlier? From our data we see similar patterns elsewhere, so that is why we continue to believe we have systemic issues.

Income is being overstated and expenses understated.

Customers have multiple loans across institutions and these are not always being detected, so their total debt burden is higher than the bank sees.

Combined these are significant and enduring risks. Chickens will come home to roost! Especially if rates rise.

The Royal Commission into Financial Services Misconduct has now uncovered evidence of poor industry practice from both the lending camp, including from mortgage brokers, and the financial advice camp. In both cases their forensic analysis revealed cases of consumers being put in the wrong products, charged for services they never received and on fee structures which were hardly transparent.

In addition, some advisers and brokers were restricted by the product portfolios available via their organisations, and ties back to the big banks and other large players were often not adequately disclosed.

But here’s the thing. There are two distinct flavours of regulation in play, despite both being within ASIC’s bailiwick. I believe it is time to move to a unified common set of regulatory standards to cover both credit and wealth domains.

Lending and credit are based on ASIC’s regulations for responsible lending, which requires both a lender, and intermediary – like a broker – to ensure the loan is “not unsuitable”.

This looking at the purpose of the loan, making an assessment of the ability of the consumer to repay, and ensuring it is fit for purpose. What warrants as appropriate steps depends on the nature of the transaction and og the individual capabilities of the customers involved, so it is “scalable”. But that said, they are not obliged to act in the best interests of their client, and fee disclosure is at best rudimentary. Trailing commissions for example are not disclosed. The precise meaning and definition of what is suitable is still subject to case law. But overall, this is weak protection, and as we have seen from the Commission has failed to protect many borrowers. There is nothing here about the best or most appropriate product and it does not include any reference to whole of market analysis. Just, at best “Not Unsuitable”.

On the financial advice side of the house, as is being explored by the Commission currently, under the FOFA rules, advisers must work in the best interests of their clients, disclose remuneration, and their relationship with product manufacturers if appropriate.

This is a whole different set of rules, again regulated by ASIC. Note again, this does not include finding the best product, or providing whole of market advice. So the rules are slightly stronger, but still incomplete.

Now consider this scenario. I am a property investor who is seeking a mortgage as part of a strategy to build wealth. I will need a life insurance policy also. Who do I talk to? A mortgage broker can assist me with finding a mortgage, but cannot help with life insurance. But if I go and talk to a financial adviser unless they are also a mortgage broker, they cannot assist with the mortgage. And if I find an adviser qualified in both regimes, which rules do they work under?

And that’s the point. The regulations, which by the way are an accident of history in that the responsible lending laws evolved from earlier state legislation, get in the way of providing holistic unified advice. A consumer has both credit AND other wealth management requirements as part of a single issue. Indeed, there are trade-offs, for example between holding more or less investment properties, versus investing in other market related investment products. Indeed, it is feasible to wrap property investments into an overall wealth strategy.

So I suggest that now is the time to create a new unified set of rules to apply to all financial advisers, whether they are advising on credit or wealth products. They should be crafted around best interests of their clients, and should mean offering whole of market advice. That means creating an advice plan which spans both investments and lending. The plan should be based on a fee for service, and the advisers’ remuneration should not be in any way linked to a commission or revenue flow from the products they suggest.

Indeed, we should break apart the advice element from the product sale, and application. I suggest that individual product application could be completed by the adviser as part of a fee for service, but they should not receive any additional remuneration related to successful product sales.

This also has implications for ASIC, as it would reshape the advice landscape, but potentially could both simplify the regulatory regime, and strengthen the protection for customers, and help facilitate better customer outcomes. Down the track, advisers would require one set of qualifications, and would be become more recognised professionals.

I believe the current chaotic regulatory environments, which were crafted to appease the finance industry, are in appropriate and the time has come to create a single unified set of regulations. This would assist customers, but would also help the industry on its journey towards professionalism.

Global litigation firm Quinn Emanuel Urquhart & Sullivan is investigating a class action lawsuit against AMP for shareholder losses following revelations at the royal commission last week.

Giving evidence before the royal commission, AMP head of financial advice Jack Regan admitted his firm lied to ASIC on 20 separate occasions about its practice of providing ‘fees for no service’ to financial advice clients.

Quinn Emanuel has backing from global litigation funding firm Burford Capital for the potential class action.

The class action is open to shareholders who acquired shares between 24 May 2013 and 16 April 2018.

Quinn Emanuel partner Damian Scattini said: “The revelations of AMP’s misconduct are especially upsetting given the people who were hurt – the ordinary Mums and Dads who as shareholders gave AMP one of Australia’s largest shareholder registers, who have now lost their savings due to its dishonesty, and who as customers were charged for services AMP has admitted they never received, all so executives could make hefty bonuses.”

“QE has been investigating AMP’s precipitous share price fall even before the most recent revelations of misconduct, and having Burford, the world’s top litigation finance company, in place as our partner means we’re ready to move quickly on behalf of shareholders,” Mr Scattini said.

Burford managing director Craig Arnott said: “The conduct admitted at the Royal Commission is starkly at odds with AMP’s responsibilities and shareholders’ legitimate expectations, requiring redress so that AMP’s shareholders can recover the value that has been lost.

“Burford is glad to join forces with Quinn’s first-rate team so we can help deliver that result for shareholders, which we hope will be as swift as possible.”

Former prime minister Tony Abbott has strongly condemned the performance of financial sector regulators, suggesting they should be sacked and replaced by “less complacent” people.

With increasing attention on the apparently inadequate performance of the Australian Securities and Investments Commission (ASIC), Abbott raised the question of what the regulators had been doing as the scandals had gone on.

“We all know there are greedy people everywhere, including in the banks,” he told 2GB on Monday. “But banking is probably the most regulated sector of our economy. What were the regulators doing to allow all this to be happening?”

Abbott said his fear was “that at the end of this royal commission we will have yet another level of regulation imposed upon the banks when frankly what should happen is, I suspect, all the existing regulators should be sacked and people who are much more vigilant and much less complacent go in in their place.”

He said the analogy was, “yes, punish the criminals but if the police are turning a blind eye to the criminals, you’ve got to get rid of the police and get decent people in there”.

Meanwhile Malcolm Turnbull, speaking to reporters in Berlin, defended refusing for so long to set up a royal commission, although he said commentators were correct in saying that “politically we would have been better off setting one up earlier”.

Turnbull said that by taking the course it had the government “put consumers first”.

“The reason I didn’t proceed with a royal commission is this – I wanted to make sure that we took the steps to reform immediately and got on with the job.

“My concern was that a royal commission would go on for several years – that’s generally been the experience – and people would then say, ‘Oh you can’t reform, you can’t legislate, you’ve got to wait for the royal commissioner’s report.’

“So if we’d started a royal commission two years ago, maybe it would be finishing now and then we’d be considering the recommendations … With the benefit of hindsight and recognising you can’t live your life backwards, isn’t it better that we’ve got on with all of those reforms?”

Turnbull dismissed Bill Shorten’s call for the government to consider a compensation scheme for victims by saying this matter was already in the commission’s terms of reference.

Among the reforms it has made, the government highlights giving ASIC more power, resources and a new chair.

But Nationals backbencher senator John Williams, who has been at the forefront of calls for tougher action against wrongdoing in the financial sector, told the ABC that ASIC has got to be “quicker, they’ve got to be stronger, they’ve got to be seen as a feared regulator.

“That is not the situation at the moment,” he said.

He had sent a text message to Peter Kell, ASIC deputy chair, a couple of nights ago “and I said, mate, Australia is waiting for you to act”.

Asked how the culture within ASIC could be changed, Williams said, “I suppose you keep asking them questions at Senate estimates, keep the pressure on them, keep the message going on with the management of ASIC regularly.

“As I have said to the new boss [chair James Shipton], you’ve got to act quickly, you’ve got to be severe, you’ve got to be feared. If you’re not a feared regulator, people are going to continue to abuse the system, do the wrong thing without fear of the punishment”.

He welcomed the increased penalties announced by the government last week.

The chair of the Australian Competition and Consumer Commission (ACCC), Rod Sims, while declining to comment on ASIC, said he agreed with Williams “that you really do have to be feared. And frankly I’d like to think the ACCC is.

“I won’t comment on others but you want people to be really watching out – watch out for the ACCC, watch out that you don’t get caught because if they catch us it’s going to be really dire consequences. And I think we’ve got that mentality,” he told the ABC.

Updated at 4:30pm

In an interview on Sky late Monday, Finance Minister Mathias Cormann admitted, “With the benefit of hindsight, we should have gone earlier with this inquiry.” This was in stark contrast with his colleague, Minister for Financial Services, Kelly O’Dwyer, refusing to make the concession when she was repeatedly pressed in an interview on Sunday.

Author: Michelle Grattan, Professorial Fellow, University of Canberra

Given the range of issues already exposed by the Royal Commission into Financial Services Misconduct, including selling loans outside suitable criteria, fees from advice not given and other factors; we need to ask about the impact on the profitability of the banks and so share prices.

And all this is in the context of higher funding costs already hitting.

A number of international investors and hedge funds have placed shorts on the major banks, signalling an expectation of further falls in share price ahead, but the majors have already dropped by around 15% in the past year.

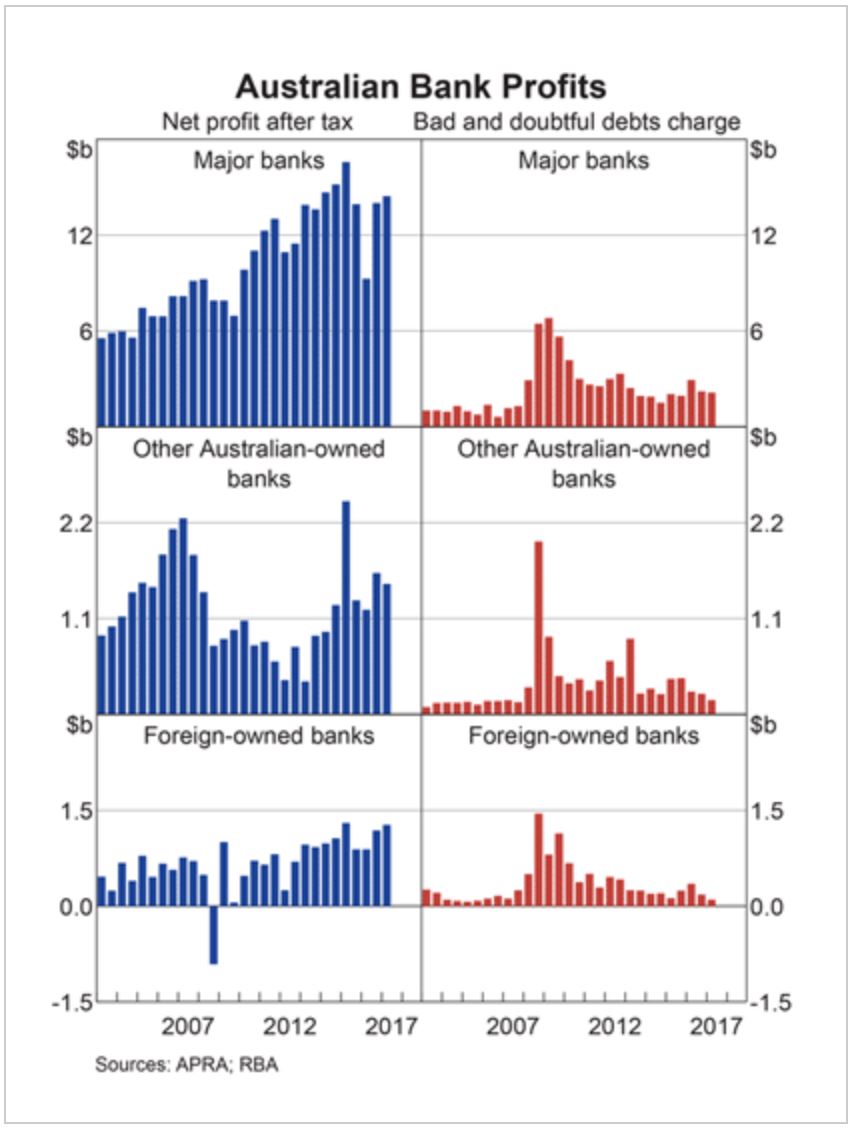

The recent RBA chart pack contained this picture on profitability. Bad and doubtful debts are very low, thanks to low interest rates. But that may change if rates were to rise, and “liar loans” are wide spread. There is no good data on the potential impact so far.

It is important to remember the Productive Commission recently called out that :

A quick survey of the banks from last year show that the return on equity – a measure of absolute profitability – or ROE range from 14.5% for CBA, 10.3% from NAB, 10.9% for ANZ and Westpac was 13.3% while AMP was 11.5%.

Looking overseas, US based Wells Fargo, which happens to be a key Warren Buffett holding, was 11.5% , the Bank of America earned less than 6.8% and Lloyds earns 4%. Barclays was -2.7%. In fact among western markets, only Canadian banks come close to our ROE’s – for example of Bank of Montreal was 11.3% but then they have the same structural issues that we do.

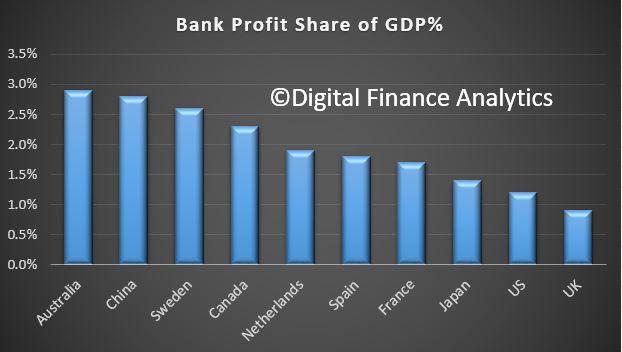

Data from news.com.au from 2016 shows the relative profit to GDP across several countries. Australia Wins.

That means 2.9 per cent of every $100 earned in Australia ends up as bank pre-tax profit, compared to the US and UK at $1.2 and 90 cents per cent respectively.

China is the highest after Australia at $2.80, Sweden $2.60 and Canada $2.30.

The Australia Institute also pointed to public money being used to secure the banking sector.

“Excessive profits provide a drag on the economy and hurt consumers who pay higher margins on bank products. The Reserve Bank found the big four banks enjoy an implicit government subsidy worth up to $4 billion dollars a year,”

The Royal Commission revelations have the potential to impact the market value of the banks as reflected in their share prices, and also raises questions about the financial stability of the entire system in Australia. APRA, in particular and the RBA have been (over?) focussed on financial stability, as the recent Productive Commission draft report highlighted.

Regulators have focused on a quest for financial stability prudential stability since the Global Financial Crisis, promoting the concept of an unquestionably strong financial system.

The institutional responsibility in the financial system for supporting competition is loosely shared across APRA, the RBA, ASIC and the ACCC. In a system where all are somewhat responsible, it is inevitable that (at important times) none are. Someone should.

The Council of Financial Regulators should be more transparent and publish minutes of their deliberations. Under the current regulatory architecture, promoting competition requires a serious rethink about how the RBA, APRA and ASIC consider competition and whether the Australian Competition and Consumer Commission (ACCC) is well-placed to do more than it currently can for competition in the financial system.

Over the next few days we will try to assess the potential impact ahead, from higher loss rates, lower fee income and potential fines and penalties. Then of course, there is the question, will these additional costs be passed on to investors and shareholders, or simply recovered from the current customer based by higher fees.

We expect banks to start making provisions for the revenue hits ahead. ANZ, for example, said their RC legal bill will be around $15 million. CBA made a $200 million expense provision for expected costs relating to currently known regulatory, compliance and remediation program costs, including the Financial Services Royal Commission.

To start the journey lets look at the relative performance of the banks’ share prices over the past year. Westpac share price is 16.8% lower compared with a year ago.

ANZ is down 16% over the same period

CBA has fallen 15.9% in the past 12 months.

and NAB’s share price dropped 14.2% over the same period.

In comparison, the ASX 200 is up 0.25% over the past year.

Among the regional banks, Bendigo Bank has fallen 16.6%

Bank Of Queensland has fallen 11.7% over the past year.

In contrast Suncorp is 0.74% higher

and Macquarie Group was up 19.5%. They of course have more than half their business offshore now.

Next time, we try to size the revenue hits ahead, and think about what that may mean for the banks and their customers.

Mr Turnbull and his senior colleagues have spent the past two years arguing against a royal commission into the financial sector, although some of his backbenchers were campaigning vigorously for a royal commission.

ABC Insiders did a nice montage yesterday showing the evolution of the spin, from initially vehemently resisting a commission.

The PM finally called a royal commission late last year and shocking revelations have emerged as it has been taking evidence.

This was after an appalling interview with Kelly O’Dwyer who has been the Minister for Revenue and Financial Services, since July 2016.

Public hearings into the financial advice sector continued on Friday as BT Financial Advice general manager Michael Wright continued giving evidence.

Counsel assisting Rowena Orr grilled Mr Wright on the remuneration practices of Westpac/BT and whether its planners could be considered professionals when they are incentivised with sales targets.

Mr Wright said that while advisers are not viewed as ‘professionals’ by Australians in the same way that doctors are, the perception is changing for the better.

Furthermore, he said, the ‘balanced scorecard’ for Westpac advisers will be changed to include more non-financial factors.

“We’ll be setting peoples’ remuneration off their qualifications, based off their competency as an adviser, based off the standards that they go through with advisers,” he said.

“We will not set people’s remuneration – fixed or variable – based off how much money they write,” Mr Wright said.

However, Ms Orr pointed out that one-fifth of the ‘balanced scorecard’ for the company’s advisers will include financial measures.

“We debated this long and hard. The reality is we want to have a viable, sustainable, professional business. We’ve not a charity,” he said.

“We considered removing revenue from the scorecard and having 100 per cent non-financials,” Mr Wright said.

From 1 October 2018, Mr Wright said, BT will be ending grandfathered commissions for superannuation and investments – although risk commissions will remain (as per the Life Insurance Framework).

When it comes to the advice business he oversees, Mr Wright said he would be “delighted” if BT moved to a completely fee-for-service model.

However, with his “BT product provider hat on”, he said there is a first-mover disadvantage to being the first institution to end grandfathering completely.