Commonwealth Bank of Australia announced its results for the half year ended 31 December 2016 today. CBA is well run, so they are a bellwether of the broader financial sector. It was a solid result with asset growth, 3% lift in underlying income and good cost management, but shows the pressure created by regulatory capital uplifts, competition in home lending and consumer deposits, and arrears in mining exposed areas. They continue to make strong progress in digital banking, where they are a leader. They do not believe there is evidence for a housing bubble. Wealth and Insurance in under some pressure, so retail banking is taking the load, thus system credit growth is critical.

They also announced further interest only investment mortgage rate price hikes which will lift NIM.

CBA reported a statutory net profit after tax (NPAT) of $4,895 million, which represents a 6 per cent increase on 1H16 period. This includes a $397 million gain on sale of the Group’s remaining investment in Visa Inc. and a $393 million one-off expense for acceleration of amortisation on certain software assets.

Cash NPAT was $4,907 million, an increase of 2 per cent on the prior comparative period.

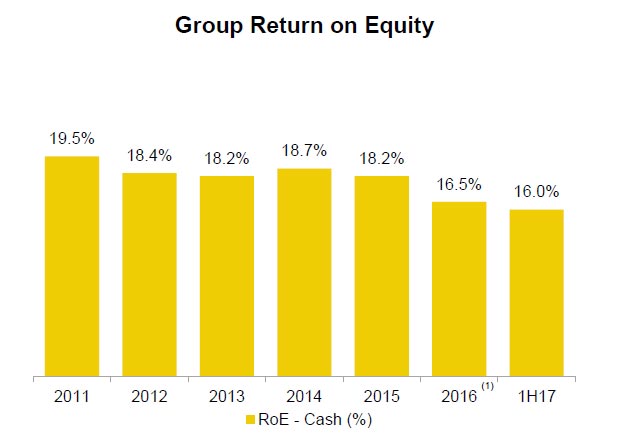

Return on equity (cash basis) was 16 per cent.

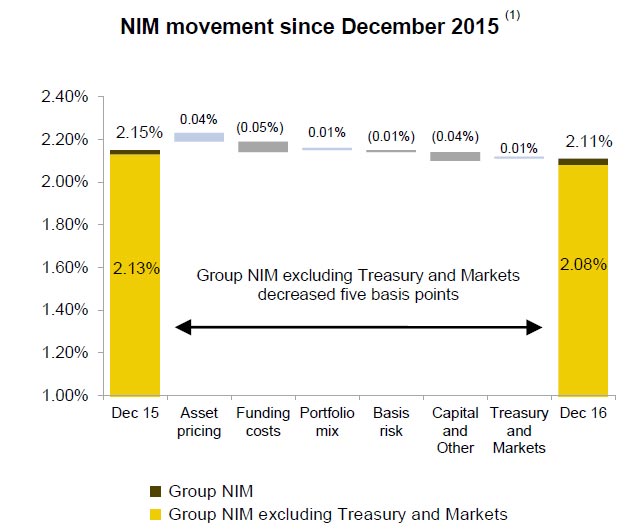

Strikingly though the net interest margin was down 4 basis points to 2.11%, or 2.08% excluding treasury, down 5 basis points. This was expected.

Strikingly though the net interest margin was down 4 basis points to 2.11%, or 2.08% excluding treasury, down 5 basis points. This was expected.

The key drivers were:

The key drivers were:

- Asset pricing: Increased margin of three basis points, reflecting the impact of home loan repricing, partly offset by the impact of competition on home and business lending.

- Funding costs: Decreased margin of five basis points, reflecting an increase in deposit costs of three basis points due to the lower cash rate and increased competition, and an increase in wholesale funding costs.

- Portfolio mix: Decreased margin of one basis point reflecting an unfavourable change in lending mix from proportionally higher levels of home lending.

- Capital and Other: Decreased margin of two basis points driven by the impact of the falling cash rate environment on free equity funding, and a lower contribution from New Zealand.

- Treasury and Markets: Increased margin of two basis points driven by a higher contribution from Treasury.

Average interest earning assets increased $23 billion on the prior half to $823 billion, driven by:

- Home loan average balances increased $16 billion or 4% on the prior half, primarily driven by growth in the domestic banking business;

- Average balances for business and corporate lending increased $5 billion or 3% on the prior half, driven by growth in business banking lending balances; and

- Average non-lending interest earning assets increased $2 billion or 1% on the prior half.

Customer deposits accounted for 66% of total funding at 31 December 2016. Of the remaining, Short-term wholesale funding accounted for 42% of total wholesale funding at 31 December 2016. During the half, the Group raised $22 billion of long-term wholesale funding. The cost of new long-term funding improved marginally on the prior half as markets shrugged off any potential negative sentiment associated with the US

Presidential election result, a 25 basis points Federal Reserve rate rise, higher global bond yields, and Brexit.

Loan impairment expense increased 6% on the prior comparative period to $599 million. The increase was driven by:

- An increase in Retail Banking Services as a result of higher home loan and personal loan losses, predominantly in Western Australia;

- Lower home loan provision releases and higher growth in New Zealand lending portfolios;

- An increase in Bankwest due to slower run-off of the troublesome book, reduced write-backs and higher home loan losses, predominantly in Western Australia; and

- An increase in IFS as a result of losses in the PT Bank Commonwealth (PTBC) commercial lending portfolio; partly offset by

- Lower individual provisions in Business and Private

Banking; and

- A reduction in Institutional Banking and Markets due to lower collective provisions and a higher level of writebacks.

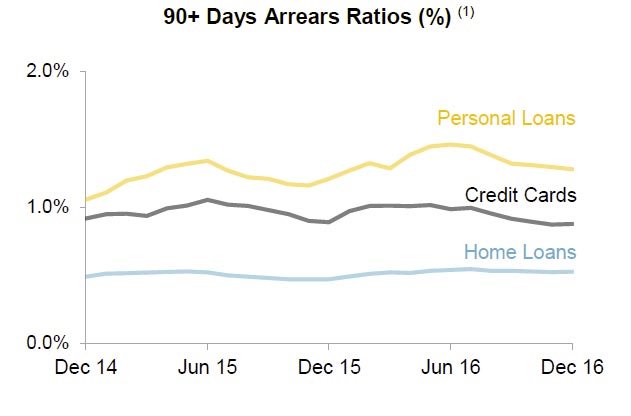

Provisioning levels remain prudent and there has been no change to the economic overlay. Retail arrears across all products reduced during the current half reflecting seasonal trends.

Home loan arrears reduced over the prior half, with 30+ days arrears decreasing from 1.21% to 1.12%, and 90+ days arrears reducing from 0.54% to 0.53%. Unsecured retail arrears improved over the half with credit card 30+ days arrears falling from 2.41% to 2.28%, and 90+ days arrears reducing from 0.99% to 0.88%. Personal loan arrears also improved with 30+ days arrears falling from 3.46% to 3.14% and 90+ days arrears falling from 1.46% to 1.28%. However personal loan arrears continue to be elevated driven primarily by Western Australia and

Queensland.

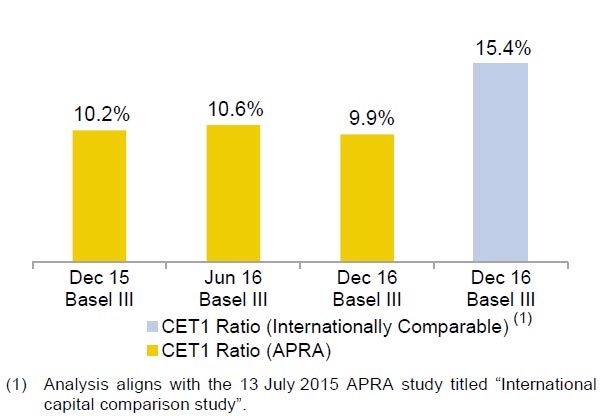

As at 31 December 2016, the Basel III Common Equity Tier 1 (CET1) ratio was 15.4% on an internationally comparable basis and 9.9% on an APRA basis.

As at 31 December 2016, the Basel III Common Equity Tier 1 (CET1) ratio was 15.4% on an internationally comparable basis and 9.9% on an APRA basis.

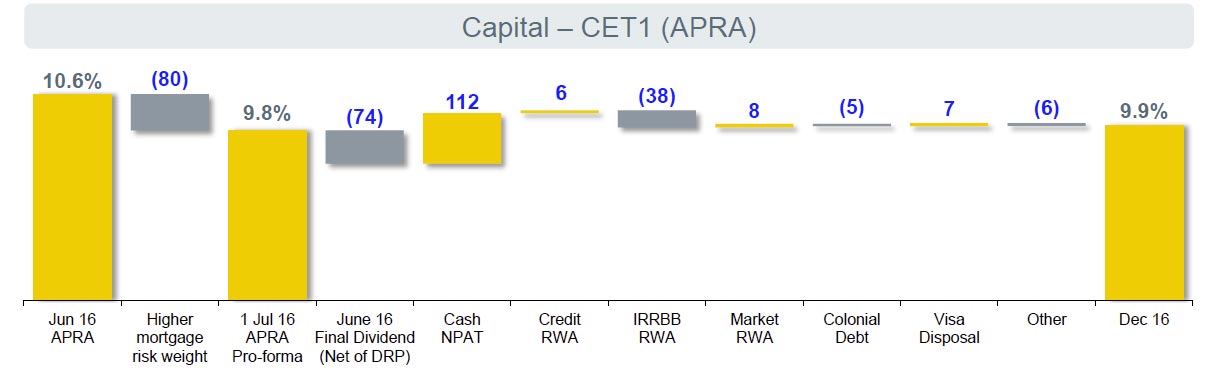

The Group’s CET1 (APRA) ratio decreased 70 basis points for the half year ended 31 December 2016. After allowing for the implementation of the APRA requirement to hold additional capital of 80 basis points with respect to Australian residential mortgages, effective from 1 July 2016, the

The Group’s CET1 (APRA) ratio decreased 70 basis points for the half year ended 31 December 2016. After allowing for the implementation of the APRA requirement to hold additional capital of 80 basis points with respect to Australian residential mortgages, effective from 1 July 2016, the

underlying increase in the Group’s CET1 (APRA) ratio was 10 basis points on the prior half.

The Group’s leverage ratio, defined as Tier 1 Capital as a percentage of total exposures, was 4.9% at 31 December 2016 on an APRA basis and 5.5% on an internationally comparable basis.

The Group’s leverage ratio, defined as Tier 1 Capital as a percentage of total exposures, was 4.9% at 31 December 2016 on an APRA basis and 5.5% on an internationally comparable basis.

There was a small decline in the ratio across the December 2016 half year with growth in exposures partly offset by an increase in capital levels.

The BCBS has advised that the leverage ratio will migrate to a Pillar 1 minimum capital requirement of 3% from 1 January 2018. The BCBS will confirm the final calibration in 2017. LCR was 135% at 31 Dec 2016.

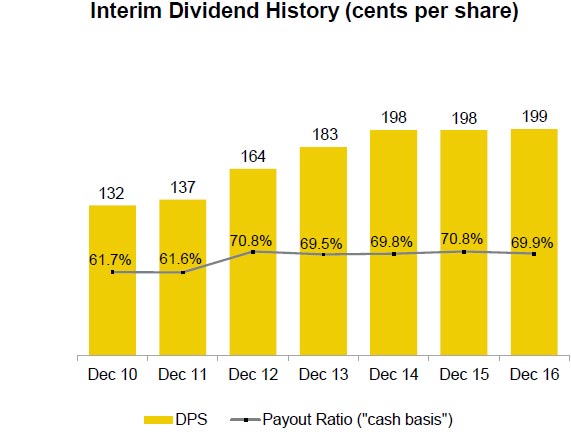

The Board determined an interim dividend of $1.99 per share, a 1 cent increase on the 2016 interim dividend.

Looking in more detail at the Australian home loan portfolio, the total book was worth $423 billion in December 16. They added $53 billion of loans in the past 6 months, with an value of $311,000 and at a serviceability buffer of 2.25%. 89% were variable rate loans. 37% were investor loans (up from 33% in the prior 6 months) and 43% originated via brokers, down from 46% in June 16, reflecting a 13% rise in branch application. 40% were interest only loans, up from 38% in the previous period.

Looking in more detail at the Australian home loan portfolio, the total book was worth $423 billion in December 16. They added $53 billion of loans in the past 6 months, with an value of $311,000 and at a serviceability buffer of 2.25%. 89% were variable rate loans. 37% were investor loans (up from 33% in the prior 6 months) and 43% originated via brokers, down from 46% in June 16, reflecting a 13% rise in branch application. 40% were interest only loans, up from 38% in the previous period.

They said 77% of customers are paying in advance by 35 months on average, but this includes offset facilities. Mortgage offset balances were up 19% in 1H17 to $36 billion.

In terms of underwriting criteria they use the following parameters:

- Higher of customer rate plus 2.25% or minimum floor rate (RBS: 7.25% pa, Bankwest: 7.35% pa)

- 80% cap on less certain income sources (e.g. rent, bonuses etc.)

- Maximum LVR of 95% for all loans (For Bankwest, maximum LVR excludes any capitalised mortgage insurance.)

- Lenders’ Mortgage Insurance (LMI) for higher risk loans, including high LVR loans

- Limits on investor income allowances e.g. RBS restrict the use of negative gearing where LVR>90%

- Buffer applied to existing mortgage repayments

- Interest only loans assessed on principal and interest basis

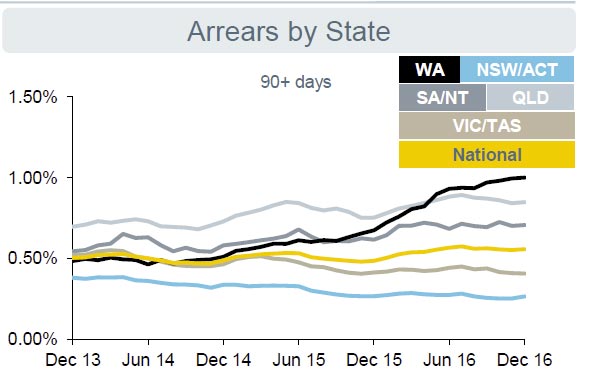

Mortgage arrears (90 day+) are highest in WA, at 1% thanks to the mining downturn. WA mining towns are 1% of portfolio. Portfolio is running at 0.53%.

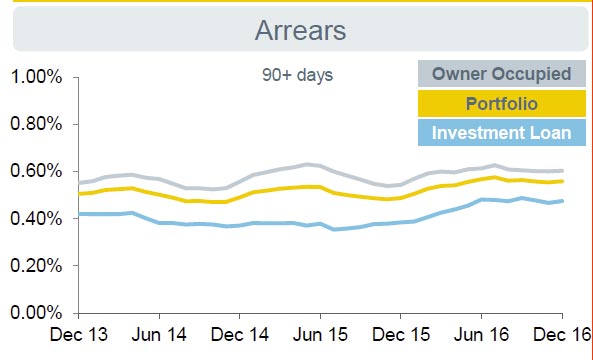

Investment mortgage arrears are running at a lower default rate, despite differential pricing, with a skew towards higher income households.

Investment mortgage arrears are running at a lower default rate, despite differential pricing, with a skew towards higher income households.

CBA says housing fundamentals suggest slower growth ahead:

CBA says housing fundamentals suggest slower growth ahead:

- Population growth has slowed as net migration eased. The slowing is concentrated in WA and Qld. Growth in NSW and Vic remains robust

- Housing supply is now running ahead of housing demand, any backlog has now been met.

- The record residential construction boom has lifted employment and related parts of retail like hardware, furnishings and white goods. But leading indicators have peaked.

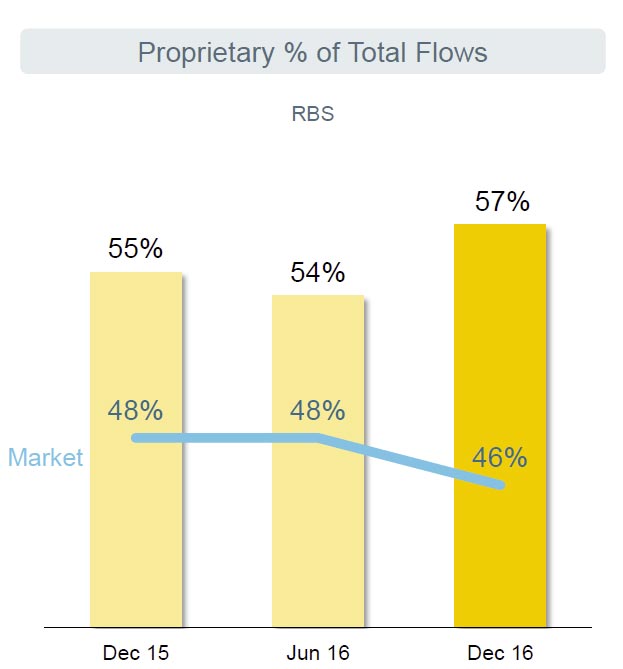

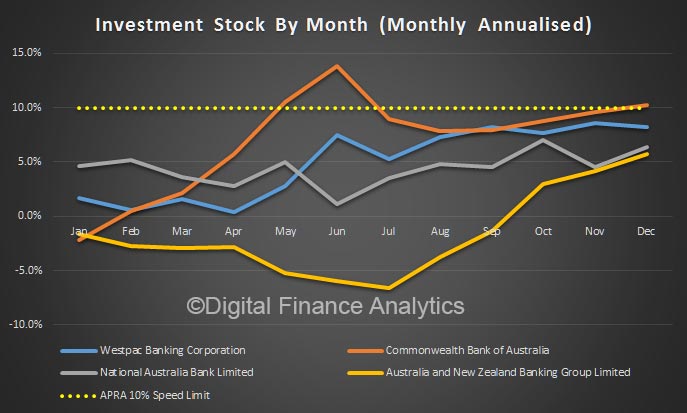

They say they are serious on the 10% benchmark for investor loans and have not exceeded the APRA speed limit.

They say households would be vulnerable to a fall in asset values and/or a rise in interest rates and unemployment though low interest rates have allowed some pre-payments and net worth has improved thanks to household asset growth.

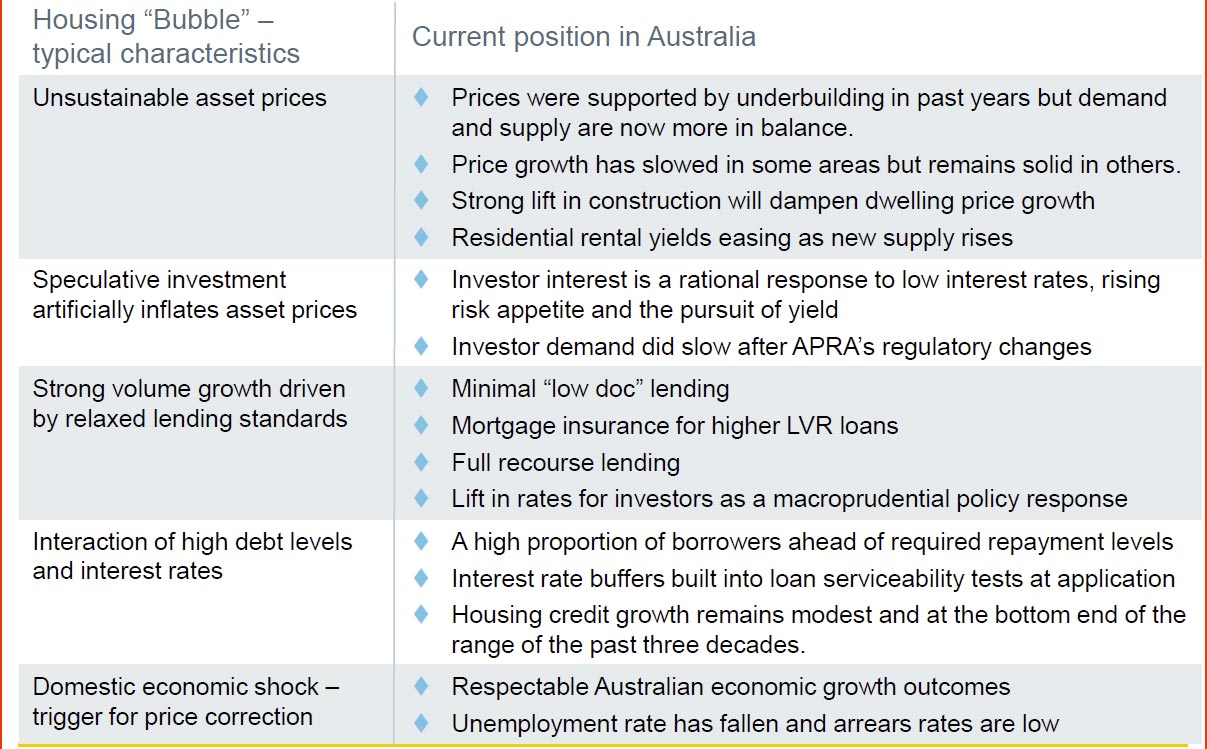

They says the typical housing bubble factors not evident in Australia:

This change relates only to investment home loans and is effective immediately. There has been no change for owner-occupier home loans.

This change relates only to investment home loans and is effective immediately. There has been no change for owner-occupier home loans.