If you want the real truth about housing affordability, read the latest shocking data from the Demographia report, just released.

http://www.demographia.com/

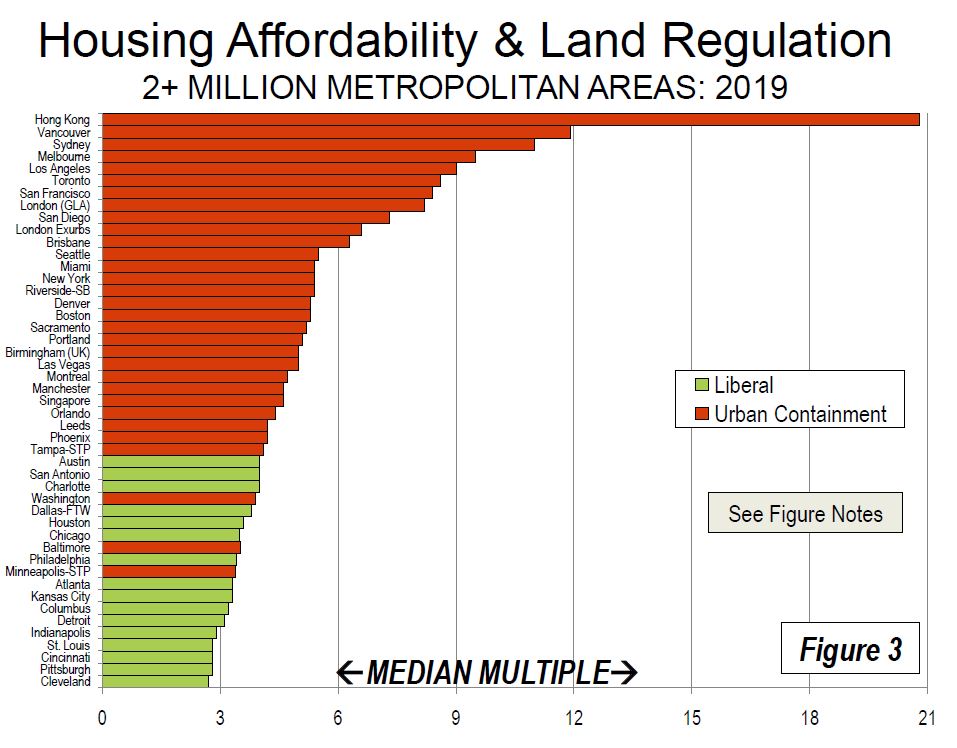

Housing affordability in 2021 is considerably worse than before, with five times as many markets at 10.0 median multiples or higher than just a decade ago. The least affordable market is Hong Kong, with a median multiple of 23.2, followed by Sydney at 15.3, Vancouver at 13.3, San Jose at 12.6 and Melbourne at 12.1. Another 46 markets are rated severely unaffordable, with median multiples (price-to-income ratios) of 5.1 or higher. Just three decades ago, nearly all of the 92 major markets covered had median multiples near 3.0 or below. The pandemic has created a “demand shock” as households move to houses with more space (inside and in yards or gardens). This has been evident in markets with overly restrictive land use regulation (especially urban containment), and worsened by the inability of home builders in well functioning markets meet the unprecedented increase in demand. The most affordable market is Pittsburgh, with a median multiple of 2.7, followed by Oklahoma City and Rochester at 3.3, with Edmonton and St. Louis at 3.6.

Go to the Walk The World Universe at https://walktheworld.com.au/

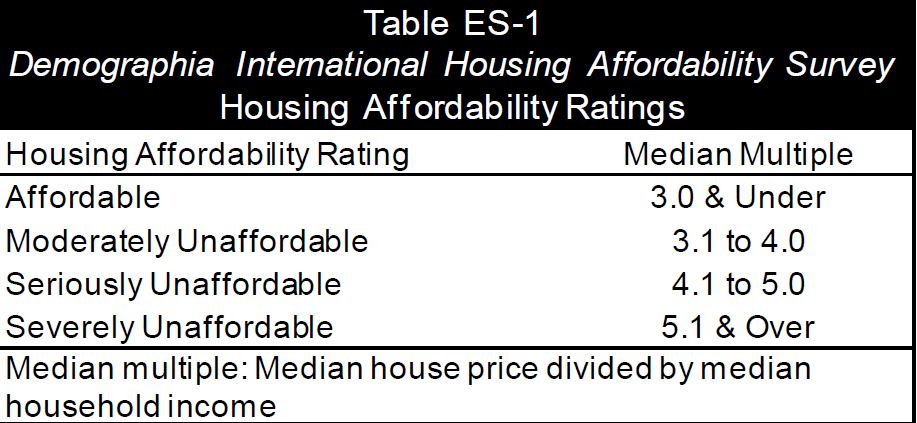

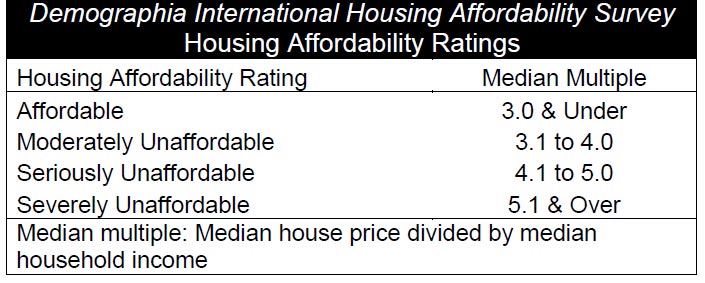

Their methodology is quite specific and allows comparisons to be made across multiple centres, and over time. Any centre scoring above 5 is judged as severely unaffordable.

I have to say I get pretty tired of some who dismiss their approach as distorting the true picture on the basis that averages mask. True I am cautious of averages generally, but it is consistently applied in my book and so makes an important contribution to understanding the relative affordability across many countries, including Australia and New Zealand. And the news is not good at all….

They also run two sets of results, the first is more major centres, and the other is the full set of the results. Across the major housing markets they conclude that all five in Australia are severely affordably (again), as is Auckland in New Zealand.

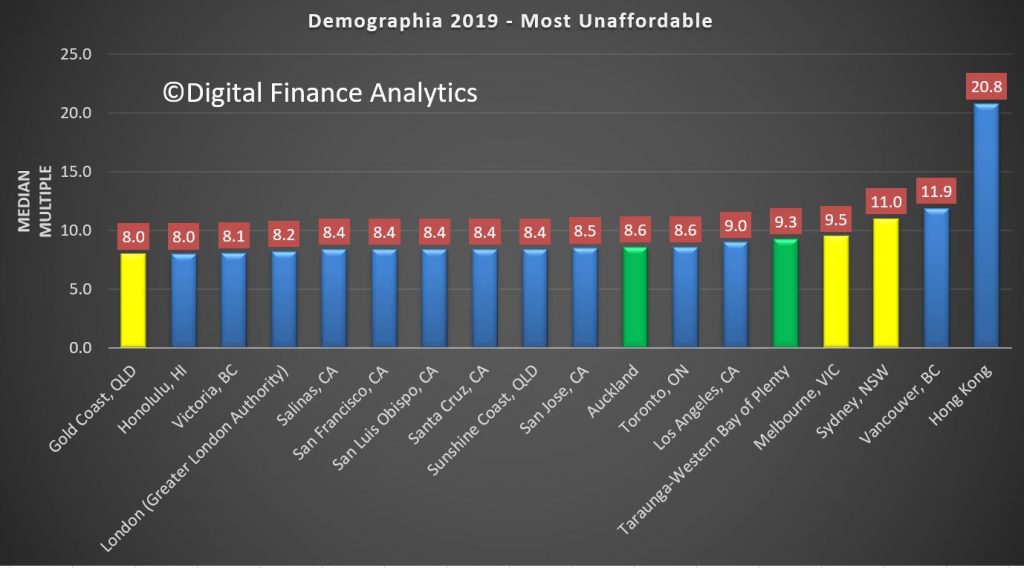

The least affordable areas include Hong Kong at 20.8, Vancouver at 11.9, Sydney at 11.0, Melbourne at 9.5, Bay of Plenty (NZ) at 9.3, LA at 9, Toronto Canada 8.6 and Auckland also at 8.6

On the other hand, in all markets, 22 out of 23 markets are unaffordable in Australia, and ALL of New Zealand’s Markets are unaffordable.

They also show the deterioration in affordability is significant is every market, but with New Zealand and Australia leading the way, with price to income ratios becoming adverse, thanks to issues of land supply (their particular thematic) and over generous lending (DFA’s thesis) of the underlying reason.

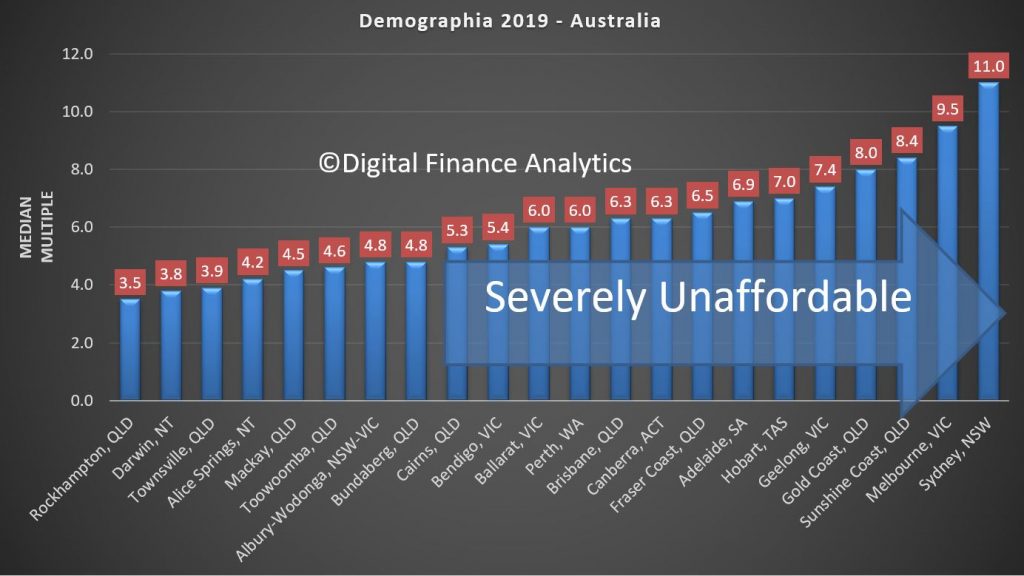

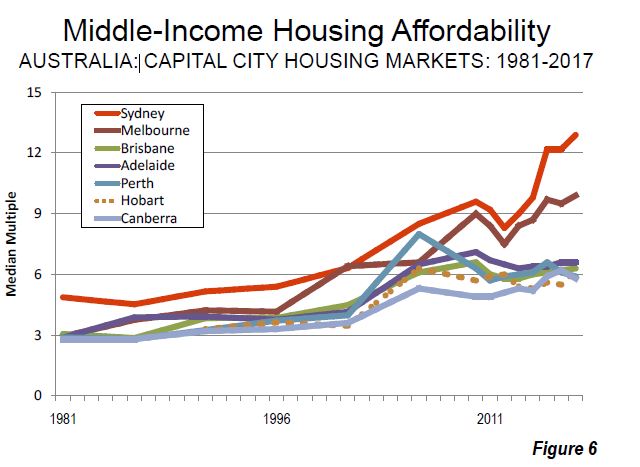

Looking at Australia, the least affordable regions are Sydney, Melbourne, Sunshine Coast, Gold Coast, Geelong, Hobart, Adelaide, Fraser Coast in QLD and Canberra, followed by Brisbane, Perth, Ballarat, and Cairns. They are all above the 5.0 affordability benchmark. Frankly this is the bulk of the populated areas in the country – this screams to me “poor policy”.

And the trends are only improving a little thanks to price fall last year. The recent reversals in some areas will just make things worse again.

Demographia said of Australia:

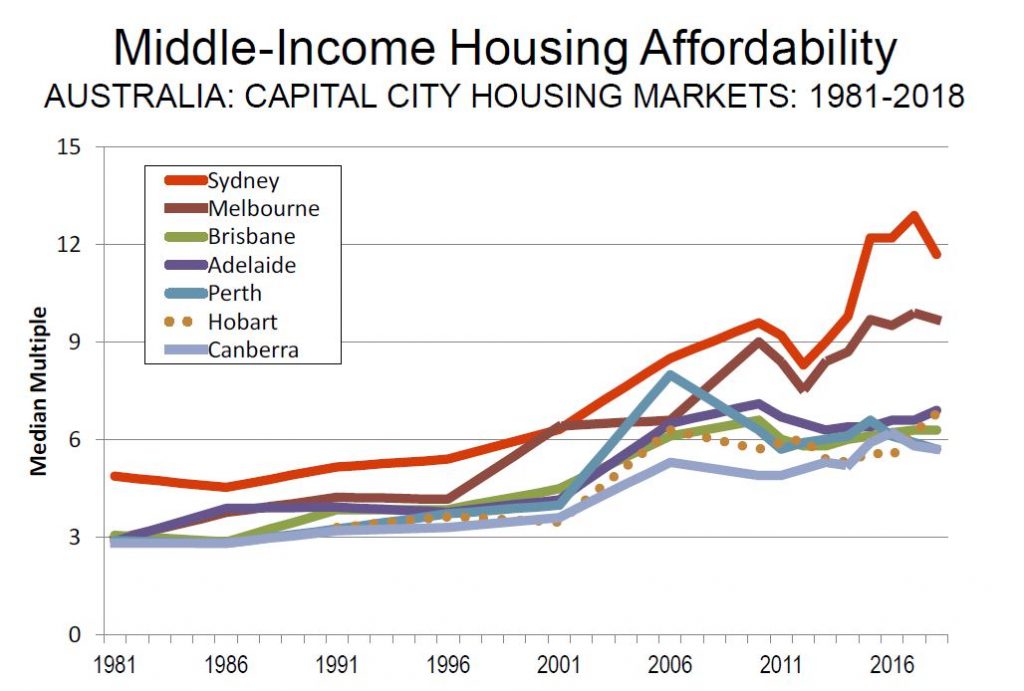

Australia’s generally unfavorable housing affordability is in significant contrast to the broad affordability that existed before implementation of urban containment (called “urban consolidation” in Australia). The price-to-income ratio in Australia was below 3.0 three decades ago

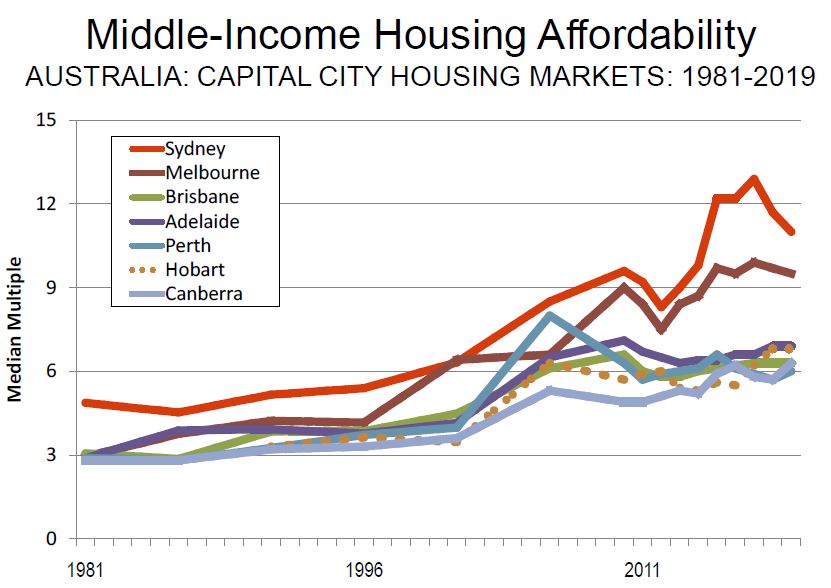

Again, as in each of the previous 15 Demographia International Housing Affordability Surveys, all of Australia’s five major housing markets are severely unaffordable. Even so, housing remains severely unaffordable in all of the major markets, and by a substantial margin in Sydney and Melbourne. Despite what has been called the largest Sydney price reduction in 35 years, house prices relative to incomes are more than double the rate of the early 1980s. In Sydney and Melbourne, median income households need at least three years’ more income to pay for the median priced house than in 2004, when the first Demographia Survey was published.

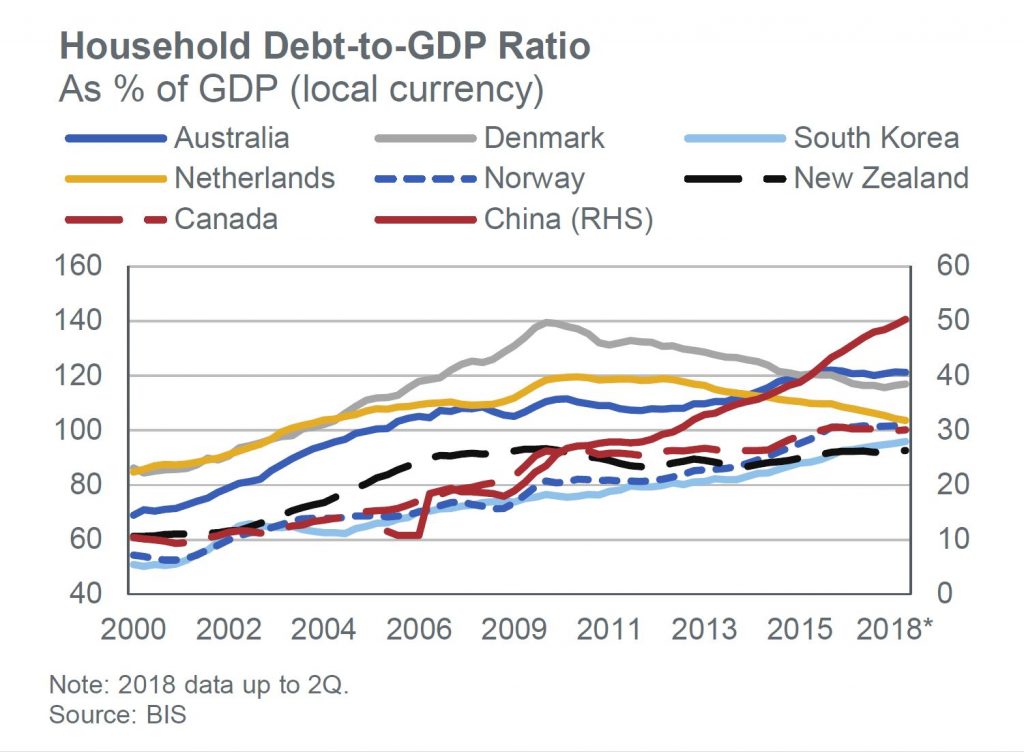

OECD expressed the following assessment of the Australian housing market (December 2018): “Australia’s housing market is a source of vulnerability. Prices have more than doubled in real terms since the early 2000s and household debt has surged. The market has started to cool over the last year, with prices falling most notably in Melbourne and Sydney. So far, data point to a soft landing without substantial consequence for the overall economy. Nevertheless, risk of a hard landing remains.”

Sydney is again Australia’s least affordable market, with a Median Multiple of 11.0, and ranks third least affordable overall, trailing Hong Kong and Vancouver. Melbourne has a Median Multiple of 9.5 and is the fourth least affordable major housing market internationally. Only Hong Kong, Vancouver, and Sydney are less affordable than Melbourne. Adelaide has a severely unaffordable 6.9 Median Multiple and is the 14th least affordable of the 92. Brisbane has a Median Multiple is 6.3 and is ranked 17th least affordable, while Perth, with a Median Multiple of 6.0 is the 19th least affordable major housing market in this year’s Demographia Survey.

Overall, Australia’s housing markets have a severely unaffordable Median Multiple of 5.9. There is only one affordable market, Gladstone, Queensland, with a Median Multiple of 2.8. Overall 14 markets in Australia are rated severely unaffordable. The least affordable are the Sunshine Coast, Queensland (8.4) and the Gold Coast, Queensland (8.0).

Australia’s high house prices have increased the cost and demand for subsidized housing. The Australian Housing and Urban Research Institute estimated that “current housing need in Australia to be 1.3 million households,” and expected the need to worsen. A Parliamentary briefing book found that “ …the stock of social housing is not increasing at a rate sufficient to keep up with demand, and waiting lists for social housing remain long. ”

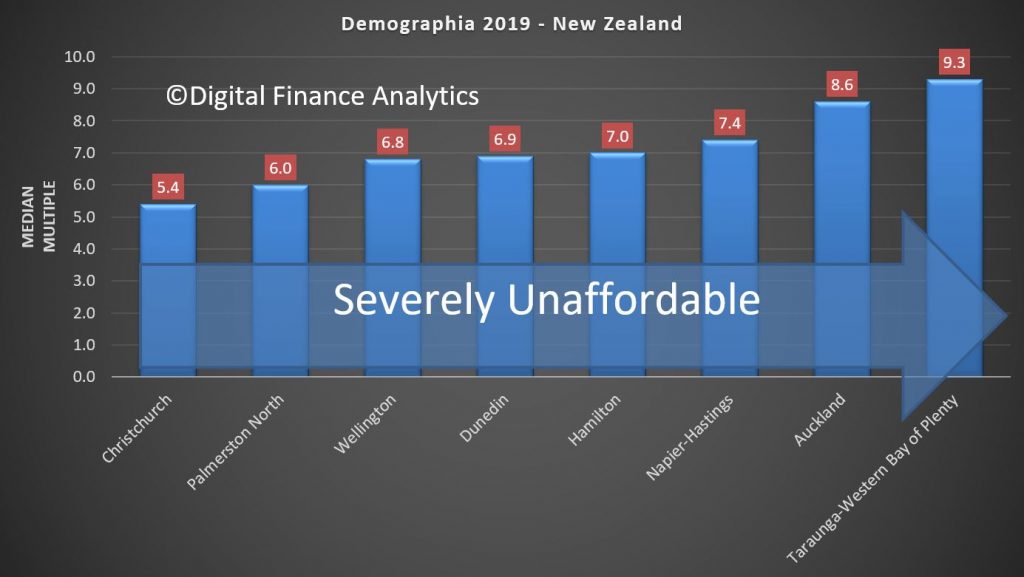

In New Zealand, all markets, including Auckland, Christchurch and Wellington are unaffordable.

The trends are also showing affordability remains a strategic issue.

Demographia says

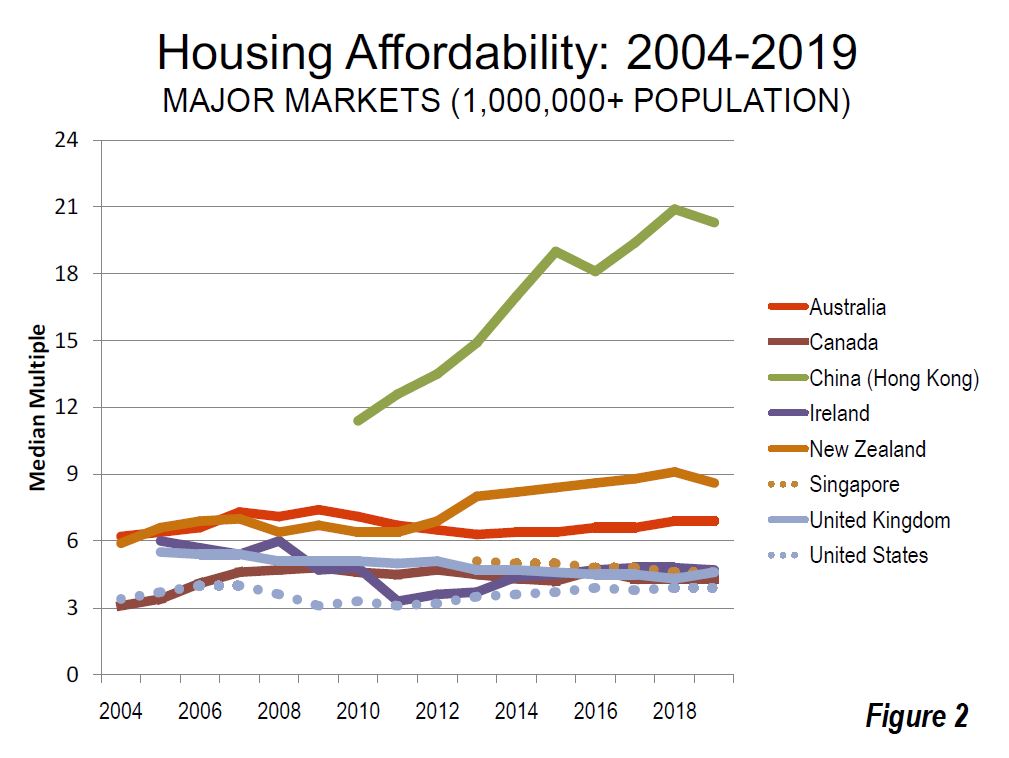

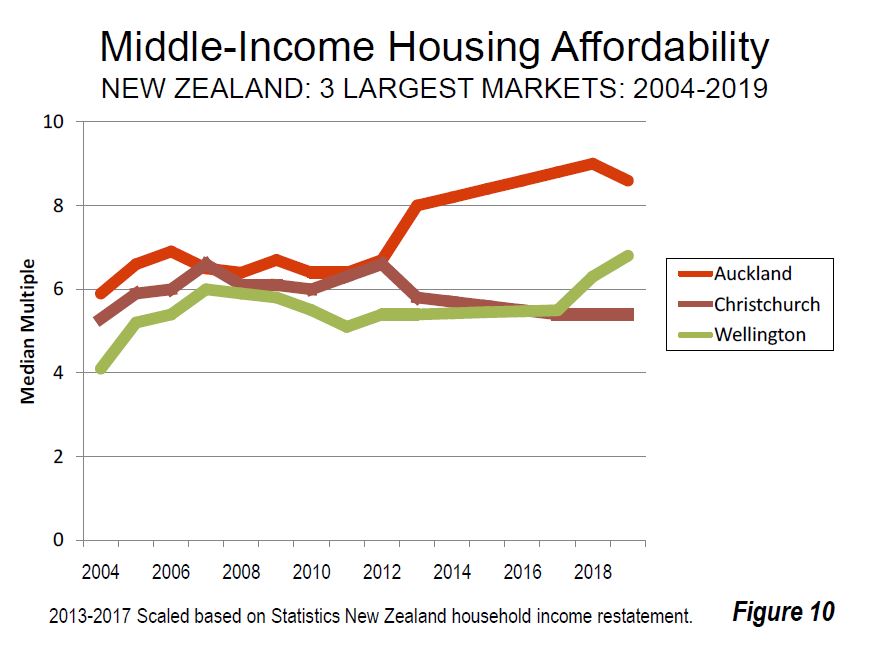

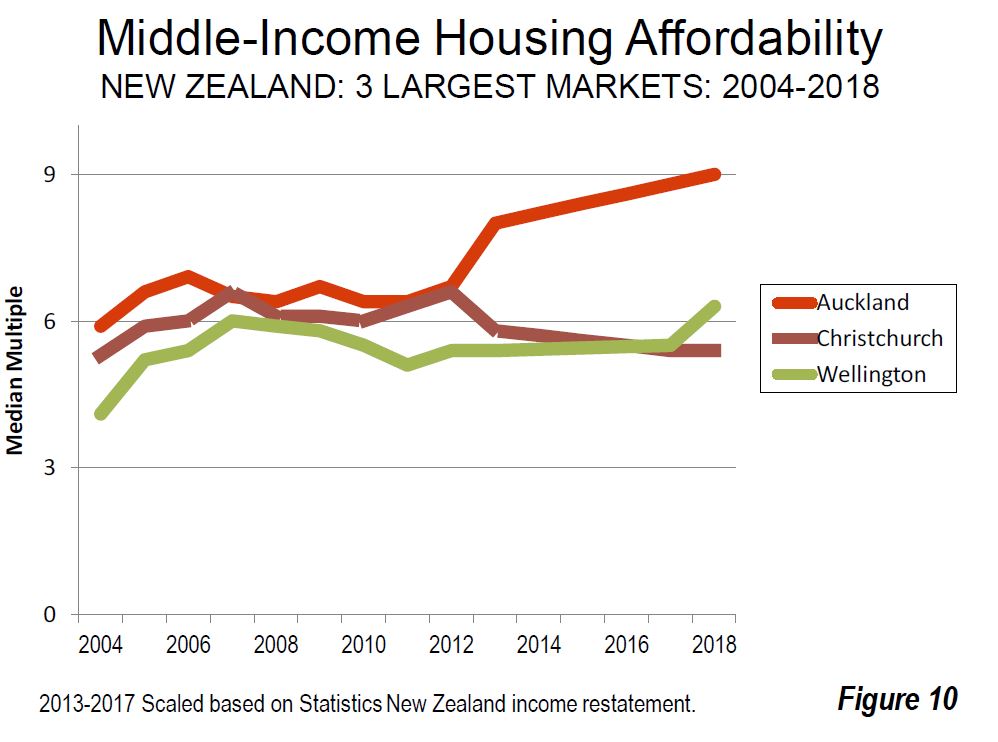

In New Zealand, as in Australia, housing had been affordable until approximately a quarter century ago. However, urban containment policies were adopted across the country, and consistent with the international experience, housing became severely unaffordable in all three of New Zealand’s largest housing markets, Auckland, Christchurch and Wellington (Figure 10). New Zealand’s price-to-income ratio was below 3.0 in the early 1990s.

Recent New Zealand Median Multiple trends have been influenced by government restatement of median income data. Auckland, New Zealand’s only major housing market has a severely unaffordable 8.6 Median Multiple. This is an improvement from 9.0 in 2018.

Even so, Auckland’s housing affordability has deteriorated from a Median Multiple of 5.9 in the first Demographia Survey (2004), thus adding nearly three years in pre-tax median household income to the house prices.

Auckland is the sixth least affordable among the 92 major housing markets, and has been severely unaffordable in all 16 Demographia International Housing Affordability Surveys. New Zealand’s’ second and third largest markets have experienced significantly different housing affordability trends over the last decade. Second largest Christchurch has a Median Multiple of 5.4, an improvement of 0.7 points from the 6th annual Demographia International Housing Affordability Survey.

Third largest Wellington has a Median Multiple of 6.8, a deterioration of 1.2 points over the past decade (Figure 10).

New Zealand’s middle-income housing crisis has strained government low-income housing budgets. Emergency aid has been increased to accommodate some low-income households in motels and waiting lists have been growing.

Housing affordability remains an issue of considerable public concern in New Zealand. The latest IPSOS New Zealand Issues Monitor (November 2019), with 62 percent respondents believing that they cannot afford to purchase a house in their own market. Housing affordability has been a principal issue from the time of the lead – up to the 2008 election and Parliaments 2007-8 Commerce Committee Housing Affordability Inquiry, chaired by the National Party’s Hon. Gerry Brownlee. National’s then Housing Spokesman and later Minister Hon. Phil Heatley toured the United States and United Kingdom prior to the election to study housing.

The Labour Party led coalition government’s Urban Growth agenda calls for intensified residential development, both greenfield and infill. This includes the abolishment of the Auckland urban containment boundary.

The government is also proceeding with plans to reform infrastructure finance to rely on debt to be serviced by residents of new developments, rather than public expenditures. During the December 1st Reading of the Infrastructure Funding and Financing Bill , Urban Development Minister Twyford acknowledged the broad political support for the Bill. Just prior to this, the Urban Development Bill was introduced in Parliament.

Twyford addressed the Government Economics Network Conference in December, reiterating the government’s commitment to improving housing affordability. “The argument I want to make to you is that generations of urban land use policy have lacked a decent grounding in economics. The consequences of that have been disastrous. And if we want to turn it around it is going to take bold reform and policies informed by an understanding of urban spatial economics”.

The final point they make is that price is directly linked to control of land supply. Markets, like Australia and New Zealand, where land releases are controlled and rationed help to explain the rising prices and falling affordability. And this of course despite falling interest rates.

This is one right royal mess, and the social and economic consequences will resonate down the years. housing affordability sucks.

The 15th edition of the annual Demographia Internal Housing Affordability Survey has been released. Once again it shows that Australia and New Zealand property is unaffordable. Globally there were 26 severely unaffordable major housing markets in 2018. As normal they argue for planning reforms to release land, but do not consider credit availability, the strongest lever to affordability!

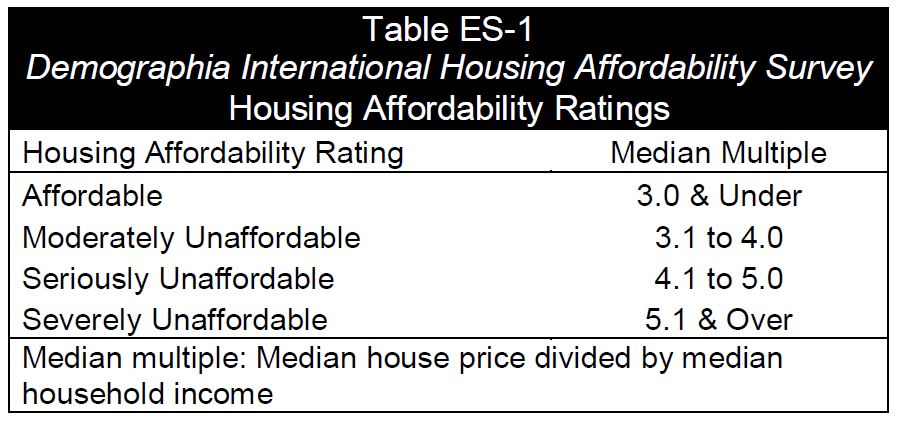

The Demographia International Housing Affordability Survey rates housing affordability using the “Median Multiple”, average house price divided by average household income or Price- Income Ratio (PIR). In the 2019 Affordability Survey covering 90 cities of more than one million people, PIR values range from 2.6 in Pittsburgh, PA and Rochester, NY to 20.9 in Hong Kong!

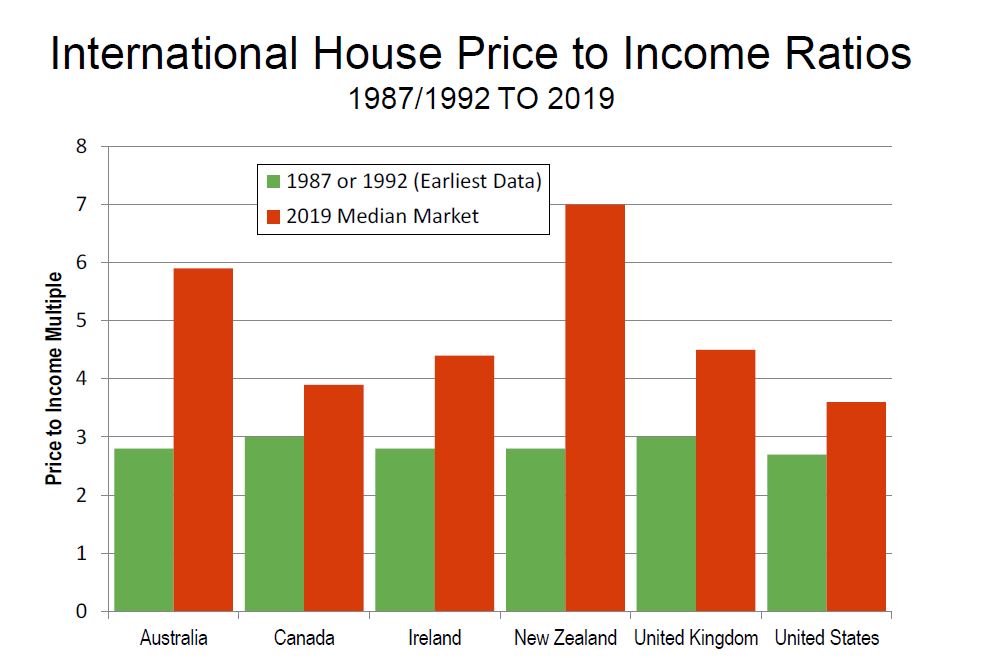

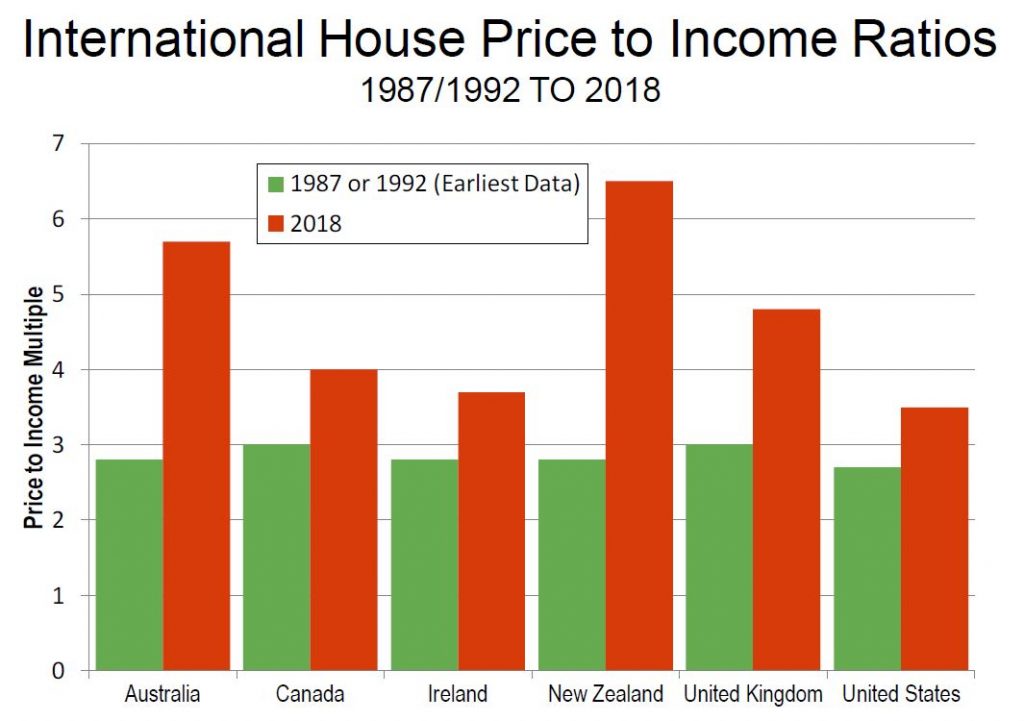

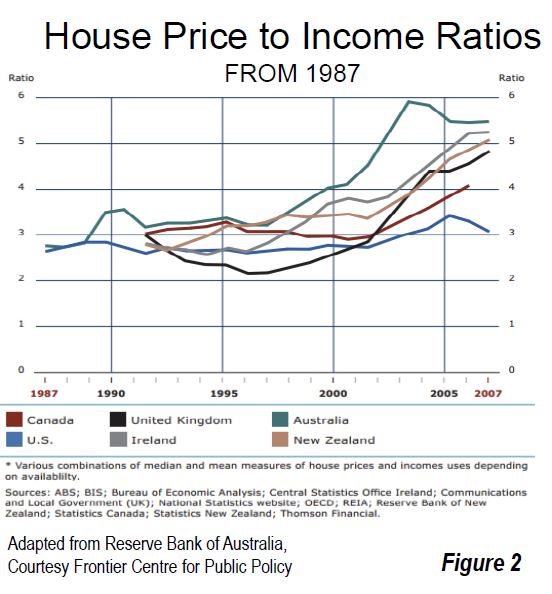

Available data shows that house costs have generally risen at a rate similar to that of household incomes until comparatively recently. This is consistent with cost trends among other basic necessities, such as personal transport, food and clothing. In some metropolitan markets house prices have doubled, tripled or even quadrupled relative to household incomes. Historically, the Median Multiple has been remarkably similar among six surveyed nations, with median house prices from 2.0 to 3.0 times median household incomes (Australia, Canada, Ireland, New Zealand, the United Kingdom and the United States). Housing affordability remained generally within this range until the late 1980s or late 1990s in each of these nations.

In recent decades, house prices have escalated far above household incomes in many parts of the world. [This coincides with the deregulation of the financial markets, and more recently QE and ultra low interest rates]

The report says that many prosperous cities consider ever increasing housing prices as an unavoidable side-effect of their economic success. But the Survey conducted by Wendell Cox and Hugh Pavletich demonstrates that some cities can be economically successful and avoid over-charging households for their housing consumption. Australia is not among them, so why do some cities manage to conciliate economic growth and housing affordability while others see their PIR number increases years after years?

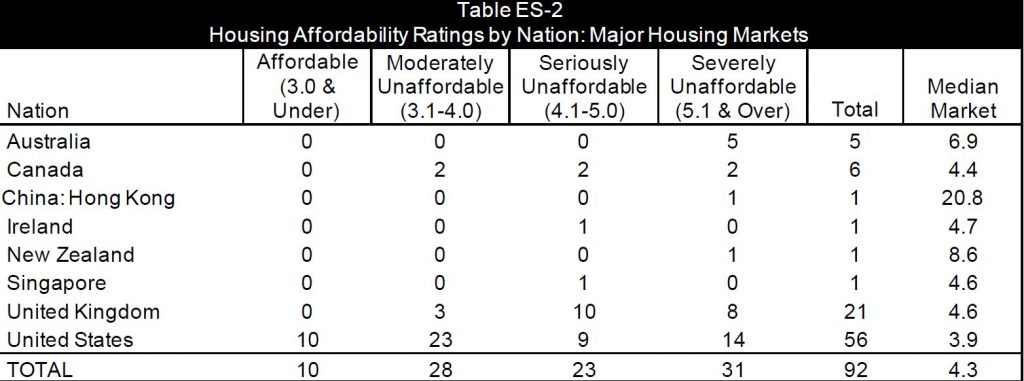

The severely unaffordable major markets include all in Australia (5), New Zealand (1) and China (1). Two of Canada’s six markets are severely unaffordable. Seven of the 21 major markets in the United Kingdom, and 13 of the 55 major markets in the United States are severely unaffordable.

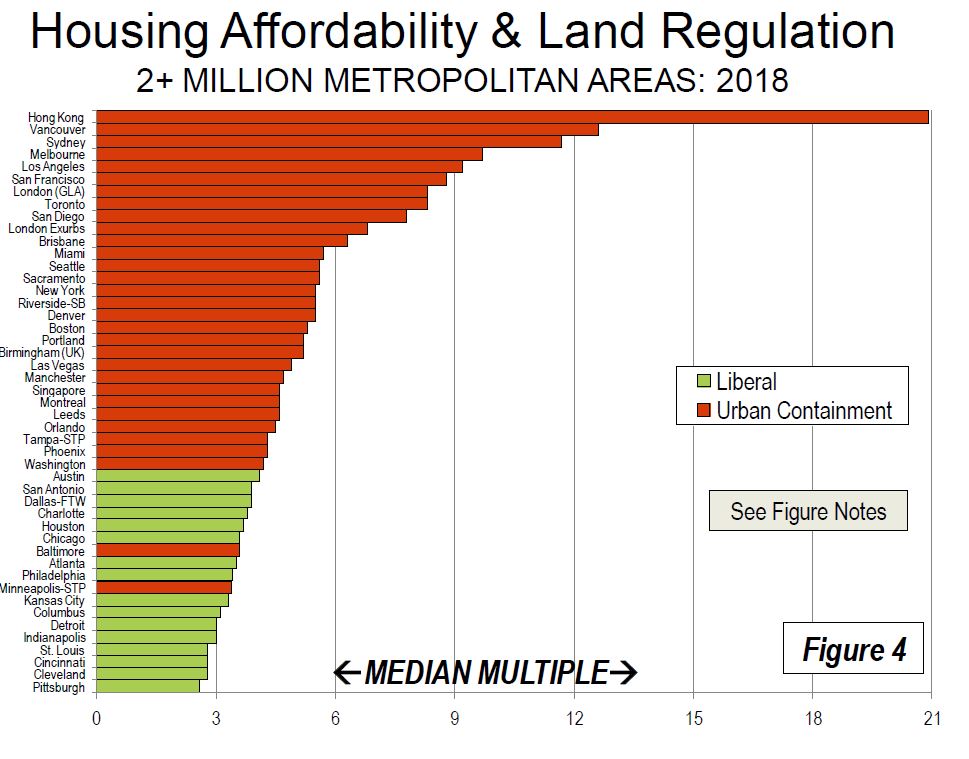

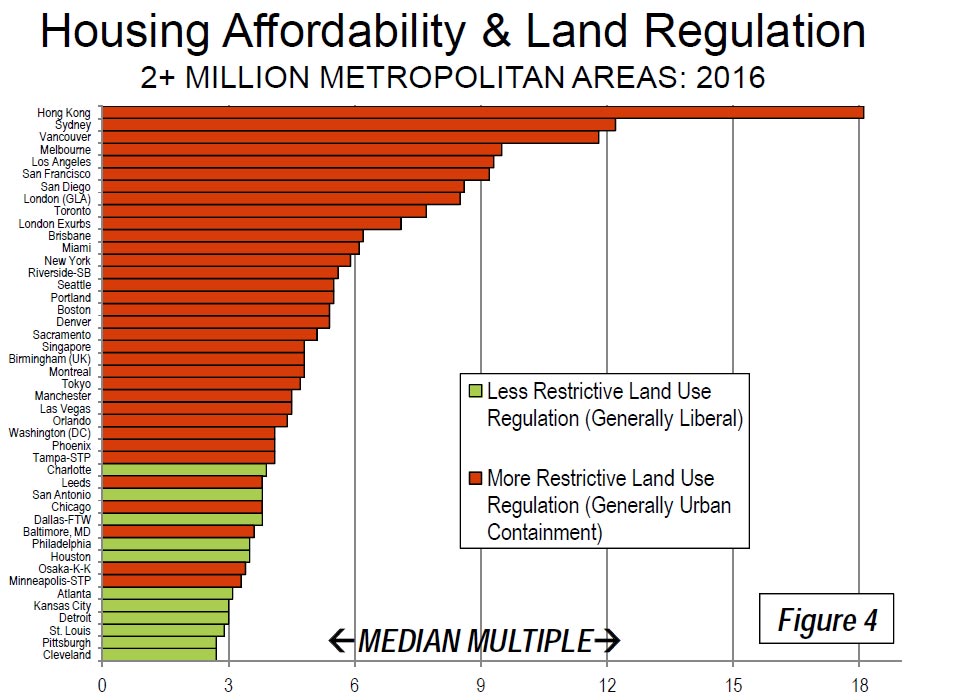

There are 26 severely unaffordable major housing markets in 2018. Again, Hong Kong is the least affordable, with a Median Multiple of 20.9 up from 19.4 last year. Vancouver has replaced Sydney as the second least affordable, with a Median Multiple of 12.6. With slightly declining house prices, Sydney’s Median Multiple dropped to 11.7. Melbourne (9.7), San Jose (9.4), Los Angeles (9.2) and Auckland (9.0) were also among the least affordable. San Francisco (8.8), Honolulu (8.6), as well as London (Greater London Authority) and Toronto (both 8.3) were also among the 10 least affordable major markets.

An already high or increasing Price-Income Ratio (PIR) should immediately signal to urban managers that they should take urgent correcting action after conducting a detailed diagnosis that would explain the high PIR figure. The Affordability Survey should be similar to the periodic health check-up taken by an individual: an abnormally high blood pressure indicates that urgent correcting steps should be taken.

Virtually all of the severely unaffordable major markets have urban containment.

Among the 79 severely unaffordable markets, 28 are in the United States, 17 in Canada, 16 in Australia, 11, six in New Zealand and one in China. Among the 10 least affordable housing markets, seven are major housing markets. s least affordable 10 also includes California’s Santa Cruz, at 9.6 and Tauranga-Western Bay of Plenty in New Zealand, at 9.1. All of the other least affordable metropolitan areas were major markets.

In Australia, housing affordability remains severely unaffordable in all of the major markets, and by a substantial margin in Sydney and Melbourne. Despite what has been called the largest Sydney price reduction in 35 years, house prices relative to incomes are more than double the rate of the early 1980s. In Sydney and Melbourne, median income households need at least three years’ more income to pay for the median priced house than in 2004, when the first Survey was published.

Major Markets: Sydney is again Australia’s least affordable market, with a Median Multiple of 11.7, and ranks third worst overall, trailing Hong Kong. Melbourne has a Median Multiple of 9.7 and is the fourth least affordable major housing market internationally. Only Hong Kong, Vancouver, and Sydney are less affordable than Melbourne. Adelaide has a severely unaffordable 6.9 Median Multiple and is the 16th least affordable of the 91 major markets. Brisbane has a Median Multiple is 6.3 and is ranked 18th least affordable, while Perth, with a Median Multiple of 5.7 is the 24th least affordable major housing market in this year’s Survey.

Other Housing Markets: Overall, Australia’s housing markets have a severely unaffordable Median Multiple of 5.9. The most affordable markets are moderately affordable, Gladstone, Queensland at 3.2 and Rockhampton, Queensland at 3.9. There are no affordable or moderately affordable markets in Australia. Overall 16 markets in Australia are rated severely unaffordable. The least affordable are the Sunshine Coast, Queensland (8.7) and the Gold Coast, Queensland (8.4).

Historical Context: Australia’s generally unfavorable housing affordability is in significant contrast to the broad affordability that existed before implementation of urban containment (called “urban consolidation” in Australia). The price-to-income ratio in Australia was below 3.0 in the late 1980s. All of Australia’s major markets have urban containment policy and all have severely unaffordable housing.

New Zealand’s housing affordability has a severely unaffordable Median Multiple of 6.5. Recent Median Multiple trends have been influenced by government restatement of median income data.

Major Housing Market: Auckland, New Zealand’s only major housing market has a severely unaffordable 9.0 Median Multiple. Housing affordability has deteriorated from a Median Multiple of 5.9 in the first Survey (2004), thus adding the equivalent of three years in pre-tax median household income to the house prices. Over the past year, Auckland’s house prices have been stable, with the Median Multiple increase resulting from the household income restatement described above. Auckland is the seventh least affordable among the 91 major housing markets, and has been severely unaffordable in all 15 Demographia International Housing Affordability Surveys.

Other Housing Markets: There is severely unaffordable housing in the two largest markets outside Auckland. Christchurch has a Median Multiple of 5.4, while Wellington is at 6.3.

Housing Affordability and Public Policy: Outside Singapore, New Zealand is the only nation in the Survey that emphasizing public policy priority to restore and maintain middle-income housing affordability. In New Zealand, as in Australia, housing had been affordable until approximately a quarter century ago. However, urban containment policies were adopted across the country, and consistent with the international experience, housing became severely unaffordable in all three of New Zealand’s largest housing markets, Auckland, Christchurch and Wellington.

Meanwhile, public opinion placed the issue of housing affordability to the top of the policy agenda in the last three national elections. That concern continues to be dominant according to the latest IPSOS New Zealand Issues Monitor (October 2018), with 45 percent saying that “Housing/Price of Housing” is the issue of greatest concern. Poll respondents were asked to identify the three most important issues, and the cost of living rated third, which is to be expected given the enormous influence of housing costs on the financial health of households. The new Labour Party led coalition government unveiled a focused housing affordability program, intending to increase the housing supply throughout Auckland, including both urban fringe and infill development. The Labour Party’s Urban Growth agenda calls for intensified residential development, both greenfield and infill. The Auckland urban containment boundary is to be abolished. Recently, the government and the city of Auckland agreed to establish a non-government debt financing mechanism to facilitate development of a 9,000 home greenfield development. The government intends to establish an Urban Development Authority, which would provide means for communities and developers to finance infrastructure for new housing development.

In his Introduction: Avoiding Dubious Urban Policies to this Survey, former World Bank principal urban planner Alain Bertaud says that “After the government has successfully passed these reforms, the international community will watch with great interest the impact it will have on Auckland’s PIR (Median multiple) in the next few years. It is hoped that the example of Auckland will create a blueprint that could be used in other high PIR cities.”

These developments build on other recent developments, especially a Productivity Commission of New Zealand report, which found that land use authorities have a responsibility to provide “capacity to house a growing population while delivering a choice of quality, affordable dwellings of the type demanded ….” Consistent with that finding, the Productivity Commission proposed a measure that would automatically expand the supply of greenfield land when housing affordability targets are not met. The Commission said, “Where large discontinuities emerge between the price of land that can be developed for housing and land that cannot be developed, this is indicative of the inadequacy of development capacity being supplied within the city.” The Productivity Commission expansion of greenfield land for development where the difference between land prices on either side of an urban containment boundary become too great.

Here are the top housing markets listed by their unaffordability.

The report highlights three myths which tend to limit policy responses, namely:

Myth #1: planners know how to allocate land equitably through the design of increasingly complex zoning regulations while ignoring price signals.

Myth #2: Regulators can mandate the creations of new affordable housing units by obliging private developers to provide a share (usually 20%) of the housing units they build at prices fixed by the government below market; regulators call these “affordable housing units.”

Myth #3: The compact city fallacy. A city can accommodate increasing income and population through densification of the existing built-up area; expansion into greenfield would result in “sprawl.”

The report says that by severely restricting or even prohibiting expansion to accommodate larger population, urban containment has virtually destroyed the competitive market for land in many urban areas, driving house prices up relative to incomes.

We agree that land supply is one important issue but the report is silent on the most powerful lever of home prices, credit availability. Our own research suggests that more credit leads to higher prices, and the reverse is also true. There are correlations with the household debt to GDP ratios.

In addition there is an “undersupply myth”. According to the latest census in Australia, from 2016, 11.2% of residential properties are unoccupied, which equates to 1,039,874 residences. We also saw in Joe Wilkes’ recent reports from Auckland, that supply is not an issue at this time in New Zealand.

Finally, some will criticise the index method they use in their surveys, but we think the consistently applied approach shows real trends and real issues.

In fact, the truth is housing affordability is a result of the complex interplay between supply and demand, planning and credit, and to that end the Demographia survey is a helpful tool to diagnose the issues we face. But planning changes alone will not solve the issue. The greatest of these is credit.

Our latest Video Blog discusses the Demographia Housing Affordability Report with specific reference to Australia.

The latest 14th edition of the Annual Demographia International Housing Affordability Survey: 2018, using 3Q 2017 data continues to demonstrate the fact that we have major issues here. There are no affordable or moderately affordable markets in Australia. NONE!

We discussed the latest Demographia report and housing affordability on 2GB today, with Ben Fordham. There are no affordable or moderately affordable markets in Australia. NONE! We have a structural problem.

The major markets of Australia (6.6), New Zealand (8.8) and China (19.4) are severely unaffordable. By international standards houses are big in both Australia and New Zealand but relatively unaffordable.

Using a standard methodology across geographies, the study benchmarks affordability of middle income housing, using an index on average prices and incomes – formally, Median Multiple: Median house price divided by median household income.

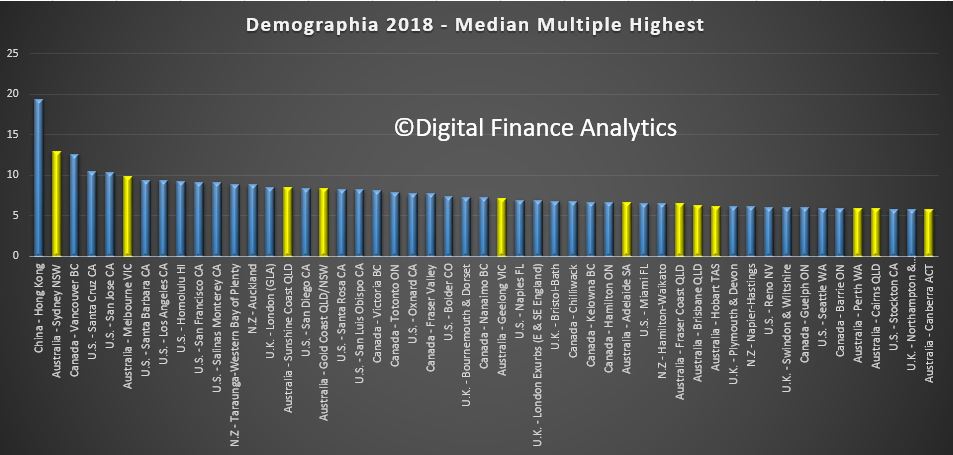

Sydney is second worst in terms of affordability after Hong Kong, with Melbourne, Sunshine Coats, Gold Coast, Geelong, Adelaide, Brisbane, Hobart, Perth, Cains and Canberra all near the top of the list. [Click on the graphic to see it larger].

In recent decades, house prices have escalated far above household incomes in many parts of the world. In some metropolitan markets house prices have doubled, tripled or even quadrupled relative to household incomes. Typically, the housing markets rated “severely unaffordable” have more

restrictive land use policy, usually “urban containment.”

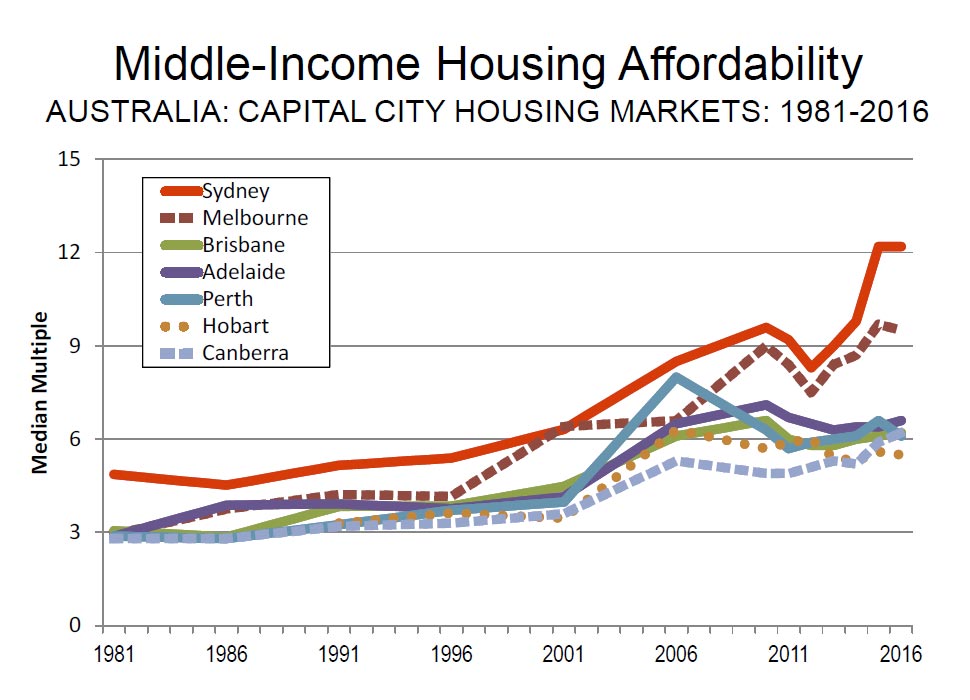

Sydney is again Australia’s least affordable market, with a Median Multiple of 12.9, and ranks second worst overall, trailing Hong Kong. Sydney’s housing affordability has worsened by the equivalent of 6.6 years in pre-tax median household income since 2001. This is a more than doubling of the Median Multiple. In contrast, Sydney’s housing affordability worsen less than one-fourth as much between 1981 and 2001.

At 12.9 Sydney’s Median Multiple is the poorest major housing affordability ever recorded by the Survey outside Hong Kong. Additionally, the UBS Global Real Estate Bubble Index rates Sydney as having the world’s fourth worst housing bubble risk (tied with Vancouver).

Melbourne has a Median Multiple of 9.9 and is the fifth least affordable major housing market internationally. Only Hong Kong, Sydney, Vancouver, and San Jose are less affordable than Melbourne. Melbourne’s Median Multiple has deteriorated from 6.3 in 2001 and under 3.0 in the early 1980s. Just since 2001, median house prices have increased the equivalent of more than three years in pre-tax median household income.

Adelaide has a severely unaffordable 6.6 Median Multiple and is the 16th least affordable of the 92 major markets. Brisbane has a Median Multiple is 6.2 and is ranked 18th least affordable, while Perth, with a Median Multiple of 5.9 is the 21st least affordable major housing market in Australia.

The report argues that:

The key to both housing affordability and an affordable standard of living is a competitive market that produces housing (including the cost of associated land) at production costs, including competitive profit margins.

None of that currently exists in Australia, with land prices sky high, linked to lack of supply (strange given the size of the country!) as well as the financialisation of property and the massive investment sector.

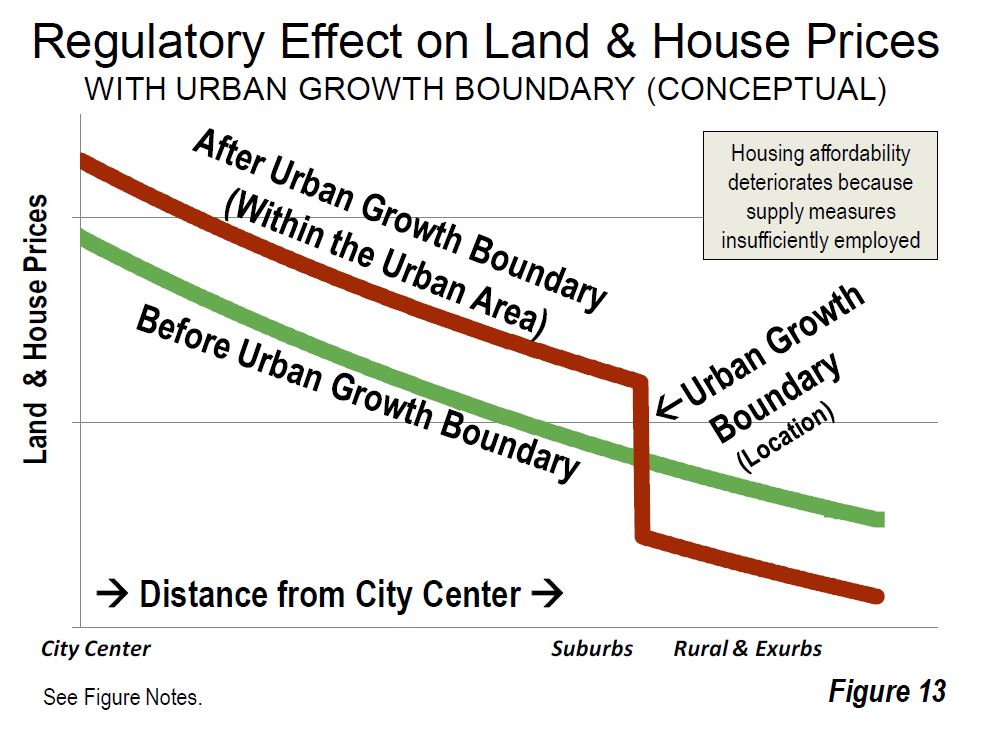

In contrast with well functioning housing markets, virtually all the severely unaffordable major housing markets covered in the Demographia International Housing Affordability Survey have restrictive land use regulation, overwhelmingly urban containment. A typical strategy for limiting or prohibiting new housing on the urban fringe an “urban growth boundary,” (UGB) which leads to (and is intended to lead to) an abrupt gap in land values.

Australia is perhaps the least densely populated major country in the world, but state governments there have contrived to drive land prices in major urban areas to very high levels, with the result that in that country housing in major state capitals has become severely unaffordable.

The 13th Annual Housing Affordability Survey – 2017 has been released by Demographia and it underscores the problem we have with affordable housing. All five of Australia’s major centres are rate “un-affordable on their scale.

The overall major housing market Median Multiple is 6.6. In 2004 (the first Survey), Sydney’s Median Multiple was 7.6, and has risen 60 percent since then.

Only Hong Kong, Sydney, Vancouver, Auckland and San Jose are less affordable than Melbourne. Adelaide has a severely unaffordable 6.6 Median Multiple and is the 16th least affordable of the 92 major markets. Brisbane has a Median Multiple is 6.2 and is ranked 18th least affordable, while Perth, with a Median Multiple of 6.1 is the 20th least affordable major housing market.

Outside of the major markets, 28 in Australia are rated severely unaffordable. The least affordable of these are Wingcaribbee, NSW (9.8), Tweed Head, NSW (9.7), Gold Coast, QLD (9.0) and Sunshine Coast, QLD (9.0).

Sydney in second place, after Hong Kong, with Melbourne also in the top 10.

Demographia’s ‘median multiple’ approach establishes a benchmark for housing affordability by linking median house prices to median household incomes. The ‘median multiple’ is not a perfect measure because it does not account for house sizes or build quality. But it is the only index that allows a quick comparison of different housing markets, and it is the best approximation of housing affordability measures we have to date.

The Median Multiple is widely used for evaluating urban markets, and has been recommended by the World Bank and the United Nations and is used by the Joint Center for Housing Studies, Harvard University. The Median Multiple and other price-to-income multiples (housing affordability multiples) are used to compare housing affordability between markets by the Organization for Economic Cooperation and Development, the International Monetary Fund, The Economist, and other organizations.

Historically, liberally regulated markets have exhibited median house prices that are three times or less that of median household incomes, for a Median Multiple of 3.0 or less.

The Survey covers 406 metropolitan housing markets (metropolitan areas) in nine countries (Australia, Canada, China, Ireland, Japan, New Zealand, Singapore, the United Kingdom and the United States) for the third quarter of 2016. A total of 92 major metropolitan markets (housing markets) — with more than 1,000,000 population — are included, including five megacities (Tokyo-Yokohama, New York, Osaka-Kobe-Kyoto, Los Angeles, and London).

There are 26 severely unaffordable major housing markets in 2016. Again, Hong Kong is the least affordable, with a Median Multiple of 18.1, down from 19.0 last year. Sydney is again second, at 12.2 (the same Median Multiple as last year). Vancouver is third least affordable, at 11.8, where house prices rose the equivalent of a full year’s household income in only a year. Auckland is fourth least affordable, at 10.0 and San Jose has a Median Multiple of 9.6. The least affordable 10 also includes Melbourne (9.5), Honolulu (9.4), Los Angeles (9.3), where house prices rose the equivalent of 14 months in household income in only 12 months. San Francisco has a Median Multiple of 9.2 and Bournemouth & Dorsett is 8.9.

Blog")