A Danish bank has dropped the hurdle below which they will charge negative interest rates on deposits.

Yes, people have to pay to hold their money at the bank.

We discuss the implications.

Digital Finance Analytics (DFA) Blog

"Intelligent Insight"

A Danish bank has dropped the hurdle below which they will charge negative interest rates on deposits.

Yes, people have to pay to hold their money at the bank.

We discuss the implications.

Jyske Bank A/S, Denmark’s second-largest listed lender, will impose negative rates on all private customers with 750,000 krone ($110,000) or more, according to Bloomberg. Until Friday, only people with roughly $1 million in surplus cash at their banks were facing a negative rate. Now, the threshold has been reduced to just over $100,000, with no guarantee it won’t go lower.

Chief Executive Officer Anders Dam said the latest Danish rate cut this month means Jyske is now “losing even more money” when it deposits excess reserves at the central bank at minus 0.75%. Dam also says it’s possible the rule will be extended to an even larger group of depositors.

Denmark’s monetary policy is designed to defend the krone’s peg to the euro. But its effect on the broader economy is being closely watched. Danes have now spent seven years with rates below zero — a world record — and Dam at Jyske says he’s bracing for another eight.

Normally, low rates encourage more household spending as it gets cheaper to borrow and less appealing to save. In Denmark, negative rates have led to a surge in mortgage refinancing, but they’ve also coincided with a record build-up of consumer deposits. And, as is the case in much of the rest of Europe, inflation is missing in action.

“Households have gotten all the benefits of negative rates so far, but now they’re starting to see the bad side of negative rates,” Nielsen said.

For consumers, it’s made more sense to keep their cash in a deposit account that paid zero, rather than invest in short-term market products at negative yields. Jyske’s decision now has implications for everything from debt levels to inflation.

But it may not just be a question of economic theory. In Germany, lawmakers have debated whether to ban banks from passing negative rates on to retail depositors. Finland’s regulator has also asked its lawyers to examine the legality of the practice. In Denmark, politicians have voiced concerns.

Perhaps is time here in Australia to mount a campaign to outlaw negative deposit rates here, and even align it to the war on cash!

In this strange new environment could it be that borrowers will be paid to take a mortgage? It could be.

In Denmark’s $495 billion mortgage-backed covered bond market, another milestone was reached on Wednesday as Nordea Bank Abp said it will start offering 20-year fixed-rate loans that charge no interest.

This is significant, as the Denmark 10-Year Government bond rate slides below minus 0.5%

The development follows an announcement earlier in the week by Jyske Bank A/S, which said it will start issuing 10-year mortgages at a coupon of minus 0.5%. Danes can also now get 30-year mortgages at 0.5%, and Nordea recently adjusted its prospectus to allow for home loans up to 30 years at negative interest rates.

“It’s never been cheaper to borrow,” Lise Nytoft Bergmann, chief analyst at Nordea’s home finance unit in Denmark, said in an email. “We expect this to contribute to driving home prices higher.”

Though good news for homeowners, Bergmann said the development is “almost eerie.”

“It’s an uncomfortable thought that there are investors who are willing to lend money for 30 years and get just 0.5% in return,” she said. “It shows how scared investors are of the current situation in the financial markets, and that they expect it to take a very long time before things improve.”

On 1 July, legislation in Denmark took effect that will trigger the inaugural issuance of Danish public housing covered bonds (almene realkreditobligationer) as a new asset class, says Moody’s.

These new covered bonds will be issued out of newly established capital centres with the sole purpose of funding mortgage loans granted to public housing companies (almen boligforening). As is the practice in the Danish covered bond market, assets serving as security for covered bonds must be segregated into independent cover pools, referred to as capital centres in mortgage banks. The Danish government guarantees in full the mortgage loans as well as the public housing covered bonds.

The law is credit positive for potential investors in public housing covered bonds because their credit risk will be lower than in existing mortgage covered bonds. Although investors in both types of covered bonds benefit from recourse to the issuing mortgage bank and a pool of good quality mortgage assets, only public housing covered bonds benefit from a state guarantee in case the issuer fails to fulfil its obligations.

Today, public housing loans benefit from a municipality’s partial guarantee of the loan, but under the new framework such loans will benefit from the federal government’s guarantee covering the full loan amount. In 2017, Danish municipalities guaranteed on average the most risky 62% of mortgage loans. Under the new model, the government will charge a guarantee commission from the mortgage banks. The mortgage banks, owing to the government’s full guarantee, will have lower capital requirements and lower over- collateralisation requirements for the covered bonds that are set in Denmark at 8% of risk-weighted assets.

Denmark’s public housing covered bonds will be issued by mortgage banks via frequently held auctions and tap sales. For the issuance of public housing covered bonds, banks shall obtain bids for purchases from Denmark’s central bank on behalf of the Danish government before the bonds are sold to others, which reduces funding execution risk for the public housing companies and the mortgage banks. According to the Danish central bank, the government will purchase DKK42.5 billion of public-sector covered bonds in 2018, corresponding to the total of new loans and refinancings of existing loans. The government will bid at a rate corresponding to the yield on government bonds.

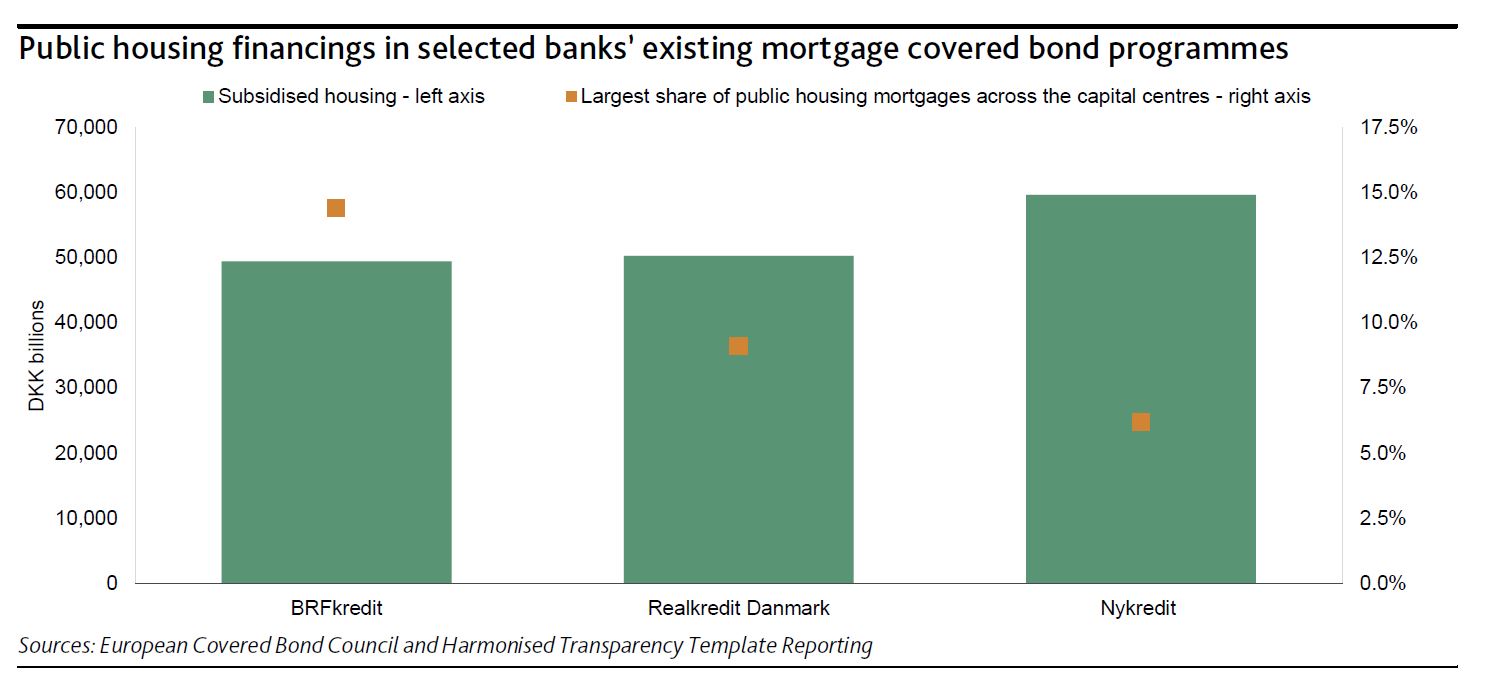

We expect a quick migration of public housing loans to the newly established capital centres in order to benefit from the government guarantees. This will lead to an increased level of prepayments and refinancings in the existing capital centres. The public housing sector has subsidised loans totalling around DKK180 billion that are largely financed by existing capital centres that issue mortgage covered bonds.

Nykredit Realkredit A/S, Realkredit Danmark A/S (part of Danske Bank) and BRFkredit A/S (part of Jyske Bank) are active lenders in this sector, each currently lending DKK50-DKK60 billion to the public housing sector. Despite the public housing loans being refinanced into the new capital centres, the risk characteristics of the capital centres will not change materially because the share of public housing loans is often small and in active capital centres does not exceed 15% as shown in the exhibit.